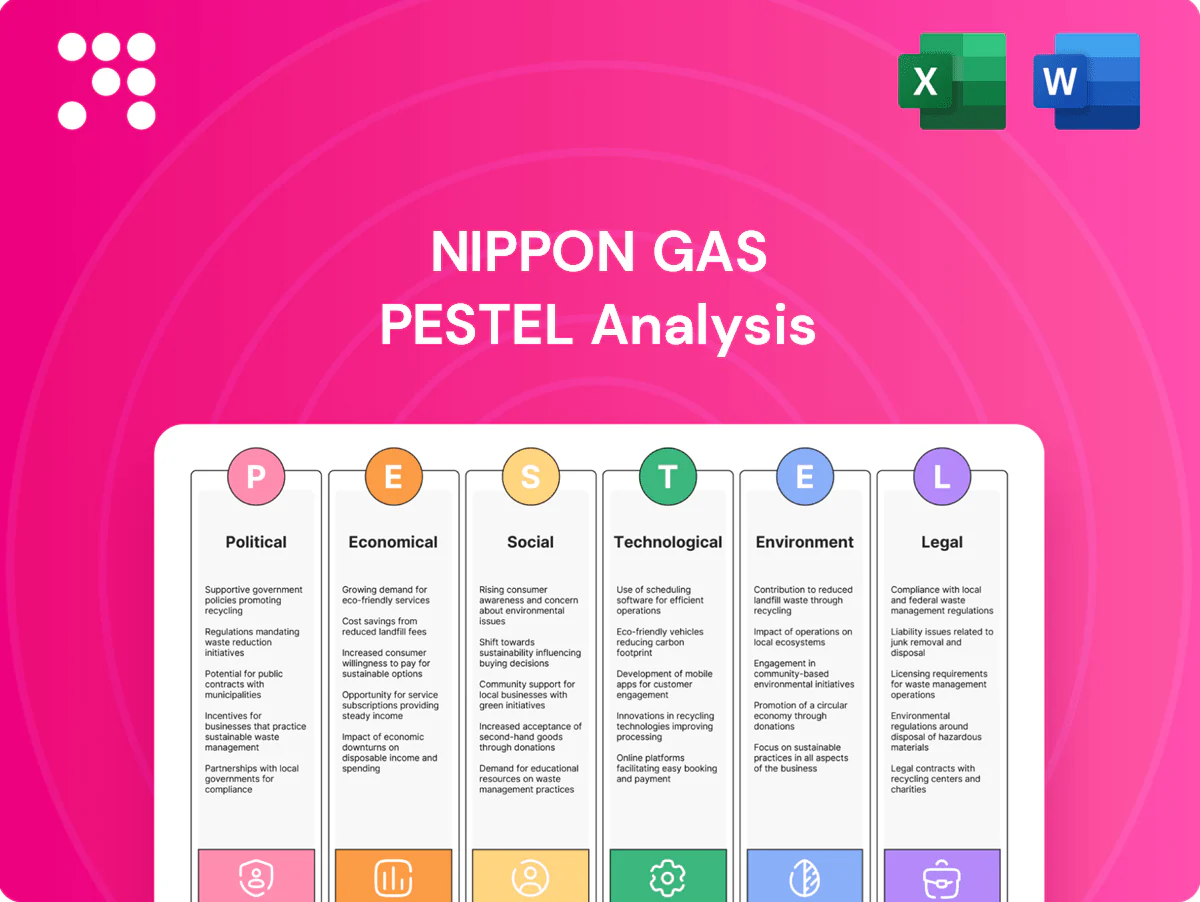

Nippon Gas PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic trends, and environmental regulations are reshaping Nippon Gas with our tailored PESTLE Analysis—insightful, up-to-date, and crafted for decision-makers. Buy the full report to access actionable intelligence, ready-to-use charts, and strategic recommendations you can apply immediately.

Political factors

Energy transition commitments

Japan’s 2050 net-zero goal and 46% GHG reduction target for 2030 (vs 2013) drive subsidies, standards and timetables for gas decarbonization; policy tilts to electrification and a 36–38% renewables share by 2030, squeezing LP/city gas demand. Nippon Gas can shift to efficiency services, biopropane/RNG pilots and green power supply; early compliance captures incentives and reduces transition risk.

Market liberalization dynamics

Japan opened electricity retail to competition in April 2016 and gas in April 2017, spurring hundreds of new entrants and higher customer churn; retail switching rates rose substantially as consumers sought bundled deals. Policymakers and regulators (METI, Fair Trade Commission) back cross-selling of LP gas, city gas and power to boost consumer choice while enforcing unbundling, pricing oversight and data access rules. Nippon Gas must sharpen bundled offerings and compliance to balance growth and separation requirements.

