Nichols PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Nichols PESTLE Analysis—three to five concise insights reveal how political, economic, social, technological, legal, and environmental trends shape its outlook. Ideal for investors and strategists, this analysis flags risks and growth levers. Purchase the full report to get the complete, actionable breakdown instantly.

Political factors

Sugar taxes and health policy

Since the UK soft drinks levy began in 2018 and with over 40 jurisdictions adopting SSB taxes by 2024, policy tightening has shifted sales toward low/no‑sugar SKUs and industry sugar levels fell ~40% in key categories, forcing Nichols to reformulate and reprice portfolios. Divergent national levies complicate cross‑market margin planning and SKU rollout timing. Proactive engagement with policymakers and trade bodies reduces sudden excise shocks and compliance costs.

Trade policy and tariffs

Brexit-era customs frictions and rule-of-origin checks continue to disrupt Nichols’ inputs and exports, with UK–EU paperwork complexities persisting into 2024 and adding border delays for beverage ingredients. Tariff shifts on sugar, flavorings, aluminium and PET can materially change Nichols’ cost-to-serve and margin sensitivity. Obtaining trusted trader/AEO status and streamlined paperwork reduces hold-ups and compliance cost. Diversifying suppliers across the EU and non-EU markets limits exposure to sudden trade-policy shifts.

Geopolitical stability in key regions

Geopolitical instability across MENA threatens Vimto’s demand and distribution, with unrest frequently causing transport disruptions and retail closures. Currency controls and import restrictions in several markets can delay receivables and squeeze working capital. Scenario planning for seasonal peaks such as Ramadan is essential to match supply with rapid demand surges. Strengthening local partnerships and holding contingency inventory materially improves resilience and recovery time.

Public procurement and OOH policy

Government health standards for schools, hospitals and public venues, reinforced since the 2018 Soft Drinks Industry Levy, shape post-mix and vending shortlists across a UK public procurement market worth about 300bn GBP annually (2023).

Restrictions on HFSS availability and placement narrow viable SKUs, pressuring high-sugar lines; public-sector buyers increasingly demand low-/no-sugar credentials to win contracts.

Tailored low-sugar formats and clear nutrition labeling preserve share while meeting compliance and procurement scoring.

- tags: procurement-market-300bn

- tags: SDIL-2018

- tags: HFSS-restrictions

- tags: nutrition-credentials

Subsidies and industrial policy

Energy support schemes and manufacturing incentives materially alter UK plant economics: the Industrial Energy Transformation Fund (IETF) (£315m) and the Net Zero Innovation Portfolio (>£1bn) lower project costs. Grants for decarbonization, automation and R&D speed upgrades, while policy uncertainty complicates capex timing; active grant pursuit can cut unit costs and boost competitiveness.

- IETF £315m

- Net Zero Innovation Portfolio >£1bn

- Grants reduce capex/unit cost

- Policy uncertainty risks timing

SSB taxes and HFSS rules drive low/no-sugar reformulation, repricing; sugar down ~40%

UK SSB taxes (SDIL 2018 + 40+ jurisdictions by 2024) and HFSS procurement rules push Nichols toward low/no‑sugar SKUs, reformulation and repricing, cutting category sugar ~40% in key markets. Brexit customs frictions and tariff volatility raise input cost risk; AEO/trusted trader status and supplier diversification reduce delays. Energy/decarbonisation grants (IETF £315m; Net Zero >£1bn) lower capex.

