NICE Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

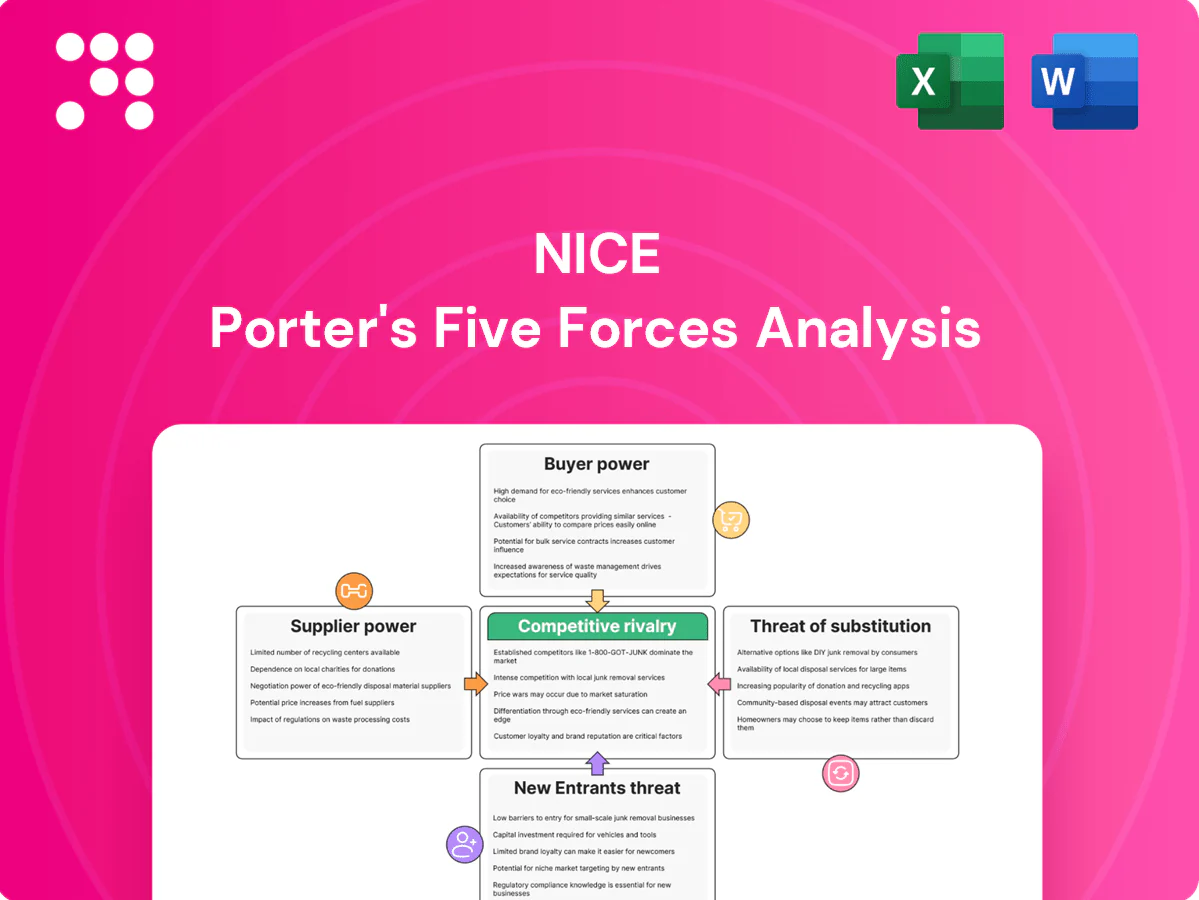

NICE’s Porter's Five Forces snapshot highlights the key competitive dynamics shaping its market, from supplier and buyer power to threat of entrants and substitutes. It summarizes rivalry intensity and strategic pressures in a concise format. This brief preview scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Proprietary data providers

Data vendors for bureau, telecom and alternative feeds command premium fees—the alternative data market was estimated at $5.6B in 2024—and per-record charges typically range $0.01–$0.10, with multi-year exclusivity common. NICE’s models rely on longitudinal, high-quality feeds, increasing vendor dependence. Contractual usage rights can limit flexibility, though scale buying and multi-source redundancy often secure discounts exceeding 30% and reduce single-vendor leverage.

