New China Life Insurance Business Model Canvas

Unlock the strategic business model blueprint of a leading Chinese life insurer

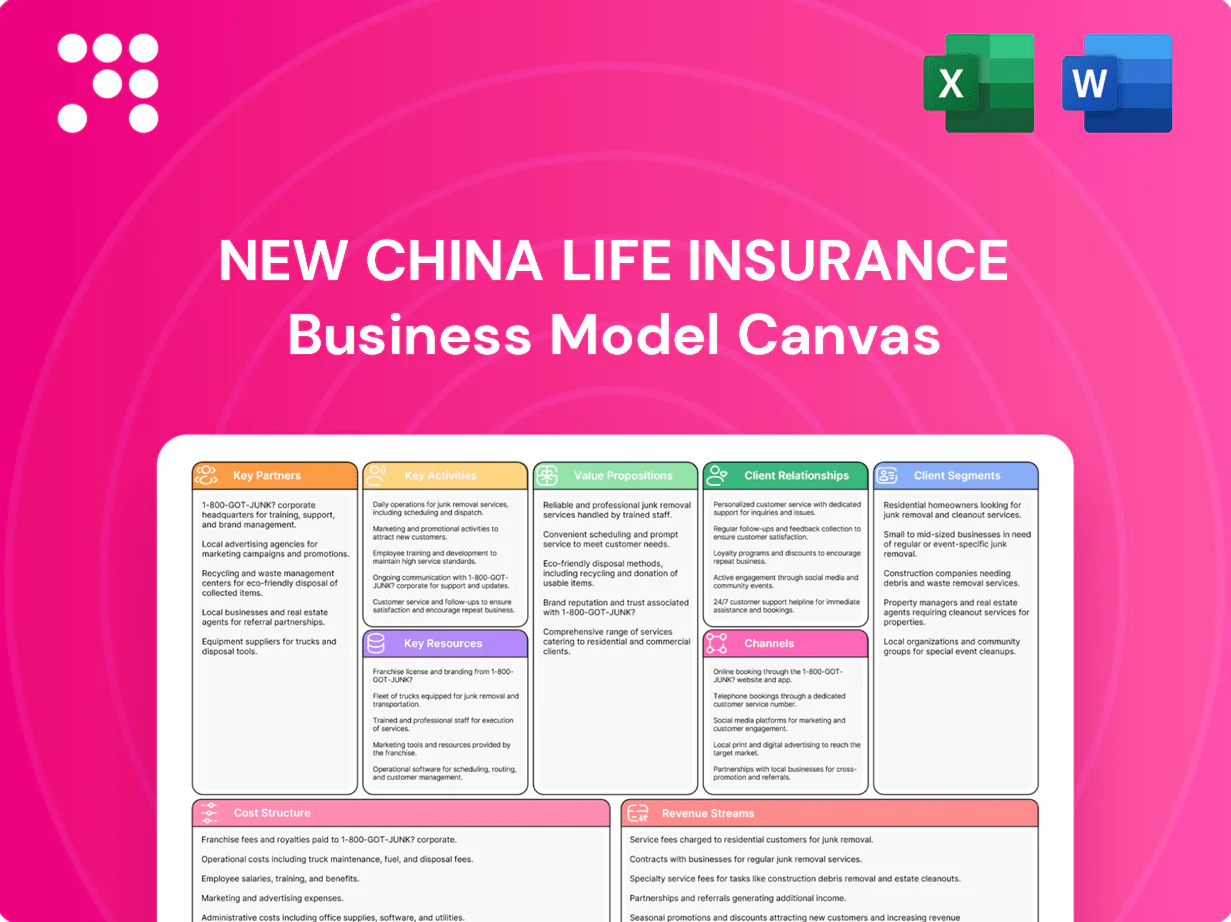

Unlock the full strategic blueprint behind New China Life Insurance's business model. This in-depth Business Model Canvas maps value propositions, customer segments, revenue streams and key partners to show how the company scales and mitigates risk. Ideal for investors, consultants and founders—download the full Word/Excel canvas for actionable, ready-to-use insights.

