Netgear PESTLE Analysis

Skip the Research. Get the Strategy.

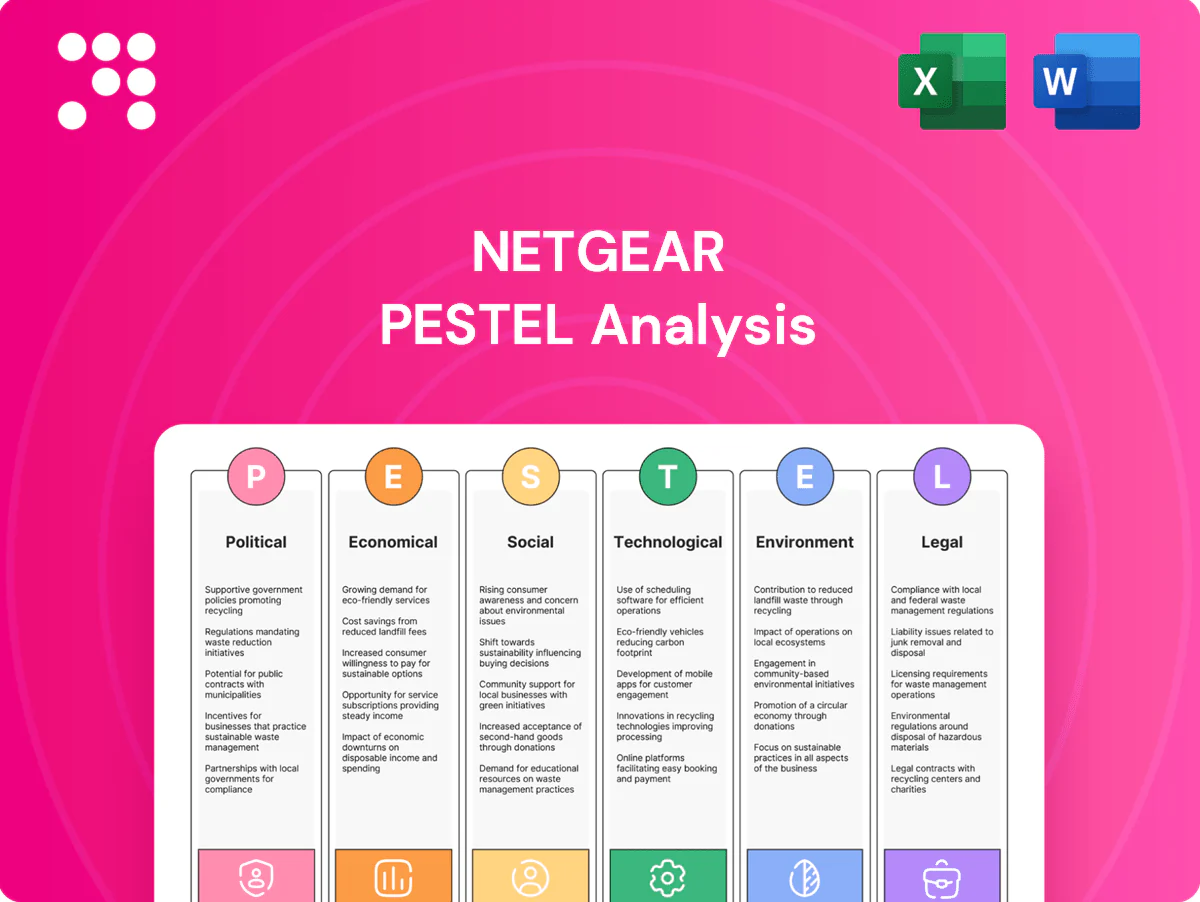

Our Netgear PESTLE highlights key political, economic, social, technological, legal, and environmental forces shaping its market position and risks. These concise insights reveal strategic threats and growth levers for investors and managers. Purchase the full, ready-to-use analysis to access the complete breakdown and actionable recommendations.

Political factors

Trade policies and tariffs on electronics

Import/export duties on networking hardware — notably US Section 301 tariffs up to 25% covering roughly $250 billion of Chinese goods — can swing Netgear’s BOM and retail pricing across markets. Ongoing US–China and EU–China tensions and expanded export controls on advanced chips (2022–2023) risk new tariffs or entity restrictions that impact ODM/OEM partners. Netgear may need to reconfigure sourcing, adjust pricing to protect margins, and hold higher inventory when policy stability is low.

