Nelnet Porter's Five Forces Analysis

From Overview to Strategy Blueprint

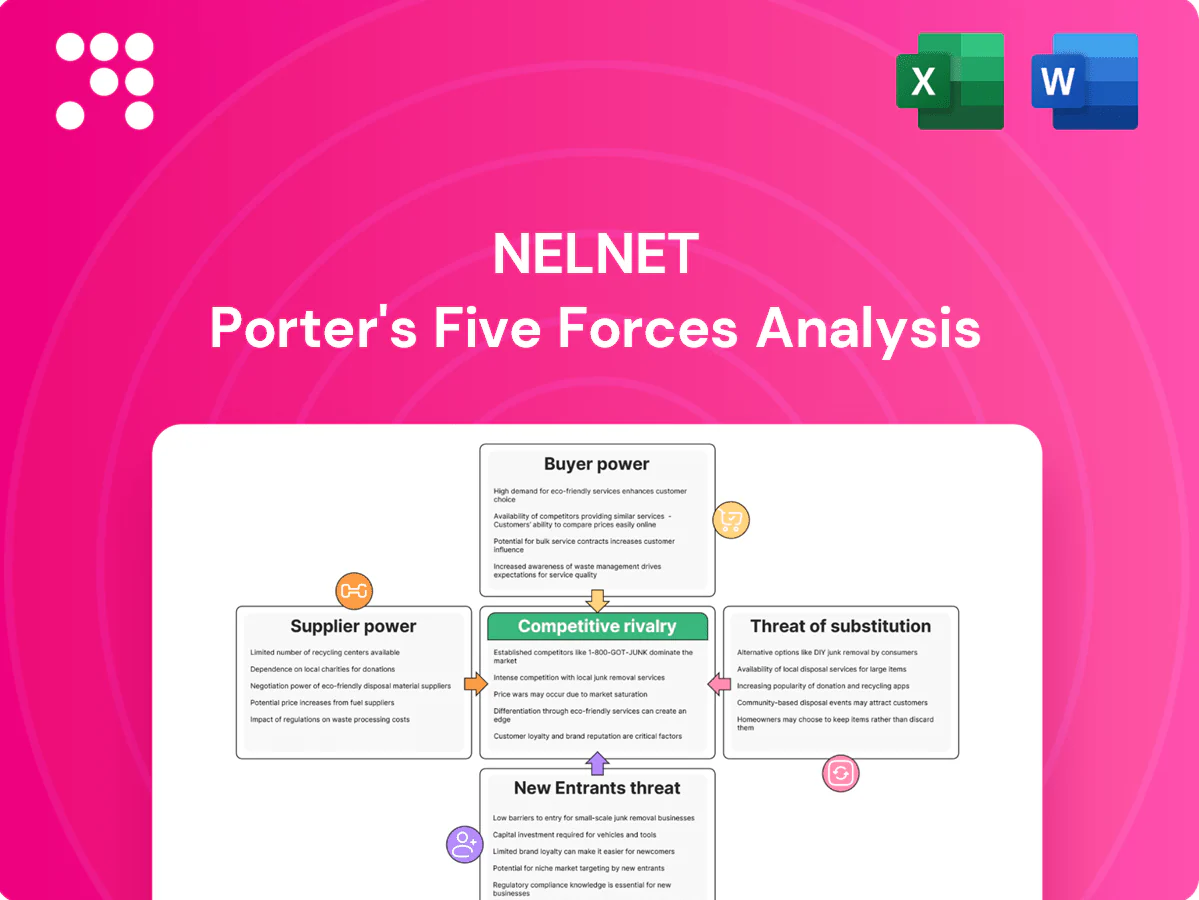

Nelnet faces moderate buyer power from institutional contracts and price-sensitive students, low supplier power, high competitive rivalry among student-loan servicers, and regulatory barriers that limit new entrants while fintech substitutes create emerging threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nelnet’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated federal contract sources

The U.S. Department of Education is the single dominant source for federally serviced loan volumes—the outstanding federal student loan portfolio was about $1.6 trillion in 2024—making its policy, data standards and platform requirements de facto supplier inputs. Changes in rules, handoffs or volume allocations by ED can quickly shift compliance and operational costs to servicers like Nelnet. This concentration gives ED supplier-like power over pricing, contract terms and implementation timelines.