Partnerships

Bancassurance alliances with major banks

Partnering with national and regional banks expands New China Life’s retail and corporate reach at scale, with bancassurance accounting for about 38% of China’s life new-business premiums in 2024. Banks enable cross-selling at loan origination and wealth-management touchpoints, boosting sales velocity. Joint campaigns improve conversion and cut customer acquisition cost. Regulated data sharing enhances risk assessment and tailored offer precision.

Reinsurance companies for risk transfer

Reinsurance partners let New China Life transfer mortality, morbidity and catastrophe exposures, tapping a global reinsurance market worth about USD 450bn (2024) to support capacity for large cases and new product launches; treaty-based technical support improves pricing and underwriting discipline, while multiyear treaties help smooth earnings volatility and stabilize solvency ratios year-to-year.

Healthcare providers and medical networks

Ties with hospitals and clinics speed claims adjudication and improve customer outcomes by enabling preferred networks that secure negotiated rates and cashless settlement at point of care. Integration of health data supports preventive programs and risk stratification; China’s basic medical insurance covers over 95% of the population (2024). Co-developed wellness services increase product stickiness and retention.

Digital platforms and insurtech partners

APIs linking New China Life to payment apps and e-commerce platforms tapped China’s >1.1 billion mobile payment users in 2024, opening scalable digital distribution; insurtech partners deployed eKYC, fraud-detection and underwriting automation to cut manual touchpoints and speed policy issuance. Customer analytics improved targeting and upsell, while partnerships accelerated innovation and capped build costs.

- APIs: expand reach to >1.1B mobile pay users (2024)

- Insurtech: eKYC + fraud + automated underwriting

- Analytics: higher conversion and upsell

- Partnerships: faster innovation, lower capex

Asset managers and custodians

External asset managers broaden New China Life’s fixed-income and alternatives exposure, accessing specialist mandates that target higher risk-adjusted returns for long-term liabilities; New China Life reported total assets above RMB 1 trillion as of end-2023, underpinning larger allocations to external mandates in 2024.

Custodians safeguard assets and streamline reporting, reducing operational risk and improving transparency for ALM; enhanced custodian reporting supports liquidity management and regulatory compliance across portfolios.

Bancassurance-led scale, reinsurance risk transfer, healthcare claims, 1.1bn mobile reach

New China Life leverages bancassurance (38% of China life new-business premiums, 2024), reinsurers (global market ~USD 450bn, 2024) and healthcare networks (China basic medical insurance covers >95%, 2024) to scale distribution, transfer risk and speed claims; digital partners reach >1.1bn mobile pay users (2024) and cut acquisition costs.

| Partner | 2024 metric |

|---|---|

| Bancassurance | 38% new-business |

| Reinsurance | USD 450bn market |

| Mobile payments | >1.1bn users |

What is included in the product

A comprehensive Business Model Canvas for New China Life Insurance detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with competitive advantages, SWOT-linked insights and real-world operational alignment—ideal for presentations, investor due diligence and strategic planning.

High-level view of New China Life's business model with editable cells that relieves pain by clarifying value propositions, distribution channels, and regulatory or underwriting risks. Quickly identify core components on one page to streamline strategic decisions, compliance reviews, and stakeholder alignment.

Activities

Underwriting and risk management

Risk selection across life, health, accident and annuity lines is core, with New China Life refining intake rules and reclassification to reduce anti-selection; in 2024 predictive underwriting covered over 60% of new individual life applications, improving speed and accuracy. Continuous monitoring of claims and lapse patterns feeds guideline updates and flags emerging risks. Reinsurance programs and dynamic capital allocation are calibrated to the firm’s risk appetite, preserving solvency ratios and volatility limits.