Energy security priorities

Government policy emphasizes diversified imports and stockpiling as Japan imports roughly 90% of its primary energy (IEA 2023), favoring fuels with secure supply chains. LP gas benefits from established nationwide storage and logistics, receiving policy support for emergency use and rapid distribution. Incentives for resilience—subsidies for backup generation and microgrids—can boost Nippon Gas solutions, though geopolitical shifts could redirect support toward domestic alternatives.

Disaster resilience initiatives

Local government influence

Prefectural and municipal policies directly affect permitting, safety inspections and building energy codes, shaping Nippon Gas project timelines and capex; Japan targets net-zero by 2050 with a 2030 GHG reduction goal of about 46% versus 2013, so local rules increasingly emphasize efficiency and electrification. Regional decarbonization plans accelerate distributed renewables and heat electrification, while partnerships with utilities and housing developers determine market access; policy heterogeneity requires tailored regional strategies.

Japan energy sector under net-zero push: 46% 2030 GHG cut and ¥1.5T resilience spend

Nippon Gas faces policy pressure from Japan’s net-zero by 2050 and a 46% GHG cut target for 2030 (vs 2013), plus a 36–38% renewables goal for 2030, pushing decarbonization and electrification.

Retail liberalization (gas 2017) and METI/Fair Trade oversight favor bundled gas+power offerings but require strict compliance and data governance.

High import dependence (~90% energy imports) and ¥1.5 trillion FY2024 disaster-resilience funding prioritize resilient LP gas logistics and emergency deployment.

| Metric | Value |

|---|---|

| 2030 GHG target | ≈46% vs 2013 |

| 2030 renewables | 36–38% |

| Energy imports | ~90% (IEA 2023) |

| FY2024 resilience spend | ¥1.5 trillion |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nippon Gas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and regional industry trends. Designed to help executives, consultants, and entrepreneurs identify threats and opportunities and support strategic planning, funding pitches, and scenario analysis.

A concise, visually segmented PESTLE summary for Nippon Gas that can be dropped into presentations, edited with region- or business-line specific notes, and easily shared across teams to support external risk discussions, market positioning and rapid strategy alignment.

Economic factors

Fuel price volatility

Fuel price volatility: LPG and LNG prices swing with global supply-demand and freight—JKM LNG spot ranged roughly $6–50/MMBtu 2021–2024 and LPG (propane) export prices moved over 100% in peak episodes. Margin management requires hedging, index-linked contracts and flexible tariffs to protect EBITDA. Volatility raises customer bills and churn risk in retail; transparent pricing and cost-sharing mechanisms stabilize revenues.

Currency and interest rates

Yen volatility (USD/JPY around 155 in mid‑2025) raises import costs for LPG/LNG and power procurement—JKM spot averaged about $12/MMBtu in 2024, amplifying bills. Rising domestic rates (10‑yr JGB ~1.0% July 2025) lifts financing costs for meters, tanks and DER projects. Nippon Gas’s balance sheet strength and fixed‑rate debt reduce immediate exposure. FX pass‑through formulas preserve margins but can depress demand.

Demand growth mix

Residential gas demand is largely mature in Japan—national LNG imports remained ~70 million tonnes in 2023—so Nippon Gas leans on C&I efficiency retrofits and power retail as primary growth levers. Electrification pressures could cap core gas volumes but create higher-margin energy services (fleet electrification, heat-pump integration). EV charging, battery storage and VPP offerings (EV/power-as-a-service) diversify revenue. A shift to a mixed portfolio improves cash‑flow stability and reduces commodity exposure.

Capex for digital and green

Capex for smart meters, IoT and decarbonization initiatives requires sustained investment; Japan targets net-zero by 2050 and a 46% GHG cut by 2030, shaping incentives and payback assumptions. Payback timing hinges on regulatory incentives and service upsell rates; phased rollouts and partner financing cut upfront intensity. Strong project-selection discipline preserves ROIC.

