Nemetschek Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Nemetschek operates in a niche software market where supplier strength, customer bargaining, and rapid innovation jointly shape profitability. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nemetschek’s competitive dynamics, market pressures, and strategic advantages in detail. Our full report quantifies force intensity, provides visuals and clear implications for action.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

Nemetschek depends on major cloud providers (AWS, Microsoft Azure, Google Cloud), which together held roughly 66% of the global cloud market in 2024, concentrating supplier power. Pricing changes or tier shifts by those hyperscalers can directly raise hosting and AI costs, squeezing software margins. Multi-cloud and edge strategies can mitigate dependence but migration is complex and costly, while long-term contracts stabilize terms at the expense of flexibility.

Specialized developer talent

AECO-domain software depends on scarce 3D/BIM, geometry and graphics engineers, while the BLS 2023 median annual wage for software developers was $110,140, underscoring wage pressure in 2024 as demand outpaces supply. Tight labor markets raise turnover risk and concentrate critical knowledge in small teams, increasing supplier (talent) bargaining power. Investment in tooling, structured training, and nearshore hubs can mitigate cost and continuity risks.

Core technology and standards

Nemetschek's dependence on kernel technologies and GPUs creates supplier leverage: NVIDIA held roughly 80% of the discrete GPU market in 2024, so licensing or deprecation (e.g., CUDA changes) can force roadmap shifts. Reliance on standards like IFC/openBIM—backed by buildingSMART, which had over 600 members in 2024—means standards bodies can reprioritize timelines and interoperability. Active participation in consortia measurably reduces exposure to vendor-driven disruption.

Third-party data and content

Third-party geospatial, materials and product libraries underpin Nemetschek offerings, with data quality, coverage and licensing in 2024 directly shaping product differentiation and go-to-market speed; vendor consolidation risks higher fees or restricted access, pressuring margins. Building proprietary datasets and strategic partnerships reduces reliance and secures feature parity and pricing control.

- Geospatial/data sourcing: external dependency

- Impact: quality, coverage, licensing affect differentiation

- Risk: vendor consolidation can raise fees/restrict access

- Mitigation: proprietary data + partnerships lower supplier power

Channel partners and resellers

Channel partners and resellers drive Nemetschek’s regional reach, with implementation partners critical in localized AECO projects; in 2024 partner-led deployments remained a dominant route to market in many regions. Strong partners can extract higher margins, MDF and exclusive territories, increasing supplier bargaining power where markets are fragmented. Diversifying channels and scaling direct SaaS sales in 2024 reduced this dependence and supplier leverage.

- 2024: partner-led sales significant in localized AECO segments

- Risk: higher bargaining power where distributors demand MDF/exclusivity

- Mitigation: diversify channels, expand direct SaaS to lower partner leverage

Cloud and GPU concentration squeeze margins; use multi-cloud, proprietary data, nearshore talent

Concentrated cloud providers (AWS/Azure/GCP ~66% global cloud share in 2024) and dominant GPU/vendor positions (NVIDIA ~80% discrete GPU share in 2024) amplify supplier power, raising hosting, AI and licensing costs. Scarce AECO/BIM talent and specialized data/library vendors further tighten leverage, pressuring margins and continuity. Mitigations: multi-cloud, proprietary data, consortia engagement and nearshore talent hubs.

| Supplier | 2024 stat | Impact | Mitigation |

|---|---|---|---|

| Cloud | 66% market | Higher hosting/AI costs | Multi-cloud/long-term contracts |

| GPU/vendors | 80% NVIDIA | Tech lock-in | Open standards/consortia |

| Talent/data | High wage/limited sources | Turnover, licensing risk | Proprietary data, training |

What is included in the product

Tailored exclusively for Nemetschek, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, and market entry risks, while identifying disruptive substitutes and emerging threats that challenge its market share.

Clear, one-sheet Porter's Five Forces for Nemetschek—quickly spot competitive threats and opportunity levers with adjustable pressure sliders and an instant radar chart to simplify board-level decisions.