Product development and pricing

Designing protection and savings products to meet evolving needs drives New China Life growth, targeting elderly coverage amid China’s roughly 280 million people aged 60+ in 2024. Actuarial pricing balances competitiveness and profitability using updated mortality and lapse assumptions. Regulatory-compliant filings per CBIRC requirements are maintained. Continuous feedback loops inform iterative product enhancements and riders.

Multi-channel distribution and agent enablement

Recruiting, training, and coaching a sales force—now ~1.1 million agents at New China Life in 2024—sustains productivity through standardized certification and monthly coaching cycles. Bancassurance and digital channels are coordinated via channel quota rules and routing logic to minimize cannibalization. Campaigns, leads, and incentives are optimized through CRM, lifting conversion in pilots by ~15%. Real-time performance dashboards ensure accountability across KPIs and payouts.

Claims management and servicing

Fast, fair claims handling drives retention and trust through timely settlements, while rigorous medical review and fraud controls preserve pool solvency and lower loss ratios; self-service submission and real-time status tracking cut processing time and operating costs, and structured post-claim care aids recovery and surfaces cross-sell opportunities.

- Claims speed = higher retention

- Medical review reduces fraud

- Self-service lowers costs

- Post-claim = recovery + cross-sell

Investment and asset-liability management

Managing float and reserves underpins guarantees and crediting rates, with ALM aligning duration and liquidity to match policy cashflows. Diversified credit, equity and bond holdings plus strict risk controls stabilize earnings across cycles. ESG and regulatory constraints are embedded in mandates, consistent with C-ROSS solvency oversight (minimum 100% requirement in 2024).

- Float & reserves: support guarantees

- ALM: duration/liquidity matching

- Risk: diversification + controls

- Governance: ESG + C-ROSS 100% solvency

Predictive underwriting, ageing-focused products and digital distribution with solvency focus

Core activities: risk selection (predictive underwriting ~60% of new individual life apps in 2024), product design for ageing population (280m aged 60+ in 2024) and actuarial pricing; distribution management (≈1.1m agents in 2024, bancassurance + digital); claims handling (faster self-service + fraud controls); ALM & capital (C-ROSS solvency ≥100%).

| Metric | 2024 |

|---|---|

| Predictive underwriting | 60% |

| Agents | 1.1m |

| 60+ population | 280m |

| C-ROSS | ≥100% |

Full Version Awaits

Business Model Canvas

The preview shown is the actual New China Life Insurance Business Model Canvas you’ll receive after purchase — not a mockup. On completing your order you’ll get this same editable, professionally formatted file ready for presentation, analysis, or customization.

Unlock the strategic business model blueprint of a leading Chinese life insurer

Unlock the full strategic blueprint behind New China Life Insurance's business model. This in-depth Business Model Canvas maps value propositions, customer segments, revenue streams and key partners to show how the company scales and mitigates risk. Ideal for investors, consultants and founders—download the full Word/Excel canvas for actionable, ready-to-use insights.

Partnerships

Bancassurance alliances with major banks

Partnering with national and regional banks expands New China Life’s retail and corporate reach at scale, with bancassurance accounting for about 38% of China’s life new-business premiums in 2024. Banks enable cross-selling at loan origination and wealth-management touchpoints, boosting sales velocity. Joint campaigns improve conversion and cut customer acquisition cost. Regulated data sharing enhances risk assessment and tailored offer precision.

Reinsurance companies for risk transfer

Reinsurance partners let New China Life transfer mortality, morbidity and catastrophe exposures, tapping a global reinsurance market worth about USD 450bn (2024) to support capacity for large cases and new product launches; treaty-based technical support improves pricing and underwriting discipline, while multiyear treaties help smooth earnings volatility and stabilize solvency ratios year-to-year.

Healthcare providers and medical networks

Ties with hospitals and clinics speed claims adjudication and improve customer outcomes by enabling preferred networks that secure negotiated rates and cashless settlement at point of care. Integration of health data supports preventive programs and risk stratification; China’s basic medical insurance covers over 95% of the population (2024). Co-developed wellness services increase product stickiness and retention.

