NextEra Energy Partners PESTLE Analysis

Skip the Research. Get the Strategy.

Our PESTLE Analysis for NextEra Energy Partners reveals how political shifts, macroeconomics, and tech innovation shape its renewable-growth path, and highlights regulatory and environmental risks investors must track. This concise intelligence guides strategy and valuation decisions. Purchase the full report to access the complete, actionable breakdown and downloadable charts for immediate use.

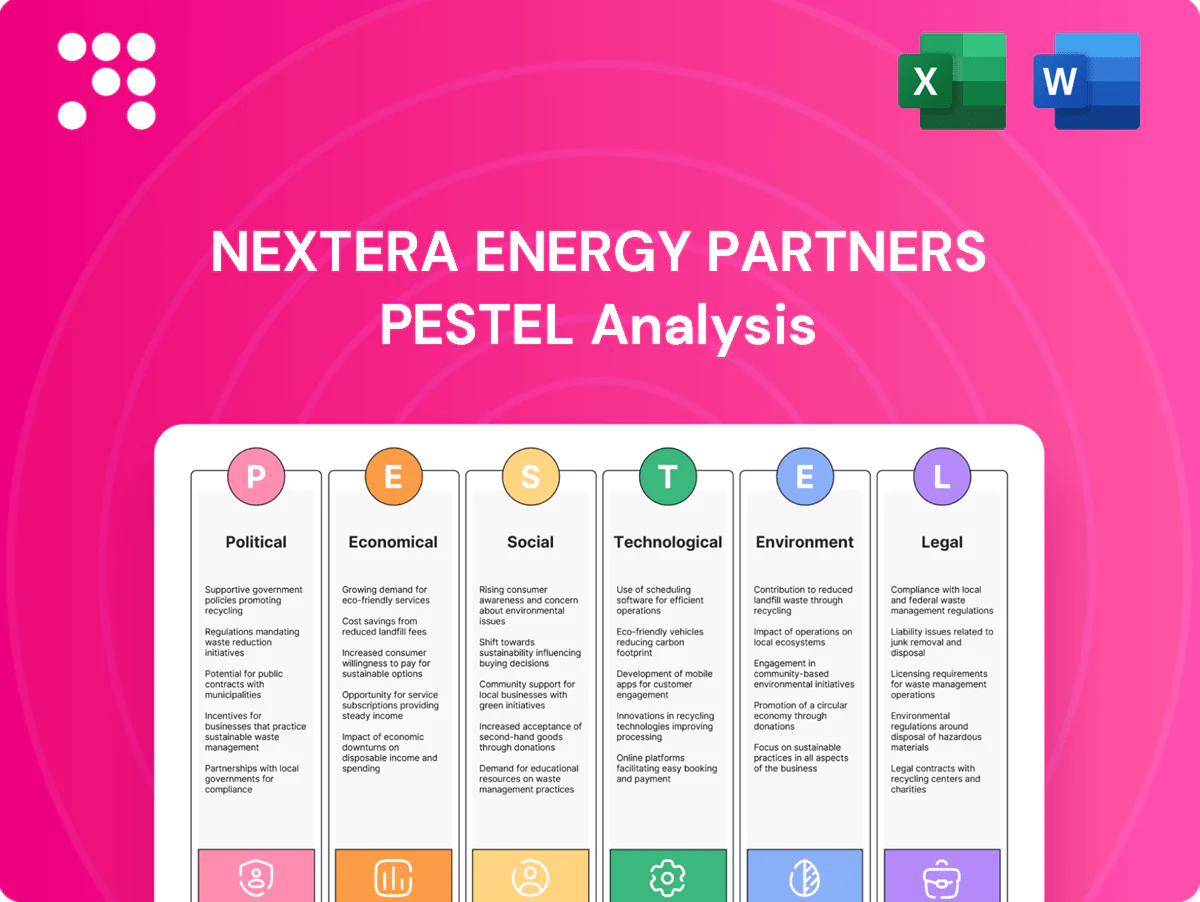

Political factors

Federal clean energy policy direction

The Inflation Reduction Act anchors long-dated tax incentives—roughly $369 billion in clean energy investments—supporting NEP’s wind, solar and storage economics through expanded ITC/PTC provisions and transferability/direct pay options running into the 2030s. Changes in administration priorities or delayed IRS guidance could alter implementation, funding timelines and dropdown cadence. Policy stability underpins NEP’s repowering plans and growth visibility; reversals or delays would compress projected cashflow and investor certainty.

