Nippon Gas Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

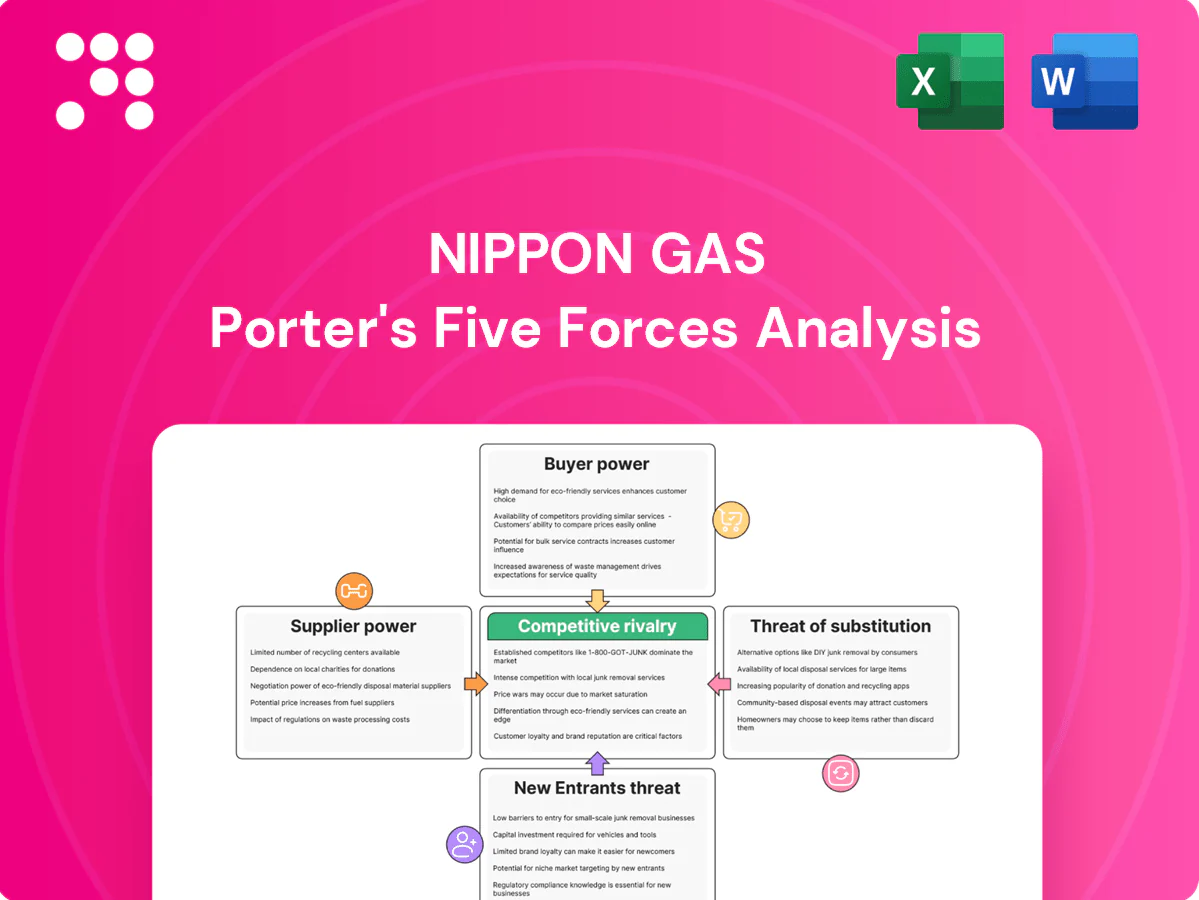

Nippon Gas faces moderate buyer power, concentrated suppliers, and rising regulatory and substitute pressures that reshape margins and growth prospects. This snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Nippon Gas’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated LPG import sources

Sourcing relies on a limited set of global LPG exporters—notably the US, Saudi Arabia, UAE, Qatar and Kuwait—raising dependence risk for Nippon Gas. Tight supply cycles or geopolitical shocks in these hubs can strengthen supplier leverage. Long-term offtake contracts provide stability, but index-linked pricing keeps margin exposure to global price swings. Diversification across Japanese ports and counterparties partially offsets this concentration.