Cloud, AI, and core IT stacks

Hyperscalers and specialized ML tool vendors exert strong supplier power for NICE due to limited substitutes and high migration costs; Synergy Research Group reports 2024 market shares roughly AWS 33%, Azure 22%, GCP 10%, concentrating leverage. Strict performance, security, and compliance needs further lock in architectures and increase switching costs. Volume discounts and multi-cloud strategies can moderate pricing, while vendor roadmaps directly shape NICE’s product velocity and cost base.

Specialized analytics and engineering talent

Data scientists, model validators and cybersecurity experts are in short supply, with 2024 surveys showing roughly 60–65% of firms reporting hiring difficulties for AI/ML roles, elevating supplier power. Wage inflation and higher retention costs—compensation for top talent rising about 10–15% in 2023–24—compress margins and delay delivery timelines. Strong employer brands and internal academies lower dependency on external hires. Offshoring and partner ecosystems diversify supply but introduce coordination and security risk.

Regulatory and public data gatekeepers

Access to government registries, credit bureaus and identity databases is permissioned and tightly rule-bound; policy shifts in 2024 have shown access terms can change with little notice, affecting data pricing and allowable use. Firms must invest in compliance, governance and vendor relationships to retain access and absorb abrupt constraints. Strong governance reduces supplier-driven volatility.

- Regulated access: permissioned registries

- 2024 risk: abrupt policy/pricing shifts

- Required: ongoing compliance investment

- Mitigation: deep supplier governance

Payment and banking infrastructure partners

Networks and core banking providers underpin fintech and risk platforms, with Visa and Mastercard accounting for roughly 75–80% of global card scheme share in 2024, giving them pricing and rule-setting leverage; certification, uptime SLAs (commonly 99.99%) and scheme rules reinforce that power. Co-development deals (often 3–7 year contracts) create mutual dependence that can stabilize commercial terms, while adding alternative rails and real-time schemes (140+ real-time systems by 2024) reduces concentration risk.

- Scheme share: Visa/Mastercard ~75–80% (2024)

- Typical SLA: 99.99%

- Co-dev contracts: 3–7 years

- Real-time rails: 140+ systems (2024)

High supplier leverage: alt-data $5.6B, cloud & card concentration raises costs

Suppliers (data vendors, hyperscalers, talent, schemes, registries) exert medium–high bargaining power: alt-data market $5.6B (2024), cloud share AWS33%/Azure22%/GCP10% (2024), Visa+MC ~75–80% (2024). High switching costs, exclusivity and regulatory access increase leverage; scale buying, multi-source redundancy and governance mitigate risk.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| Data vendors | $5.6B market; $0.01–$0.10/record | Pricing/exclusivity | Multi-source, scale discounts |

| Hyperscalers | AWS33%/Azure22%/GCP10% | Lock‑in, roadmap risk | Multi‑cloud |

What is included in the product

Concise Porter's Five Forces analysis tailored to NICE, revealing competitive intensity, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary and editable Word format for investor decks and internal strategy use.

A concise one-sheet that visualizes all five forces with editable pressure levels and an instant radar chart—ready to drop into decks, duplicate for scenarios, or attach to reports for faster strategic decisions.

Customers Bargaining Power

Large financial institutions’ procurement clout

Banks, insurers and card issuers use large RFPs to extract price discounts and bespoke SLAs, forcing NICE to absorb lower margins; in 2024 sales cycles commonly span 12–24 months with strict validation, raising cost-to-serve. Multi-year deals (often 3–5 years) and reference clients stabilize revenue, while cross-selling ratings, data and fintech services can rebalance buyer power.

Multi-homing across bureaus and raters

Clients commonly multi-home: 2024 industry surveys report roughly 60% of lenders benchmark across two or more credit bureaus and raters, raising price sensitivity and lowering switching costs on incremental spend. Clear performance differentiation is required to defend premium pricing; firms without demonstrable lift see churn. Bundled analytics, scorecards and APIs increase stickiness by integrating into workflows and raising migration costs.

