nicko tours GmbH Porter's Five Forces Analysis

From Overview to Strategy Blueprint

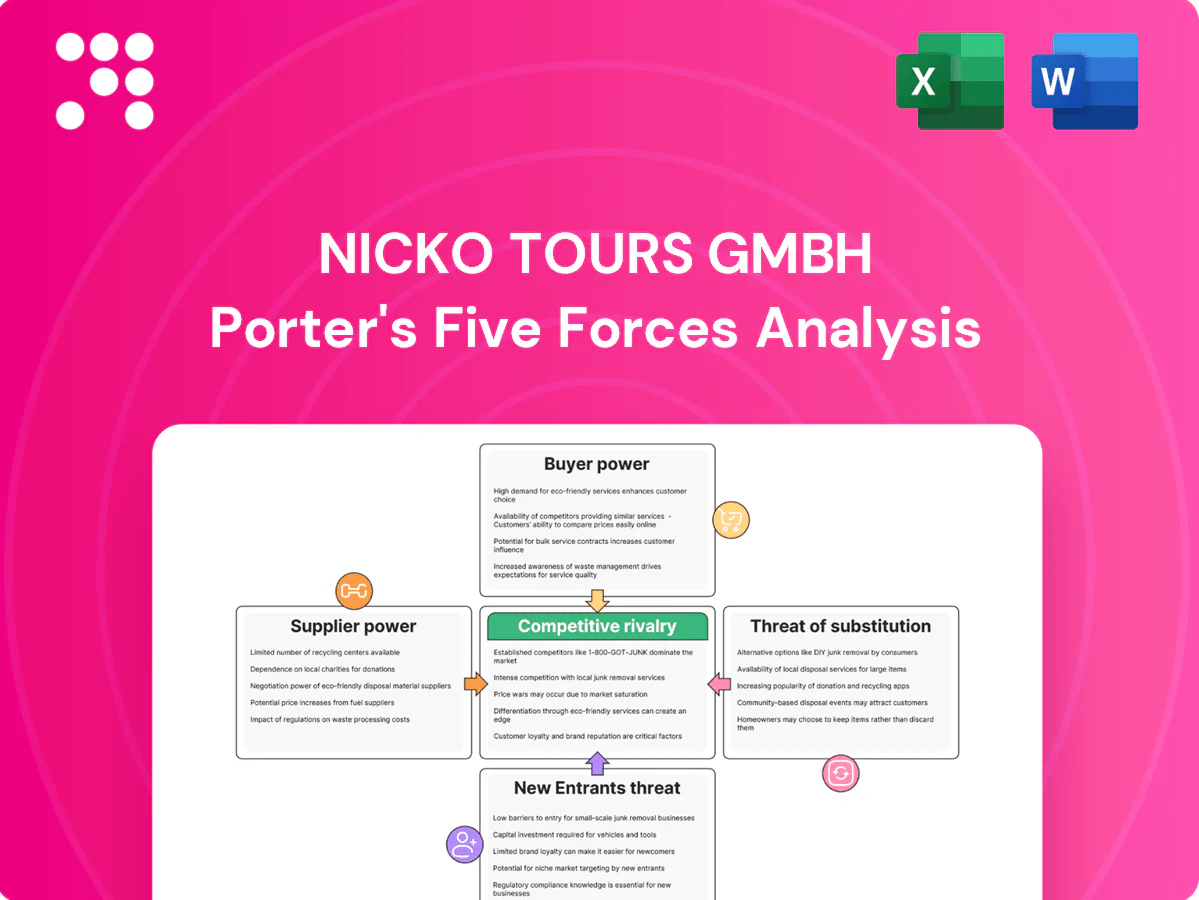

nicko tours GmbH faces moderate buyer power, niche supplier relationships, and evolving substitute threats from alternative travel formats; barriers to entry are moderate but brand and operational scale matter. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications tailored to nicko tours GmbH.

Suppliers Bargaining Power

Concentrated shipyards and vessel lessors

Modern river ships are built by a small number of European yards concentrated in Germany, Croatia and Romania, and many vessels are chartered from a few large lessors, creating concentrated supplier leverage. Lead times for newbuilds and green retrofits commonly run 18–36 months, raising switching costs and delivery risk. Suppliers therefore can dictate pricing, technical specs and payment terms for newbuilds and retrofit packages. Multi‑year charters (typically 3–7 years) secure availability but often embed escalation clauses.

