NerdWallet Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

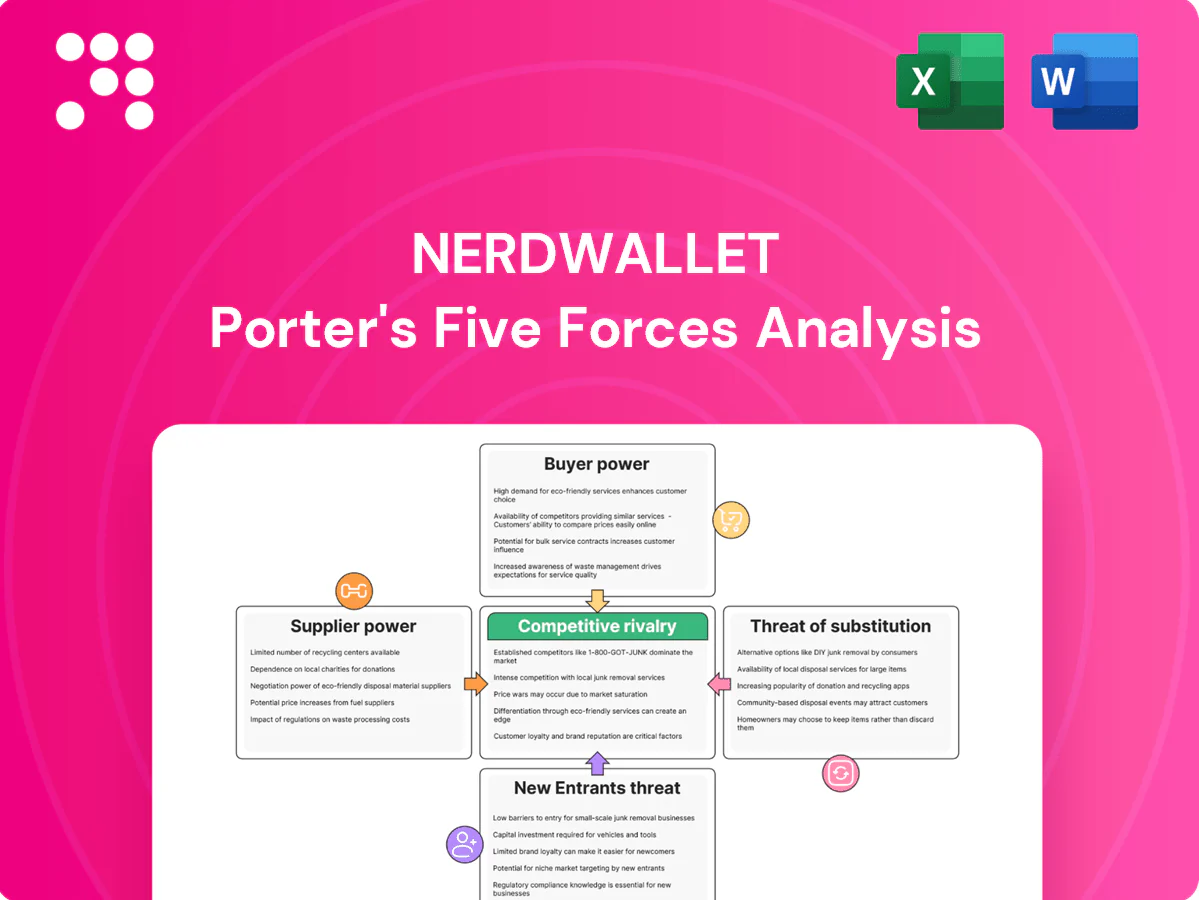

NerdWallet's Porter’s Five Forces analysis outlines buyer and supplier power, threat of substitutes and entrants, and rivalry shaping its fintech niche. It highlights strengths like brand and content moat while noting threats from platforms and lenders. This brief snapshot only scratches the surface; unlock the full Porter’s Five Forces Analysis for detailed ratings, visuals, and business implications to guide investment or strategy.