Price transparency and outcome-based demands

Buyers increasingly press NICE for usage-based pricing tied to approvals, losses, or AUC lifts, reflecting a 2024 procurement shift toward outcomes contracts in tech and health buyers. Benchmarking against global peers (industry discount ranges ~15–25% in 2024) sharpens negotiation leverage. Demonstrable ROI and regulatory credibility—backed by NICE’s FY2024 revenue near $1.9bn—help sustain pricing. Bundled value-add services limit commoditization.

Integration switching frictions

Deep workflow integrations into LOS, core banking and ERP create strong exit frictions: re-integration and revalidation often mean months of work and material cost, curbing buyer leverage post-implementation. Open APIs and modular architectures—adopted by over 70% of major banks by 2024—lower trial barriers, but ongoing product innovation is required to justify retention.

- Exit friction: high re-integration/revalidation costs

- Retention: needs continuous product innovation

- Counterforce: open APIs/modularity (70%+ adoption in 2024)

Consumer and SME segments’ sensitivity

Retail and SME users are highly price- and experience-sensitive, with 2024 surveys indicating roughly 65% of buyers prioritize cost and UX when choosing information services, pressuring fee structures for vendors like NICE. Strong data privacy expectations now sway vendor choice and can be a differentiator in procurement. Simple, rapid onboarding increases conversion rates; tiered pricing expands retail/SME reach without eroding enterprise margins.

- Price/UX sensitivity ~65% (2024)

- Data privacy a key selection factor

- Fast onboarding boosts adoption

- Tiered pricing preserves enterprise ARPU

RFPs 12–24m, discounts 15–25%, >70% API adoption, FY24 $1.9bn

B2B buyers exert strong leverage: 12–24 month RFPs and 15–25% discounts in 2024 compress margins, while multi-homing (~60%) raises price sensitivity. Deep LOS/ERP integrations and FY2024 revenue ~$1.9bn create retention friction, but 70%+ API adoption and 65% price/UX sensitivity force continuous innovation and outcome-linked pricing.

| Metric | 2024 |

|---|---|

| Sales cycle | 12–24 months |

| Discount range | 15–25% |

| Multi-home | ~60% |

| API adoption | >70% |

| Price/UX sensitivity | ~65% |

| FY revenue | ~$1.9bn |

Preview the Actual Deliverable

NICE Porter's Five Forces Analysis

This preview shows the exact NICE Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable; once payment is complete you'll get instant access to this identical file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

NICE’s Porter's Five Forces snapshot highlights the key competitive dynamics shaping its market, from supplier and buyer power to threat of entrants and substitutes. It summarizes rivalry intensity and strategic pressures in a concise format. This brief preview scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Proprietary data providers

Data vendors for bureau, telecom and alternative feeds command premium fees—the alternative data market was estimated at $5.6B in 2024—and per-record charges typically range $0.01–$0.10, with multi-year exclusivity common. NICE’s models rely on longitudinal, high-quality feeds, increasing vendor dependence. Contractual usage rights can limit flexibility, though scale buying and multi-source redundancy often secure discounts exceeding 30% and reduce single-vendor leverage.

Cloud, AI, and core IT stacks

Hyperscalers and specialized ML tool vendors exert strong supplier power for NICE due to limited substitutes and high migration costs; Synergy Research Group reports 2024 market shares roughly AWS 33%, Azure 22%, GCP 10%, concentrating leverage. Strict performance, security, and compliance needs further lock in architectures and increase switching costs. Volume discounts and multi-cloud strategies can moderate pricing, while vendor roadmaps directly shape NICE’s product velocity and cost base.

Specialized analytics and engineering talent

Data scientists, model validators and cybersecurity experts are in short supply, with 2024 surveys showing roughly 60–65% of firms reporting hiring difficulties for AI/ML roles, elevating supplier power. Wage inflation and higher retention costs—compensation for top talent rising about 10–15% in 2023–24—compress margins and delay delivery timelines. Strong employer brands and internal academies lower dependency on external hires. Offshoring and partner ecosystems diversify supply but introduce coordination and security risk.