Cloud and core software dependence

Nelnet’s servicing, payments and EdTech stacks depend on dominant IaaS and core processing vendors—AWS (≈32% share), Azure (≈23%) and Google Cloud (≈10%) in 2024—creating few substitutes and significant switching friction. Migrating core platforms is costly and risky, giving incumbents leverage to affect pricing, roadmaps and SLAs (typical uptime SLAs 99.95–99.99%). Multi-cloud and modular architectures reduce but do not eliminate vendor lock-in.

Telecom equipment and fiber inputs

Fiber builds rely on a narrow set of optical gear, last-mile materials and specialized contractors, with optical module and cable lead times running roughly 20–40 weeks in 2023–24, heightening supplier leverage. Tight supply chains and long leads raise input bargaining power, often shifting schedule risk and increasing capex by mid-single to low-double-digit percentages on large builds. Volume commitments reduce but do not eliminate dependency on a few suppliers.

Data, credit, and payments rails

Data, credit and payments rails—credit bureaus, KYC/AML utilities and card networks—are essential suppliers for Nelnet; the three major U.S. bureaus (Equifax, Experian, TransUnion) supply over 90% of consumer credit data and Visa/Mastercard account for roughly 80%+ of card volume, so their fees and rule changes directly affect Nelnet’s unit economics and margins. Compliance with bureau and KYC/AML standards raises operating complexity and costs, and limited alternatives keep supplier bargaining power relatively strong.

- Credit bureaus: >90% market share

- Card networks: ~80%+ transaction share

- KYC/AML: raises compliance costs

- Result: high supplier leverage on fees and rules

Skilled labor and compliance expertise

Nelnet faces high supplier power for skilled labor: regulatory, cybersecurity, and AI/analytics talent remain scarce — ISC2 estimated a ~3.5M global cybersecurity shortfall in 2024. US wage growth was ~4.3% YoY (June 2024), ML engineer median base pay ≈$145k in 2024; turnover costs 6–9 months' salary; remote hiring widens but doesn’t remove scarcity.

- Leverage: certification and wage inflation raise supplier bargaining power

- Cost: turnover = 6–9 months' salary, knowledge loss impacts compliance workflows

- Mitigation: remote hiring expands pools but scarcity persists

ED's $1.6T loan control, cloud and bureau dominance, critical cyber talent gap

The U.S. Dept of Education controls ~$1.6T federal loans, creating major supplier power over Nelnet. Cloud (AWS 32%, Azure 23%, GCP 10%), credit bureaus (>90%) and card networks (~80%+) raise switching costs and fees; optical lead times 20–40 wks increase capex risk. Skilled labor scarcity (cyber shortfall ~3.5M; ML median pay ~$145k; 4.3% wage growth 2024) amplifies leverage.

| Supplier | Key metric |

|---|---|

| ED | $1.6T |

| Cloud | AWS32%/AZ23%/GCP10% |

| Bureaus | >90% |

| Cards | ~80%+ |

| Labor | 3.5M shortfall / $145k |

What is included in the product

Tailored Porter's Five Forces analysis of Nelnet uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary for investor reports and editable Word use.

Clear one-sheet Porter's Five Forces for Nelnet—customize pressure levels, swap in your data, and export a clean spider chart ready for pitch decks or executive reports.

Customers Bargaining Power

Dominant government servicing client

The Department of Education oversees roughly $1.6 trillion in federal student loans (2024), commanding scale and imposing stringent performance metrics on servicers. It can reallocate volumes or reset pricing via recompetes, and its scorecards and penalty regimes materially raise switching threats. These dynamics make buyer power very high in federal servicing.

Price-sensitive educational institutions

Price-sensitive educational institutions (part of a global edtech market valued at about $228B in 2024) adopt payment and EdTech tools under tight budgets and procurement rigor, driving RFP-driven cycles that encourage price comparisons and feature parity. Integration needs create customer stickiness but also negotiation leverage, with discounts and multi-year terms commonly requested during procurement.