Port authorities, berths, and lock scheduling

Prime berthing slots in key European cities are scarce, giving port authorities measurable leverage as demand peaks; for example the Kiel Canal handles roughly 32,000 transits annually, concentrating slot pressure. Congestion and lock maintenance windows can force itinerary changes and trigger delay costs and supplementary docking fees. Preferred access often requires multi‑season commitments and can push port charges up to ~25% above standard rates, while limited substitutes on popular stretches constrain nicko tours negotiation power.

Fuel, utilities, and environmental compliance

Marine fuel, shore power equipment and emissions tech are supplied by specialized vendors, and fuel can represent up to 50% of vessel OPEX, making operators sensitive to price swings; EU ETS averaged about €70/ton CO2 in 2024, raising upstream cost pressure. Suppliers of SCR, shore-power systems and wastewater treatment can command premiums, with retrofits commonly in the €0.5–2m range per ship, while tightening compliance timelines erode operator negotiating leverage.

Catering, F&B, and excursion partners

Onboard provisioning and local tour providers materially shape guest experience and margins for nicko tours; CLIA estimated ~26 million cruise passengers in 2024, concentrating demand in marquee ports where top excursion partners maintain waitlists and price discipline, limiting substitution despite bulk-procurement savings. Seasonal peaks further amplify supplier clout.

- High supplier concentration in marquee ports

- Bulk contracts lower provisioning cost

- Quality positioning limits substitution

- Seasonal peaks increase prices and waitlists

Crewing, training, and regulatory services

Qualified river pilots and multilingual hospitality crew are finite, concentrating bargaining power with crewing agencies; crew wage inflation reached about 8% in 2024 across European inland shipping markets, squeezing operators like nicko tours GmbH. Crewing agencies and training providers can raise fees in tight labor markets, while medical, insurance and class society services remain mandatory and largely price-inelastic. EU labor regulations on waterways further restrict staffing flexibility and increase compliance costs.

- Limited supply: finite qualified river pilots and multilingual crew

- Cost pressure: ~8% crew wage inflation in 2024

- Inelastic services: mandatory medical/insurance/class society fees

- Regulatory constraint: strict EU waterways labor rules

Supply squeeze: 18-36, 50% fuel, €70/t

Suppliers hold strong leverage: limited European shipyards and lessors, 18–36 month newbuild lead times, and multi‑year charters restrict switching. Fuel can be ~50% of vessel OPEX and EU ETS averaged ~€70/ton CO2 in 2024, raising costs; crewing costs rose ~8% in 2024. Key ports command scarce berthing and can push charges ~+25% at peaks.

| Metric | 2024 Value |

|---|---|

| Newbuild lead time | 18–36 months |

| Fuel share of OPEX | ~50% |

| EU ETS price | €70/ton |

| Crew wage inflation | ~8% |

| Peak port premium | ~+25% |

What is included in the product

Tailored Porter's Five Forces analysis for nicko tours GmbH that uncovers competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlights disruptive trends and market entry barriers to inform strategic positioning and profitability.

Compact Porter's Five Forces summary tailored to nicko tours GmbH—quickly spot competitive pressures and relief strategies for smarter, faster decisions.

Customers Bargaining Power

Price-sensitive leisure travelers

Price-sensitive leisure travelers routinely compare inclusions and fares across brands and dates, with 2024 surveys showing about 70% use price-comparison tools before booking, boosting their leverage. Transparent online pricing elevates bargaining power by making add-ons and true prices visible. Promotions and early-booking discounts (often 10–20%) are expected, and economic downturns rapidly shift demand toward lower-value tiers.

Travel agencies and OTAs

Travel agencies and OTAs aggregate demand and routinely negotiate commissions, amenities and allotments, with agency commissions typically negotiated in the 10–20% range while OTA commissions run about 15–25% (2024). Preferred partner programs (e.g., enhanced placement) can divert volume if nicko tours' terms lag peers. OTAs boost visibility but compress margins via fees; consortia leverage further pressure on net rates and room allocations.