- Smart meters/IoT: sustained capex

- Regulatory incentives drive payback

- Phased deployment + partnerships lower capital intensity

- Strict project selection protects ROIC

Labor and productivity

Japan energy sector under net-zero push: 46% 2030 GHG cut and ¥1.5T resilience spend

Fuel price swings (JKM avg ~$12/MMBtu in 2024) and yen volatility (USD/JPY ~155 mid‑2025) raise import and billing risk; hedging and pass‑through contracts protect margins. Mature domestic demand (LNG imports ~70 Mt in 2023) shifts growth to C&I, power retail and DERs. Capex and skilled‑labor tightness (job/offers ~1.36 in 2024) pressure costs; automation lifts utility productivity 15–25% (2023–24).

| Metric | Value |

|---|---|

| JKM (2024 avg) | $12/MMBtu |

| Japan LNG imports (2023) | ~70 Mt |

| USD/JPY (mid‑2025) | ~155 |

| Job‑offers/applicants (2024) | 1.36 |

| Automation productivity (2023–24) | 15–25% |

Preview Before You Purchase

Nippon Gas PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Nippon Gas PESTLE Analysis delivers a concise, actionable review of political, economic, social, technological, legal and environmental factors affecting the company and sector. Use it immediately for strategic planning, risk assessment and investment decision-making.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic trends, and environmental regulations are reshaping Nippon Gas with our tailored PESTLE Analysis—insightful, up-to-date, and crafted for decision-makers. Buy the full report to access actionable intelligence, ready-to-use charts, and strategic recommendations you can apply immediately.

Political factors

Energy transition commitments

Japan’s 2050 net-zero goal and 46% GHG reduction target for 2030 (vs 2013) drive subsidies, standards and timetables for gas decarbonization; policy tilts to electrification and a 36–38% renewables share by 2030, squeezing LP/city gas demand. Nippon Gas can shift to efficiency services, biopropane/RNG pilots and green power supply; early compliance captures incentives and reduces transition risk.

Market liberalization dynamics

Japan opened electricity retail to competition in April 2016 and gas in April 2017, spurring hundreds of new entrants and higher customer churn; retail switching rates rose substantially as consumers sought bundled deals. Policymakers and regulators (METI, Fair Trade Commission) back cross-selling of LP gas, city gas and power to boost consumer choice while enforcing unbundling, pricing oversight and data access rules. Nippon Gas must sharpen bundled offerings and compliance to balance growth and separation requirements.

Energy security priorities

Government policy emphasizes diversified imports and stockpiling as Japan imports roughly 90% of its primary energy (IEA 2023), favoring fuels with secure supply chains. LP gas benefits from established nationwide storage and logistics, receiving policy support for emergency use and rapid distribution. Incentives for resilience—subsidies for backup generation and microgrids—can boost Nippon Gas solutions, though geopolitical shifts could redirect support toward domestic alternatives.

Disaster resilience initiatives

Local government influence

Prefectural and municipal policies directly affect permitting, safety inspections and building energy codes, shaping Nippon Gas project timelines and capex; Japan targets net-zero by 2050 with a 2030 GHG reduction goal of about 46% versus 2013, so local rules increasingly emphasize efficiency and electrification. Regional decarbonization plans accelerate distributed renewables and heat electrification, while partnerships with utilities and housing developers determine market access; policy heterogeneity requires tailored regional strategies.

Japan energy sector under net-zero push: 46% 2030 GHG cut and ¥1.5T resilience spend

Nippon Gas faces policy pressure from Japan’s net-zero by 2050 and a 46% GHG cut target for 2030 (vs 2013), plus a 36–38% renewables goal for 2030, pushing decarbonization and electrification.

Retail liberalization (gas 2017) and METI/Fair Trade oversight favor bundled gas+power offerings but require strict compliance and data governance.

High import dependence (~90% energy imports) and ¥1.5 trillion FY2024 disaster-resilience funding prioritize resilient LP gas logistics and emergency deployment.

| Metric | Value |

|---|---|

| 2030 GHG target | ≈46% vs 2013 |

| 2030 renewables | 36–38% |

| Energy imports | ~90% (IEA 2023) |

| FY2024 resilience spend | ¥1.5 trillion |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nippon Gas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and regional industry trends. Designed to help executives, consultants, and entrepreneurs identify threats and opportunities and support strategic planning, funding pitches, and scenario analysis.

A concise, visually segmented PESTLE summary for Nippon Gas that can be dropped into presentations, edited with region- or business-line specific notes, and easily shared across teams to support external risk discussions, market positioning and rapid strategy alignment.

Economic factors

Fuel price volatility

Fuel price volatility: LPG and LNG prices swing with global supply-demand and freight—JKM LNG spot ranged roughly $6–50/MMBtu 2021–2024 and LPG (propane) export prices moved over 100% in peak episodes. Margin management requires hedging, index-linked contracts and flexible tariffs to protect EBITDA. Volatility raises customer bills and churn risk in retail; transparent pricing and cost-sharing mechanisms stabilize revenues.