State-level RPS and siting politics

State renewable portfolio standards (about 30 states plus DC) and 100% clean/zero-carbon targets (21 states plus DC as of 2025) drive PPA demand but vary widely in timelines and carve-outs. Gubernatorial and commission turnover can rapidly change approval dynamics after elections. Local council opposition or support frequently alters siting and permitting outcomes. NEP must prioritize projects in receptive jurisdictions to secure PPAs and interconnection.

Energy security and gas policy

Geopolitical tensions and supply security drive closer oversight of cross-border and LNG-linked pipelines, influencing demand patterns for firms like NextEra Energy Partners. Federal and state actions — e.g., EPA methane regulations tightened in 2024 and state-level new-gas hookup restrictions in California and New York — can compress pipeline cash flows or accelerate asset retirements. Transition mandates for methane controls raise capex and O&M needs; diversified asset positioning limits single-policy exposure.

Transmission and regional market governance

FERC orders and RTO/ISO rules determine interconnection queues, congestion management and curtailment; U.S. interconnection backlogs exceeded 1,000 GW by 2024, amplifying the value of effective queue reform. Pro-transmission policies and targeted transmission builds can unlock stranded value from existing assets and repowerings, increasing dispatch and revenue potential. Market rule changes that shift congestion and capacity payments can reallocate tens to hundreds of millions annually across generators and load, while regulatory predictability minimizes contract renegotiation risk for NextEra Energy Partners.

Trade and industrial policy

Tariffs, AD/CVD actions and domestic-content rules materially constrain solar and storage supply chains, raising lead times and capex for project developers. Buy American incentives can reduce tax-equity needs by enabling direct pay/credits but tend to increase procurement costs. Policy tweaks shift expected COD windows and dropdown pacing, so NEP must hedge procurement, supply contracts and timing against regulatory volatility.

- Tariffs/AD/CVD: supply risk

- Domestic content: higher capex, lower tax-equity

- Buy American: less tax-equity, more cost

- Action: hedge procurement/timing

IRA's $369B incentives fuel clean PPAs; >1,000 GW backlog and tariffs risk timing

Inflation Reduction Act’s ~$369B clean-energy incentives and transferability/direct pay through the 2030s underpin NEP’s tax-equity and dropdown economics; shifting IRS guidance or administration priorities could change timing. State RPS and 100% clean targets (21 states + DC as of 2025) sustain PPA demand but create uneven siting risk. Interconnection backlog >1,000 GW (2024) and tariffs/Buy American pressure capex and lead times.

| Factor | 2024/25 datapoint |

|---|---|

| IRA funding | $369B |

| 100% clean states | 21 + DC (2025) |

| Interconnection backlog | >1,000 GW (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect NextEra Energy Partners across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis. Designed for executives, investors, and advisors to spot risks, opportunities, and support scenario-driven strategy and funding decisions.

A concise, visually segmented PESTLE summary of NextEra Energy Partners that can be dropped into presentations, edited with custom notes, and easily shared to streamline external risk and market-position discussions across teams.

Economic factors

Interest rates and cost of capital

Yield-oriented models like NextEra Energy Partners are highly rate-sensitive as the federal funds target (about 5.25–5.50% through 2024–25) and 10-year Treasury (near 4.3%) compress valuation multiples and raise refinancing costs. Higher long-term rates increase interest expense and pressure distribution coverage, while lower rates ease coverage and enable accretive acquisitions. NEP mitigates exposure through extensive hedging programs and laddered maturities disclosed in its filings, limiting short-term refinancing risk.

PPA prices and counterparty credit

NextEra Energy Partners’ long-term contracted revenues depend heavily on offtaker credit quality, with over 95% of cash flows backed by investment-grade utilities, CCAs or corporate counterparts as of 2024. Rising wholesale power and REC prices in 2023–2024 lifted new PPA bids and improved repower economics, compressing payback periods. Counterparty distress or renegotiations could materially impair cash flows and coverage ratios. Diversification across utilities and CCAs reduces concentration risk.

Tax equity and monetization

IRA transferability, effective January 1, 2023, broadened eligible buyers for ITC/PTC sales, changing transaction yields by opening cash-sale options beyond traditional tax equity partners. Market depth for transferable credits determines proceeds and timing, with industry reports showing heightened trading activity since 2023 as buyers diversify. Tight tax equity conditions in 2022–23 delayed some CODs or increased required returns, so efficient monetization is critical to support NextEra Energy Partners distribution growth targets.