Consumer borrowers with limited choice

Student loan borrowers have limited servicer choice—about 43 million borrowers holding roughly $1.6 trillion in federal student debt in 2024—so direct bargaining power is muted. High service expectations and regulatory complaint channels amplify impact; CFPB and ED complaints and enforcement (industry settlements such as Navient’s $1.7B resolution) mean poor service can trigger penalties. That regulatory leverage indirectly raises effective buyer influence on servicers like Nelnet.

Broadband households and municipalities

Subscribers choose fiber vs cable, fixed wireless and satellite across over 120 million US broadband households in 2024, increasing price transparency and switching risk for providers. Local governments and franchise arrangements, plus subsidies and municipal broadband initiatives, shift pricing leverage and access. Promotional churn and bundle-driven competition kept headline broadband ARPU largely flat in 2024, while community partnerships reduce but do not eliminate buyer power.

- Market size: >120M US broadband households (2024)

- Channels: fiber, cable, fixed wireless, satellite

- Drivers: municipal policy, subsidies, promotional churn, bundles

Enterprise and platform integrators

Enterprise and platform integrators can demand custom terms from Nelnet because their payment and data volumes justify bespoke pricing and SLAs; in 2024 Nelnet reported $1.64 billion in revenue with material contribution from payment and servicing businesses, underscoring dependence on large partners. Vendor consolidation in payments raised buyer leverage in 2024 as top consolidators expanded share, while co-marketing and joint go-to-market value can offset required discounts.

- High-volume leverage

- Bespoke SLAs and pricing

- Consolidation increases customer bargaining

- Co-marketing offsets margin pressure

Federal buyer power: $1.6T loans, ≈43M borrowers, edtech

Federal buyer power is very high: the Department of Education manages ~$1.6T in loans (2024) and can reallocate volumes via recompetes and scorecards. Institutions in a $228B global edtech market push RFP-driven pricing and integration demands. Borrowers (≈43M) have limited choice but regulatory channels (CFPB, ED) amplify service pressures. Broadband competition (~120M US households) raises price transparency and churn risk.

| Metric | 2024 Value |

|---|---|

| Federal student loan stock | $1.6T |

| Borrowers | ≈43M |

| Global edtech market | $228B |

| US broadband households | ≈120M |

| Nelnet revenue | $1.64B |

Preview Before You Purchase

Nelnet Porter's Five Forces Analysis

This preview shows the exact Nelnet Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final, complete file.

From Overview to Strategy Blueprint

Nelnet faces moderate buyer power from institutional contracts and price-sensitive students, low supplier power, high competitive rivalry among student-loan servicers, and regulatory barriers that limit new entrants while fintech substitutes create emerging threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nelnet’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated federal contract sources

The U.S. Department of Education is the single dominant source for federally serviced loan volumes—the outstanding federal student loan portfolio was about $1.6 trillion in 2024—making its policy, data standards and platform requirements de facto supplier inputs. Changes in rules, handoffs or volume allocations by ED can quickly shift compliance and operational costs to servicers like Nelnet. This concentration gives ED supplier-like power over pricing, contract terms and implementation timelines.

Cloud and core software dependence

Nelnet’s servicing, payments and EdTech stacks depend on dominant IaaS and core processing vendors—AWS (≈32% share), Azure (≈23%) and Google Cloud (≈10%) in 2024—creating few substitutes and significant switching friction. Migrating core platforms is costly and risky, giving incumbents leverage to affect pricing, roadmaps and SLAs (typical uptime SLAs 99.95–99.99%). Multi-cloud and modular architectures reduce but do not eliminate vendor lock-in.

Telecom equipment and fiber inputs

Fiber builds rely on a narrow set of optical gear, last-mile materials and specialized contractors, with optical module and cable lead times running roughly 20–40 weeks in 2023–24, heightening supplier leverage. Tight supply chains and long leads raise input bargaining power, often shifting schedule risk and increasing capex by mid-single to low-double-digit percentages on large builds. Volume commitments reduce but do not eliminate dependency on a few suppliers.