Regulatory and public data gatekeepers

Access to government registries, credit bureaus and identity databases is permissioned and tightly rule-bound; policy shifts in 2024 have shown access terms can change with little notice, affecting data pricing and allowable use. Firms must invest in compliance, governance and vendor relationships to retain access and absorb abrupt constraints. Strong governance reduces supplier-driven volatility.

- Regulated access: permissioned registries

- 2024 risk: abrupt policy/pricing shifts

- Required: ongoing compliance investment

- Mitigation: deep supplier governance

Payment and banking infrastructure partners

Networks and core banking providers underpin fintech and risk platforms, with Visa and Mastercard accounting for roughly 75–80% of global card scheme share in 2024, giving them pricing and rule-setting leverage; certification, uptime SLAs (commonly 99.99%) and scheme rules reinforce that power. Co-development deals (often 3–7 year contracts) create mutual dependence that can stabilize commercial terms, while adding alternative rails and real-time schemes (140+ real-time systems by 2024) reduces concentration risk.

- Scheme share: Visa/Mastercard ~75–80% (2024)

- Typical SLA: 99.99%

- Co-dev contracts: 3–7 years

- Real-time rails: 140+ systems (2024)

High supplier leverage: alt-data $5.6B, cloud & card concentration raises costs

Suppliers (data vendors, hyperscalers, talent, schemes, registries) exert medium–high bargaining power: alt-data market $5.6B (2024), cloud share AWS33%/Azure22%/GCP10% (2024), Visa+MC ~75–80% (2024). High switching costs, exclusivity and regulatory access increase leverage; scale buying, multi-source redundancy and governance mitigate risk.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| Data vendors | $5.6B market; $0.01–$0.10/record | Pricing/exclusivity | Multi-source, scale discounts |

| Hyperscalers | AWS33%/Azure22%/GCP10% | Lock‑in, roadmap risk | Multi‑cloud |

What is included in the product

Concise Porter's Five Forces analysis tailored to NICE, revealing competitive intensity, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary and editable Word format for investor decks and internal strategy use.

A concise one-sheet that visualizes all five forces with editable pressure levels and an instant radar chart—ready to drop into decks, duplicate for scenarios, or attach to reports for faster strategic decisions.

Customers Bargaining Power

Large financial institutions’ procurement clout

Banks, insurers and card issuers use large RFPs to extract price discounts and bespoke SLAs, forcing NICE to absorb lower margins; in 2024 sales cycles commonly span 12–24 months with strict validation, raising cost-to-serve. Multi-year deals (often 3–5 years) and reference clients stabilize revenue, while cross-selling ratings, data and fintech services can rebalance buyer power.

Multi-homing across bureaus and raters

Clients commonly multi-home: 2024 industry surveys report roughly 60% of lenders benchmark across two or more credit bureaus and raters, raising price sensitivity and lowering switching costs on incremental spend. Clear performance differentiation is required to defend premium pricing; firms without demonstrable lift see churn. Bundled analytics, scorecards and APIs increase stickiness by integrating into workflows and raising migration costs.

Price transparency and outcome-based demands

Buyers increasingly press NICE for usage-based pricing tied to approvals, losses, or AUC lifts, reflecting a 2024 procurement shift toward outcomes contracts in tech and health buyers. Benchmarking against global peers (industry discount ranges ~15–25% in 2024) sharpens negotiation leverage. Demonstrable ROI and regulatory credibility—backed by NICE’s FY2024 revenue near $1.9bn—help sustain pricing. Bundled value-add services limit commoditization.

Integration switching frictions

Deep workflow integrations into LOS, core banking and ERP create strong exit frictions: re-integration and revalidation often mean months of work and material cost, curbing buyer leverage post-implementation. Open APIs and modular architectures—adopted by over 70% of major banks by 2024—lower trial barriers, but ongoing product innovation is required to justify retention.

- Exit friction: high re-integration/revalidation costs

- Retention: needs continuous product innovation

- Counterforce: open APIs/modularity (70%+ adoption in 2024)

Consumer and SME segments’ sensitivity

Retail and SME users are highly price- and experience-sensitive, with 2024 surveys indicating roughly 65% of buyers prioritize cost and UX when choosing information services, pressuring fee structures for vendors like NICE. Strong data privacy expectations now sway vendor choice and can be a differentiator in procurement. Simple, rapid onboarding increases conversion rates; tiered pricing expands retail/SME reach without eroding enterprise margins.