Government broadband and digital-inclusion programs

Public subsidies such as the US BEAD program ($42.45B) and EU recovery funds (€672.5B) expand addressable demand for routers, mesh systems and SMB switches. Eligibility criteria and local content rules force Netgear to tailor product specs and forge regional partnerships. Participation speeds channel pull-through but increases compliance and certification costs. Funding timelines create pronounced sales seasonality tied to grant cycles.

Geopolitical supply-chain risks

Regional instability, port closures, or sanctions can disrupt component flow and logistics, amplified by roughly 60–70% of advanced semiconductor capacity concentrated in Taiwan and South Korea. Netgear must diversify suppliers, pursue dual-sourcing and hold multi-week buffer inventory to reduce downtime risk. Political risk insurance further mitigates financial exposure from abrupt geopolitical shocks.

Telecom and spectrum policy direction

Telecom allocation of 6 GHz (FCC opened 1200 MHz) and moves toward future bands drive Netgear product roadmaps and accelerate Wi‑Fi 6E/7 adoption, shaping R&D spend and inventory planning. National certification regimes in over 40 countries stagger launches, raising time‑to‑market and working capital needs. Harmonized standards reduce SKUs and unit cost; fragmented rules inflate compliance and NRE. Engagement with regulators preserves market access and policy influence.

- 1200 MHz 6 GHz allocation impacts device design and throughput

- >40 countries with varied 6 GHz rules create staggered launches

- Harmonization lowers SKUs, fragmentation increases compliance cost

- Regulatory engagement mitigates market risk and shapes standards

Public cybersecurity posture

- Regulations: EU CRA, California SB-327

- Mandates: default-password bans, auto-updates, vuln disclosure

- Scale: 29.4 billion IoT devices (2025)

- Impact: higher dev costs, certification = competitive edge

Tariffs, Export Controls and Grants Reshape Supply, Compliance and 6 GHz Roadmaps

Tariffs, US–China/EU–China export controls and regional sanctions raise BOM and supply risks, forcing dual‑sourcing and higher inventories. Public programs (US BEAD $42.45B, EU Recovery €672.5B) boost demand but add local‑content and compliance burdens. 6 GHz allocation and 40+ national certification regimes drive R&D and time‑to‑market. Cyber rules (EU CRA, CA SB‑327) increase dev/cert costs while raising trust.

| Issue | Key Figure | Impact |

|---|---|---|

| BEAD | $42.45B | Grant-driven demand |

| EU Recovery | €672.5B | Procurement opportunities |

| 6 GHz | 1200 MHz | Wi‑Fi 6E/7 roadmap |

| IoT scale | 29.4B (2025) | Regulatory scope |

What is included in the product

Explores how macro-environmental factors uniquely affect Netgear across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and sector trends to highlight risks and opportunities for executives and investors.

A concise, visually segmented Netgear PESTLE summary that relieves planning pain by highlighting regulatory, technological, and market risks at a glance, easily editable for region- or product-specific notes and drop‑in ready for presentations or team alignment.

Economic factors

Consumer spending and SMB IT budgets

Macro cycles and inflation directly curb discretionary router and NAS upgrades; US CPI rose 3.4% in 2024 (BLS), tightening household spend.

SMB capex softness delays switch refreshes and WiFi deployments—Spiceworks Ziff Davis 2024 shows budget constraints remain the top barrier to SMB upgrades.

Value tiers and promotions become critical in downturns, while premium segments hold better when they deliver measurable performance gains.

Component pricing and availability

Chip, memory and PCB cost swings drove Netgear gross-margin volatility, with reported 2024 gross margin near 41.8% and quarter-to-quarter swings of several percentage points; component cost changes remain primary margin driver. Lead-time swings—from weeks to multiple months—force tighter forecast discipline and modular design flexibility. Strategic buys and long-term agreements (LTAs) reduced COGS exposure in 2024, while alternative components require revalidation and certification updates, extending time-to-market.