Data, credit, and payments rails

Data, credit and payments rails—credit bureaus, KYC/AML utilities and card networks—are essential suppliers for Nelnet; the three major U.S. bureaus (Equifax, Experian, TransUnion) supply over 90% of consumer credit data and Visa/Mastercard account for roughly 80%+ of card volume, so their fees and rule changes directly affect Nelnet’s unit economics and margins. Compliance with bureau and KYC/AML standards raises operating complexity and costs, and limited alternatives keep supplier bargaining power relatively strong.

- Credit bureaus: >90% market share

- Card networks: ~80%+ transaction share

- KYC/AML: raises compliance costs

- Result: high supplier leverage on fees and rules

Skilled labor and compliance expertise

Nelnet faces high supplier power for skilled labor: regulatory, cybersecurity, and AI/analytics talent remain scarce — ISC2 estimated a ~3.5M global cybersecurity shortfall in 2024. US wage growth was ~4.3% YoY (June 2024), ML engineer median base pay ≈$145k in 2024; turnover costs 6–9 months' salary; remote hiring widens but doesn’t remove scarcity.

- Leverage: certification and wage inflation raise supplier bargaining power

- Cost: turnover = 6–9 months' salary, knowledge loss impacts compliance workflows

- Mitigation: remote hiring expands pools but scarcity persists

ED's $1.6T loan control, cloud and bureau dominance, critical cyber talent gap

The U.S. Dept of Education controls ~$1.6T federal loans, creating major supplier power over Nelnet. Cloud (AWS 32%, Azure 23%, GCP 10%), credit bureaus (>90%) and card networks (~80%+) raise switching costs and fees; optical lead times 20–40 wks increase capex risk. Skilled labor scarcity (cyber shortfall ~3.5M; ML median pay ~$145k; 4.3% wage growth 2024) amplifies leverage.

| Supplier | Key metric |

|---|---|

| ED | $1.6T |

| Cloud | AWS32%/AZ23%/GCP10% |

| Bureaus | >90% |

| Cards | ~80%+ |

| Labor | 3.5M shortfall / $145k |

What is included in the product

Tailored Porter's Five Forces analysis of Nelnet uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary for investor reports and editable Word use.

Clear one-sheet Porter's Five Forces for Nelnet—customize pressure levels, swap in your data, and export a clean spider chart ready for pitch decks or executive reports.

Customers Bargaining Power

Dominant government servicing client

The Department of Education oversees roughly $1.6 trillion in federal student loans (2024), commanding scale and imposing stringent performance metrics on servicers. It can reallocate volumes or reset pricing via recompetes, and its scorecards and penalty regimes materially raise switching threats. These dynamics make buyer power very high in federal servicing.

Price-sensitive educational institutions

Price-sensitive educational institutions (part of a global edtech market valued at about $228B in 2024) adopt payment and EdTech tools under tight budgets and procurement rigor, driving RFP-driven cycles that encourage price comparisons and feature parity. Integration needs create customer stickiness but also negotiation leverage, with discounts and multi-year terms commonly requested during procurement.

Consumer borrowers with limited choice

Student loan borrowers have limited servicer choice—about 43 million borrowers holding roughly $1.6 trillion in federal student debt in 2024—so direct bargaining power is muted. High service expectations and regulatory complaint channels amplify impact; CFPB and ED complaints and enforcement (industry settlements such as Navient’s $1.7B resolution) mean poor service can trigger penalties. That regulatory leverage indirectly raises effective buyer influence on servicers like Nelnet.

Broadband households and municipalities

Subscribers choose fiber vs cable, fixed wireless and satellite across over 120 million US broadband households in 2024, increasing price transparency and switching risk for providers. Local governments and franchise arrangements, plus subsidies and municipal broadband initiatives, shift pricing leverage and access. Promotional churn and bundle-driven competition kept headline broadband ARPU largely flat in 2024, while community partnerships reduce but do not eliminate buyer power.

- Market size: >120M US broadband households (2024)

- Channels: fiber, cable, fixed wireless, satellite

- Drivers: municipal policy, subsidies, promotional churn, bundles

Enterprise and platform integrators

Enterprise and platform integrators can demand custom terms from Nelnet because their payment and data volumes justify bespoke pricing and SLAs; in 2024 Nelnet reported $1.64 billion in revenue with material contribution from payment and servicing businesses, underscoring dependence on large partners. Vendor consolidation in payments raised buyer leverage in 2024 as top consolidators expanded share, while co-marketing and joint go-to-market value can offset required discounts.