Customers Bargaining Power

Large enterprise procurement

Major contractors, engineers, and owners negotiate enterprise-wide deals that concentrate purchasing power—Nemetschek's scale (≈€1.1bn revenue in 2024) makes these customers seek volume discounts, audits, and multi-year commitments that materially boost buyer leverage. Competitive bidding among rival suites intensifies price pressure, often compressing margins by low-double digits on large deals. Value-based bundles and outcome SLAs can defend pricing by tying fees to measurable ROI.

High switching costs, but project-driven

BIM workflows, training burdens and proprietary file compatibility create strong lock-in for Nemetschek customers, despite the Group reaching about 1.1bn EUR revenue in 2024; project-driven tool choices allow gradual switching between phases, while rising EU BIM adoption (~68% in 2024) and touted interoperability increase buyer power by easing migration, and migration services and data-portability strategies materially shape negotiation dynamics.

SMB price sensitivity

Small studios and mid-sized firms show high price sensitivity with annual churn around 20–30% in 2024, driven by tight budgets and frequent vendor switching. Monthly SaaS and per-seat pricing encourage comparison shopping—about 60% of SMB buyers reported price as a primary selection factor in 2024. Freemium and promotional offers boost trial traffic by 3–10x but keep conversion rates low (2–5%), increasing elasticity. Clear ROI proof points and tiered packaging have been shown to reduce discount pressure by roughly 10–25%.

Interoperability expectations

Buyers insist on openBIM/IFC (ISO 16739:2013) support to avoid vendor lock-in, letting projects export/import models across platforms.

Strong standards compliance enables multi-homing across tools, eroding pricing power where product differentiation is thin.

Deep integrations and unique features—workflows, proprietary analytics—can preserve margins by creating switching costs.

- openBIM: ISO 16739:2013

- Multi-home reduces pricing leverage

- Differentiation via integrations offsets commoditization

Service and implementation demands

Contractor leverage and high SMB churn compress margins as EU BIM ~68% boosts buyer power

Large contractors and owners wield strong leverage—Nemetschek ≈€1.1bn revenue (2024) faces volume-discount and multi-year demands that compress margins. SMBs show 20–30% annual churn (2024), high price sensitivity; EU BIM adoption ~68% (2024) eases switching and raises buyer power. Service-heavy TCO adds 20–40% to license costs, enabling discount negotiation.

