Nicotra Gebhardt S.p.A Porter's Five Forces Analysis

From Overview to Strategy Blueprint

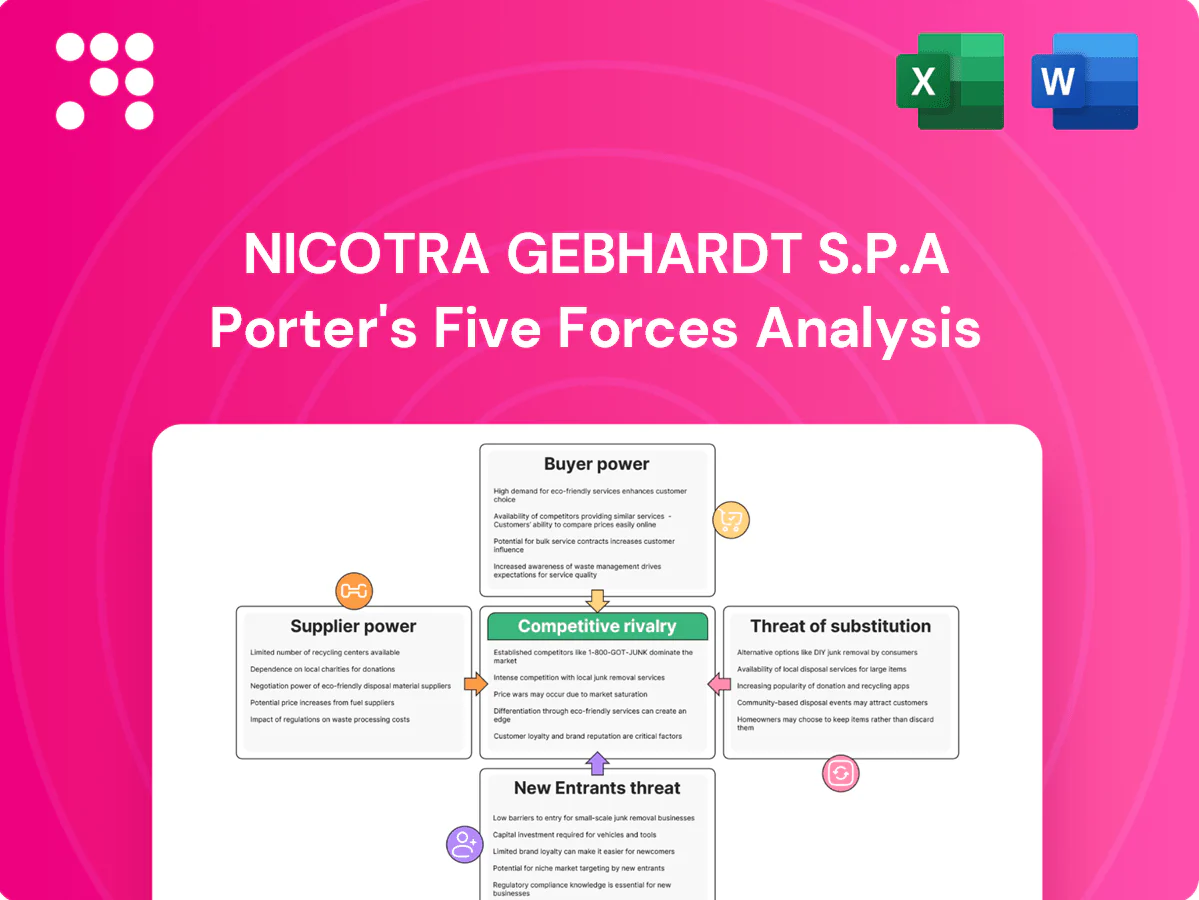

Nicotra Gebhardt S.p.A faces moderate supplier power and competitive rivalry driven by specialized HVAC components and regional players, while buyer bargaining and threat of substitutes remain contained by technical differentiation. Barriers to entry are medium due to capital and certification needs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nicotra Gebhardt S.p.A’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components dependence

High-efficiency EC motors, bearings and control electronics are sourced from a narrow pool of often 2–3 qualified suppliers, creating switching costs and lead times that can reach 16–20 weeks; this concentration gives suppliers pricing and delivery leverage. Dual-sourcing and design-to-value lower exposure but do not remove supplier-driven volatility.