Equipment and construction costs

Turbine, module, inverter and battery costs drive NEP project returns; BNEF estimates battery pack prices fell to about 120–132 USD/kWh in 2024, easing CAPEX pressure while global PV module prices dropped ~10–15% year-over-year. Freight and construction wages remained elevated—US construction wage inflation near 4–5% in 2024—pressuring schedules and margins; EPC availability tightens timelines, but NEP scale and NextEra affiliates secure preferential procurement and financing.

- Battery price 2024: ~120–132 USD/kWh (BNEF)

- PV module prices: -10–15% YoY in 2024

- Construction wage inflation: ~4–5% (2024)

- Risks: freight, EPC shortages, scheduling

- Mitigant: NEP scale + NextEra affiliate terms

Inflation and indexation

Inflation raises O&M, land-lease and insurance costs for NextEra Energy Partners; US CPI was 3.4% in 2024 (BLS). Contract escalators and pass-throughs limit margin erosion. Solar/module component prices fell roughly 20% from 2022–24 (BNEF), partially offsetting service inflation; prudent budgeting helps preserve coverage ratios.

- Inflation exposure: O&M, leases, insurance

- Mitigation: escalators/pass-throughs in contracts

- Offset: ~20% module price decline 2022–24

- Action: conservative budgeting to protect covenants

IRA's $369B incentives fuel clean PPAs; >1,000 GW backlog and tariffs risk timing

NEP is rate-sensitive: fed funds ~5.25–5.50% (2024–25) and 10yr ~4.3% compress multiples and raise refinancing costs, partially mitigated by hedges and laddered maturities. Over 95% of cash flows backed by investment-grade counterparties supports coverage despite commodity/REC price volatility. Declining battery/module costs (2022–24) and IRA transferability improve monetization and accretive growth.

| Metric | Value |

|---|---|

| Fed funds (2024–25) | 5.25–5.50% |

| 10yr Treasury (2024) | ~4.3% |

| Battery price (2024) | $120–132/kWh |

| PV module YoY (2024) | -10–15% |

| CPI (2024) | 3.4% |

| IG-backed cash flows | >95% |

What You See Is What You Get

NextEra Energy Partners PESTLE Analysis

The preview shown here is the exact, fully formatted NextEra Energy Partners PESTLE Analysis you’ll receive after purchase—no placeholders or teasers. It contains the complete political, economic, social, technological, legal and environmental assessment, professionally structured and ready to download immediately after payment.

Skip the Research. Get the Strategy.

Our PESTLE Analysis for NextEra Energy Partners reveals how political shifts, macroeconomics, and tech innovation shape its renewable-growth path, and highlights regulatory and environmental risks investors must track. This concise intelligence guides strategy and valuation decisions. Purchase the full report to access the complete, actionable breakdown and downloadable charts for immediate use.

Political factors

Federal clean energy policy direction

The Inflation Reduction Act anchors long-dated tax incentives—roughly $369 billion in clean energy investments—supporting NEP’s wind, solar and storage economics through expanded ITC/PTC provisions and transferability/direct pay options running into the 2030s. Changes in administration priorities or delayed IRS guidance could alter implementation, funding timelines and dropdown cadence. Policy stability underpins NEP’s repowering plans and growth visibility; reversals or delays would compress projected cashflow and investor certainty.

State-level RPS and siting politics

State renewable portfolio standards (about 30 states plus DC) and 100% clean/zero-carbon targets (21 states plus DC as of 2025) drive PPA demand but vary widely in timelines and carve-outs. Gubernatorial and commission turnover can rapidly change approval dynamics after elections. Local council opposition or support frequently alters siting and permitting outcomes. NEP must prioritize projects in receptive jurisdictions to secure PPAs and interconnection.

Energy security and gas policy

Geopolitical tensions and supply security drive closer oversight of cross-border and LNG-linked pipelines, influencing demand patterns for firms like NextEra Energy Partners. Federal and state actions — e.g., EPA methane regulations tightened in 2024 and state-level new-gas hookup restrictions in California and New York — can compress pipeline cash flows or accelerate asset retirements. Transition mandates for methane controls raise capex and O&M needs; diversified asset positioning limits single-policy exposure.

Transmission and regional market governance

FERC orders and RTO/ISO rules determine interconnection queues, congestion management and curtailment; U.S. interconnection backlogs exceeded 1,000 GW by 2024, amplifying the value of effective queue reform. Pro-transmission policies and targeted transmission builds can unlock stranded value from existing assets and repowerings, increasing dispatch and revenue potential. Market rule changes that shift congestion and capacity payments can reallocate tens to hundreds of millions annually across generators and load, while regulatory predictability minimizes contract renegotiation risk for NextEra Energy Partners.