Foreign exchange fluctuations

Netgear earns a large share of revenue overseas, while many supply-chain and R&D costs remain USD-linked, so foreign exchange swings materially affect reported earnings and channel price competitiveness. Hedging programs—used in 2024—cut quarter-to-quarter volatility but cannot offset long-term structural currency shifts. Localized pricing and currency-indexed contracts help protect market share in key regions.

Channel inventory and retailer dynamics

Big-box, e-commerce and distributors typically target 4–12 weeks-of-supply; overbuild forces 10–30% discounting, compressing gross margins by ~200–500 bps. POS analytics and S&OP alignment have cut returns in comparable CE channels by up to 15% and improved forecast accuracy. Bundles and attach offers boost sell-through and can raise attach rates 10–20%.

- weeks-of-supply: 4–12

- discounting: 10–30%

- margin erosion: ~200–500 bps

- returns reduction: up to 15%

- attach rate lift: 10–20%

Interest rates and financing conditions

Higher interest rates (US federal funds ~5.25–5.50% in mid‑2025) dampen consumer credit‑fuelled purchases and SMB leasing, raising costs for Netgear channel demand; working capital costs rise as financing inventory and receivables becomes more expensive. Efficient cash conversion cycles and tighter receivables management become a competitive differentiator, while deferred revenue from services and subscriptions helps stabilize cash flows.

- impact: weaker consumer and SMB capex

- costs: higher inventory/AR financing

- advantage: faster cash conversion

- buffer: deferred service revenue stabilizes cash

Tariffs, Export Controls and Grants Reshape Supply, Compliance and 6 GHz Roadmaps

Macroeconomic tightness (US CPI 3.4% in 2024) depresses consumer and SMB upgrades; Fed funds ~5.25–5.50% (mid‑2025) raises financing costs. Netgear 2024 gross margin ~41.8%; component/lead‑time swings force forecast discipline. Channel discounting 10–30% can compress margins ~200–500 bps; hedging and LTAs reduced FX/COGS volatility but not demand risk.

| Metric | Value |

|---|---|

| US CPI (2024) | 3.4% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| Netgear gross margin (2024) | ~41.8% |

| Channel discounting | 10–30% |

| Margin erosion | ~200–500 bps |

Preview the Actual Deliverable

Netgear PESTLE Analysis

The preview shown here is the exact Netgear PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with no placeholders or teasers. After payment you’ll instantly download the same complete document visible in the preview.

Skip the Research. Get the Strategy.

Our Netgear PESTLE highlights key political, economic, social, technological, legal, and environmental forces shaping its market position and risks. These concise insights reveal strategic threats and growth levers for investors and managers. Purchase the full, ready-to-use analysis to access the complete breakdown and actionable recommendations.

Political factors

Trade policies and tariffs on electronics

Import/export duties on networking hardware — notably US Section 301 tariffs up to 25% covering roughly $250 billion of Chinese goods — can swing Netgear’s BOM and retail pricing across markets. Ongoing US–China and EU–China tensions and expanded export controls on advanced chips (2022–2023) risk new tariffs or entity restrictions that impact ODM/OEM partners. Netgear may need to reconfigure sourcing, adjust pricing to protect margins, and hold higher inventory when policy stability is low.

Government broadband and digital-inclusion programs

Public subsidies such as the US BEAD program ($42.45B) and EU recovery funds (€672.5B) expand addressable demand for routers, mesh systems and SMB switches. Eligibility criteria and local content rules force Netgear to tailor product specs and forge regional partnerships. Participation speeds channel pull-through but increases compliance and certification costs. Funding timelines create pronounced sales seasonality tied to grant cycles.

Geopolitical supply-chain risks

Regional instability, port closures, or sanctions can disrupt component flow and logistics, amplified by roughly 60–70% of advanced semiconductor capacity concentrated in Taiwan and South Korea. Netgear must diversify suppliers, pursue dual-sourcing and hold multi-week buffer inventory to reduce downtime risk. Political risk insurance further mitigates financial exposure from abrupt geopolitical shocks.