Raw material volatility

Raw material volatility—steel (+8% in 2024), aluminum (+5% in 2024), copper (+10% in 2024) and rare-earth magnets (NdPr +25% in 2024)—drives cost swings that directly pressure Nicotra Gebhardt margins. Commodity price spikes can compress margins absent indexed contracts, while hedging and long-term agreements have reduced input cost volatility for peers. Cost passthrough is more feasible on bespoke projects but limited on fixed-bid tenders.

Quality and certification requirements

Components for Nicotra Gebhardt must comply with AMCA, ISO, ErP and acoustic standards, raising documentation and testing burdens. Fewer suppliers possess accredited labs and full certification chains, narrowing the sourcing pool and increasing supplier leverage. Lengthy qualification cycles and retesting under evolving 2024 regulatory guidance slow switching and raise switching costs, strengthening supplier bargaining power.

Logistics and lead-time constraints

Logistics and energy-driven freight cost volatility materially raise input costs for bulky fan components: container rates remain ~60% below 2021 highs but bulk freight and 2024 energy spikes still add 8–15% to landed cost. Long lead times for motors and electronics (commonly 12–24 weeks) strain project schedules, and expedited shipping premiums of 10–30% erode margins. Nearshoring and inventory buffers (safety stock 8–12 weeks) have reduced supplier leverage.

- Freight/energy add 8–15% to landed cost

- Typical lead times 12–24 weeks

- Expedited shipping premium 10–30%

- Nearshoring/inventory cut leverage (safety stock 8–12 weeks)

Technological co-development

Co-engineering with motor and control suppliers delivers measurable performance gains through matched torque, efficiency and control logic, and in 2024 the global industrial fan market is estimated around €6.5bn, increasing incentives for tight supplier integration. Embedded designs and firmware create lock-in as IP and bespoke tooling raise switching costs, while modular interfaces preserve flexibility and bargaining leverage.

Risk: 2–3, 12–24w, commodities +25%

Concentrated suppliers (2–3) and long lead times (12–24w) give vendors pricing/delivery leverage; commodity swings in 2024 (steel +8%, Al +5%, Cu +10%, NdPr +25%) compress margins. Logistics add 8–15% landed cost; expedited shipping 10–30% and safety stock 8–12w mitigate but raise inventory costs. Co-engineering/embedded IP increases lock-in versus modular options.

| Metric | 2024 |

|---|---|

| Supplier pool | 2–3 |

| Lead times | 12–24 weeks |

| Commodity moves | Steel +8% Al +5% Cu +10% NdPr +25% |

| Logistics | +8–15% landed |

| Market size | €6.5bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Nicotra Gebhardt S.p.A; evaluates suppliers' and buyers' power, threat of substitutes, competitive rivalry, and barriers protecting incumbents, with strategic commentary on disruptive forces and actionable implications for pricing and profitability.

Concise Porter's Five Forces snapshot for Nicotra Gebhardt S.p.A—clear, customizable pressure levels and radar visualization to simplify strategic decisions and slot directly into pitch decks or dashboards.

Customers Bargaining Power

Project-based procurement

Project-based procurement for HVAC OEMs, contractors and infrastructure clients is dominated by tenders, with over 65% of large system contracts awarded through competitive bidding in 2024, intensifying price pressure and compressing supplier margins by 200–400 basis points. Award criteria increasingly blend lowest cost with energy efficiency and delivery timelines, while stringent prequalification and technical specs can shift bargaining power toward clients or, when niche capabilities are required, back to Nicotra Gebhardt.

Moderate switching costs

Fans are often standardized by size and duty points, so switching suppliers is feasible but not frictionless. Re‑qualification, BIM model updates and commissioning introduce time and performance risks that raise switching costs. For AHUs, system integration and certification create greater stickiness. Established service history and transferable warranties further bias buyers toward incumbent suppliers.

Volume and consolidation

Large OEMs and global contractors aggregate purchasing volumes for components like blowers and fans, securing framework agreements that often include volume rebates typically in the 5–12% range, increasing their negotiating leverage with suppliers such as Nicotra Gebhardt S.p.A.