City gas and power wholesale dependence

Wholesale LNG and electricity market moves drive input costs for City gas and power; 2024 JKM spot averaged about $9/MMBtu, while Japan wholesale power peaks exceeded ¥35/kWh in summer 2024, tightening margins. Grid access fees and balancing charges are largely non-negotiable and can add several percent to supply costs. Hedging and multi-market procurement lower but do not remove supplier leverage during peak volatility.

Equipment OEM and parts specificity

Gas meters, regulators and safety devices are typically supplied by specialized OEMs and must meet certification regimes such as MID in Europe, ANSI/AGA in the US and JIS in Japan, reducing interchangeable substitutes and increasing supplier leverage.

Japan had roughly 52–53 million households in 2024, concentrating demand and amplifying supplier influence for meter deployments.

Bulk purchasing programs and dual-sourcing strategies can blunt price pressure, but long-term lifecycle service contracts often lock in terms and sustain supplier bargaining power.

Regulatory and safety compliance inputs

Compliance-mandated materials and inspections narrow vendor options, concentrating buying power among certified suppliers. In 2024 certified-component premiums were reported around 10–20%, enabling suppliers to command higher margins. Mandatory audits and extensive documentation raise switching costs, while standardization initiatives are gradually lowering supplier leverage.

- Compliance narrows vendors

- Certified premiums 10–20% (2024)

- Audits increase switching frictions

- Standardization reduces leverage over time

Logistics and storage constraints

Logistics and storage constraints create supplier leverage for Nippon Gas because limited LPG storage, cylinder fleets, and road/sea transport capacity form recurring bottlenecks; seasonal winter demand spikes concentrate volume and raise logistics providers' bargaining power. Forward-positioning inventory reduces interruptions but ties up working capital, while digital route optimization and telematics have been shown to recover capacity and reduce trip costs.

- Storage bottlenecks: limited tank and cylinder availability

- Transport capacity: road/sea constraints amplify seasonal leverage

- Inventory trade-off: forward positioning frees supply but locks capital

- Tech mitigation: route optimization and telematics reduce logistics leverage

Japan LPG buyers hit by exporter concentration, $9/MMBtu

Nippon Gas faces high supplier power from concentrated global LPG exporters (US, Saudi, UAE, Qatar, Kuwait) and non-negotiable grid and logistics fees; 2024 JKM averaged about $9/MMBtu. Certified-component premiums ran 10–20% in 2024 and Japan had ~52.5M households, intensifying demand-side leverage. Hedging, dual-sourcing and tech reduce but do not remove supplier bargaining strength.

| Metric | 2024 |

|---|---|

| JKM spot | $9/MMBtu |

| Certified premium | 10–20% |

| Households | ~52.5M |

What is included in the product

Dissects competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and industry structure shaping Nippon Gas’s pricing, margins, and strategic position; identifies regulatory, infrastructure, and technological threats plus opportunities to reinforce incumbent advantages.

Clear one-sheet Porter's Five Forces for Nippon Gas—quickly pinpoint supplier/buyer power, entrant threats, substitutes and rivalry to remove strategic blind spots and speed board-level decisions.

Customers Bargaining Power

Fragmented residential customers

Households in Japan number about 53 million, making residential customers numerous and geographically dispersed, which limits individual bargaining power. Full retail gas liberalization since 2017 has eased switching among providers, increasing price sensitivity. Promotions and bundled services (electricity+gas) sway choices, while churn management and loyalty programs deployed by providers reduce overall buyer leverage.