Group and charter buyers

Group and charter buyers—affinity groups, MICE planners and wholesalers—leverage trade volumes for deeper discounts, custom terms and often request exclusive sailings or partial ship charters; CLIA reported cruise passenger volumes near 30 million in 2023–24, amplifying buyer leverage. Cancellation and payment flexibility are frequent asks, and operators report losing a few large accounts can reduce load factors by several percentage points, materially hitting revenue per sailing.

Low switching costs across brands

Routes and ships on major rivers are broadly comparable, so customers easily swap operators based on dates, cabin availability and onboard perks; loyalty programs remain present but are weaker than in airlines and hotels, encouraging trial purchases. Review scores and recent refurbishments frequently tip the balance in final booking decisions.

- Low switching costs

- Date/cabin-driven churn

- Weak loyalty vs airlines/hotels

- Reviews/refurbs as tiebreakers

Influence of reviews and social proof

Review platforms and forums amplify nicko tours GmbH service issues and itinerary disruptions, with 93% of travelers consulting reviews before booking (2024 travel sector data), forcing visible, immediate responses.

High visibility pushes operators toward service recovery credits and upgrades; effective recovery can restore loyalty in about 70% of cases, creating de facto post‑purchase concession power.

Maintaining a consistent NPS around or above 40 materially moderates buyer leverage by reducing complaint visibility and escalation.

- 93% travelers check reviews (2024)

- ≈70% loyalty return after successful recovery

- Target NPS ≥40 to reduce buyer power

Customers in control: 70% compare prices, 93% read reviews; OTAs 15-25% commissions

Customers wield strong leverage: 70% use price-comparison tools (2024), OTAs take 15–25% commissions, and 93% consult reviews, making transparency and reputation critical. Groups/charters and agencies demand deeper discounts and flexible terms, with cruise volumes ~30M (2023–24) amplifying buyer power. Effective service recovery restores ~70% loyalty; maintaining NPS ≥40 reduces escalation.

| Metric | Value (2024) |

|---|---|

| Price-comparison users | 70% |

| Review consults | 93% |

| OTA commissions | 15–25% |

| Cruise volumes | ≈30M |

| Recovery loyalty | ≈70% |

| Target NPS | ≥40 |

Full Version Awaits

nicko tours GmbH Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of nicko tours GmbH you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It assesses competitive rivalry, threat of new entrants and substitutes, buyer and supplier power, and industry-specific dynamics for river-cruise and tour operators. Instant download is available upon payment.

From Overview to Strategy Blueprint

nicko tours GmbH faces moderate buyer power, niche supplier relationships, and evolving substitute threats from alternative travel formats; barriers to entry are moderate but brand and operational scale matter. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications tailored to nicko tours GmbH.

Suppliers Bargaining Power

Concentrated shipyards and vessel lessors

Modern river ships are built by a small number of European yards concentrated in Germany, Croatia and Romania, and many vessels are chartered from a few large lessors, creating concentrated supplier leverage. Lead times for newbuilds and green retrofits commonly run 18–36 months, raising switching costs and delivery risk. Suppliers therefore can dictate pricing, technical specs and payment terms for newbuilds and retrofit packages. Multi‑year charters (typically 3–7 years) secure availability but often embed escalation clauses.

Port authorities, berths, and lock scheduling

Prime berthing slots in key European cities are scarce, giving port authorities measurable leverage as demand peaks; for example the Kiel Canal handles roughly 32,000 transits annually, concentrating slot pressure. Congestion and lock maintenance windows can force itinerary changes and trigger delay costs and supplementary docking fees. Preferred access often requires multi‑season commitments and can push port charges up to ~25% above standard rates, while limited substitutes on popular stretches constrain nicko tours negotiation power.

Fuel, utilities, and environmental compliance

Marine fuel, shore power equipment and emissions tech are supplied by specialized vendors, and fuel can represent up to 50% of vessel OPEX, making operators sensitive to price swings; EU ETS averaged about €70/ton CO2 in 2024, raising upstream cost pressure. Suppliers of SCR, shore-power systems and wastewater treatment can command premiums, with retrofits commonly in the €0.5–2m range per ship, while tightening compliance timelines erode operator negotiating leverage.