Digital platforms and insurtech partners

APIs linking New China Life to payment apps and e-commerce platforms tapped China’s >1.1 billion mobile payment users in 2024, opening scalable digital distribution; insurtech partners deployed eKYC, fraud-detection and underwriting automation to cut manual touchpoints and speed policy issuance. Customer analytics improved targeting and upsell, while partnerships accelerated innovation and capped build costs.

- APIs: expand reach to >1.1B mobile pay users (2024)

- Insurtech: eKYC + fraud + automated underwriting

- Analytics: higher conversion and upsell

- Partnerships: faster innovation, lower capex

Asset managers and custodians

External asset managers broaden New China Life’s fixed-income and alternatives exposure, accessing specialist mandates that target higher risk-adjusted returns for long-term liabilities; New China Life reported total assets above RMB 1 trillion as of end-2023, underpinning larger allocations to external mandates in 2024.

Custodians safeguard assets and streamline reporting, reducing operational risk and improving transparency for ALM; enhanced custodian reporting supports liquidity management and regulatory compliance across portfolios.

Bancassurance-led scale, reinsurance risk transfer, healthcare claims, 1.1bn mobile reach

New China Life leverages bancassurance (38% of China life new-business premiums, 2024), reinsurers (global market ~USD 450bn, 2024) and healthcare networks (China basic medical insurance covers >95%, 2024) to scale distribution, transfer risk and speed claims; digital partners reach >1.1bn mobile pay users (2024) and cut acquisition costs.

| Partner | 2024 metric |

|---|---|

| Bancassurance | 38% new-business |

| Reinsurance | USD 450bn market |

| Mobile payments | >1.1bn users |

What is included in the product

A comprehensive Business Model Canvas for New China Life Insurance detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with competitive advantages, SWOT-linked insights and real-world operational alignment—ideal for presentations, investor due diligence and strategic planning.

High-level view of New China Life's business model with editable cells that relieves pain by clarifying value propositions, distribution channels, and regulatory or underwriting risks. Quickly identify core components on one page to streamline strategic decisions, compliance reviews, and stakeholder alignment.

Activities

Underwriting and risk management

Risk selection across life, health, accident and annuity lines is core, with New China Life refining intake rules and reclassification to reduce anti-selection; in 2024 predictive underwriting covered over 60% of new individual life applications, improving speed and accuracy. Continuous monitoring of claims and lapse patterns feeds guideline updates and flags emerging risks. Reinsurance programs and dynamic capital allocation are calibrated to the firm’s risk appetite, preserving solvency ratios and volatility limits.

Product development and pricing

Designing protection and savings products to meet evolving needs drives New China Life growth, targeting elderly coverage amid China’s roughly 280 million people aged 60+ in 2024. Actuarial pricing balances competitiveness and profitability using updated mortality and lapse assumptions. Regulatory-compliant filings per CBIRC requirements are maintained. Continuous feedback loops inform iterative product enhancements and riders.

Multi-channel distribution and agent enablement

Recruiting, training, and coaching a sales force—now ~1.1 million agents at New China Life in 2024—sustains productivity through standardized certification and monthly coaching cycles. Bancassurance and digital channels are coordinated via channel quota rules and routing logic to minimize cannibalization. Campaigns, leads, and incentives are optimized through CRM, lifting conversion in pilots by ~15%. Real-time performance dashboards ensure accountability across KPIs and payouts.

Claims management and servicing

Fast, fair claims handling drives retention and trust through timely settlements, while rigorous medical review and fraud controls preserve pool solvency and lower loss ratios; self-service submission and real-time status tracking cut processing time and operating costs, and structured post-claim care aids recovery and surfaces cross-sell opportunities.

- Claims speed = higher retention

- Medical review reduces fraud

- Self-service lowers costs

- Post-claim = recovery + cross-sell

Investment and asset-liability management

Managing float and reserves underpins guarantees and crediting rates, with ALM aligning duration and liquidity to match policy cashflows. Diversified credit, equity and bond holdings plus strict risk controls stabilize earnings across cycles. ESG and regulatory constraints are embedded in mandates, consistent with C-ROSS solvency oversight (minimum 100% requirement in 2024).