- Price/UX sensitivity ~65% (2024)

- Data privacy a key selection factor

- Fast onboarding boosts adoption

- Tiered pricing preserves enterprise ARPU

RFPs 12–24m, discounts 15–25%, >70% API adoption, FY24 $1.9bn

B2B buyers exert strong leverage: 12–24 month RFPs and 15–25% discounts in 2024 compress margins, while multi-homing (~60%) raises price sensitivity. Deep LOS/ERP integrations and FY2024 revenue ~$1.9bn create retention friction, but 70%+ API adoption and 65% price/UX sensitivity force continuous innovation and outcome-linked pricing.

| Metric | 2024 |

|---|---|

| Sales cycle | 12–24 months |

| Discount range | 15–25% |

| Multi-home | ~60% |

| API adoption | >70% |

| Price/UX sensitivity | ~65% |

| FY revenue | ~$1.9bn |

Preview the Actual Deliverable

NICE Porter's Five Forces Analysis

This preview shows the exact NICE Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable; once payment is complete you'll get instant access to this identical file.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

NICE’s Porter's Five Forces snapshot highlights the key competitive dynamics shaping its market, from supplier and buyer power to threat of entrants and substitutes. It summarizes rivalry intensity and strategic pressures in a concise format. This brief preview scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Proprietary data providers

Data vendors for bureau, telecom and alternative feeds command premium fees—the alternative data market was estimated at $5.6B in 2024—and per-record charges typically range $0.01–$0.10, with multi-year exclusivity common. NICE’s models rely on longitudinal, high-quality feeds, increasing vendor dependence. Contractual usage rights can limit flexibility, though scale buying and multi-source redundancy often secure discounts exceeding 30% and reduce single-vendor leverage.

Cloud, AI, and core IT stacks

Hyperscalers and specialized ML tool vendors exert strong supplier power for NICE due to limited substitutes and high migration costs; Synergy Research Group reports 2024 market shares roughly AWS 33%, Azure 22%, GCP 10%, concentrating leverage. Strict performance, security, and compliance needs further lock in architectures and increase switching costs. Volume discounts and multi-cloud strategies can moderate pricing, while vendor roadmaps directly shape NICE’s product velocity and cost base.

Specialized analytics and engineering talent

Data scientists, model validators and cybersecurity experts are in short supply, with 2024 surveys showing roughly 60–65% of firms reporting hiring difficulties for AI/ML roles, elevating supplier power. Wage inflation and higher retention costs—compensation for top talent rising about 10–15% in 2023–24—compress margins and delay delivery timelines. Strong employer brands and internal academies lower dependency on external hires. Offshoring and partner ecosystems diversify supply but introduce coordination and security risk.

Regulatory and public data gatekeepers

Access to government registries, credit bureaus and identity databases is permissioned and tightly rule-bound; policy shifts in 2024 have shown access terms can change with little notice, affecting data pricing and allowable use. Firms must invest in compliance, governance and vendor relationships to retain access and absorb abrupt constraints. Strong governance reduces supplier-driven volatility.

- Regulated access: permissioned registries

- 2024 risk: abrupt policy/pricing shifts

- Required: ongoing compliance investment

- Mitigation: deep supplier governance

Payment and banking infrastructure partners

Networks and core banking providers underpin fintech and risk platforms, with Visa and Mastercard accounting for roughly 75–80% of global card scheme share in 2024, giving them pricing and rule-setting leverage; certification, uptime SLAs (commonly 99.99%) and scheme rules reinforce that power. Co-development deals (often 3–7 year contracts) create mutual dependence that can stabilize commercial terms, while adding alternative rails and real-time schemes (140+ real-time systems by 2024) reduces concentration risk.