Price-sensitive commercial accounts

Restaurants, small factories and property managers negotiate aggressively, with contract size and usage profiles granting them notable leverage over price and terms; in 2024 multi-bid processes and RFPs drove roughly 50% of new commercial gas contracts, intensifying price pressure. Brokers report average savings targets of 8–12% in negotiations, while Nippon Gas can counter by bundling value-added services and efficiency solutions to shift buying decisions beyond pure price.

Switching costs declining

Full retail liberalization of Japan’s power market in April 2016 and the emergence of over 900 retail entrants have lowered barriers to change, while digital onboarding and smart-meter data streamline supplier switches. This drives buyer power in power retail, pressuring margins for incumbents like Nippon Gas. Retention through high service reliability and bundled energy-plus services mitigates churn risk.

Information transparency rising

Demand elasticity varies by use

Demand elasticity varies by use: essential heating and cooking remain largely inelastic, limiting buyer leverage, while discretionary/process loads are more price-sensitive and can switch fuels or technologies; in 2024 increased efficiency adoption reduced volumes and broadened alternatives. Tailored plans that price by elasticity profile improve retention and margin capture.

- Essential loads: low elasticity, stable revenue

- Discretionary loads: higher elasticity, switching risk

- Efficiency uptake 2024: accelerates option set

- Pricing: align plans to elasticity to balance churn and ARPU

Buyers Gain Edge: 38% compare; RFPs now 50% of new deals

Households (≈53M) are numerous so individual leverage is low, but 38% used comparison sites in 2024, raising price sensitivity. Commercial clients drove ~50% of new contracts via RFPs in 2024 with typical savings targets of 8–12%, increasing pressure. Smart meters, liberalized markets (post‑2017) and efficiency uptake shift bargaining toward buyers, while essential loads remain relatively inelastic.

| Segment | 2024 metric | Impact |

|---|---|---|

| Households | 53M; 38% use comparison sites | Higher switching, low individual power |

| Commercial | ~50% via RFPs; 8–12% savings targets | Strong negotiation leverage |

| Load elasticity | Essential: low; Discretionary: rising | Mixed pricing power |

What You See Is What You Get

Nippon Gas Porter's Five Forces Analysis

This preview displays the complete Nippon Gas Porter's Five Forces Analysis — the exact, fully formatted document you will receive immediately after purchase. It is not a sample or excerpt; the file available for download is identical to what you see here. Ready for use in reports, presentations, or decision-making with no further setup required.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Nippon Gas faces moderate buyer power, concentrated suppliers, and rising regulatory and substitute pressures that reshape margins and growth prospects. This snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Nippon Gas’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated LPG import sources

Sourcing relies on a limited set of global LPG exporters—notably the US, Saudi Arabia, UAE, Qatar and Kuwait—raising dependence risk for Nippon Gas. Tight supply cycles or geopolitical shocks in these hubs can strengthen supplier leverage. Long-term offtake contracts provide stability, but index-linked pricing keeps margin exposure to global price swings. Diversification across Japanese ports and counterparties partially offsets this concentration.

City gas and power wholesale dependence

Wholesale LNG and electricity market moves drive input costs for City gas and power; 2024 JKM spot averaged about $9/MMBtu, while Japan wholesale power peaks exceeded ¥35/kWh in summer 2024, tightening margins. Grid access fees and balancing charges are largely non-negotiable and can add several percent to supply costs. Hedging and multi-market procurement lower but do not remove supplier leverage during peak volatility.

Equipment OEM and parts specificity

Gas meters, regulators and safety devices are typically supplied by specialized OEMs and must meet certification regimes such as MID in Europe, ANSI/AGA in the US and JIS in Japan, reducing interchangeable substitutes and increasing supplier leverage.

Japan had roughly 52–53 million households in 2024, concentrating demand and amplifying supplier influence for meter deployments.

Bulk purchasing programs and dual-sourcing strategies can blunt price pressure, but long-term lifecycle service contracts often lock in terms and sustain supplier bargaining power.