Currency and interest rates

Yen volatility (USD/JPY around 155 in mid‑2025) raises import costs for LPG/LNG and power procurement—JKM spot averaged about $12/MMBtu in 2024, amplifying bills. Rising domestic rates (10‑yr JGB ~1.0% July 2025) lifts financing costs for meters, tanks and DER projects. Nippon Gas’s balance sheet strength and fixed‑rate debt reduce immediate exposure. FX pass‑through formulas preserve margins but can depress demand.

Demand growth mix

Residential gas demand is largely mature in Japan—national LNG imports remained ~70 million tonnes in 2023—so Nippon Gas leans on C&I efficiency retrofits and power retail as primary growth levers. Electrification pressures could cap core gas volumes but create higher-margin energy services (fleet electrification, heat-pump integration). EV charging, battery storage and VPP offerings (EV/power-as-a-service) diversify revenue. A shift to a mixed portfolio improves cash‑flow stability and reduces commodity exposure.

Capex for digital and green

Capex for smart meters, IoT and decarbonization initiatives requires sustained investment; Japan targets net-zero by 2050 and a 46% GHG cut by 2030, shaping incentives and payback assumptions. Payback timing hinges on regulatory incentives and service upsell rates; phased rollouts and partner financing cut upfront intensity. Strong project-selection discipline preserves ROIC.

- Smart meters/IoT: sustained capex

- Regulatory incentives drive payback

- Phased deployment + partnerships lower capital intensity

- Strict project selection protects ROIC

Labor and productivity

Japan energy sector under net-zero push: 46% 2030 GHG cut and ¥1.5T resilience spend

Fuel price swings (JKM avg ~$12/MMBtu in 2024) and yen volatility (USD/JPY ~155 mid‑2025) raise import and billing risk; hedging and pass‑through contracts protect margins. Mature domestic demand (LNG imports ~70 Mt in 2023) shifts growth to C&I, power retail and DERs. Capex and skilled‑labor tightness (job/offers ~1.36 in 2024) pressure costs; automation lifts utility productivity 15–25% (2023–24).

| Metric | Value |

|---|---|

| JKM (2024 avg) | $12/MMBtu |

| Japan LNG imports (2023) | ~70 Mt |

| USD/JPY (mid‑2025) | ~155 |

| Job‑offers/applicants (2024) | 1.36 |

| Automation productivity (2023–24) | 15–25% |

Preview Before You Purchase

Nippon Gas PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Nippon Gas PESTLE Analysis delivers a concise, actionable review of political, economic, social, technological, legal and environmental factors affecting the company and sector. Use it immediately for strategic planning, risk assessment and investment decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock how political shifts, economic trends, and environmental regulations are reshaping Nippon Gas with our tailored PESTLE Analysis—insightful, up-to-date, and crafted for decision-makers. Buy the full report to access actionable intelligence, ready-to-use charts, and strategic recommendations you can apply immediately.

Political factors

Energy transition commitments

Japan’s 2050 net-zero goal and 46% GHG reduction target for 2030 (vs 2013) drive subsidies, standards and timetables for gas decarbonization; policy tilts to electrification and a 36–38% renewables share by 2030, squeezing LP/city gas demand. Nippon Gas can shift to efficiency services, biopropane/RNG pilots and green power supply; early compliance captures incentives and reduces transition risk.

Market liberalization dynamics

Japan opened electricity retail to competition in April 2016 and gas in April 2017, spurring hundreds of new entrants and higher customer churn; retail switching rates rose substantially as consumers sought bundled deals. Policymakers and regulators (METI, Fair Trade Commission) back cross-selling of LP gas, city gas and power to boost consumer choice while enforcing unbundling, pricing oversight and data access rules. Nippon Gas must sharpen bundled offerings and compliance to balance growth and separation requirements.

Energy security priorities

Government policy emphasizes diversified imports and stockpiling as Japan imports roughly 90% of its primary energy (IEA 2023), favoring fuels with secure supply chains. LP gas benefits from established nationwide storage and logistics, receiving policy support for emergency use and rapid distribution. Incentives for resilience—subsidies for backup generation and microgrids—can boost Nippon Gas solutions, though geopolitical shifts could redirect support toward domestic alternatives.

Disaster resilience initiatives

Local government influence

Prefectural and municipal policies directly affect permitting, safety inspections and building energy codes, shaping Nippon Gas project timelines and capex; Japan targets net-zero by 2050 with a 2030 GHG reduction goal of about 46% versus 2013, so local rules increasingly emphasize efficiency and electrification. Regional decarbonization plans accelerate distributed renewables and heat electrification, while partnerships with utilities and housing developers determine market access; policy heterogeneity requires tailored regional strategies.