| Metric | 2024 value | Impact |

|---|---|---|

| Revenue | ≈€1.1bn | Buyer focus on enterprise deals |

| EU BIM adoption | ~68% | Reduces lock-in |

| SMB churn | 20–30% | Price sensitivity |

| TCO uplift | 20–40% | Negotiation leverage |

Preview the Actual Deliverable

Nemetschek Porter's Five Forces Analysis

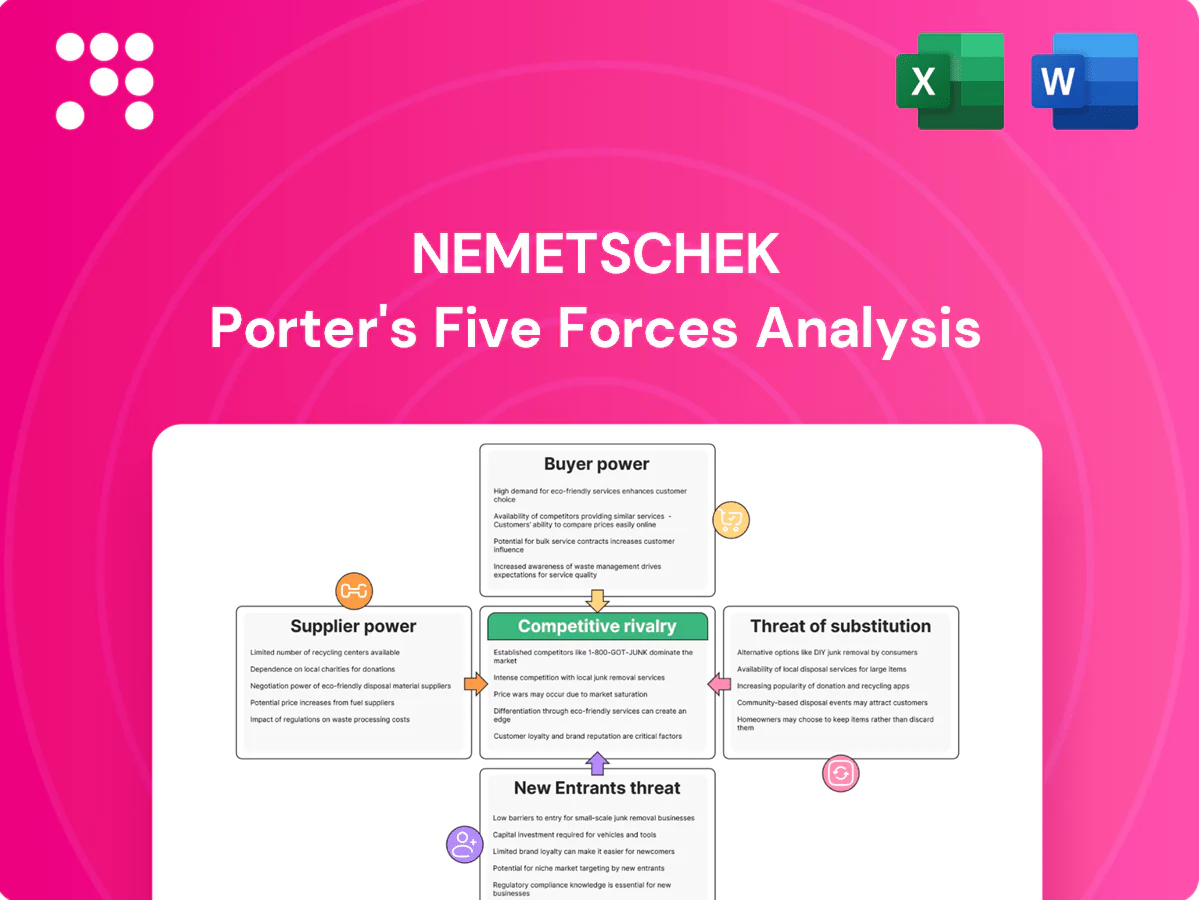

This preview shows the exact Nemetschek Porter's Five Forces analysis you’ll receive immediately after purchase—no samples, no placeholders. It’s the full, professionally formatted document, ready for download and use the moment you buy. The report covers threat of new entrants, supplier and buyer power, substitutes, and competitive rivalry specific to Nemetschek, enabling immediate strategic or investment use.

From Overview to Strategy Blueprint

Nemetschek operates in a niche software market where supplier strength, customer bargaining, and rapid innovation jointly shape profitability. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nemetschek’s competitive dynamics, market pressures, and strategic advantages in detail. Our full report quantifies force intensity, provides visuals and clear implications for action.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

Nemetschek depends on major cloud providers (AWS, Microsoft Azure, Google Cloud), which together held roughly 66% of the global cloud market in 2024, concentrating supplier power. Pricing changes or tier shifts by those hyperscalers can directly raise hosting and AI costs, squeezing software margins. Multi-cloud and edge strategies can mitigate dependence but migration is complex and costly, while long-term contracts stabilize terms at the expense of flexibility.

Specialized developer talent

AECO-domain software depends on scarce 3D/BIM, geometry and graphics engineers, while the BLS 2023 median annual wage for software developers was $110,140, underscoring wage pressure in 2024 as demand outpaces supply. Tight labor markets raise turnover risk and concentrate critical knowledge in small teams, increasing supplier (talent) bargaining power. Investment in tooling, structured training, and nearshore hubs can mitigate cost and continuity risks.

Core technology and standards

Nemetschek's dependence on kernel technologies and GPUs creates supplier leverage: NVIDIA held roughly 80% of the discrete GPU market in 2024, so licensing or deprecation (e.g., CUDA changes) can force roadmap shifts. Reliance on standards like IFC/openBIM—backed by buildingSMART, which had over 600 members in 2024—means standards bodies can reprioritize timelines and interoperability. Active participation in consortia measurably reduces exposure to vendor-driven disruption.

Third-party data and content

Third-party geospatial, materials and product libraries underpin Nemetschek offerings, with data quality, coverage and licensing in 2024 directly shaping product differentiation and go-to-market speed; vendor consolidation risks higher fees or restricted access, pressuring margins. Building proprietary datasets and strategic partnerships reduces reliance and secures feature parity and pricing control.