| Issue | Metric |

|---|---|

| SSB adoption | 40+ jurisdictions by 2024 |

| Category sugar drop | ~40% |

| IETF | £315m |

| Net Zero portfolio | >£1bn |

What is included in the product

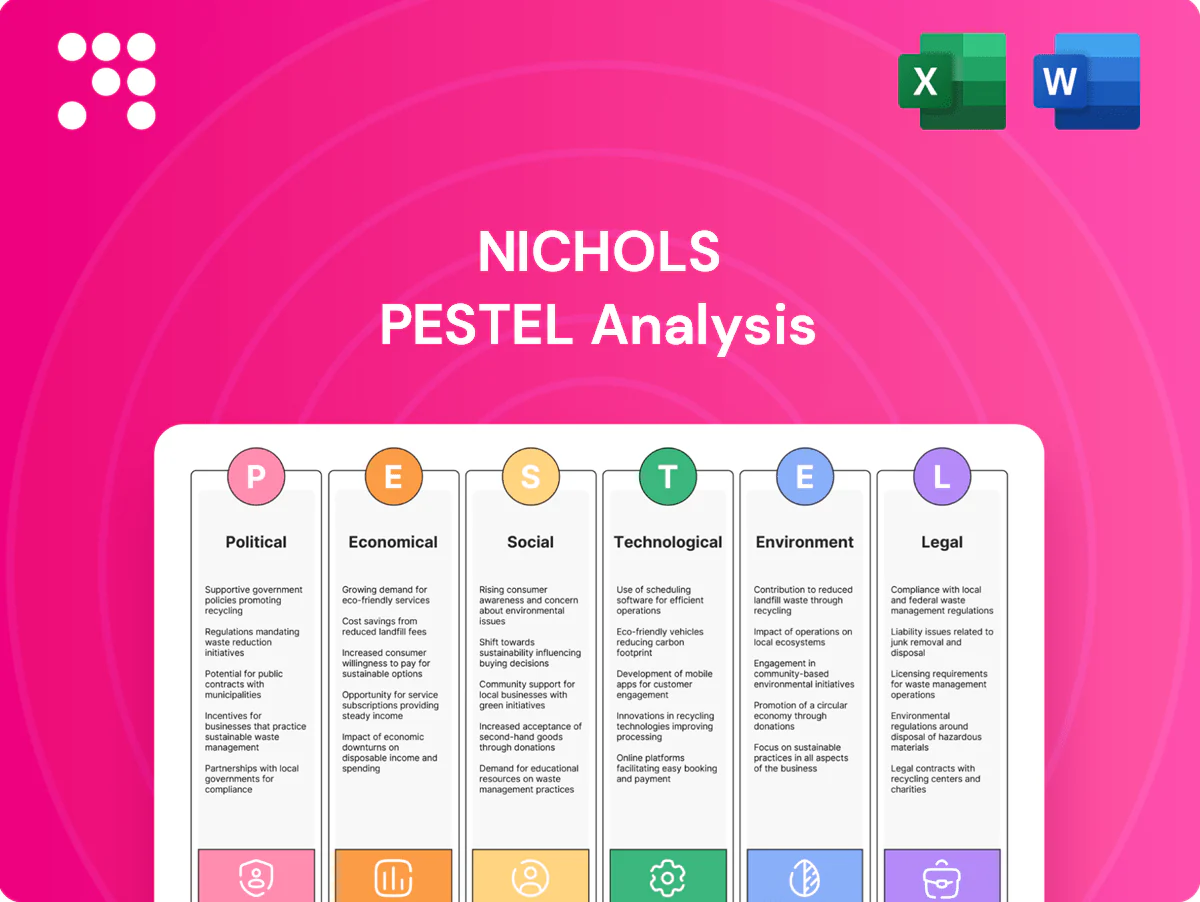

Explores how external macro-environmental factors uniquely affect Nichols across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities. Designed for executives and investors, it includes forward-looking insights and ready-to-use formatting for reports and pitches.

Visually segmented by PESTLE categories for rapid interpretation at a glance, Nichols' PESTLE analysis streamlines meetings and planning by highlighting key external risks and opportunities. Easily shareable and concise, it accelerates cross‑team alignment and decision-making during strategy sessions.

Economic factors

Input cost volatility

Input cost volatility—raw sugar (~18.5 USc/lb 2024 average), alternative sweeteners, aluminum (LME ~$2,300/ton 2024), PET resin (~$1,300/t Asian avg 2024) and CO2 (EU ETS ~€90/t 2024)—swings with global cycles and can sharply compress Nichols margins unless pricing and hedging are agile. Supplier diversification and forward contracts stabilize budgets; pack‑mix optimization protects contribution per case.

Consumer spending cycles

Soft drinks remain resilient in spending cycles, but downtrading rises during stress; UK CPI eased to 2.3% in June 2024 (ONS), yet consumers shift to cheaper SKUs. Value packs and private label pressure retail margins as private label penetration in grocery remains high, intensifying price competition. Premium licensed variants can sustain prices if clearly differentiated; monitoring elasticity by channel (on‑trade vs off‑trade) should guide price‑pack architecture.

FX exposure

Revenue from international markets and imported inputs exposes Nichols to GBP/EUR/USD swings; in 2024 GBP traded around 1.27 USD and 1.17 EUR on average, creating direct COGS and reported-profit volatility. FX moves affect both input costs and consolidated margins. Currency-matched costs offer natural hedges, while layered financial hedges (forwards/options) add predictability for budgeting and planning.