Japan energy sector under net-zero push: 46% 2030 GHG cut and ¥1.5T resilience spend

Nippon Gas faces policy pressure from Japan’s net-zero by 2050 and a 46% GHG cut target for 2030 (vs 2013), plus a 36–38% renewables goal for 2030, pushing decarbonization and electrification.

Retail liberalization (gas 2017) and METI/Fair Trade oversight favor bundled gas+power offerings but require strict compliance and data governance.

High import dependence (~90% energy imports) and ¥1.5 trillion FY2024 disaster-resilience funding prioritize resilient LP gas logistics and emergency deployment.

| Metric | Value |

|---|---|

| 2030 GHG target | ≈46% vs 2013 |

| 2030 renewables | 36–38% |

| Energy imports | ~90% (IEA 2023) |

| FY2024 resilience spend | ¥1.5 trillion |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nippon Gas across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and regional industry trends. Designed to help executives, consultants, and entrepreneurs identify threats and opportunities and support strategic planning, funding pitches, and scenario analysis.

A concise, visually segmented PESTLE summary for Nippon Gas that can be dropped into presentations, edited with region- or business-line specific notes, and easily shared across teams to support external risk discussions, market positioning and rapid strategy alignment.

Economic factors

Fuel price volatility

Fuel price volatility: LPG and LNG prices swing with global supply-demand and freight—JKM LNG spot ranged roughly $6–50/MMBtu 2021–2024 and LPG (propane) export prices moved over 100% in peak episodes. Margin management requires hedging, index-linked contracts and flexible tariffs to protect EBITDA. Volatility raises customer bills and churn risk in retail; transparent pricing and cost-sharing mechanisms stabilize revenues.

Currency and interest rates

Yen volatility (USD/JPY around 155 in mid‑2025) raises import costs for LPG/LNG and power procurement—JKM spot averaged about $12/MMBtu in 2024, amplifying bills. Rising domestic rates (10‑yr JGB ~1.0% July 2025) lifts financing costs for meters, tanks and DER projects. Nippon Gas’s balance sheet strength and fixed‑rate debt reduce immediate exposure. FX pass‑through formulas preserve margins but can depress demand.

Demand growth mix

Residential gas demand is largely mature in Japan—national LNG imports remained ~70 million tonnes in 2023—so Nippon Gas leans on C&I efficiency retrofits and power retail as primary growth levers. Electrification pressures could cap core gas volumes but create higher-margin energy services (fleet electrification, heat-pump integration). EV charging, battery storage and VPP offerings (EV/power-as-a-service) diversify revenue. A shift to a mixed portfolio improves cash‑flow stability and reduces commodity exposure.

Capex for digital and green

Capex for smart meters, IoT and decarbonization initiatives requires sustained investment; Japan targets net-zero by 2050 and a 46% GHG cut by 2030, shaping incentives and payback assumptions. Payback timing hinges on regulatory incentives and service upsell rates; phased rollouts and partner financing cut upfront intensity. Strong project-selection discipline preserves ROIC.

- Smart meters/IoT: sustained capex

- Regulatory incentives drive payback

- Phased deployment + partnerships lower capital intensity

- Strict project selection protects ROIC

Labor and productivity

Japan energy sector under net-zero push: 46% 2030 GHG cut and ¥1.5T resilience spend

Fuel price swings (JKM avg ~$12/MMBtu in 2024) and yen volatility (USD/JPY ~155 mid‑2025) raise import and billing risk; hedging and pass‑through contracts protect margins. Mature domestic demand (LNG imports ~70 Mt in 2023) shifts growth to C&I, power retail and DERs. Capex and skilled‑labor tightness (job/offers ~1.36 in 2024) pressure costs; automation lifts utility productivity 15–25% (2023–24).

| Metric | Value |

|---|---|

| JKM (2024 avg) | $12/MMBtu |

| Japan LNG imports (2023) | ~70 Mt |

| USD/JPY (mid‑2025) | ~155 |

| Job‑offers/applicants (2024) | 1.36 |

| Automation productivity (2023–24) | 15–25% |

Preview Before You Purchase

Nippon Gas PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Nippon Gas PESTLE Analysis delivers a concise, actionable review of political, economic, social, technological, legal and environmental factors affecting the company and sector. Use it immediately for strategic planning, risk assessment and investment decision-making.