- Geospatial/data sourcing: external dependency

- Impact: quality, coverage, licensing affect differentiation

- Risk: vendor consolidation can raise fees/restrict access

- Mitigation: proprietary data + partnerships lower supplier power

Channel partners and resellers

Channel partners and resellers drive Nemetschek’s regional reach, with implementation partners critical in localized AECO projects; in 2024 partner-led deployments remained a dominant route to market in many regions. Strong partners can extract higher margins, MDF and exclusive territories, increasing supplier bargaining power where markets are fragmented. Diversifying channels and scaling direct SaaS sales in 2024 reduced this dependence and supplier leverage.

- 2024: partner-led sales significant in localized AECO segments

- Risk: higher bargaining power where distributors demand MDF/exclusivity

- Mitigation: diversify channels, expand direct SaaS to lower partner leverage

Cloud and GPU concentration squeeze margins; use multi-cloud, proprietary data, nearshore talent

Concentrated cloud providers (AWS/Azure/GCP ~66% global cloud share in 2024) and dominant GPU/vendor positions (NVIDIA ~80% discrete GPU share in 2024) amplify supplier power, raising hosting, AI and licensing costs. Scarce AECO/BIM talent and specialized data/library vendors further tighten leverage, pressuring margins and continuity. Mitigations: multi-cloud, proprietary data, consortia engagement and nearshore talent hubs.

| Supplier | 2024 stat | Impact | Mitigation |

|---|---|---|---|

| Cloud | 66% market | Higher hosting/AI costs | Multi-cloud/long-term contracts |

| GPU/vendors | 80% NVIDIA | Tech lock-in | Open standards/consortia |

| Talent/data | High wage/limited sources | Turnover, licensing risk | Proprietary data, training |

What is included in the product

Tailored exclusively for Nemetschek, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, and market entry risks, while identifying disruptive substitutes and emerging threats that challenge its market share.

Clear, one-sheet Porter's Five Forces for Nemetschek—quickly spot competitive threats and opportunity levers with adjustable pressure sliders and an instant radar chart to simplify board-level decisions.

Customers Bargaining Power

Large enterprise procurement

Major contractors, engineers, and owners negotiate enterprise-wide deals that concentrate purchasing power—Nemetschek's scale (≈€1.1bn revenue in 2024) makes these customers seek volume discounts, audits, and multi-year commitments that materially boost buyer leverage. Competitive bidding among rival suites intensifies price pressure, often compressing margins by low-double digits on large deals. Value-based bundles and outcome SLAs can defend pricing by tying fees to measurable ROI.

High switching costs, but project-driven

BIM workflows, training burdens and proprietary file compatibility create strong lock-in for Nemetschek customers, despite the Group reaching about 1.1bn EUR revenue in 2024; project-driven tool choices allow gradual switching between phases, while rising EU BIM adoption (~68% in 2024) and touted interoperability increase buyer power by easing migration, and migration services and data-portability strategies materially shape negotiation dynamics.

SMB price sensitivity

Small studios and mid-sized firms show high price sensitivity with annual churn around 20–30% in 2024, driven by tight budgets and frequent vendor switching. Monthly SaaS and per-seat pricing encourage comparison shopping—about 60% of SMB buyers reported price as a primary selection factor in 2024. Freemium and promotional offers boost trial traffic by 3–10x but keep conversion rates low (2–5%), increasing elasticity. Clear ROI proof points and tiered packaging have been shown to reduce discount pressure by roughly 10–25%.

Interoperability expectations

Buyers insist on openBIM/IFC (ISO 16739:2013) support to avoid vendor lock-in, letting projects export/import models across platforms.

Strong standards compliance enables multi-homing across tools, eroding pricing power where product differentiation is thin.

Deep integrations and unique features—workflows, proprietary analytics—can preserve margins by creating switching costs.