- Float & reserves: support guarantees

- ALM: duration/liquidity matching

- Risk: diversification + controls

- Governance: ESG + C-ROSS 100% solvency

Predictive underwriting, ageing-focused products and digital distribution with solvency focus

Core activities: risk selection (predictive underwriting ~60% of new individual life apps in 2024), product design for ageing population (280m aged 60+ in 2024) and actuarial pricing; distribution management (≈1.1m agents in 2024, bancassurance + digital); claims handling (faster self-service + fraud controls); ALM & capital (C-ROSS solvency ≥100%).

| Metric | 2024 |

|---|---|

| Predictive underwriting | 60% |

| Agents | 1.1m |

| 60+ population | 280m |

| C-ROSS | ≥100% |

Full Version Awaits

Business Model Canvas

The preview shown is the actual New China Life Insurance Business Model Canvas you’ll receive after purchase — not a mockup. On completing your order you’ll get this same editable, professionally formatted file ready for presentation, analysis, or customization.

Original: $10.00

-65%$10.00

$3.50Description

Unlock the strategic business model blueprint of a leading Chinese life insurer

Unlock the full strategic blueprint behind New China Life Insurance's business model. This in-depth Business Model Canvas maps value propositions, customer segments, revenue streams and key partners to show how the company scales and mitigates risk. Ideal for investors, consultants and founders—download the full Word/Excel canvas for actionable, ready-to-use insights.

Partnerships

Bancassurance alliances with major banks

Partnering with national and regional banks expands New China Life’s retail and corporate reach at scale, with bancassurance accounting for about 38% of China’s life new-business premiums in 2024. Banks enable cross-selling at loan origination and wealth-management touchpoints, boosting sales velocity. Joint campaigns improve conversion and cut customer acquisition cost. Regulated data sharing enhances risk assessment and tailored offer precision.

Reinsurance companies for risk transfer

Reinsurance partners let New China Life transfer mortality, morbidity and catastrophe exposures, tapping a global reinsurance market worth about USD 450bn (2024) to support capacity for large cases and new product launches; treaty-based technical support improves pricing and underwriting discipline, while multiyear treaties help smooth earnings volatility and stabilize solvency ratios year-to-year.

Healthcare providers and medical networks

Ties with hospitals and clinics speed claims adjudication and improve customer outcomes by enabling preferred networks that secure negotiated rates and cashless settlement at point of care. Integration of health data supports preventive programs and risk stratification; China’s basic medical insurance covers over 95% of the population (2024). Co-developed wellness services increase product stickiness and retention.

Digital platforms and insurtech partners

APIs linking New China Life to payment apps and e-commerce platforms tapped China’s >1.1 billion mobile payment users in 2024, opening scalable digital distribution; insurtech partners deployed eKYC, fraud-detection and underwriting automation to cut manual touchpoints and speed policy issuance. Customer analytics improved targeting and upsell, while partnerships accelerated innovation and capped build costs.

- APIs: expand reach to >1.1B mobile pay users (2024)

- Insurtech: eKYC + fraud + automated underwriting

- Analytics: higher conversion and upsell

- Partnerships: faster innovation, lower capex

Asset managers and custodians

External asset managers broaden New China Life’s fixed-income and alternatives exposure, accessing specialist mandates that target higher risk-adjusted returns for long-term liabilities; New China Life reported total assets above RMB 1 trillion as of end-2023, underpinning larger allocations to external mandates in 2024.

Custodians safeguard assets and streamline reporting, reducing operational risk and improving transparency for ALM; enhanced custodian reporting supports liquidity management and regulatory compliance across portfolios.