Smaller distributors, handling under 5% of total sector volume each, lack scale and accept thinner margins, limiting their bargaining power relative to consolidated buyers.

Regional sales mix matters: Western Europe and North America buyers generally achieve higher average discounts (often 6–10%) versus emerging markets, where discounts are lower due to fragmented demand and price sensitivity.

Performance and compliance sensitivity

Buyers of Nicotra Gebhardt blowers prioritize energy efficiency, low acoustic emission and regulatory conformity, since 2024 standards and procurement tenders price lifecycle energy and noise performance over initial cost.

Non‑compliance risks fines and retrofit charges that materially reduce willingness to switch suppliers on price alone; certified test data and EU/ISO labels attenuate buyer bargaining power.

Lifecycle TCO arguments shift negotiation toward opex savings and service contracts, improving margin resilience.

- verified labels reduce price pressure

- compliance avoids retrofit fines

- TCO focus favors higher‑efficiency models

Cyclical end-markets

Cyclical construction and industrial end-markets drive order timing for Nicotra Gebhardt, so buyer leverage rises in downturns when customers press harder on price and payment terms; in 2024 several European construction segments remained uneven, sustaining demand volatility. During tight supply phases, customers prioritize delivery reliability over discounts, and the companys backlog coverage—when high—reduces buyer bargaining power.

- 2024 demand volatility: cyclical order timing

- Downturns: stronger price/term pressure

- Tight supply: delivery > discounts

- High backlog: moderates customer leverage

Buyers wield high power: 65% tenders, margins 200–400 bp

Customers hold moderate-to-high bargaining power: 65% of large HVAC contracts awarded by tender in 2024, compressing supplier margins 200–400 bp; large buyers secure 5–12% volume rebates while Western buyers achieve 6–10% discounts; switching costs (requalification, certification) and certified efficiency labels mitigate pure price pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Tender share | 65% | Higher price pressure |

| Margin compression | 200–400 bp | Reduced supplier margins |

| Volume rebates | 5–12% | Buyer leverage |

| West discounts | 6–10% | Regional pressure |

| Distributor share | <5% | Low leverage |

Preview the Actual Deliverable

Nicotra Gebhardt S.p.A Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Nicotra Gebhardt S.p.A you'll receive immediately after purchase—no surprises or placeholders. The report assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for market positioning. It's professionally formatted, ready for download and immediate use.

From Overview to Strategy Blueprint

Nicotra Gebhardt S.p.A faces moderate supplier power and competitive rivalry driven by specialized HVAC components and regional players, while buyer bargaining and threat of substitutes remain contained by technical differentiation. Barriers to entry are medium due to capital and certification needs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nicotra Gebhardt S.p.A’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components dependence

High-efficiency EC motors, bearings and control electronics are sourced from a narrow pool of often 2–3 qualified suppliers, creating switching costs and lead times that can reach 16–20 weeks; this concentration gives suppliers pricing and delivery leverage. Dual-sourcing and design-to-value lower exposure but do not remove supplier-driven volatility.

Raw material volatility

Raw material volatility—steel (+8% in 2024), aluminum (+5% in 2024), copper (+10% in 2024) and rare-earth magnets (NdPr +25% in 2024)—drives cost swings that directly pressure Nicotra Gebhardt margins. Commodity price spikes can compress margins absent indexed contracts, while hedging and long-term agreements have reduced input cost volatility for peers. Cost passthrough is more feasible on bespoke projects but limited on fixed-bid tenders.

Quality and certification requirements

Components for Nicotra Gebhardt must comply with AMCA, ISO, ErP and acoustic standards, raising documentation and testing burdens. Fewer suppliers possess accredited labs and full certification chains, narrowing the sourcing pool and increasing supplier leverage. Lengthy qualification cycles and retesting under evolving 2024 regulatory guidance slow switching and raise switching costs, strengthening supplier bargaining power.

Logistics and lead-time constraints

Logistics and energy-driven freight cost volatility materially raise input costs for bulky fan components: container rates remain ~60% below 2021 highs but bulk freight and 2024 energy spikes still add 8–15% to landed cost. Long lead times for motors and electronics (commonly 12–24 weeks) strain project schedules, and expedited shipping premiums of 10–30% erode margins. Nearshoring and inventory buffers (safety stock 8–12 weeks) have reduced supplier leverage.