Telecom and spectrum policy direction

Telecom allocation of 6 GHz (FCC opened 1200 MHz) and moves toward future bands drive Netgear product roadmaps and accelerate Wi‑Fi 6E/7 adoption, shaping R&D spend and inventory planning. National certification regimes in over 40 countries stagger launches, raising time‑to‑market and working capital needs. Harmonized standards reduce SKUs and unit cost; fragmented rules inflate compliance and NRE. Engagement with regulators preserves market access and policy influence.

- 1200 MHz 6 GHz allocation impacts device design and throughput

- >40 countries with varied 6 GHz rules create staggered launches

- Harmonization lowers SKUs, fragmentation increases compliance cost

- Regulatory engagement mitigates market risk and shapes standards

Public cybersecurity posture

- Regulations: EU CRA, California SB-327

- Mandates: default-password bans, auto-updates, vuln disclosure

- Scale: 29.4 billion IoT devices (2025)

- Impact: higher dev costs, certification = competitive edge

Tariffs, Export Controls and Grants Reshape Supply, Compliance and 6 GHz Roadmaps

Tariffs, US–China/EU–China export controls and regional sanctions raise BOM and supply risks, forcing dual‑sourcing and higher inventories. Public programs (US BEAD $42.45B, EU Recovery €672.5B) boost demand but add local‑content and compliance burdens. 6 GHz allocation and 40+ national certification regimes drive R&D and time‑to‑market. Cyber rules (EU CRA, CA SB‑327) increase dev/cert costs while raising trust.

| Issue | Key Figure | Impact |

|---|---|---|

| BEAD | $42.45B | Grant-driven demand |

| EU Recovery | €672.5B | Procurement opportunities |

| 6 GHz | 1200 MHz | Wi‑Fi 6E/7 roadmap |

| IoT scale | 29.4B (2025) | Regulatory scope |

What is included in the product

Explores how macro-environmental factors uniquely affect Netgear across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and sector trends to highlight risks and opportunities for executives and investors.

A concise, visually segmented Netgear PESTLE summary that relieves planning pain by highlighting regulatory, technological, and market risks at a glance, easily editable for region- or product-specific notes and drop‑in ready for presentations or team alignment.

Economic factors

Consumer spending and SMB IT budgets

Macro cycles and inflation directly curb discretionary router and NAS upgrades; US CPI rose 3.4% in 2024 (BLS), tightening household spend.

SMB capex softness delays switch refreshes and WiFi deployments—Spiceworks Ziff Davis 2024 shows budget constraints remain the top barrier to SMB upgrades.

Value tiers and promotions become critical in downturns, while premium segments hold better when they deliver measurable performance gains.

Component pricing and availability

Chip, memory and PCB cost swings drove Netgear gross-margin volatility, with reported 2024 gross margin near 41.8% and quarter-to-quarter swings of several percentage points; component cost changes remain primary margin driver. Lead-time swings—from weeks to multiple months—force tighter forecast discipline and modular design flexibility. Strategic buys and long-term agreements (LTAs) reduced COGS exposure in 2024, while alternative components require revalidation and certification updates, extending time-to-market.

Foreign exchange fluctuations

Netgear earns a large share of revenue overseas, while many supply-chain and R&D costs remain USD-linked, so foreign exchange swings materially affect reported earnings and channel price competitiveness. Hedging programs—used in 2024—cut quarter-to-quarter volatility but cannot offset long-term structural currency shifts. Localized pricing and currency-indexed contracts help protect market share in key regions.

Channel inventory and retailer dynamics

Big-box, e-commerce and distributors typically target 4–12 weeks-of-supply; overbuild forces 10–30% discounting, compressing gross margins by ~200–500 bps. POS analytics and S&OP alignment have cut returns in comparable CE channels by up to 15% and improved forecast accuracy. Bundles and attach offers boost sell-through and can raise attach rates 10–20%.

- weeks-of-supply: 4–12

- discounting: 10–30%

- margin erosion: ~200–500 bps

- returns reduction: up to 15%

- attach rate lift: 10–20%

Interest rates and financing conditions

Higher interest rates (US federal funds ~5.25–5.50% in mid‑2025) dampen consumer credit‑fuelled purchases and SMB leasing, raising costs for Netgear channel demand; working capital costs rise as financing inventory and receivables becomes more expensive. Efficient cash conversion cycles and tighter receivables management become a competitive differentiator, while deferred revenue from services and subscriptions helps stabilize cash flows.