Trade and industrial policy

Tariffs, AD/CVD actions and domestic-content rules materially constrain solar and storage supply chains, raising lead times and capex for project developers. Buy American incentives can reduce tax-equity needs by enabling direct pay/credits but tend to increase procurement costs. Policy tweaks shift expected COD windows and dropdown pacing, so NEP must hedge procurement, supply contracts and timing against regulatory volatility.

- Tariffs/AD/CVD: supply risk

- Domestic content: higher capex, lower tax-equity

- Buy American: less tax-equity, more cost

- Action: hedge procurement/timing

IRA's $369B incentives fuel clean PPAs; >1,000 GW backlog and tariffs risk timing

Inflation Reduction Act’s ~$369B clean-energy incentives and transferability/direct pay through the 2030s underpin NEP’s tax-equity and dropdown economics; shifting IRS guidance or administration priorities could change timing. State RPS and 100% clean targets (21 states + DC as of 2025) sustain PPA demand but create uneven siting risk. Interconnection backlog >1,000 GW (2024) and tariffs/Buy American pressure capex and lead times.

| Factor | 2024/25 datapoint |

|---|---|

| IRA funding | $369B |

| 100% clean states | 21 + DC (2025) |

| Interconnection backlog | >1,000 GW (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect NextEra Energy Partners across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis. Designed for executives, investors, and advisors to spot risks, opportunities, and support scenario-driven strategy and funding decisions.

A concise, visually segmented PESTLE summary of NextEra Energy Partners that can be dropped into presentations, edited with custom notes, and easily shared to streamline external risk and market-position discussions across teams.

Economic factors

Interest rates and cost of capital

Yield-oriented models like NextEra Energy Partners are highly rate-sensitive as the federal funds target (about 5.25–5.50% through 2024–25) and 10-year Treasury (near 4.3%) compress valuation multiples and raise refinancing costs. Higher long-term rates increase interest expense and pressure distribution coverage, while lower rates ease coverage and enable accretive acquisitions. NEP mitigates exposure through extensive hedging programs and laddered maturities disclosed in its filings, limiting short-term refinancing risk.

PPA prices and counterparty credit

NextEra Energy Partners’ long-term contracted revenues depend heavily on offtaker credit quality, with over 95% of cash flows backed by investment-grade utilities, CCAs or corporate counterparts as of 2024. Rising wholesale power and REC prices in 2023–2024 lifted new PPA bids and improved repower economics, compressing payback periods. Counterparty distress or renegotiations could materially impair cash flows and coverage ratios. Diversification across utilities and CCAs reduces concentration risk.

Tax equity and monetization

IRA transferability, effective January 1, 2023, broadened eligible buyers for ITC/PTC sales, changing transaction yields by opening cash-sale options beyond traditional tax equity partners. Market depth for transferable credits determines proceeds and timing, with industry reports showing heightened trading activity since 2023 as buyers diversify. Tight tax equity conditions in 2022–23 delayed some CODs or increased required returns, so efficient monetization is critical to support NextEra Energy Partners distribution growth targets.

Equipment and construction costs

Turbine, module, inverter and battery costs drive NEP project returns; BNEF estimates battery pack prices fell to about 120–132 USD/kWh in 2024, easing CAPEX pressure while global PV module prices dropped ~10–15% year-over-year. Freight and construction wages remained elevated—US construction wage inflation near 4–5% in 2024—pressuring schedules and margins; EPC availability tightens timelines, but NEP scale and NextEra affiliates secure preferential procurement and financing.

- Battery price 2024: ~120–132 USD/kWh (BNEF)

- PV module prices: -10–15% YoY in 2024

- Construction wage inflation: ~4–5% (2024)

- Risks: freight, EPC shortages, scheduling

- Mitigant: NEP scale + NextEra affiliate terms

Inflation and indexation

Inflation raises O&M, land-lease and insurance costs for NextEra Energy Partners; US CPI was 3.4% in 2024 (BLS). Contract escalators and pass-throughs limit margin erosion. Solar/module component prices fell roughly 20% from 2022–24 (BNEF), partially offsetting service inflation; prudent budgeting helps preserve coverage ratios.