Channel mix dynamics

Channel mix dynamics: OOH rebounds lift post-mix volumes and margins as on-trade demand recovers, while retail normalises following pandemic-era spike promotions; tourism and major events amplify seasonal peaks. Contract terms and strategic equipment placement increase stickiness and reduce churn, and balanced channel exposure smooths earnings volatility across cycles.

- OOH recovery supports higher-margin post-mix sales

- Retail normalization reduces one-off promo gains

- Contracts + equipment placement = customer stickiness

- Balanced mix smooths seasonal earnings swings

Labor and logistics costs

Wage inflation near 5% in 2024 and an HGV driver shortfall estimated around 100,000 continue to pressure Nichols distribution costs; warehouse rents and volatile freight rates elevate margin risk. Investment in automation and route-optimization algorithms is reducing unit distribution costs, while strategic 3PL partnerships improve service levels and operational flexibility.

- Wage inflation ~5% (2024)

- HGV shortfall ~100,000

- Freight/warehouse volatility up

- Automation + route optimization cut costs

- 3PLs boost flexibility

SSB taxes and HFSS rules drive low/no-sugar reformulation, repricing; sugar down ~40%

Input-cost volatility (raw sugar 18.5 USc/lb, PET ~$1,300/t, CO2 €90/t in 2024) and FX swings (GBP ~1.27 USD/1.17 EUR avg 2024) pressure margins; active hedging, supplier diversification and pack‑mix optimize resilience. Soft‑drink demand is resilient but downtrading rises as UK CPI 2.3% (Jun 2024); value packs and premium SKUs must be balanced. Wage inflation ~5% and HGV shortfall ~100,000 raise distribution costs; automation and 3PLs mitigate.

| Metric | 2024 Value |

|---|---|

| Raw sugar | 18.5 USc/lb |

| PET resin | $1,300/t |

| EU ETS CO2 | €90/t |

| GBP | 1.27 USD / 1.17 EUR |

| UK CPI | 2.3% (Jun 2024) |

| Wage inflation | ~5% |

| HGV shortfall | ~100,000 |

Same Document Delivered

Nichols PESTLE Analysis

The Nichols PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase—ready to use with no placeholders or surprises. The layout, content, and structure visible are identical to the downloadable file delivered immediately after checkout. This is the real, final product for professional analysis and decision-making.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Nichols PESTLE Analysis—three to five concise insights reveal how political, economic, social, technological, legal, and environmental trends shape its outlook. Ideal for investors and strategists, this analysis flags risks and growth levers. Purchase the full report to get the complete, actionable breakdown instantly.

Political factors

Sugar taxes and health policy

Since the UK soft drinks levy began in 2018 and with over 40 jurisdictions adopting SSB taxes by 2024, policy tightening has shifted sales toward low/no‑sugar SKUs and industry sugar levels fell ~40% in key categories, forcing Nichols to reformulate and reprice portfolios. Divergent national levies complicate cross‑market margin planning and SKU rollout timing. Proactive engagement with policymakers and trade bodies reduces sudden excise shocks and compliance costs.

Trade policy and tariffs

Brexit-era customs frictions and rule-of-origin checks continue to disrupt Nichols’ inputs and exports, with UK–EU paperwork complexities persisting into 2024 and adding border delays for beverage ingredients. Tariff shifts on sugar, flavorings, aluminium and PET can materially change Nichols’ cost-to-serve and margin sensitivity. Obtaining trusted trader/AEO status and streamlined paperwork reduces hold-ups and compliance cost. Diversifying suppliers across the EU and non-EU markets limits exposure to sudden trade-policy shifts.

Geopolitical stability in key regions

Geopolitical instability across MENA threatens Vimto’s demand and distribution, with unrest frequently causing transport disruptions and retail closures. Currency controls and import restrictions in several markets can delay receivables and squeeze working capital. Scenario planning for seasonal peaks such as Ramadan is essential to match supply with rapid demand surges. Strengthening local partnerships and holding contingency inventory materially improves resilience and recovery time.

Public procurement and OOH policy

Government health standards for schools, hospitals and public venues, reinforced since the 2018 Soft Drinks Industry Levy, shape post-mix and vending shortlists across a UK public procurement market worth about 300bn GBP annually (2023).