- openBIM: ISO 16739:2013

- Multi-home reduces pricing leverage

- Differentiation via integrations offsets commoditization

Service and implementation demands

Contractor leverage and high SMB churn compress margins as EU BIM ~68% boosts buyer power

Large contractors and owners wield strong leverage—Nemetschek ≈€1.1bn revenue (2024) faces volume-discount and multi-year demands that compress margins. SMBs show 20–30% annual churn (2024), high price sensitivity; EU BIM adoption ~68% (2024) eases switching and raises buyer power. Service-heavy TCO adds 20–40% to license costs, enabling discount negotiation.

| Metric | 2024 value | Impact |

|---|---|---|

| Revenue | ≈€1.1bn | Buyer focus on enterprise deals |

| EU BIM adoption | ~68% | Reduces lock-in |

| SMB churn | 20–30% | Price sensitivity |

| TCO uplift | 20–40% | Negotiation leverage |

Preview the Actual Deliverable

Nemetschek Porter's Five Forces Analysis

This preview shows the exact Nemetschek Porter's Five Forces analysis you’ll receive immediately after purchase—no samples, no placeholders. It’s the full, professionally formatted document, ready for download and use the moment you buy. The report covers threat of new entrants, supplier and buyer power, substitutes, and competitive rivalry specific to Nemetschek, enabling immediate strategic or investment use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Nemetschek operates in a niche software market where supplier strength, customer bargaining, and rapid innovation jointly shape profitability. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nemetschek’s competitive dynamics, market pressures, and strategic advantages in detail. Our full report quantifies force intensity, provides visuals and clear implications for action.

Suppliers Bargaining Power

Dependence on cloud hyperscalers

Nemetschek depends on major cloud providers (AWS, Microsoft Azure, Google Cloud), which together held roughly 66% of the global cloud market in 2024, concentrating supplier power. Pricing changes or tier shifts by those hyperscalers can directly raise hosting and AI costs, squeezing software margins. Multi-cloud and edge strategies can mitigate dependence but migration is complex and costly, while long-term contracts stabilize terms at the expense of flexibility.

Specialized developer talent

AECO-domain software depends on scarce 3D/BIM, geometry and graphics engineers, while the BLS 2023 median annual wage for software developers was $110,140, underscoring wage pressure in 2024 as demand outpaces supply. Tight labor markets raise turnover risk and concentrate critical knowledge in small teams, increasing supplier (talent) bargaining power. Investment in tooling, structured training, and nearshore hubs can mitigate cost and continuity risks.

Core technology and standards

Nemetschek's dependence on kernel technologies and GPUs creates supplier leverage: NVIDIA held roughly 80% of the discrete GPU market in 2024, so licensing or deprecation (e.g., CUDA changes) can force roadmap shifts. Reliance on standards like IFC/openBIM—backed by buildingSMART, which had over 600 members in 2024—means standards bodies can reprioritize timelines and interoperability. Active participation in consortia measurably reduces exposure to vendor-driven disruption.

Third-party data and content

Third-party geospatial, materials and product libraries underpin Nemetschek offerings, with data quality, coverage and licensing in 2024 directly shaping product differentiation and go-to-market speed; vendor consolidation risks higher fees or restricted access, pressuring margins. Building proprietary datasets and strategic partnerships reduces reliance and secures feature parity and pricing control.

- Geospatial/data sourcing: external dependency

- Impact: quality, coverage, licensing affect differentiation

- Risk: vendor consolidation can raise fees/restrict access

- Mitigation: proprietary data + partnerships lower supplier power

Channel partners and resellers

Channel partners and resellers drive Nemetschek’s regional reach, with implementation partners critical in localized AECO projects; in 2024 partner-led deployments remained a dominant route to market in many regions. Strong partners can extract higher margins, MDF and exclusive territories, increasing supplier bargaining power where markets are fragmented. Diversifying channels and scaling direct SaaS sales in 2024 reduced this dependence and supplier leverage.