Regulatory and safety compliance inputs

Compliance-mandated materials and inspections narrow vendor options, concentrating buying power among certified suppliers. In 2024 certified-component premiums were reported around 10–20%, enabling suppliers to command higher margins. Mandatory audits and extensive documentation raise switching costs, while standardization initiatives are gradually lowering supplier leverage.

- Compliance narrows vendors

- Certified premiums 10–20% (2024)

- Audits increase switching frictions

- Standardization reduces leverage over time

Logistics and storage constraints

Logistics and storage constraints create supplier leverage for Nippon Gas because limited LPG storage, cylinder fleets, and road/sea transport capacity form recurring bottlenecks; seasonal winter demand spikes concentrate volume and raise logistics providers' bargaining power. Forward-positioning inventory reduces interruptions but ties up working capital, while digital route optimization and telematics have been shown to recover capacity and reduce trip costs.

- Storage bottlenecks: limited tank and cylinder availability

- Transport capacity: road/sea constraints amplify seasonal leverage

- Inventory trade-off: forward positioning frees supply but locks capital

- Tech mitigation: route optimization and telematics reduce logistics leverage

Japan LPG buyers hit by exporter concentration, $9/MMBtu

Nippon Gas faces high supplier power from concentrated global LPG exporters (US, Saudi, UAE, Qatar, Kuwait) and non-negotiable grid and logistics fees; 2024 JKM averaged about $9/MMBtu. Certified-component premiums ran 10–20% in 2024 and Japan had ~52.5M households, intensifying demand-side leverage. Hedging, dual-sourcing and tech reduce but do not remove supplier bargaining strength.

| Metric | 2024 |

|---|---|

| JKM spot | $9/MMBtu |

| Certified premium | 10–20% |

| Households | ~52.5M |

What is included in the product

Dissects competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and industry structure shaping Nippon Gas’s pricing, margins, and strategic position; identifies regulatory, infrastructure, and technological threats plus opportunities to reinforce incumbent advantages.

Clear one-sheet Porter's Five Forces for Nippon Gas—quickly pinpoint supplier/buyer power, entrant threats, substitutes and rivalry to remove strategic blind spots and speed board-level decisions.

Customers Bargaining Power

Fragmented residential customers

Households in Japan number about 53 million, making residential customers numerous and geographically dispersed, which limits individual bargaining power. Full retail gas liberalization since 2017 has eased switching among providers, increasing price sensitivity. Promotions and bundled services (electricity+gas) sway choices, while churn management and loyalty programs deployed by providers reduce overall buyer leverage.

Price-sensitive commercial accounts

Restaurants, small factories and property managers negotiate aggressively, with contract size and usage profiles granting them notable leverage over price and terms; in 2024 multi-bid processes and RFPs drove roughly 50% of new commercial gas contracts, intensifying price pressure. Brokers report average savings targets of 8–12% in negotiations, while Nippon Gas can counter by bundling value-added services and efficiency solutions to shift buying decisions beyond pure price.

Switching costs declining

Full retail liberalization of Japan’s power market in April 2016 and the emergence of over 900 retail entrants have lowered barriers to change, while digital onboarding and smart-meter data streamline supplier switches. This drives buyer power in power retail, pressuring margins for incumbents like Nippon Gas. Retention through high service reliability and bundled energy-plus services mitigates churn risk.

Information transparency rising

Demand elasticity varies by use

Demand elasticity varies by use: essential heating and cooking remain largely inelastic, limiting buyer leverage, while discretionary/process loads are more price-sensitive and can switch fuels or technologies; in 2024 increased efficiency adoption reduced volumes and broadened alternatives. Tailored plans that price by elasticity profile improve retention and margin capture.