- High-volume leverage

- Bespoke SLAs and pricing

- Consolidation increases customer bargaining

- Co-marketing offsets margin pressure

Federal buyer power: $1.6T loans, ≈43M borrowers, edtech

Federal buyer power is very high: the Department of Education manages ~$1.6T in loans (2024) and can reallocate volumes via recompetes and scorecards. Institutions in a $228B global edtech market push RFP-driven pricing and integration demands. Borrowers (≈43M) have limited choice but regulatory channels (CFPB, ED) amplify service pressures. Broadband competition (~120M US households) raises price transparency and churn risk.

| Metric | 2024 Value |

|---|---|

| Federal student loan stock | $1.6T |

| Borrowers | ≈43M |

| Global edtech market | $228B |

| US broadband households | ≈120M |

| Nelnet revenue | $1.64B |

Preview Before You Purchase

Nelnet Porter's Five Forces Analysis

This preview shows the exact Nelnet Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final, complete file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Nelnet faces moderate buyer power from institutional contracts and price-sensitive students, low supplier power, high competitive rivalry among student-loan servicers, and regulatory barriers that limit new entrants while fintech substitutes create emerging threats. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nelnet’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated federal contract sources

The U.S. Department of Education is the single dominant source for federally serviced loan volumes—the outstanding federal student loan portfolio was about $1.6 trillion in 2024—making its policy, data standards and platform requirements de facto supplier inputs. Changes in rules, handoffs or volume allocations by ED can quickly shift compliance and operational costs to servicers like Nelnet. This concentration gives ED supplier-like power over pricing, contract terms and implementation timelines.

Cloud and core software dependence

Nelnet’s servicing, payments and EdTech stacks depend on dominant IaaS and core processing vendors—AWS (≈32% share), Azure (≈23%) and Google Cloud (≈10%) in 2024—creating few substitutes and significant switching friction. Migrating core platforms is costly and risky, giving incumbents leverage to affect pricing, roadmaps and SLAs (typical uptime SLAs 99.95–99.99%). Multi-cloud and modular architectures reduce but do not eliminate vendor lock-in.

Telecom equipment and fiber inputs

Fiber builds rely on a narrow set of optical gear, last-mile materials and specialized contractors, with optical module and cable lead times running roughly 20–40 weeks in 2023–24, heightening supplier leverage. Tight supply chains and long leads raise input bargaining power, often shifting schedule risk and increasing capex by mid-single to low-double-digit percentages on large builds. Volume commitments reduce but do not eliminate dependency on a few suppliers.

Data, credit, and payments rails

Data, credit and payments rails—credit bureaus, KYC/AML utilities and card networks—are essential suppliers for Nelnet; the three major U.S. bureaus (Equifax, Experian, TransUnion) supply over 90% of consumer credit data and Visa/Mastercard account for roughly 80%+ of card volume, so their fees and rule changes directly affect Nelnet’s unit economics and margins. Compliance with bureau and KYC/AML standards raises operating complexity and costs, and limited alternatives keep supplier bargaining power relatively strong.

- Credit bureaus: >90% market share

- Card networks: ~80%+ transaction share

- KYC/AML: raises compliance costs

- Result: high supplier leverage on fees and rules

Skilled labor and compliance expertise

Nelnet faces high supplier power for skilled labor: regulatory, cybersecurity, and AI/analytics talent remain scarce — ISC2 estimated a ~3.5M global cybersecurity shortfall in 2024. US wage growth was ~4.3% YoY (June 2024), ML engineer median base pay ≈$145k in 2024; turnover costs 6–9 months' salary; remote hiring widens but doesn’t remove scarcity.