- Freight/energy add 8–15% to landed cost

- Typical lead times 12–24 weeks

- Expedited shipping premium 10–30%

- Nearshoring/inventory cut leverage (safety stock 8–12 weeks)

Technological co-development

Co-engineering with motor and control suppliers delivers measurable performance gains through matched torque, efficiency and control logic, and in 2024 the global industrial fan market is estimated around €6.5bn, increasing incentives for tight supplier integration. Embedded designs and firmware create lock-in as IP and bespoke tooling raise switching costs, while modular interfaces preserve flexibility and bargaining leverage.

Risk: 2–3, 12–24w, commodities +25%

Concentrated suppliers (2–3) and long lead times (12–24w) give vendors pricing/delivery leverage; commodity swings in 2024 (steel +8%, Al +5%, Cu +10%, NdPr +25%) compress margins. Logistics add 8–15% landed cost; expedited shipping 10–30% and safety stock 8–12w mitigate but raise inventory costs. Co-engineering/embedded IP increases lock-in versus modular options.

| Metric | 2024 |

|---|---|

| Supplier pool | 2–3 |

| Lead times | 12–24 weeks |

| Commodity moves | Steel +8% Al +5% Cu +10% NdPr +25% |

| Logistics | +8–15% landed |

| Market size | €6.5bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Nicotra Gebhardt S.p.A; evaluates suppliers' and buyers' power, threat of substitutes, competitive rivalry, and barriers protecting incumbents, with strategic commentary on disruptive forces and actionable implications for pricing and profitability.

Concise Porter's Five Forces snapshot for Nicotra Gebhardt S.p.A—clear, customizable pressure levels and radar visualization to simplify strategic decisions and slot directly into pitch decks or dashboards.

Customers Bargaining Power

Project-based procurement

Project-based procurement for HVAC OEMs, contractors and infrastructure clients is dominated by tenders, with over 65% of large system contracts awarded through competitive bidding in 2024, intensifying price pressure and compressing supplier margins by 200–400 basis points. Award criteria increasingly blend lowest cost with energy efficiency and delivery timelines, while stringent prequalification and technical specs can shift bargaining power toward clients or, when niche capabilities are required, back to Nicotra Gebhardt.

Moderate switching costs

Fans are often standardized by size and duty points, so switching suppliers is feasible but not frictionless. Re‑qualification, BIM model updates and commissioning introduce time and performance risks that raise switching costs. For AHUs, system integration and certification create greater stickiness. Established service history and transferable warranties further bias buyers toward incumbent suppliers.

Volume and consolidation

Large OEMs and global contractors aggregate purchasing volumes for components like blowers and fans, securing framework agreements that often include volume rebates typically in the 5–12% range, increasing their negotiating leverage with suppliers such as Nicotra Gebhardt S.p.A.

Smaller distributors, handling under 5% of total sector volume each, lack scale and accept thinner margins, limiting their bargaining power relative to consolidated buyers.

Regional sales mix matters: Western Europe and North America buyers generally achieve higher average discounts (often 6–10%) versus emerging markets, where discounts are lower due to fragmented demand and price sensitivity.

Performance and compliance sensitivity

Buyers of Nicotra Gebhardt blowers prioritize energy efficiency, low acoustic emission and regulatory conformity, since 2024 standards and procurement tenders price lifecycle energy and noise performance over initial cost.

Non‑compliance risks fines and retrofit charges that materially reduce willingness to switch suppliers on price alone; certified test data and EU/ISO labels attenuate buyer bargaining power.

Lifecycle TCO arguments shift negotiation toward opex savings and service contracts, improving margin resilience.

- verified labels reduce price pressure

- compliance avoids retrofit fines

- TCO focus favors higher‑efficiency models

Cyclical end-markets

Cyclical construction and industrial end-markets drive order timing for Nicotra Gebhardt, so buyer leverage rises in downturns when customers press harder on price and payment terms; in 2024 several European construction segments remained uneven, sustaining demand volatility. During tight supply phases, customers prioritize delivery reliability over discounts, and the companys backlog coverage—when high—reduces buyer bargaining power.