Catering, F&B, and excursion partners

Onboard provisioning and local tour providers materially shape guest experience and margins for nicko tours; CLIA estimated ~26 million cruise passengers in 2024, concentrating demand in marquee ports where top excursion partners maintain waitlists and price discipline, limiting substitution despite bulk-procurement savings. Seasonal peaks further amplify supplier clout.

- High supplier concentration in marquee ports

- Bulk contracts lower provisioning cost

- Quality positioning limits substitution

- Seasonal peaks increase prices and waitlists

Crewing, training, and regulatory services

Qualified river pilots and multilingual hospitality crew are finite, concentrating bargaining power with crewing agencies; crew wage inflation reached about 8% in 2024 across European inland shipping markets, squeezing operators like nicko tours GmbH. Crewing agencies and training providers can raise fees in tight labor markets, while medical, insurance and class society services remain mandatory and largely price-inelastic. EU labor regulations on waterways further restrict staffing flexibility and increase compliance costs.

- Limited supply: finite qualified river pilots and multilingual crew

- Cost pressure: ~8% crew wage inflation in 2024

- Inelastic services: mandatory medical/insurance/class society fees

- Regulatory constraint: strict EU waterways labor rules

Supply squeeze: 18-36, 50% fuel, €70/t

Suppliers hold strong leverage: limited European shipyards and lessors, 18–36 month newbuild lead times, and multi‑year charters restrict switching. Fuel can be ~50% of vessel OPEX and EU ETS averaged ~€70/ton CO2 in 2024, raising costs; crewing costs rose ~8% in 2024. Key ports command scarce berthing and can push charges ~+25% at peaks.

| Metric | 2024 Value |

|---|---|

| Newbuild lead time | 18–36 months |

| Fuel share of OPEX | ~50% |

| EU ETS price | €70/ton |

| Crew wage inflation | ~8% |

| Peak port premium | ~+25% |

What is included in the product

Tailored Porter's Five Forces analysis for nicko tours GmbH that uncovers competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlights disruptive trends and market entry barriers to inform strategic positioning and profitability.

Compact Porter's Five Forces summary tailored to nicko tours GmbH—quickly spot competitive pressures and relief strategies for smarter, faster decisions.

Customers Bargaining Power

Price-sensitive leisure travelers

Price-sensitive leisure travelers routinely compare inclusions and fares across brands and dates, with 2024 surveys showing about 70% use price-comparison tools before booking, boosting their leverage. Transparent online pricing elevates bargaining power by making add-ons and true prices visible. Promotions and early-booking discounts (often 10–20%) are expected, and economic downturns rapidly shift demand toward lower-value tiers.

Travel agencies and OTAs

Travel agencies and OTAs aggregate demand and routinely negotiate commissions, amenities and allotments, with agency commissions typically negotiated in the 10–20% range while OTA commissions run about 15–25% (2024). Preferred partner programs (e.g., enhanced placement) can divert volume if nicko tours' terms lag peers. OTAs boost visibility but compress margins via fees; consortia leverage further pressure on net rates and room allocations.

Group and charter buyers

Group and charter buyers—affinity groups, MICE planners and wholesalers—leverage trade volumes for deeper discounts, custom terms and often request exclusive sailings or partial ship charters; CLIA reported cruise passenger volumes near 30 million in 2023–24, amplifying buyer leverage. Cancellation and payment flexibility are frequent asks, and operators report losing a few large accounts can reduce load factors by several percentage points, materially hitting revenue per sailing.

Low switching costs across brands

Routes and ships on major rivers are broadly comparable, so customers easily swap operators based on dates, cabin availability and onboard perks; loyalty programs remain present but are weaker than in airlines and hotels, encouraging trial purchases. Review scores and recent refurbishments frequently tip the balance in final booking decisions.

- Low switching costs

- Date/cabin-driven churn

- Weak loyalty vs airlines/hotels

- Reviews/refurbs as tiebreakers

Influence of reviews and social proof

Review platforms and forums amplify nicko tours GmbH service issues and itinerary disruptions, with 93% of travelers consulting reviews before booking (2024 travel sector data), forcing visible, immediate responses.

High visibility pushes operators toward service recovery credits and upgrades; effective recovery can restore loyalty in about 70% of cases, creating de facto post‑purchase concession power.

Maintaining a consistent NPS around or above 40 materially moderates buyer leverage by reducing complaint visibility and escalation.