Restrictions on HFSS availability and placement narrow viable SKUs, pressuring high-sugar lines; public-sector buyers increasingly demand low-/no-sugar credentials to win contracts.

Tailored low-sugar formats and clear nutrition labeling preserve share while meeting compliance and procurement scoring.

- tags: procurement-market-300bn

- tags: SDIL-2018

- tags: HFSS-restrictions

- tags: nutrition-credentials

Subsidies and industrial policy

Energy support schemes and manufacturing incentives materially alter UK plant economics: the Industrial Energy Transformation Fund (IETF) (£315m) and the Net Zero Innovation Portfolio (>£1bn) lower project costs. Grants for decarbonization, automation and R&D speed upgrades, while policy uncertainty complicates capex timing; active grant pursuit can cut unit costs and boost competitiveness.

- IETF £315m

- Net Zero Innovation Portfolio >£1bn

- Grants reduce capex/unit cost

- Policy uncertainty risks timing

SSB taxes and HFSS rules drive low/no-sugar reformulation, repricing; sugar down ~40%

UK SSB taxes (SDIL 2018 + 40+ jurisdictions by 2024) and HFSS procurement rules push Nichols toward low/no‑sugar SKUs, reformulation and repricing, cutting category sugar ~40% in key markets. Brexit customs frictions and tariff volatility raise input cost risk; AEO/trusted trader status and supplier diversification reduce delays. Energy/decarbonisation grants (IETF £315m; Net Zero >£1bn) lower capex.

| Issue | Metric |

|---|---|

| SSB adoption | 40+ jurisdictions by 2024 |

| Category sugar drop | ~40% |

| IETF | £315m |

| Net Zero portfolio | >£1bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nichols across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities. Designed for executives and investors, it includes forward-looking insights and ready-to-use formatting for reports and pitches.

Visually segmented by PESTLE categories for rapid interpretation at a glance, Nichols' PESTLE analysis streamlines meetings and planning by highlighting key external risks and opportunities. Easily shareable and concise, it accelerates cross‑team alignment and decision-making during strategy sessions.

Economic factors

Input cost volatility

Input cost volatility—raw sugar (~18.5 USc/lb 2024 average), alternative sweeteners, aluminum (LME ~$2,300/ton 2024), PET resin (~$1,300/t Asian avg 2024) and CO2 (EU ETS ~€90/t 2024)—swings with global cycles and can sharply compress Nichols margins unless pricing and hedging are agile. Supplier diversification and forward contracts stabilize budgets; pack‑mix optimization protects contribution per case.

Consumer spending cycles

Soft drinks remain resilient in spending cycles, but downtrading rises during stress; UK CPI eased to 2.3% in June 2024 (ONS), yet consumers shift to cheaper SKUs. Value packs and private label pressure retail margins as private label penetration in grocery remains high, intensifying price competition. Premium licensed variants can sustain prices if clearly differentiated; monitoring elasticity by channel (on‑trade vs off‑trade) should guide price‑pack architecture.

FX exposure

Revenue from international markets and imported inputs exposes Nichols to GBP/EUR/USD swings; in 2024 GBP traded around 1.27 USD and 1.17 EUR on average, creating direct COGS and reported-profit volatility. FX moves affect both input costs and consolidated margins. Currency-matched costs offer natural hedges, while layered financial hedges (forwards/options) add predictability for budgeting and planning.

Channel mix dynamics

Channel mix dynamics: OOH rebounds lift post-mix volumes and margins as on-trade demand recovers, while retail normalises following pandemic-era spike promotions; tourism and major events amplify seasonal peaks. Contract terms and strategic equipment placement increase stickiness and reduce churn, and balanced channel exposure smooths earnings volatility across cycles.

- OOH recovery supports higher-margin post-mix sales

- Retail normalization reduces one-off promo gains

- Contracts + equipment placement = customer stickiness

- Balanced mix smooths seasonal earnings swings

Labor and logistics costs

Wage inflation near 5% in 2024 and an HGV driver shortfall estimated around 100,000 continue to pressure Nichols distribution costs; warehouse rents and volatile freight rates elevate margin risk. Investment in automation and route-optimization algorithms is reducing unit distribution costs, while strategic 3PL partnerships improve service levels and operational flexibility.