- Essential loads: low elasticity, stable revenue

- Discretionary loads: higher elasticity, switching risk

- Efficiency uptake 2024: accelerates option set

- Pricing: align plans to elasticity to balance churn and ARPU

Buyers Gain Edge: 38% compare; RFPs now 50% of new deals

Households (≈53M) are numerous so individual leverage is low, but 38% used comparison sites in 2024, raising price sensitivity. Commercial clients drove ~50% of new contracts via RFPs in 2024 with typical savings targets of 8–12%, increasing pressure. Smart meters, liberalized markets (post‑2017) and efficiency uptake shift bargaining toward buyers, while essential loads remain relatively inelastic.

| Segment | 2024 metric | Impact |

|---|---|---|

| Households | 53M; 38% use comparison sites | Higher switching, low individual power |

| Commercial | ~50% via RFPs; 8–12% savings targets | Strong negotiation leverage |

| Load elasticity | Essential: low; Discretionary: rising | Mixed pricing power |

What You See Is What You Get

Nippon Gas Porter's Five Forces Analysis

This preview displays the complete Nippon Gas Porter's Five Forces Analysis — the exact, fully formatted document you will receive immediately after purchase. It is not a sample or excerpt; the file available for download is identical to what you see here. Ready for use in reports, presentations, or decision-making with no further setup required.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Nippon Gas faces moderate buyer power, concentrated suppliers, and rising regulatory and substitute pressures that reshape margins and growth prospects. This snapshot highlights key competitive tensions and strategic levers. Unlock the full Porter's Five Forces Analysis to explore Nippon Gas’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated LPG import sources

Sourcing relies on a limited set of global LPG exporters—notably the US, Saudi Arabia, UAE, Qatar and Kuwait—raising dependence risk for Nippon Gas. Tight supply cycles or geopolitical shocks in these hubs can strengthen supplier leverage. Long-term offtake contracts provide stability, but index-linked pricing keeps margin exposure to global price swings. Diversification across Japanese ports and counterparties partially offsets this concentration.

City gas and power wholesale dependence

Wholesale LNG and electricity market moves drive input costs for City gas and power; 2024 JKM spot averaged about $9/MMBtu, while Japan wholesale power peaks exceeded ¥35/kWh in summer 2024, tightening margins. Grid access fees and balancing charges are largely non-negotiable and can add several percent to supply costs. Hedging and multi-market procurement lower but do not remove supplier leverage during peak volatility.

Equipment OEM and parts specificity

Gas meters, regulators and safety devices are typically supplied by specialized OEMs and must meet certification regimes such as MID in Europe, ANSI/AGA in the US and JIS in Japan, reducing interchangeable substitutes and increasing supplier leverage.

Japan had roughly 52–53 million households in 2024, concentrating demand and amplifying supplier influence for meter deployments.

Bulk purchasing programs and dual-sourcing strategies can blunt price pressure, but long-term lifecycle service contracts often lock in terms and sustain supplier bargaining power.

Regulatory and safety compliance inputs

Compliance-mandated materials and inspections narrow vendor options, concentrating buying power among certified suppliers. In 2024 certified-component premiums were reported around 10–20%, enabling suppliers to command higher margins. Mandatory audits and extensive documentation raise switching costs, while standardization initiatives are gradually lowering supplier leverage.

- Compliance narrows vendors

- Certified premiums 10–20% (2024)

- Audits increase switching frictions

- Standardization reduces leverage over time

Logistics and storage constraints

Logistics and storage constraints create supplier leverage for Nippon Gas because limited LPG storage, cylinder fleets, and road/sea transport capacity form recurring bottlenecks; seasonal winter demand spikes concentrate volume and raise logistics providers' bargaining power. Forward-positioning inventory reduces interruptions but ties up working capital, while digital route optimization and telematics have been shown to recover capacity and reduce trip costs.