- impact: weaker consumer and SMB capex

- costs: higher inventory/AR financing

- advantage: faster cash conversion

- buffer: deferred service revenue stabilizes cash

Tariffs, Export Controls and Grants Reshape Supply, Compliance and 6 GHz Roadmaps

Macroeconomic tightness (US CPI 3.4% in 2024) depresses consumer and SMB upgrades; Fed funds ~5.25–5.50% (mid‑2025) raises financing costs. Netgear 2024 gross margin ~41.8%; component/lead‑time swings force forecast discipline. Channel discounting 10–30% can compress margins ~200–500 bps; hedging and LTAs reduced FX/COGS volatility but not demand risk.

| Metric | Value |

|---|---|

| US CPI (2024) | 3.4% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| Netgear gross margin (2024) | ~41.8% |

| Channel discounting | 10–30% |

| Margin erosion | ~200–500 bps |

Preview the Actual Deliverable

Netgear PESTLE Analysis

The preview shown here is the exact Netgear PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with no placeholders or teasers. After payment you’ll instantly download the same complete document visible in the preview.

Description

Skip the Research. Get the Strategy.

Our Netgear PESTLE highlights key political, economic, social, technological, legal, and environmental forces shaping its market position and risks. These concise insights reveal strategic threats and growth levers for investors and managers. Purchase the full, ready-to-use analysis to access the complete breakdown and actionable recommendations.

Political factors

Trade policies and tariffs on electronics

Import/export duties on networking hardware — notably US Section 301 tariffs up to 25% covering roughly $250 billion of Chinese goods — can swing Netgear’s BOM and retail pricing across markets. Ongoing US–China and EU–China tensions and expanded export controls on advanced chips (2022–2023) risk new tariffs or entity restrictions that impact ODM/OEM partners. Netgear may need to reconfigure sourcing, adjust pricing to protect margins, and hold higher inventory when policy stability is low.

Government broadband and digital-inclusion programs

Public subsidies such as the US BEAD program ($42.45B) and EU recovery funds (€672.5B) expand addressable demand for routers, mesh systems and SMB switches. Eligibility criteria and local content rules force Netgear to tailor product specs and forge regional partnerships. Participation speeds channel pull-through but increases compliance and certification costs. Funding timelines create pronounced sales seasonality tied to grant cycles.

Geopolitical supply-chain risks

Regional instability, port closures, or sanctions can disrupt component flow and logistics, amplified by roughly 60–70% of advanced semiconductor capacity concentrated in Taiwan and South Korea. Netgear must diversify suppliers, pursue dual-sourcing and hold multi-week buffer inventory to reduce downtime risk. Political risk insurance further mitigates financial exposure from abrupt geopolitical shocks.

Telecom and spectrum policy direction

Telecom allocation of 6 GHz (FCC opened 1200 MHz) and moves toward future bands drive Netgear product roadmaps and accelerate Wi‑Fi 6E/7 adoption, shaping R&D spend and inventory planning. National certification regimes in over 40 countries stagger launches, raising time‑to‑market and working capital needs. Harmonized standards reduce SKUs and unit cost; fragmented rules inflate compliance and NRE. Engagement with regulators preserves market access and policy influence.

- 1200 MHz 6 GHz allocation impacts device design and throughput

- >40 countries with varied 6 GHz rules create staggered launches

- Harmonization lowers SKUs, fragmentation increases compliance cost

- Regulatory engagement mitigates market risk and shapes standards

Public cybersecurity posture

- Regulations: EU CRA, California SB-327

- Mandates: default-password bans, auto-updates, vuln disclosure

- Scale: 29.4 billion IoT devices (2025)

- Impact: higher dev costs, certification = competitive edge

Tariffs, Export Controls and Grants Reshape Supply, Compliance and 6 GHz Roadmaps

Tariffs, US–China/EU–China export controls and regional sanctions raise BOM and supply risks, forcing dual‑sourcing and higher inventories. Public programs (US BEAD $42.45B, EU Recovery €672.5B) boost demand but add local‑content and compliance burdens. 6 GHz allocation and 40+ national certification regimes drive R&D and time‑to‑market. Cyber rules (EU CRA, CA SB‑327) increase dev/cert costs while raising trust.