- 93% travelers check reviews (2024)

- ≈70% loyalty return after successful recovery

- Target NPS ≥40 to reduce buyer power

Customers in control: 70% compare prices, 93% read reviews; OTAs 15-25% commissions

Customers wield strong leverage: 70% use price-comparison tools (2024), OTAs take 15–25% commissions, and 93% consult reviews, making transparency and reputation critical. Groups/charters and agencies demand deeper discounts and flexible terms, with cruise volumes ~30M (2023–24) amplifying buyer power. Effective service recovery restores ~70% loyalty; maintaining NPS ≥40 reduces escalation.

| Metric | Value (2024) |

|---|---|

| Price-comparison users | 70% |

| Review consults | 93% |

| OTA commissions | 15–25% |

| Cruise volumes | ≈30M |

| Recovery loyalty | ≈70% |

| Target NPS | ≥40 |

Full Version Awaits

nicko tours GmbH Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of nicko tours GmbH you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It assesses competitive rivalry, threat of new entrants and substitutes, buyer and supplier power, and industry-specific dynamics for river-cruise and tour operators. Instant download is available upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

nicko tours GmbH faces moderate buyer power, niche supplier relationships, and evolving substitute threats from alternative travel formats; barriers to entry are moderate but brand and operational scale matter. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications tailored to nicko tours GmbH.

Suppliers Bargaining Power

Concentrated shipyards and vessel lessors

Modern river ships are built by a small number of European yards concentrated in Germany, Croatia and Romania, and many vessels are chartered from a few large lessors, creating concentrated supplier leverage. Lead times for newbuilds and green retrofits commonly run 18–36 months, raising switching costs and delivery risk. Suppliers therefore can dictate pricing, technical specs and payment terms for newbuilds and retrofit packages. Multi‑year charters (typically 3–7 years) secure availability but often embed escalation clauses.

Port authorities, berths, and lock scheduling

Prime berthing slots in key European cities are scarce, giving port authorities measurable leverage as demand peaks; for example the Kiel Canal handles roughly 32,000 transits annually, concentrating slot pressure. Congestion and lock maintenance windows can force itinerary changes and trigger delay costs and supplementary docking fees. Preferred access often requires multi‑season commitments and can push port charges up to ~25% above standard rates, while limited substitutes on popular stretches constrain nicko tours negotiation power.

Fuel, utilities, and environmental compliance

Marine fuel, shore power equipment and emissions tech are supplied by specialized vendors, and fuel can represent up to 50% of vessel OPEX, making operators sensitive to price swings; EU ETS averaged about €70/ton CO2 in 2024, raising upstream cost pressure. Suppliers of SCR, shore-power systems and wastewater treatment can command premiums, with retrofits commonly in the €0.5–2m range per ship, while tightening compliance timelines erode operator negotiating leverage.

Catering, F&B, and excursion partners

Onboard provisioning and local tour providers materially shape guest experience and margins for nicko tours; CLIA estimated ~26 million cruise passengers in 2024, concentrating demand in marquee ports where top excursion partners maintain waitlists and price discipline, limiting substitution despite bulk-procurement savings. Seasonal peaks further amplify supplier clout.

- High supplier concentration in marquee ports

- Bulk contracts lower provisioning cost

- Quality positioning limits substitution

- Seasonal peaks increase prices and waitlists

Crewing, training, and regulatory services

Qualified river pilots and multilingual hospitality crew are finite, concentrating bargaining power with crewing agencies; crew wage inflation reached about 8% in 2024 across European inland shipping markets, squeezing operators like nicko tours GmbH. Crewing agencies and training providers can raise fees in tight labor markets, while medical, insurance and class society services remain mandatory and largely price-inelastic. EU labor regulations on waterways further restrict staffing flexibility and increase compliance costs.