- Wage inflation ~5% (2024)

- HGV shortfall ~100,000

- Freight/warehouse volatility up

- Automation + route optimization cut costs

- 3PLs boost flexibility

SSB taxes and HFSS rules drive low/no-sugar reformulation, repricing; sugar down ~40%

Input-cost volatility (raw sugar 18.5 USc/lb, PET ~$1,300/t, CO2 €90/t in 2024) and FX swings (GBP ~1.27 USD/1.17 EUR avg 2024) pressure margins; active hedging, supplier diversification and pack‑mix optimize resilience. Soft‑drink demand is resilient but downtrading rises as UK CPI 2.3% (Jun 2024); value packs and premium SKUs must be balanced. Wage inflation ~5% and HGV shortfall ~100,000 raise distribution costs; automation and 3PLs mitigate.

| Metric | 2024 Value |

|---|---|

| Raw sugar | 18.5 USc/lb |

| PET resin | $1,300/t |

| EU ETS CO2 | €90/t |

| GBP | 1.27 USD / 1.17 EUR |

| UK CPI | 2.3% (Jun 2024) |

| Wage inflation | ~5% |

| HGV shortfall | ~100,000 |

Same Document Delivered

Nichols PESTLE Analysis

The Nichols PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase—ready to use with no placeholders or surprises. The layout, content, and structure visible are identical to the downloadable file delivered immediately after checkout. This is the real, final product for professional analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Nichols PESTLE Analysis—three to five concise insights reveal how political, economic, social, technological, legal, and environmental trends shape its outlook. Ideal for investors and strategists, this analysis flags risks and growth levers. Purchase the full report to get the complete, actionable breakdown instantly.

Political factors

Sugar taxes and health policy

Since the UK soft drinks levy began in 2018 and with over 40 jurisdictions adopting SSB taxes by 2024, policy tightening has shifted sales toward low/no‑sugar SKUs and industry sugar levels fell ~40% in key categories, forcing Nichols to reformulate and reprice portfolios. Divergent national levies complicate cross‑market margin planning and SKU rollout timing. Proactive engagement with policymakers and trade bodies reduces sudden excise shocks and compliance costs.

Trade policy and tariffs

Brexit-era customs frictions and rule-of-origin checks continue to disrupt Nichols’ inputs and exports, with UK–EU paperwork complexities persisting into 2024 and adding border delays for beverage ingredients. Tariff shifts on sugar, flavorings, aluminium and PET can materially change Nichols’ cost-to-serve and margin sensitivity. Obtaining trusted trader/AEO status and streamlined paperwork reduces hold-ups and compliance cost. Diversifying suppliers across the EU and non-EU markets limits exposure to sudden trade-policy shifts.

Geopolitical stability in key regions

Geopolitical instability across MENA threatens Vimto’s demand and distribution, with unrest frequently causing transport disruptions and retail closures. Currency controls and import restrictions in several markets can delay receivables and squeeze working capital. Scenario planning for seasonal peaks such as Ramadan is essential to match supply with rapid demand surges. Strengthening local partnerships and holding contingency inventory materially improves resilience and recovery time.

Public procurement and OOH policy

Government health standards for schools, hospitals and public venues, reinforced since the 2018 Soft Drinks Industry Levy, shape post-mix and vending shortlists across a UK public procurement market worth about 300bn GBP annually (2023).

Restrictions on HFSS availability and placement narrow viable SKUs, pressuring high-sugar lines; public-sector buyers increasingly demand low-/no-sugar credentials to win contracts.

Tailored low-sugar formats and clear nutrition labeling preserve share while meeting compliance and procurement scoring.

- tags: procurement-market-300bn

- tags: SDIL-2018

- tags: HFSS-restrictions

- tags: nutrition-credentials

Subsidies and industrial policy

Energy support schemes and manufacturing incentives materially alter UK plant economics: the Industrial Energy Transformation Fund (IETF) (£315m) and the Net Zero Innovation Portfolio (>£1bn) lower project costs. Grants for decarbonization, automation and R&D speed upgrades, while policy uncertainty complicates capex timing; active grant pursuit can cut unit costs and boost competitiveness.

- IETF £315m

- Net Zero Innovation Portfolio >£1bn

- Grants reduce capex/unit cost

- Policy uncertainty risks timing

SSB taxes and HFSS rules drive low/no-sugar reformulation, repricing; sugar down ~40%

UK SSB taxes (SDIL 2018 + 40+ jurisdictions by 2024) and HFSS procurement rules push Nichols toward low/no‑sugar SKUs, reformulation and repricing, cutting category sugar ~40% in key markets. Brexit customs frictions and tariff volatility raise input cost risk; AEO/trusted trader status and supplier diversification reduce delays. Energy/decarbonisation grants (IETF £315m; Net Zero >£1bn) lower capex.

| Issue | Metric |

|---|---|

| SSB adoption | 40+ jurisdictions by 2024 |

| Category sugar drop | ~40% |

| IETF | £315m |

| Net Zero portfolio | >£1bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Nichols across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities. Designed for executives and investors, it includes forward-looking insights and ready-to-use formatting for reports and pitches.