Suppliers Bargaining Power

Concentrated financial partners

Major banks and card issuers dominate offers — the top five issuers (JPMorgan, Bank of America, Citigroup, Capital One, American Express) control roughly 65% of U.S. card market share in 2024, giving them leverage over payout rates and placement terms. If a few large issuers pause or reduce affiliate programs, NerdWallet’s inventory quality and revenue mix can weaken quickly. Balancing partner exposure and using volume-based tiers helps offset concentrated supplier power.

Platform gatekeepers (search)

Google’s algorithm and evolving SERP features act as a de facto supplier of traffic, directly shaping visibility and acquisition costs. Google held roughly 92% of global search share in 2024 and zero-click searches exceeded 60%, so shifts in ranking, reviews, or AI overviews can materially cut lead flow. This dependence strengthens Google’s bargaining position absent any contract, making diversification into app, email, and direct channels essential to mitigate risk.

Data and API providers

Credit score, rate, and product-feed APIs are concentrated: FICO scores underlie about 90% of U.S. lending decisions and the three major bureaus hold roughly 95% of consumer credit data, enabling price hikes or restricted access. Data quality and latency directly dent conversion and trust. Multi-sourcing and internal pipelines reduce switching costs. Regulatory regimes (GDPR, CCPA, CFPB) further entrench key vendors.

Content contributors and experts

Experienced editors and domain specialists are scarce and command premium compensation, and in 2024 high-quality personal finance reviews require continuous updates, increasing supplier power in talent markets; strong employer brand and proprietary tooling at NerdWallet reduce reliance on single individuals, while structured content frameworks enable scale without diluting quality.

- Scarcity: premium pay for senior editors

- Ongoing updates: raises repeat costs

- Mitigants: employer brand + tooling

- Scaling: structured frameworks preserve quality

Ad networks and martech

Ad networks and martech vendors can dictate monetization via fees (SSP/ADX take rates typically 10–30%) and policy changes; privacy shifts and third-party cookie deprecations in 2024 have pushed many publishers toward identity solutions and walled gardens, concentrating supplier power. Negotiating enterprise contracts and building first-party data (can reduce acquisition costs by ~30%) lowers exposure, while incrementality testing—used by roughly 40% of marketers—limits vendor lock-in.

- fee-rates: 10–30%

- first-party data: ~30% lower CPA

- incrementality testing adoption: ~40%

- privacy-driven reliance: higher on identity/walled gardens (2024)

Supplier concentration raises pricing risk; company cuts CPA ≈30% via first-party data

Suppliers exert high leverage: top five card issuers hold ~65% U.S. share (2024), Google controls ~92% search with >60% zero-click, FICO/bureaus underpin ~90%/95% of lending data, and ad tech fees run 10–30%; these concentrations raise pricing and access risk, so NerdWallet offsets via partner diversification, first-party data (≈30% lower CPA) and enterprise contracts.

| Supplier | Key metric (2024) |

|---|---|

| Top card issuers | ~65% US share |

| Google search | ~92% share; >60% zero-click |

| Credit data | FICO ~90%; bureaus ~95% |

| Ad tech fees | 10–30% take rates |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to NerdWallet, detailing supplier and buyer power, substitutes, and disruptive threats that challenge market share; actionable insights highlight barriers protecting incumbents and strategic levers to sustain pricing and profitability.

Clear one-sheet summary of all five forces with customizable pressure levels and an instant spider chart—perfect for quick decision-making, pitch decks, and boardroom slides without complex macros.

Customers Bargaining Power

Low switching costs for users

Low switching costs mean consumers can compare offers across rival sites instantly, with over 70% of borrowers citing online comparison as key to choice in 2024, pressuring margins and forcing continuous UX optimization to protect conversion. Loyalty is fragile when rewards and rates shift, so clear value propositions and personalization can raise perceived switching costs. Strong trust signals and brand reputation retain traffic and improve lifetime value.