- Inflation exposure: O&M, leases, insurance

- Mitigation: escalators/pass-throughs in contracts

- Offset: ~20% module price decline 2022–24

- Action: conservative budgeting to protect covenants

IRA's $369B incentives fuel clean PPAs; >1,000 GW backlog and tariffs risk timing

NEP is rate-sensitive: fed funds ~5.25–5.50% (2024–25) and 10yr ~4.3% compress multiples and raise refinancing costs, partially mitigated by hedges and laddered maturities. Over 95% of cash flows backed by investment-grade counterparties supports coverage despite commodity/REC price volatility. Declining battery/module costs (2022–24) and IRA transferability improve monetization and accretive growth.

| Metric | Value |

|---|---|

| Fed funds (2024–25) | 5.25–5.50% |

| 10yr Treasury (2024) | ~4.3% |

| Battery price (2024) | $120–132/kWh |

| PV module YoY (2024) | -10–15% |

| CPI (2024) | 3.4% |

| IG-backed cash flows | >95% |

What You See Is What You Get

NextEra Energy Partners PESTLE Analysis

The preview shown here is the exact, fully formatted NextEra Energy Partners PESTLE Analysis you’ll receive after purchase—no placeholders or teasers. It contains the complete political, economic, social, technological, legal and environmental assessment, professionally structured and ready to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE Analysis for NextEra Energy Partners reveals how political shifts, macroeconomics, and tech innovation shape its renewable-growth path, and highlights regulatory and environmental risks investors must track. This concise intelligence guides strategy and valuation decisions. Purchase the full report to access the complete, actionable breakdown and downloadable charts for immediate use.

Political factors

Federal clean energy policy direction

The Inflation Reduction Act anchors long-dated tax incentives—roughly $369 billion in clean energy investments—supporting NEP’s wind, solar and storage economics through expanded ITC/PTC provisions and transferability/direct pay options running into the 2030s. Changes in administration priorities or delayed IRS guidance could alter implementation, funding timelines and dropdown cadence. Policy stability underpins NEP’s repowering plans and growth visibility; reversals or delays would compress projected cashflow and investor certainty.

State-level RPS and siting politics

State renewable portfolio standards (about 30 states plus DC) and 100% clean/zero-carbon targets (21 states plus DC as of 2025) drive PPA demand but vary widely in timelines and carve-outs. Gubernatorial and commission turnover can rapidly change approval dynamics after elections. Local council opposition or support frequently alters siting and permitting outcomes. NEP must prioritize projects in receptive jurisdictions to secure PPAs and interconnection.

Energy security and gas policy

Geopolitical tensions and supply security drive closer oversight of cross-border and LNG-linked pipelines, influencing demand patterns for firms like NextEra Energy Partners. Federal and state actions — e.g., EPA methane regulations tightened in 2024 and state-level new-gas hookup restrictions in California and New York — can compress pipeline cash flows or accelerate asset retirements. Transition mandates for methane controls raise capex and O&M needs; diversified asset positioning limits single-policy exposure.

Transmission and regional market governance

FERC orders and RTO/ISO rules determine interconnection queues, congestion management and curtailment; U.S. interconnection backlogs exceeded 1,000 GW by 2024, amplifying the value of effective queue reform. Pro-transmission policies and targeted transmission builds can unlock stranded value from existing assets and repowerings, increasing dispatch and revenue potential. Market rule changes that shift congestion and capacity payments can reallocate tens to hundreds of millions annually across generators and load, while regulatory predictability minimizes contract renegotiation risk for NextEra Energy Partners.

Trade and industrial policy

Tariffs, AD/CVD actions and domestic-content rules materially constrain solar and storage supply chains, raising lead times and capex for project developers. Buy American incentives can reduce tax-equity needs by enabling direct pay/credits but tend to increase procurement costs. Policy tweaks shift expected COD windows and dropdown pacing, so NEP must hedge procurement, supply contracts and timing against regulatory volatility.

- Tariffs/AD/CVD: supply risk

- Domestic content: higher capex, lower tax-equity

- Buy American: less tax-equity, more cost

- Action: hedge procurement/timing

IRA's $369B incentives fuel clean PPAs; >1,000 GW backlog and tariffs risk timing

Inflation Reduction Act’s ~$369B clean-energy incentives and transferability/direct pay through the 2030s underpin NEP’s tax-equity and dropdown economics; shifting IRS guidance or administration priorities could change timing. State RPS and 100% clean targets (21 states + DC as of 2025) sustain PPA demand but create uneven siting risk. Interconnection backlog >1,000 GW (2024) and tariffs/Buy American pressure capex and lead times.

| Factor | 2024/25 datapoint |

|---|---|

| IRA funding | $369B |

| 100% clean states | 21 + DC (2025) |

| Interconnection backlog | >1,000 GW (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect NextEra Energy Partners across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and trend analysis. Designed for executives, investors, and advisors to spot risks, opportunities, and support scenario-driven strategy and funding decisions.