- Leverage: certification and wage inflation raise supplier bargaining power

- Cost: turnover = 6–9 months' salary, knowledge loss impacts compliance workflows

- Mitigation: remote hiring expands pools but scarcity persists

ED's $1.6T loan control, cloud and bureau dominance, critical cyber talent gap

The U.S. Dept of Education controls ~$1.6T federal loans, creating major supplier power over Nelnet. Cloud (AWS 32%, Azure 23%, GCP 10%), credit bureaus (>90%) and card networks (~80%+) raise switching costs and fees; optical lead times 20–40 wks increase capex risk. Skilled labor scarcity (cyber shortfall ~3.5M; ML median pay ~$145k; 4.3% wage growth 2024) amplifies leverage.

| Supplier | Key metric |

|---|---|

| ED | $1.6T |

| Cloud | AWS32%/AZ23%/GCP10% |

| Bureaus | >90% |

| Cards | ~80%+ |

| Labor | 3.5M shortfall / $145k |

What is included in the product

Tailored Porter's Five Forces analysis of Nelnet uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary for investor reports and editable Word use.

Clear one-sheet Porter's Five Forces for Nelnet—customize pressure levels, swap in your data, and export a clean spider chart ready for pitch decks or executive reports.

Customers Bargaining Power

Dominant government servicing client

The Department of Education oversees roughly $1.6 trillion in federal student loans (2024), commanding scale and imposing stringent performance metrics on servicers. It can reallocate volumes or reset pricing via recompetes, and its scorecards and penalty regimes materially raise switching threats. These dynamics make buyer power very high in federal servicing.

Price-sensitive educational institutions

Price-sensitive educational institutions (part of a global edtech market valued at about $228B in 2024) adopt payment and EdTech tools under tight budgets and procurement rigor, driving RFP-driven cycles that encourage price comparisons and feature parity. Integration needs create customer stickiness but also negotiation leverage, with discounts and multi-year terms commonly requested during procurement.

Consumer borrowers with limited choice

Student loan borrowers have limited servicer choice—about 43 million borrowers holding roughly $1.6 trillion in federal student debt in 2024—so direct bargaining power is muted. High service expectations and regulatory complaint channels amplify impact; CFPB and ED complaints and enforcement (industry settlements such as Navient’s $1.7B resolution) mean poor service can trigger penalties. That regulatory leverage indirectly raises effective buyer influence on servicers like Nelnet.

Broadband households and municipalities

Subscribers choose fiber vs cable, fixed wireless and satellite across over 120 million US broadband households in 2024, increasing price transparency and switching risk for providers. Local governments and franchise arrangements, plus subsidies and municipal broadband initiatives, shift pricing leverage and access. Promotional churn and bundle-driven competition kept headline broadband ARPU largely flat in 2024, while community partnerships reduce but do not eliminate buyer power.

- Market size: >120M US broadband households (2024)

- Channels: fiber, cable, fixed wireless, satellite

- Drivers: municipal policy, subsidies, promotional churn, bundles

Enterprise and platform integrators

Enterprise and platform integrators can demand custom terms from Nelnet because their payment and data volumes justify bespoke pricing and SLAs; in 2024 Nelnet reported $1.64 billion in revenue with material contribution from payment and servicing businesses, underscoring dependence on large partners. Vendor consolidation in payments raised buyer leverage in 2024 as top consolidators expanded share, while co-marketing and joint go-to-market value can offset required discounts.

- High-volume leverage

- Bespoke SLAs and pricing

- Consolidation increases customer bargaining

- Co-marketing offsets margin pressure

Federal buyer power: $1.6T loans, ≈43M borrowers, edtech

Federal buyer power is very high: the Department of Education manages ~$1.6T in loans (2024) and can reallocate volumes via recompetes and scorecards. Institutions in a $228B global edtech market push RFP-driven pricing and integration demands. Borrowers (≈43M) have limited choice but regulatory channels (CFPB, ED) amplify service pressures. Broadband competition (~120M US households) raises price transparency and churn risk.

| Metric | 2024 Value |

|---|---|

| Federal student loan stock | $1.6T |

| Borrowers | ≈43M |

| Global edtech market | $228B |

| US broadband households | ≈120M |

| Nelnet revenue | $1.64B |

Preview Before You Purchase

Nelnet Porter's Five Forces Analysis

This preview shows the exact Nelnet Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final, complete file.