- 2024: partner-led sales significant in localized AECO segments

- Risk: higher bargaining power where distributors demand MDF/exclusivity

- Mitigation: diversify channels, expand direct SaaS to lower partner leverage

Cloud and GPU concentration squeeze margins; use multi-cloud, proprietary data, nearshore talent

Concentrated cloud providers (AWS/Azure/GCP ~66% global cloud share in 2024) and dominant GPU/vendor positions (NVIDIA ~80% discrete GPU share in 2024) amplify supplier power, raising hosting, AI and licensing costs. Scarce AECO/BIM talent and specialized data/library vendors further tighten leverage, pressuring margins and continuity. Mitigations: multi-cloud, proprietary data, consortia engagement and nearshore talent hubs.

| Supplier | 2024 stat | Impact | Mitigation |

|---|---|---|---|

| Cloud | 66% market | Higher hosting/AI costs | Multi-cloud/long-term contracts |

| GPU/vendors | 80% NVIDIA | Tech lock-in | Open standards/consortia |

| Talent/data | High wage/limited sources | Turnover, licensing risk | Proprietary data, training |

What is included in the product

Tailored exclusively for Nemetschek, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, and market entry risks, while identifying disruptive substitutes and emerging threats that challenge its market share.

Clear, one-sheet Porter's Five Forces for Nemetschek—quickly spot competitive threats and opportunity levers with adjustable pressure sliders and an instant radar chart to simplify board-level decisions.

Customers Bargaining Power

Large enterprise procurement

Major contractors, engineers, and owners negotiate enterprise-wide deals that concentrate purchasing power—Nemetschek's scale (≈€1.1bn revenue in 2024) makes these customers seek volume discounts, audits, and multi-year commitments that materially boost buyer leverage. Competitive bidding among rival suites intensifies price pressure, often compressing margins by low-double digits on large deals. Value-based bundles and outcome SLAs can defend pricing by tying fees to measurable ROI.

High switching costs, but project-driven

BIM workflows, training burdens and proprietary file compatibility create strong lock-in for Nemetschek customers, despite the Group reaching about 1.1bn EUR revenue in 2024; project-driven tool choices allow gradual switching between phases, while rising EU BIM adoption (~68% in 2024) and touted interoperability increase buyer power by easing migration, and migration services and data-portability strategies materially shape negotiation dynamics.

SMB price sensitivity

Small studios and mid-sized firms show high price sensitivity with annual churn around 20–30% in 2024, driven by tight budgets and frequent vendor switching. Monthly SaaS and per-seat pricing encourage comparison shopping—about 60% of SMB buyers reported price as a primary selection factor in 2024. Freemium and promotional offers boost trial traffic by 3–10x but keep conversion rates low (2–5%), increasing elasticity. Clear ROI proof points and tiered packaging have been shown to reduce discount pressure by roughly 10–25%.

Interoperability expectations

Buyers insist on openBIM/IFC (ISO 16739:2013) support to avoid vendor lock-in, letting projects export/import models across platforms.

Strong standards compliance enables multi-homing across tools, eroding pricing power where product differentiation is thin.

Deep integrations and unique features—workflows, proprietary analytics—can preserve margins by creating switching costs.

- openBIM: ISO 16739:2013

- Multi-home reduces pricing leverage

- Differentiation via integrations offsets commoditization

Service and implementation demands

Contractor leverage and high SMB churn compress margins as EU BIM ~68% boosts buyer power

Large contractors and owners wield strong leverage—Nemetschek ≈€1.1bn revenue (2024) faces volume-discount and multi-year demands that compress margins. SMBs show 20–30% annual churn (2024), high price sensitivity; EU BIM adoption ~68% (2024) eases switching and raises buyer power. Service-heavy TCO adds 20–40% to license costs, enabling discount negotiation.

| Metric | 2024 value | Impact |

|---|---|---|

| Revenue | ≈€1.1bn | Buyer focus on enterprise deals |

| EU BIM adoption | ~68% | Reduces lock-in |

| SMB churn | 20–30% | Price sensitivity |

| TCO uplift | 20–40% | Negotiation leverage |

Preview the Actual Deliverable

Nemetschek Porter's Five Forces Analysis

This preview shows the exact Nemetschek Porter's Five Forces analysis you’ll receive immediately after purchase—no samples, no placeholders. It’s the full, professionally formatted document, ready for download and use the moment you buy. The report covers threat of new entrants, supplier and buyer power, substitutes, and competitive rivalry specific to Nemetschek, enabling immediate strategic or investment use.