- Storage bottlenecks: limited tank and cylinder availability

- Transport capacity: road/sea constraints amplify seasonal leverage

- Inventory trade-off: forward positioning frees supply but locks capital

- Tech mitigation: route optimization and telematics reduce logistics leverage

Japan LPG buyers hit by exporter concentration, $9/MMBtu

Nippon Gas faces high supplier power from concentrated global LPG exporters (US, Saudi, UAE, Qatar, Kuwait) and non-negotiable grid and logistics fees; 2024 JKM averaged about $9/MMBtu. Certified-component premiums ran 10–20% in 2024 and Japan had ~52.5M households, intensifying demand-side leverage. Hedging, dual-sourcing and tech reduce but do not remove supplier bargaining strength.

| Metric | 2024 |

|---|---|

| JKM spot | $9/MMBtu |

| Certified premium | 10–20% |

| Households | ~52.5M |

What is included in the product

Dissects competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and industry structure shaping Nippon Gas’s pricing, margins, and strategic position; identifies regulatory, infrastructure, and technological threats plus opportunities to reinforce incumbent advantages.

Clear one-sheet Porter's Five Forces for Nippon Gas—quickly pinpoint supplier/buyer power, entrant threats, substitutes and rivalry to remove strategic blind spots and speed board-level decisions.

Customers Bargaining Power

Fragmented residential customers

Households in Japan number about 53 million, making residential customers numerous and geographically dispersed, which limits individual bargaining power. Full retail gas liberalization since 2017 has eased switching among providers, increasing price sensitivity. Promotions and bundled services (electricity+gas) sway choices, while churn management and loyalty programs deployed by providers reduce overall buyer leverage.

Price-sensitive commercial accounts

Restaurants, small factories and property managers negotiate aggressively, with contract size and usage profiles granting them notable leverage over price and terms; in 2024 multi-bid processes and RFPs drove roughly 50% of new commercial gas contracts, intensifying price pressure. Brokers report average savings targets of 8–12% in negotiations, while Nippon Gas can counter by bundling value-added services and efficiency solutions to shift buying decisions beyond pure price.

Switching costs declining

Full retail liberalization of Japan’s power market in April 2016 and the emergence of over 900 retail entrants have lowered barriers to change, while digital onboarding and smart-meter data streamline supplier switches. This drives buyer power in power retail, pressuring margins for incumbents like Nippon Gas. Retention through high service reliability and bundled energy-plus services mitigates churn risk.

Information transparency rising

Demand elasticity varies by use

Demand elasticity varies by use: essential heating and cooking remain largely inelastic, limiting buyer leverage, while discretionary/process loads are more price-sensitive and can switch fuels or technologies; in 2024 increased efficiency adoption reduced volumes and broadened alternatives. Tailored plans that price by elasticity profile improve retention and margin capture.

- Essential loads: low elasticity, stable revenue

- Discretionary loads: higher elasticity, switching risk

- Efficiency uptake 2024: accelerates option set

- Pricing: align plans to elasticity to balance churn and ARPU

Buyers Gain Edge: 38% compare; RFPs now 50% of new deals

Households (≈53M) are numerous so individual leverage is low, but 38% used comparison sites in 2024, raising price sensitivity. Commercial clients drove ~50% of new contracts via RFPs in 2024 with typical savings targets of 8–12%, increasing pressure. Smart meters, liberalized markets (post‑2017) and efficiency uptake shift bargaining toward buyers, while essential loads remain relatively inelastic.

| Segment | 2024 metric | Impact |

|---|---|---|

| Households | 53M; 38% use comparison sites | Higher switching, low individual power |

| Commercial | ~50% via RFPs; 8–12% savings targets | Strong negotiation leverage |

| Load elasticity | Essential: low; Discretionary: rising | Mixed pricing power |

What You See Is What You Get

Nippon Gas Porter's Five Forces Analysis

This preview displays the complete Nippon Gas Porter's Five Forces Analysis — the exact, fully formatted document you will receive immediately after purchase. It is not a sample or excerpt; the file available for download is identical to what you see here. Ready for use in reports, presentations, or decision-making with no further setup required.