Price-sensitive advertisers

Price-sensitive advertisers in finance tighten bounties with credit cycles and can reallocate spend to direct channels or other affiliates within weeks, driven by market moves such as US credit card debt near $1.1 trillion in 2024 that pressures acquisition economics. Robust performance data and LTV insights give NerdWallet stronger negotiating leverage, while category diversification across cards, loans, and insurance smooths advertiser churn.

High information transparency

High information transparency is critical as NerdWallet serves over 20 million monthly users (2024), and users expect comprehensive, unbiased comparisons and will quickly abandon perceived bias. Clear methodology disclosures and editorial independence — cited in site policies and reviewer notes — lower skepticism. Rich filters and calculators boost perceived fairness, while poor disclosures drive negative reviews and increase customer bargaining power.

Multi-homing behavior

Users frequently multi-home, consulting several comparison sites before applying, which dilutes any single platform’s influence and compresses conversion rates and payouts; unique tools and proprietary ratings, however, can anchor decisions and raise lifetime value. Email and app ecosystems encourage gradual single-homing by retaining users over time in 2024.

- Multi-homing reduces per-visit conversion

- Proprietary tools increase retention

- Email/app ecosystems foster single-homing

Enterprise partners demand compliance

Enterprise partners demand strict marketing, disclosure and brand controls from affiliates; top US banks (largest five hold ~40% of deposits, FDIC 2023) enforce these to protect reputation, with noncompliance risking program removal or reduced commissions. Robust compliance ops lower partner leverage; accreditation and audits convert risk into trust-based upsells.

- Compliance controls reduce churn

- Noncompliance = program removal/reduced commissions

- Audits/accreditation enable upsell

Low switching costs and 70%+ online comparison compress margins, force UX tuning

Low switching costs and 70% of borrowers using online comparison in 2024 compress margins and force constant UX/rate tuning. NerdWallet’s 20M monthly users demand transparency, raising bargaining power when perceived bias appears. Advertiser leverage fluctuates with credit cycles (US credit card debt ~1.1T in 2024) and top banks (~40% deposits) enforce strict compliance.

| Metric | 2024 Value |

|---|---|

| Online comparison share | 70%+ |

| Monthly users | 20M |

| US credit card debt | $1.1T |

| Top5 banks deposit share | ~40% |

Same Document Delivered

NerdWallet Porter's Five Forces Analysis

This preview shows the exact NerdWallet Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the professionally formatted, ready-to-use file you'll be able to download the moment you buy. No surprises, just the full analysis as shown.

A Must-Have Tool for Decision-Makers

NerdWallet's Porter’s Five Forces analysis outlines buyer and supplier power, threat of substitutes and entrants, and rivalry shaping its fintech niche. It highlights strengths like brand and content moat while noting threats from platforms and lenders. This brief snapshot only scratches the surface; unlock the full Porter’s Five Forces Analysis for detailed ratings, visuals, and business implications to guide investment or strategy.

Suppliers Bargaining Power

Concentrated financial partners

Major banks and card issuers dominate offers — the top five issuers (JPMorgan, Bank of America, Citigroup, Capital One, American Express) control roughly 65% of U.S. card market share in 2024, giving them leverage over payout rates and placement terms. If a few large issuers pause or reduce affiliate programs, NerdWallet’s inventory quality and revenue mix can weaken quickly. Balancing partner exposure and using volume-based tiers helps offset concentrated supplier power.

Platform gatekeepers (search)

Google’s algorithm and evolving SERP features act as a de facto supplier of traffic, directly shaping visibility and acquisition costs. Google held roughly 92% of global search share in 2024 and zero-click searches exceeded 60%, so shifts in ranking, reviews, or AI overviews can materially cut lead flow. This dependence strengthens Google’s bargaining position absent any contract, making diversification into app, email, and direct channels essential to mitigate risk.

Data and API providers

Credit score, rate, and product-feed APIs are concentrated: FICO scores underlie about 90% of U.S. lending decisions and the three major bureaus hold roughly 95% of consumer credit data, enabling price hikes or restricted access. Data quality and latency directly dent conversion and trust. Multi-sourcing and internal pipelines reduce switching costs. Regulatory regimes (GDPR, CCPA, CFPB) further entrench key vendors.