- 2024 demand volatility: cyclical order timing

- Downturns: stronger price/term pressure

- Tight supply: delivery > discounts

- High backlog: moderates customer leverage

Buyers wield high power: 65% tenders, margins 200–400 bp

Customers hold moderate-to-high bargaining power: 65% of large HVAC contracts awarded by tender in 2024, compressing supplier margins 200–400 bp; large buyers secure 5–12% volume rebates while Western buyers achieve 6–10% discounts; switching costs (requalification, certification) and certified efficiency labels mitigate pure price pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Tender share | 65% | Higher price pressure |

| Margin compression | 200–400 bp | Reduced supplier margins |

| Volume rebates | 5–12% | Buyer leverage |

| West discounts | 6–10% | Regional pressure |

| Distributor share | <5% | Low leverage |

Preview the Actual Deliverable

Nicotra Gebhardt S.p.A Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Nicotra Gebhardt S.p.A you'll receive immediately after purchase—no surprises or placeholders. The report assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for market positioning. It's professionally formatted, ready for download and immediate use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Nicotra Gebhardt S.p.A faces moderate supplier power and competitive rivalry driven by specialized HVAC components and regional players, while buyer bargaining and threat of substitutes remain contained by technical differentiation. Barriers to entry are medium due to capital and certification needs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nicotra Gebhardt S.p.A’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components dependence

High-efficiency EC motors, bearings and control electronics are sourced from a narrow pool of often 2–3 qualified suppliers, creating switching costs and lead times that can reach 16–20 weeks; this concentration gives suppliers pricing and delivery leverage. Dual-sourcing and design-to-value lower exposure but do not remove supplier-driven volatility.

Raw material volatility

Raw material volatility—steel (+8% in 2024), aluminum (+5% in 2024), copper (+10% in 2024) and rare-earth magnets (NdPr +25% in 2024)—drives cost swings that directly pressure Nicotra Gebhardt margins. Commodity price spikes can compress margins absent indexed contracts, while hedging and long-term agreements have reduced input cost volatility for peers. Cost passthrough is more feasible on bespoke projects but limited on fixed-bid tenders.

Quality and certification requirements

Components for Nicotra Gebhardt must comply with AMCA, ISO, ErP and acoustic standards, raising documentation and testing burdens. Fewer suppliers possess accredited labs and full certification chains, narrowing the sourcing pool and increasing supplier leverage. Lengthy qualification cycles and retesting under evolving 2024 regulatory guidance slow switching and raise switching costs, strengthening supplier bargaining power.

Logistics and lead-time constraints

Logistics and energy-driven freight cost volatility materially raise input costs for bulky fan components: container rates remain ~60% below 2021 highs but bulk freight and 2024 energy spikes still add 8–15% to landed cost. Long lead times for motors and electronics (commonly 12–24 weeks) strain project schedules, and expedited shipping premiums of 10–30% erode margins. Nearshoring and inventory buffers (safety stock 8–12 weeks) have reduced supplier leverage.

- Freight/energy add 8–15% to landed cost

- Typical lead times 12–24 weeks

- Expedited shipping premium 10–30%

- Nearshoring/inventory cut leverage (safety stock 8–12 weeks)

Technological co-development

Co-engineering with motor and control suppliers delivers measurable performance gains through matched torque, efficiency and control logic, and in 2024 the global industrial fan market is estimated around €6.5bn, increasing incentives for tight supplier integration. Embedded designs and firmware create lock-in as IP and bespoke tooling raise switching costs, while modular interfaces preserve flexibility and bargaining leverage.

Risk: 2–3, 12–24w, commodities +25%

Concentrated suppliers (2–3) and long lead times (12–24w) give vendors pricing/delivery leverage; commodity swings in 2024 (steel +8%, Al +5%, Cu +10%, NdPr +25%) compress margins. Logistics add 8–15% landed cost; expedited shipping 10–30% and safety stock 8–12w mitigate but raise inventory costs. Co-engineering/embedded IP increases lock-in versus modular options.

| Metric | 2024 |

|---|---|

| Supplier pool | 2–3 |

| Lead times | 12–24 weeks |

| Commodity moves | Steel +8% Al +5% Cu +10% NdPr +25% |

| Logistics | +8–15% landed |

| Market size | €6.5bn |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Nicotra Gebhardt S.p.A; evaluates suppliers' and buyers' power, threat of substitutes, competitive rivalry, and barriers protecting incumbents, with strategic commentary on disruptive forces and actionable implications for pricing and profitability.