A concise, visually segmented PESTLE summary of NextEra Energy Partners that can be dropped into presentations, edited with custom notes, and easily shared to streamline external risk and market-position discussions across teams.

Economic factors

Interest rates and cost of capital

Yield-oriented models like NextEra Energy Partners are highly rate-sensitive as the federal funds target (about 5.25–5.50% through 2024–25) and 10-year Treasury (near 4.3%) compress valuation multiples and raise refinancing costs. Higher long-term rates increase interest expense and pressure distribution coverage, while lower rates ease coverage and enable accretive acquisitions. NEP mitigates exposure through extensive hedging programs and laddered maturities disclosed in its filings, limiting short-term refinancing risk.

PPA prices and counterparty credit

NextEra Energy Partners’ long-term contracted revenues depend heavily on offtaker credit quality, with over 95% of cash flows backed by investment-grade utilities, CCAs or corporate counterparts as of 2024. Rising wholesale power and REC prices in 2023–2024 lifted new PPA bids and improved repower economics, compressing payback periods. Counterparty distress or renegotiations could materially impair cash flows and coverage ratios. Diversification across utilities and CCAs reduces concentration risk.

Tax equity and monetization

IRA transferability, effective January 1, 2023, broadened eligible buyers for ITC/PTC sales, changing transaction yields by opening cash-sale options beyond traditional tax equity partners. Market depth for transferable credits determines proceeds and timing, with industry reports showing heightened trading activity since 2023 as buyers diversify. Tight tax equity conditions in 2022–23 delayed some CODs or increased required returns, so efficient monetization is critical to support NextEra Energy Partners distribution growth targets.

Equipment and construction costs

Turbine, module, inverter and battery costs drive NEP project returns; BNEF estimates battery pack prices fell to about 120–132 USD/kWh in 2024, easing CAPEX pressure while global PV module prices dropped ~10–15% year-over-year. Freight and construction wages remained elevated—US construction wage inflation near 4–5% in 2024—pressuring schedules and margins; EPC availability tightens timelines, but NEP scale and NextEra affiliates secure preferential procurement and financing.

- Battery price 2024: ~120–132 USD/kWh (BNEF)

- PV module prices: -10–15% YoY in 2024

- Construction wage inflation: ~4–5% (2024)

- Risks: freight, EPC shortages, scheduling

- Mitigant: NEP scale + NextEra affiliate terms

Inflation and indexation

Inflation raises O&M, land-lease and insurance costs for NextEra Energy Partners; US CPI was 3.4% in 2024 (BLS). Contract escalators and pass-throughs limit margin erosion. Solar/module component prices fell roughly 20% from 2022–24 (BNEF), partially offsetting service inflation; prudent budgeting helps preserve coverage ratios.

- Inflation exposure: O&M, leases, insurance

- Mitigation: escalators/pass-throughs in contracts

- Offset: ~20% module price decline 2022–24

- Action: conservative budgeting to protect covenants

IRA's $369B incentives fuel clean PPAs; >1,000 GW backlog and tariffs risk timing

NEP is rate-sensitive: fed funds ~5.25–5.50% (2024–25) and 10yr ~4.3% compress multiples and raise refinancing costs, partially mitigated by hedges and laddered maturities. Over 95% of cash flows backed by investment-grade counterparties supports coverage despite commodity/REC price volatility. Declining battery/module costs (2022–24) and IRA transferability improve monetization and accretive growth.

| Metric | Value |

|---|---|

| Fed funds (2024–25) | 5.25–5.50% |

| 10yr Treasury (2024) | ~4.3% |

| Battery price (2024) | $120–132/kWh |

| PV module YoY (2024) | -10–15% |

| CPI (2024) | 3.4% |

| IG-backed cash flows | >95% |

What You See Is What You Get

NextEra Energy Partners PESTLE Analysis

The preview shown here is the exact, fully formatted NextEra Energy Partners PESTLE Analysis you’ll receive after purchase—no placeholders or teasers. It contains the complete political, economic, social, technological, legal and environmental assessment, professionally structured and ready to download immediately after payment.