- Limited supply: finite qualified river pilots and multilingual crew

- Cost pressure: ~8% crew wage inflation in 2024

- Inelastic services: mandatory medical/insurance/class society fees

- Regulatory constraint: strict EU waterways labor rules

Supply squeeze: 18-36, 50% fuel, €70/t

Suppliers hold strong leverage: limited European shipyards and lessors, 18–36 month newbuild lead times, and multi‑year charters restrict switching. Fuel can be ~50% of vessel OPEX and EU ETS averaged ~€70/ton CO2 in 2024, raising costs; crewing costs rose ~8% in 2024. Key ports command scarce berthing and can push charges ~+25% at peaks.

| Metric | 2024 Value |

|---|---|

| Newbuild lead time | 18–36 months |

| Fuel share of OPEX | ~50% |

| EU ETS price | €70/ton |

| Crew wage inflation | ~8% |

| Peak port premium | ~+25% |

What is included in the product

Tailored Porter's Five Forces analysis for nicko tours GmbH that uncovers competitive rivalry, buyer and supplier power, threats from substitutes and new entrants, and highlights disruptive trends and market entry barriers to inform strategic positioning and profitability.

Compact Porter's Five Forces summary tailored to nicko tours GmbH—quickly spot competitive pressures and relief strategies for smarter, faster decisions.

Customers Bargaining Power

Price-sensitive leisure travelers

Price-sensitive leisure travelers routinely compare inclusions and fares across brands and dates, with 2024 surveys showing about 70% use price-comparison tools before booking, boosting their leverage. Transparent online pricing elevates bargaining power by making add-ons and true prices visible. Promotions and early-booking discounts (often 10–20%) are expected, and economic downturns rapidly shift demand toward lower-value tiers.

Travel agencies and OTAs

Travel agencies and OTAs aggregate demand and routinely negotiate commissions, amenities and allotments, with agency commissions typically negotiated in the 10–20% range while OTA commissions run about 15–25% (2024). Preferred partner programs (e.g., enhanced placement) can divert volume if nicko tours' terms lag peers. OTAs boost visibility but compress margins via fees; consortia leverage further pressure on net rates and room allocations.

Group and charter buyers

Group and charter buyers—affinity groups, MICE planners and wholesalers—leverage trade volumes for deeper discounts, custom terms and often request exclusive sailings or partial ship charters; CLIA reported cruise passenger volumes near 30 million in 2023–24, amplifying buyer leverage. Cancellation and payment flexibility are frequent asks, and operators report losing a few large accounts can reduce load factors by several percentage points, materially hitting revenue per sailing.

Low switching costs across brands

Routes and ships on major rivers are broadly comparable, so customers easily swap operators based on dates, cabin availability and onboard perks; loyalty programs remain present but are weaker than in airlines and hotels, encouraging trial purchases. Review scores and recent refurbishments frequently tip the balance in final booking decisions.

- Low switching costs

- Date/cabin-driven churn

- Weak loyalty vs airlines/hotels

- Reviews/refurbs as tiebreakers

Influence of reviews and social proof

Review platforms and forums amplify nicko tours GmbH service issues and itinerary disruptions, with 93% of travelers consulting reviews before booking (2024 travel sector data), forcing visible, immediate responses.

High visibility pushes operators toward service recovery credits and upgrades; effective recovery can restore loyalty in about 70% of cases, creating de facto post‑purchase concession power.

Maintaining a consistent NPS around or above 40 materially moderates buyer leverage by reducing complaint visibility and escalation.

- 93% travelers check reviews (2024)

- ≈70% loyalty return after successful recovery

- Target NPS ≥40 to reduce buyer power

Customers in control: 70% compare prices, 93% read reviews; OTAs 15-25% commissions

Customers wield strong leverage: 70% use price-comparison tools (2024), OTAs take 15–25% commissions, and 93% consult reviews, making transparency and reputation critical. Groups/charters and agencies demand deeper discounts and flexible terms, with cruise volumes ~30M (2023–24) amplifying buyer power. Effective service recovery restores ~70% loyalty; maintaining NPS ≥40 reduces escalation.

| Metric | Value (2024) |

|---|---|

| Price-comparison users | 70% |

| Review consults | 93% |

| OTA commissions | 15–25% |

| Cruise volumes | ≈30M |

| Recovery loyalty | ≈70% |

| Target NPS | ≥40 |

Full Version Awaits

nicko tours GmbH Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of nicko tours GmbH you'll receive immediately after purchase—no surprises, fully formatted and ready to use. It assesses competitive rivalry, threat of new entrants and substitutes, buyer and supplier power, and industry-specific dynamics for river-cruise and tour operators. Instant download is available upon payment.