Content contributors and experts

Experienced editors and domain specialists are scarce and command premium compensation, and in 2024 high-quality personal finance reviews require continuous updates, increasing supplier power in talent markets; strong employer brand and proprietary tooling at NerdWallet reduce reliance on single individuals, while structured content frameworks enable scale without diluting quality.

- Scarcity: premium pay for senior editors

- Ongoing updates: raises repeat costs

- Mitigants: employer brand + tooling

- Scaling: structured frameworks preserve quality

Ad networks and martech

Ad networks and martech vendors can dictate monetization via fees (SSP/ADX take rates typically 10–30%) and policy changes; privacy shifts and third-party cookie deprecations in 2024 have pushed many publishers toward identity solutions and walled gardens, concentrating supplier power. Negotiating enterprise contracts and building first-party data (can reduce acquisition costs by ~30%) lowers exposure, while incrementality testing—used by roughly 40% of marketers—limits vendor lock-in.

- fee-rates: 10–30%

- first-party data: ~30% lower CPA

- incrementality testing adoption: ~40%

- privacy-driven reliance: higher on identity/walled gardens (2024)

Supplier concentration raises pricing risk; company cuts CPA ≈30% via first-party data

Suppliers exert high leverage: top five card issuers hold ~65% U.S. share (2024), Google controls ~92% search with >60% zero-click, FICO/bureaus underpin ~90%/95% of lending data, and ad tech fees run 10–30%; these concentrations raise pricing and access risk, so NerdWallet offsets via partner diversification, first-party data (≈30% lower CPA) and enterprise contracts.

| Supplier | Key metric (2024) |

|---|---|

| Top card issuers | ~65% US share |

| Google search | ~92% share; >60% zero-click |

| Credit data | FICO ~90%; bureaus ~95% |

| Ad tech fees | 10–30% take rates |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to NerdWallet, detailing supplier and buyer power, substitutes, and disruptive threats that challenge market share; actionable insights highlight barriers protecting incumbents and strategic levers to sustain pricing and profitability.

Clear one-sheet summary of all five forces with customizable pressure levels and an instant spider chart—perfect for quick decision-making, pitch decks, and boardroom slides without complex macros.

Customers Bargaining Power

Low switching costs for users

Low switching costs mean consumers can compare offers across rival sites instantly, with over 70% of borrowers citing online comparison as key to choice in 2024, pressuring margins and forcing continuous UX optimization to protect conversion. Loyalty is fragile when rewards and rates shift, so clear value propositions and personalization can raise perceived switching costs. Strong trust signals and brand reputation retain traffic and improve lifetime value.

Price-sensitive advertisers

Price-sensitive advertisers in finance tighten bounties with credit cycles and can reallocate spend to direct channels or other affiliates within weeks, driven by market moves such as US credit card debt near $1.1 trillion in 2024 that pressures acquisition economics. Robust performance data and LTV insights give NerdWallet stronger negotiating leverage, while category diversification across cards, loans, and insurance smooths advertiser churn.

High information transparency

High information transparency is critical as NerdWallet serves over 20 million monthly users (2024), and users expect comprehensive, unbiased comparisons and will quickly abandon perceived bias. Clear methodology disclosures and editorial independence — cited in site policies and reviewer notes — lower skepticism. Rich filters and calculators boost perceived fairness, while poor disclosures drive negative reviews and increase customer bargaining power.

Multi-homing behavior

Users frequently multi-home, consulting several comparison sites before applying, which dilutes any single platform’s influence and compresses conversion rates and payouts; unique tools and proprietary ratings, however, can anchor decisions and raise lifetime value. Email and app ecosystems encourage gradual single-homing by retaining users over time in 2024.