Concise Porter's Five Forces snapshot for Nicotra Gebhardt S.p.A—clear, customizable pressure levels and radar visualization to simplify strategic decisions and slot directly into pitch decks or dashboards.

Customers Bargaining Power

Project-based procurement

Project-based procurement for HVAC OEMs, contractors and infrastructure clients is dominated by tenders, with over 65% of large system contracts awarded through competitive bidding in 2024, intensifying price pressure and compressing supplier margins by 200–400 basis points. Award criteria increasingly blend lowest cost with energy efficiency and delivery timelines, while stringent prequalification and technical specs can shift bargaining power toward clients or, when niche capabilities are required, back to Nicotra Gebhardt.

Moderate switching costs

Fans are often standardized by size and duty points, so switching suppliers is feasible but not frictionless. Re‑qualification, BIM model updates and commissioning introduce time and performance risks that raise switching costs. For AHUs, system integration and certification create greater stickiness. Established service history and transferable warranties further bias buyers toward incumbent suppliers.

Volume and consolidation

Large OEMs and global contractors aggregate purchasing volumes for components like blowers and fans, securing framework agreements that often include volume rebates typically in the 5–12% range, increasing their negotiating leverage with suppliers such as Nicotra Gebhardt S.p.A.

Smaller distributors, handling under 5% of total sector volume each, lack scale and accept thinner margins, limiting their bargaining power relative to consolidated buyers.

Regional sales mix matters: Western Europe and North America buyers generally achieve higher average discounts (often 6–10%) versus emerging markets, where discounts are lower due to fragmented demand and price sensitivity.

Performance and compliance sensitivity

Buyers of Nicotra Gebhardt blowers prioritize energy efficiency, low acoustic emission and regulatory conformity, since 2024 standards and procurement tenders price lifecycle energy and noise performance over initial cost.

Non‑compliance risks fines and retrofit charges that materially reduce willingness to switch suppliers on price alone; certified test data and EU/ISO labels attenuate buyer bargaining power.

Lifecycle TCO arguments shift negotiation toward opex savings and service contracts, improving margin resilience.

- verified labels reduce price pressure

- compliance avoids retrofit fines

- TCO focus favors higher‑efficiency models

Cyclical end-markets

Cyclical construction and industrial end-markets drive order timing for Nicotra Gebhardt, so buyer leverage rises in downturns when customers press harder on price and payment terms; in 2024 several European construction segments remained uneven, sustaining demand volatility. During tight supply phases, customers prioritize delivery reliability over discounts, and the companys backlog coverage—when high—reduces buyer bargaining power.

- 2024 demand volatility: cyclical order timing

- Downturns: stronger price/term pressure

- Tight supply: delivery > discounts

- High backlog: moderates customer leverage

Buyers wield high power: 65% tenders, margins 200–400 bp

Customers hold moderate-to-high bargaining power: 65% of large HVAC contracts awarded by tender in 2024, compressing supplier margins 200–400 bp; large buyers secure 5–12% volume rebates while Western buyers achieve 6–10% discounts; switching costs (requalification, certification) and certified efficiency labels mitigate pure price pressure.

| Metric | 2024 | Impact |

|---|---|---|

| Tender share | 65% | Higher price pressure |

| Margin compression | 200–400 bp | Reduced supplier margins |

| Volume rebates | 5–12% | Buyer leverage |

| West discounts | 6–10% | Regional pressure |

| Distributor share | <5% | Low leverage |

Preview the Actual Deliverable

Nicotra Gebhardt S.p.A Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Nicotra Gebhardt S.p.A you'll receive immediately after purchase—no surprises or placeholders. The report assesses competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications for market positioning. It's professionally formatted, ready for download and immediate use.