- Scheme share: Visa/Mastercard ~75–80% (2024)

- Typical SLA: 99.99%

- Co-dev contracts: 3–7 years

- Real-time rails: 140+ systems (2024)

High supplier leverage: alt-data $5.6B, cloud & card concentration raises costs

Suppliers (data vendors, hyperscalers, talent, schemes, registries) exert medium–high bargaining power: alt-data market $5.6B (2024), cloud share AWS33%/Azure22%/GCP10% (2024), Visa+MC ~75–80% (2024). High switching costs, exclusivity and regulatory access increase leverage; scale buying, multi-source redundancy and governance mitigate risk.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| Data vendors | $5.6B market; $0.01–$0.10/record | Pricing/exclusivity | Multi-source, scale discounts |

| Hyperscalers | AWS33%/Azure22%/GCP10% | Lock‑in, roadmap risk | Multi‑cloud |

What is included in the product

Concise Porter's Five Forces analysis tailored to NICE, revealing competitive intensity, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic commentary and editable Word format for investor decks and internal strategy use.

A concise one-sheet that visualizes all five forces with editable pressure levels and an instant radar chart—ready to drop into decks, duplicate for scenarios, or attach to reports for faster strategic decisions.

Customers Bargaining Power

Large financial institutions’ procurement clout

Banks, insurers and card issuers use large RFPs to extract price discounts and bespoke SLAs, forcing NICE to absorb lower margins; in 2024 sales cycles commonly span 12–24 months with strict validation, raising cost-to-serve. Multi-year deals (often 3–5 years) and reference clients stabilize revenue, while cross-selling ratings, data and fintech services can rebalance buyer power.

Multi-homing across bureaus and raters

Clients commonly multi-home: 2024 industry surveys report roughly 60% of lenders benchmark across two or more credit bureaus and raters, raising price sensitivity and lowering switching costs on incremental spend. Clear performance differentiation is required to defend premium pricing; firms without demonstrable lift see churn. Bundled analytics, scorecards and APIs increase stickiness by integrating into workflows and raising migration costs.

Price transparency and outcome-based demands

Buyers increasingly press NICE for usage-based pricing tied to approvals, losses, or AUC lifts, reflecting a 2024 procurement shift toward outcomes contracts in tech and health buyers. Benchmarking against global peers (industry discount ranges ~15–25% in 2024) sharpens negotiation leverage. Demonstrable ROI and regulatory credibility—backed by NICE’s FY2024 revenue near $1.9bn—help sustain pricing. Bundled value-add services limit commoditization.

Integration switching frictions

Deep workflow integrations into LOS, core banking and ERP create strong exit frictions: re-integration and revalidation often mean months of work and material cost, curbing buyer leverage post-implementation. Open APIs and modular architectures—adopted by over 70% of major banks by 2024—lower trial barriers, but ongoing product innovation is required to justify retention.

- Exit friction: high re-integration/revalidation costs

- Retention: needs continuous product innovation

- Counterforce: open APIs/modularity (70%+ adoption in 2024)

Consumer and SME segments’ sensitivity

Retail and SME users are highly price- and experience-sensitive, with 2024 surveys indicating roughly 65% of buyers prioritize cost and UX when choosing information services, pressuring fee structures for vendors like NICE. Strong data privacy expectations now sway vendor choice and can be a differentiator in procurement. Simple, rapid onboarding increases conversion rates; tiered pricing expands retail/SME reach without eroding enterprise margins.

- Price/UX sensitivity ~65% (2024)

- Data privacy a key selection factor

- Fast onboarding boosts adoption

- Tiered pricing preserves enterprise ARPU

RFPs 12–24m, discounts 15–25%, >70% API adoption, FY24 $1.9bn

B2B buyers exert strong leverage: 12–24 month RFPs and 15–25% discounts in 2024 compress margins, while multi-homing (~60%) raises price sensitivity. Deep LOS/ERP integrations and FY2024 revenue ~$1.9bn create retention friction, but 70%+ API adoption and 65% price/UX sensitivity force continuous innovation and outcome-linked pricing.

| Metric | 2024 |

|---|---|

| Sales cycle | 12–24 months |

| Discount range | 15–25% |

| Multi-home | ~60% |

| API adoption | >70% |

| Price/UX sensitivity | ~65% |

| FY revenue | ~$1.9bn |

Preview the Actual Deliverable

NICE Porter's Five Forces Analysis

This preview shows the exact NICE Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the final deliverable; once payment is complete you'll get instant access to this identical file.