- Multi-homing reduces per-visit conversion

- Proprietary tools increase retention

- Email/app ecosystems foster single-homing

Enterprise partners demand compliance

Enterprise partners demand strict marketing, disclosure and brand controls from affiliates; top US banks (largest five hold ~40% of deposits, FDIC 2023) enforce these to protect reputation, with noncompliance risking program removal or reduced commissions. Robust compliance ops lower partner leverage; accreditation and audits convert risk into trust-based upsells.

- Compliance controls reduce churn

- Noncompliance = program removal/reduced commissions

- Audits/accreditation enable upsell

Low switching costs and 70%+ online comparison compress margins, force UX tuning

Low switching costs and 70% of borrowers using online comparison in 2024 compress margins and force constant UX/rate tuning. NerdWallet’s 20M monthly users demand transparency, raising bargaining power when perceived bias appears. Advertiser leverage fluctuates with credit cycles (US credit card debt ~1.1T in 2024) and top banks (~40% deposits) enforce strict compliance.

| Metric | 2024 Value |

|---|---|

| Online comparison share | 70%+ |

| Monthly users | 20M |

| US credit card debt | $1.1T |

| Top5 banks deposit share | ~40% |

Same Document Delivered

NerdWallet Porter's Five Forces Analysis

This preview shows the exact NerdWallet Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the professionally formatted, ready-to-use file you'll be able to download the moment you buy. No surprises, just the full analysis as shown.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

NerdWallet's Porter’s Five Forces analysis outlines buyer and supplier power, threat of substitutes and entrants, and rivalry shaping its fintech niche. It highlights strengths like brand and content moat while noting threats from platforms and lenders. This brief snapshot only scratches the surface; unlock the full Porter’s Five Forces Analysis for detailed ratings, visuals, and business implications to guide investment or strategy.

Suppliers Bargaining Power

Concentrated financial partners

Major banks and card issuers dominate offers — the top five issuers (JPMorgan, Bank of America, Citigroup, Capital One, American Express) control roughly 65% of U.S. card market share in 2024, giving them leverage over payout rates and placement terms. If a few large issuers pause or reduce affiliate programs, NerdWallet’s inventory quality and revenue mix can weaken quickly. Balancing partner exposure and using volume-based tiers helps offset concentrated supplier power.

Platform gatekeepers (search)

Google’s algorithm and evolving SERP features act as a de facto supplier of traffic, directly shaping visibility and acquisition costs. Google held roughly 92% of global search share in 2024 and zero-click searches exceeded 60%, so shifts in ranking, reviews, or AI overviews can materially cut lead flow. This dependence strengthens Google’s bargaining position absent any contract, making diversification into app, email, and direct channels essential to mitigate risk.

Data and API providers

Credit score, rate, and product-feed APIs are concentrated: FICO scores underlie about 90% of U.S. lending decisions and the three major bureaus hold roughly 95% of consumer credit data, enabling price hikes or restricted access. Data quality and latency directly dent conversion and trust. Multi-sourcing and internal pipelines reduce switching costs. Regulatory regimes (GDPR, CCPA, CFPB) further entrench key vendors.

Content contributors and experts

Experienced editors and domain specialists are scarce and command premium compensation, and in 2024 high-quality personal finance reviews require continuous updates, increasing supplier power in talent markets; strong employer brand and proprietary tooling at NerdWallet reduce reliance on single individuals, while structured content frameworks enable scale without diluting quality.

- Scarcity: premium pay for senior editors

- Ongoing updates: raises repeat costs

- Mitigants: employer brand + tooling

- Scaling: structured frameworks preserve quality

Ad networks and martech

Ad networks and martech vendors can dictate monetization via fees (SSP/ADX take rates typically 10–30%) and policy changes; privacy shifts and third-party cookie deprecations in 2024 have pushed many publishers toward identity solutions and walled gardens, concentrating supplier power. Negotiating enterprise contracts and building first-party data (can reduce acquisition costs by ~30%) lowers exposure, while incrementality testing—used by roughly 40% of marketers—limits vendor lock-in.