| Issue | Key Figure | Impact |

|---|---|---|

| BEAD | $42.45B | Grant-driven demand |

| EU Recovery | €672.5B | Procurement opportunities |

| 6 GHz | 1200 MHz | Wi‑Fi 6E/7 roadmap |

| IoT scale | 29.4B (2025) | Regulatory scope |

What is included in the product

Explores how macro-environmental factors uniquely affect Netgear across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by data and sector trends to highlight risks and opportunities for executives and investors.

A concise, visually segmented Netgear PESTLE summary that relieves planning pain by highlighting regulatory, technological, and market risks at a glance, easily editable for region- or product-specific notes and drop‑in ready for presentations or team alignment.

Economic factors

Consumer spending and SMB IT budgets

Macro cycles and inflation directly curb discretionary router and NAS upgrades; US CPI rose 3.4% in 2024 (BLS), tightening household spend.

SMB capex softness delays switch refreshes and WiFi deployments—Spiceworks Ziff Davis 2024 shows budget constraints remain the top barrier to SMB upgrades.

Value tiers and promotions become critical in downturns, while premium segments hold better when they deliver measurable performance gains.

Component pricing and availability

Chip, memory and PCB cost swings drove Netgear gross-margin volatility, with reported 2024 gross margin near 41.8% and quarter-to-quarter swings of several percentage points; component cost changes remain primary margin driver. Lead-time swings—from weeks to multiple months—force tighter forecast discipline and modular design flexibility. Strategic buys and long-term agreements (LTAs) reduced COGS exposure in 2024, while alternative components require revalidation and certification updates, extending time-to-market.

Foreign exchange fluctuations

Netgear earns a large share of revenue overseas, while many supply-chain and R&D costs remain USD-linked, so foreign exchange swings materially affect reported earnings and channel price competitiveness. Hedging programs—used in 2024—cut quarter-to-quarter volatility but cannot offset long-term structural currency shifts. Localized pricing and currency-indexed contracts help protect market share in key regions.

Channel inventory and retailer dynamics

Big-box, e-commerce and distributors typically target 4–12 weeks-of-supply; overbuild forces 10–30% discounting, compressing gross margins by ~200–500 bps. POS analytics and S&OP alignment have cut returns in comparable CE channels by up to 15% and improved forecast accuracy. Bundles and attach offers boost sell-through and can raise attach rates 10–20%.

- weeks-of-supply: 4–12

- discounting: 10–30%

- margin erosion: ~200–500 bps

- returns reduction: up to 15%

- attach rate lift: 10–20%

Interest rates and financing conditions

Higher interest rates (US federal funds ~5.25–5.50% in mid‑2025) dampen consumer credit‑fuelled purchases and SMB leasing, raising costs for Netgear channel demand; working capital costs rise as financing inventory and receivables becomes more expensive. Efficient cash conversion cycles and tighter receivables management become a competitive differentiator, while deferred revenue from services and subscriptions helps stabilize cash flows.

- impact: weaker consumer and SMB capex

- costs: higher inventory/AR financing

- advantage: faster cash conversion

- buffer: deferred service revenue stabilizes cash

Tariffs, Export Controls and Grants Reshape Supply, Compliance and 6 GHz Roadmaps

Macroeconomic tightness (US CPI 3.4% in 2024) depresses consumer and SMB upgrades; Fed funds ~5.25–5.50% (mid‑2025) raises financing costs. Netgear 2024 gross margin ~41.8%; component/lead‑time swings force forecast discipline. Channel discounting 10–30% can compress margins ~200–500 bps; hedging and LTAs reduced FX/COGS volatility but not demand risk.

| Metric | Value |

|---|---|

| US CPI (2024) | 3.4% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| Netgear gross margin (2024) | ~41.8% |

| Channel discounting | 10–30% |

| Margin erosion | ~200–500 bps |

Preview the Actual Deliverable

Netgear PESTLE Analysis

The preview shown here is the exact Netgear PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with no placeholders or teasers. After payment you’ll instantly download the same complete document visible in the preview.