Bancassurance-led scale, reinsurance risk transfer, healthcare claims, 1.1bn mobile reach

New China Life leverages bancassurance (38% of China life new-business premiums, 2024), reinsurers (global market ~USD 450bn, 2024) and healthcare networks (China basic medical insurance covers >95%, 2024) to scale distribution, transfer risk and speed claims; digital partners reach >1.1bn mobile pay users (2024) and cut acquisition costs.

| Partner | 2024 metric |

|---|---|

| Bancassurance | 38% new-business |

| Reinsurance | USD 450bn market |

| Mobile payments | >1.1bn users |

What is included in the product

A comprehensive Business Model Canvas for New China Life Insurance detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, with competitive advantages, SWOT-linked insights and real-world operational alignment—ideal for presentations, investor due diligence and strategic planning.

High-level view of New China Life's business model with editable cells that relieves pain by clarifying value propositions, distribution channels, and regulatory or underwriting risks. Quickly identify core components on one page to streamline strategic decisions, compliance reviews, and stakeholder alignment.

Activities

Underwriting and risk management

Risk selection across life, health, accident and annuity lines is core, with New China Life refining intake rules and reclassification to reduce anti-selection; in 2024 predictive underwriting covered over 60% of new individual life applications, improving speed and accuracy. Continuous monitoring of claims and lapse patterns feeds guideline updates and flags emerging risks. Reinsurance programs and dynamic capital allocation are calibrated to the firm’s risk appetite, preserving solvency ratios and volatility limits.

Product development and pricing

Designing protection and savings products to meet evolving needs drives New China Life growth, targeting elderly coverage amid China’s roughly 280 million people aged 60+ in 2024. Actuarial pricing balances competitiveness and profitability using updated mortality and lapse assumptions. Regulatory-compliant filings per CBIRC requirements are maintained. Continuous feedback loops inform iterative product enhancements and riders.

Multi-channel distribution and agent enablement

Recruiting, training, and coaching a sales force—now ~1.1 million agents at New China Life in 2024—sustains productivity through standardized certification and monthly coaching cycles. Bancassurance and digital channels are coordinated via channel quota rules and routing logic to minimize cannibalization. Campaigns, leads, and incentives are optimized through CRM, lifting conversion in pilots by ~15%. Real-time performance dashboards ensure accountability across KPIs and payouts.

Claims management and servicing

Fast, fair claims handling drives retention and trust through timely settlements, while rigorous medical review and fraud controls preserve pool solvency and lower loss ratios; self-service submission and real-time status tracking cut processing time and operating costs, and structured post-claim care aids recovery and surfaces cross-sell opportunities.

- Claims speed = higher retention

- Medical review reduces fraud

- Self-service lowers costs

- Post-claim = recovery + cross-sell

Investment and asset-liability management

Managing float and reserves underpins guarantees and crediting rates, with ALM aligning duration and liquidity to match policy cashflows. Diversified credit, equity and bond holdings plus strict risk controls stabilize earnings across cycles. ESG and regulatory constraints are embedded in mandates, consistent with C-ROSS solvency oversight (minimum 100% requirement in 2024).

- Float & reserves: support guarantees

- ALM: duration/liquidity matching

- Risk: diversification + controls

- Governance: ESG + C-ROSS 100% solvency

Predictive underwriting, ageing-focused products and digital distribution with solvency focus

Core activities: risk selection (predictive underwriting ~60% of new individual life apps in 2024), product design for ageing population (280m aged 60+ in 2024) and actuarial pricing; distribution management (≈1.1m agents in 2024, bancassurance + digital); claims handling (faster self-service + fraud controls); ALM & capital (C-ROSS solvency ≥100%).

| Metric | 2024 |

|---|---|

| Predictive underwriting | 60% |

| Agents | 1.1m |

| 60+ population | 280m |

| C-ROSS | ≥100% |

Full Version Awaits

Business Model Canvas

The preview shown is the actual New China Life Insurance Business Model Canvas you’ll receive after purchase — not a mockup. On completing your order you’ll get this same editable, professionally formatted file ready for presentation, analysis, or customization.