- fee-rates: 10–30%

- first-party data: ~30% lower CPA

- incrementality testing adoption: ~40%

- privacy-driven reliance: higher on identity/walled gardens (2024)

Supplier concentration raises pricing risk; company cuts CPA ≈30% via first-party data

Suppliers exert high leverage: top five card issuers hold ~65% U.S. share (2024), Google controls ~92% search with >60% zero-click, FICO/bureaus underpin ~90%/95% of lending data, and ad tech fees run 10–30%; these concentrations raise pricing and access risk, so NerdWallet offsets via partner diversification, first-party data (≈30% lower CPA) and enterprise contracts.

| Supplier | Key metric (2024) |

|---|---|

| Top card issuers | ~65% US share |

| Google search | ~92% share; >60% zero-click |

| Credit data | FICO ~90%; bureaus ~95% |

| Ad tech fees | 10–30% take rates |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to NerdWallet, detailing supplier and buyer power, substitutes, and disruptive threats that challenge market share; actionable insights highlight barriers protecting incumbents and strategic levers to sustain pricing and profitability.

Clear one-sheet summary of all five forces with customizable pressure levels and an instant spider chart—perfect for quick decision-making, pitch decks, and boardroom slides without complex macros.

Customers Bargaining Power

Low switching costs for users

Low switching costs mean consumers can compare offers across rival sites instantly, with over 70% of borrowers citing online comparison as key to choice in 2024, pressuring margins and forcing continuous UX optimization to protect conversion. Loyalty is fragile when rewards and rates shift, so clear value propositions and personalization can raise perceived switching costs. Strong trust signals and brand reputation retain traffic and improve lifetime value.

Price-sensitive advertisers

Price-sensitive advertisers in finance tighten bounties with credit cycles and can reallocate spend to direct channels or other affiliates within weeks, driven by market moves such as US credit card debt near $1.1 trillion in 2024 that pressures acquisition economics. Robust performance data and LTV insights give NerdWallet stronger negotiating leverage, while category diversification across cards, loans, and insurance smooths advertiser churn.

High information transparency

High information transparency is critical as NerdWallet serves over 20 million monthly users (2024), and users expect comprehensive, unbiased comparisons and will quickly abandon perceived bias. Clear methodology disclosures and editorial independence — cited in site policies and reviewer notes — lower skepticism. Rich filters and calculators boost perceived fairness, while poor disclosures drive negative reviews and increase customer bargaining power.

Multi-homing behavior

Users frequently multi-home, consulting several comparison sites before applying, which dilutes any single platform’s influence and compresses conversion rates and payouts; unique tools and proprietary ratings, however, can anchor decisions and raise lifetime value. Email and app ecosystems encourage gradual single-homing by retaining users over time in 2024.

- Multi-homing reduces per-visit conversion

- Proprietary tools increase retention

- Email/app ecosystems foster single-homing

Enterprise partners demand compliance

Enterprise partners demand strict marketing, disclosure and brand controls from affiliates; top US banks (largest five hold ~40% of deposits, FDIC 2023) enforce these to protect reputation, with noncompliance risking program removal or reduced commissions. Robust compliance ops lower partner leverage; accreditation and audits convert risk into trust-based upsells.

- Compliance controls reduce churn

- Noncompliance = program removal/reduced commissions

- Audits/accreditation enable upsell

Low switching costs and 70%+ online comparison compress margins, force UX tuning

Low switching costs and 70% of borrowers using online comparison in 2024 compress margins and force constant UX/rate tuning. NerdWallet’s 20M monthly users demand transparency, raising bargaining power when perceived bias appears. Advertiser leverage fluctuates with credit cycles (US credit card debt ~1.1T in 2024) and top banks (~40% deposits) enforce strict compliance.

| Metric | 2024 Value |

|---|---|

| Online comparison share | 70%+ |

| Monthly users | 20M |

| US credit card debt | $1.1T |

| Top5 banks deposit share | ~40% |

Same Document Delivered

NerdWallet Porter's Five Forces Analysis

This preview shows the exact NerdWallet Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the professionally formatted, ready-to-use file you'll be able to download the moment you buy. No surprises, just the full analysis as shown.