Visually segmented by PESTLE categories for rapid interpretation at a glance, Nichols' PESTLE analysis streamlines meetings and planning by highlighting key external risks and opportunities. Easily shareable and concise, it accelerates cross‑team alignment and decision-making during strategy sessions.

Economic factors

Input cost volatility

Input cost volatility—raw sugar (~18.5 USc/lb 2024 average), alternative sweeteners, aluminum (LME ~$2,300/ton 2024), PET resin (~$1,300/t Asian avg 2024) and CO2 (EU ETS ~€90/t 2024)—swings with global cycles and can sharply compress Nichols margins unless pricing and hedging are agile. Supplier diversification and forward contracts stabilize budgets; pack‑mix optimization protects contribution per case.

Consumer spending cycles

Soft drinks remain resilient in spending cycles, but downtrading rises during stress; UK CPI eased to 2.3% in June 2024 (ONS), yet consumers shift to cheaper SKUs. Value packs and private label pressure retail margins as private label penetration in grocery remains high, intensifying price competition. Premium licensed variants can sustain prices if clearly differentiated; monitoring elasticity by channel (on‑trade vs off‑trade) should guide price‑pack architecture.

FX exposure

Revenue from international markets and imported inputs exposes Nichols to GBP/EUR/USD swings; in 2024 GBP traded around 1.27 USD and 1.17 EUR on average, creating direct COGS and reported-profit volatility. FX moves affect both input costs and consolidated margins. Currency-matched costs offer natural hedges, while layered financial hedges (forwards/options) add predictability for budgeting and planning.

Channel mix dynamics

Channel mix dynamics: OOH rebounds lift post-mix volumes and margins as on-trade demand recovers, while retail normalises following pandemic-era spike promotions; tourism and major events amplify seasonal peaks. Contract terms and strategic equipment placement increase stickiness and reduce churn, and balanced channel exposure smooths earnings volatility across cycles.

- OOH recovery supports higher-margin post-mix sales

- Retail normalization reduces one-off promo gains

- Contracts + equipment placement = customer stickiness

- Balanced mix smooths seasonal earnings swings

Labor and logistics costs

Wage inflation near 5% in 2024 and an HGV driver shortfall estimated around 100,000 continue to pressure Nichols distribution costs; warehouse rents and volatile freight rates elevate margin risk. Investment in automation and route-optimization algorithms is reducing unit distribution costs, while strategic 3PL partnerships improve service levels and operational flexibility.

- Wage inflation ~5% (2024)

- HGV shortfall ~100,000

- Freight/warehouse volatility up

- Automation + route optimization cut costs

- 3PLs boost flexibility

SSB taxes and HFSS rules drive low/no-sugar reformulation, repricing; sugar down ~40%

Input-cost volatility (raw sugar 18.5 USc/lb, PET ~$1,300/t, CO2 €90/t in 2024) and FX swings (GBP ~1.27 USD/1.17 EUR avg 2024) pressure margins; active hedging, supplier diversification and pack‑mix optimize resilience. Soft‑drink demand is resilient but downtrading rises as UK CPI 2.3% (Jun 2024); value packs and premium SKUs must be balanced. Wage inflation ~5% and HGV shortfall ~100,000 raise distribution costs; automation and 3PLs mitigate.

| Metric | 2024 Value |

|---|---|

| Raw sugar | 18.5 USc/lb |

| PET resin | $1,300/t |

| EU ETS CO2 | €90/t |

| GBP | 1.27 USD / 1.17 EUR |

| UK CPI | 2.3% (Jun 2024) |

| Wage inflation | ~5% |

| HGV shortfall | ~100,000 |

Same Document Delivered

Nichols PESTLE Analysis

The Nichols PESTLE Analysis preview shown here is the exact, fully formatted document you’ll receive after purchase—ready to use with no placeholders or surprises. The layout, content, and structure visible are identical to the downloadable file delivered immediately after checkout. This is the real, final product for professional analysis and decision-making.