Nidec PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Nidec's performance is being reshaped by political trade tensions, shifting economic cycles, rapid electrification and automation, social sustainability expectations, and tightening regulatory standards. Our concise PESTLE highlights these external pressures and strategic implications in plain terms. Purchase the full analysis to access actionable insights and detailed forecasts you can use immediately.

Political factors

Trade policy and tariffs

Shifts in US–China trade policy since 2018, notably US tariffs of up to 25% on about $250bn of Chinese goods, affect flows of motors, magnets and electronics into Nidec’s supply chain. Tariffs on components or finished motors can materially reshape margins and pricing for manufacturers with cross-border production. Proactive localization and diversified sourcing reduce exposure to tariff shocks. Monitoring FTAs such as the 11-member CPTPP can unlock duty savings and supply-chain flexibility.

Industrial policy and subsidies

Industrial policy and subsidies — notably the US Inflation Reduction Act's roughly $369 billion clean-energy package and up to $7,500 EV tax credit — plus China (≈60% of global EV sales in 2023), EU and Japan green incentives, are steering capital into e-axles, batteries and efficient motors. Subsidy access can materially cut project paybacks; alignment with local partners and strict compliance are prerequisites to secure funds. Policy reversals and geopolitical shifts raise execution and cash-flow risks for Nidec.

Geopolitical tensions and supply chain

Geopolitics can disrupt rare-earth magnet and controller supply chains: China accounts for over 60% of global rare‑earth processing capacity (USGS 2023). Sanctions or export restrictions can delay deliveries and raise input costs for motor and controller makers. Nidec’s multi-region production footprint across Asia, Europe and the Americas, combined with scenario planning, supports continuity for automotive and industrial customers.

Energy and infrastructure policy

Policy shifts toward higher grid efficiency and electrification are raising demand for premium motors—global electric vehicle sales reached about 14.2 million in 2023, expanding motor content and aftermarket opportunities. Public spending such as the US Infrastructure Investment and Jobs Act ($1.2 trillion) accelerates factory and logistics automation, while renewable buildouts favor specialized drive systems and converging standards ease cross-border deployment.

- Electrification: 14.2M EVs (2023)

- Public spend: IIJA $1.2T

- Renewables: drives demand for specialized inverters/drives

- Standards convergence: simplifies global rollouts

Local content and FDI rules

Local content mandates in automotive and industrial projects (often requiring significant domestic value addition) shape Nidec plant siting and supplier strategies, especially in growth markets where localisation targets can exceed 30%. FDI reviews in over 50 major markets can prolong acquisitions central to Nidec’s external-growth model, raising deal timelines and costs. Supplier qualification under public-procurement rules directly affects share gains in electrification contracts. Early regulatory engagement reduces approval friction and shortens time-to-contract.

- Localisation pressure: >30% targets

- FDI screening: >50 markets

- Procurement rules shape supplier wins

- Proactive regulator outreach cuts delays

Tariffs, FDI screening and rare-earth risks lift e-motor costs as IRA fuels EV demand

US–China tariffs on ~$250bn of goods and FDI screening in >50 markets raise sourcing and M&A costs for Nidec. Clean-energy incentives (IRA ~$369bn; up to $7,500 EV credit) and 14.2M EVs (2023) boost e-motor demand but require localisation (>30% in some projects). China controls ~60% of rare‑earth processing, creating supply risk mitigated by multi-region plants and allied sourcing.

| Metric | Value |

|---|---|

| Tariff base | $250bn |

| IRA size | $369bn |

| EV sales (2023) | 14.2M |

| China rare‑earth share | ≈60% |

What is included in the product

Provides a concise PESTLE analysis of Nidec, examining Political, Economic, Social, Technological, Environmental and Legal forces with data-backed trends and region-specific examples to reveal risks, opportunities and strategic implications for executives, investors and planners.

Concise Nidec PESTLE summary isolating regulatory, technological, and supply‑chain risks by category for quick reference in meetings, enabling teams to align mitigation plans and add region‑ or business‑specific notes.

Economic factors

Global demand cycles

Cyclicality in electronics, appliances and autos drives sharp volume swings—global auto production ~80 million units (2023) causing demand volatility for traction and small motors; HDD and consumer-goods inventory corrections periodically depress small motor lines; industrial capex cycles boost demand for larger motors and factory automation; Nidec’s diversified end-market mix helps cushion downturns.

FX and yen sensitivity

Nidec generates roughly 90% of revenue outside Japan while a portion of costs (HQ, R&D, some supply contracts) remain yen-denominated, so yen swings materially affect margins and pricing competitiveness. Active FX hedging, geographic cost matching and local sourcing have reduced realized exposure in recent years. Currency moves also alter acquisition valuations and cross-border deal economics, impacting reported goodwill and purchase price in yen terms.

Interest rates and capex

Higher global policy rates, with the US federal funds rate at 5.25–5.50% in 2024–25, raise borrowing costs and dampen customer capex for automation, lengthening payback periods for efficiency upgrades and delaying orders; conversely lower rates can reaccelerate project pipelines, while disciplined capital allocation helps Nidec preserve ROIC through cycles.

Input costs and materials

Copper (~9,500 USD/ton LME 2024), hot‑rolled steel (~800 USD/ton 2024) and NdPr rare‑earths (~70 USD/kg 2024) drive Nidec’s BOM volatility; swings inflate motor costs and margin pressure. Long‑term supply contracts and design optimization (efficiency/part count reduction) defend margins. Substitution, increased magnet recycling and transparent commodity surcharges enable pass‑through of spikes.

- Copper price 2024: ~9,500 USD/ton

- Steel HRC 2024: ~800 USD/ton

- NdPr 2024: ~70 USD/kg

- Defensive levers: contracts, design, substitution, recycling, surcharges

Labor markets and productivity

Tight labor markets—Japan unemployment ~2.5% in 2024—push wage costs at Nidec plants and suppliers, while automation (industrial robot installations rose sharply through 2023) and lean initiatives mitigate unit-cost inflation; regional talent availability influences site choices and training programs maintain quality as volume scales.

- Wage pressure: Japan unemployment ~2.5% (2024)

- Automation: rising robot adoption reduces unit costs

- Footprint: talent pools drive location decisions

- Training: sustains quality at higher output

Tariffs, FDI screening and rare-earth risks lift e-motor costs as IRA fuels EV demand

Cyclicality in autos (global production ~80M units in 2023), HDD and consumer inventory swings drive motor demand volatility; Nidec’s diversified end markets cushion downturns.

About 90% of revenue is generated outside Japan, so yen moves matter; FX hedging and local sourcing have reduced realized exposure.

Higher rates (US funds 5.25–5.50% in 2024–25) and commodity costs (Cu ~9,500 USD/t; HRC ~800 USD/t; NdPr ~70 USD/kg in 2024) squeeze margins; contracts, design and recycling mitigate.

| Metric | Value (2024) |

|---|---|

| Global auto prod. | ~80M units (2023) |

| Revenue ex-Japan | ~90% |

| US rate | 5.25–5.50% |

| Copper | ~9,500 USD/t |

| NdPr | ~70 USD/kg |

What You See Is What You Get

Nidec PESTLE Analysis

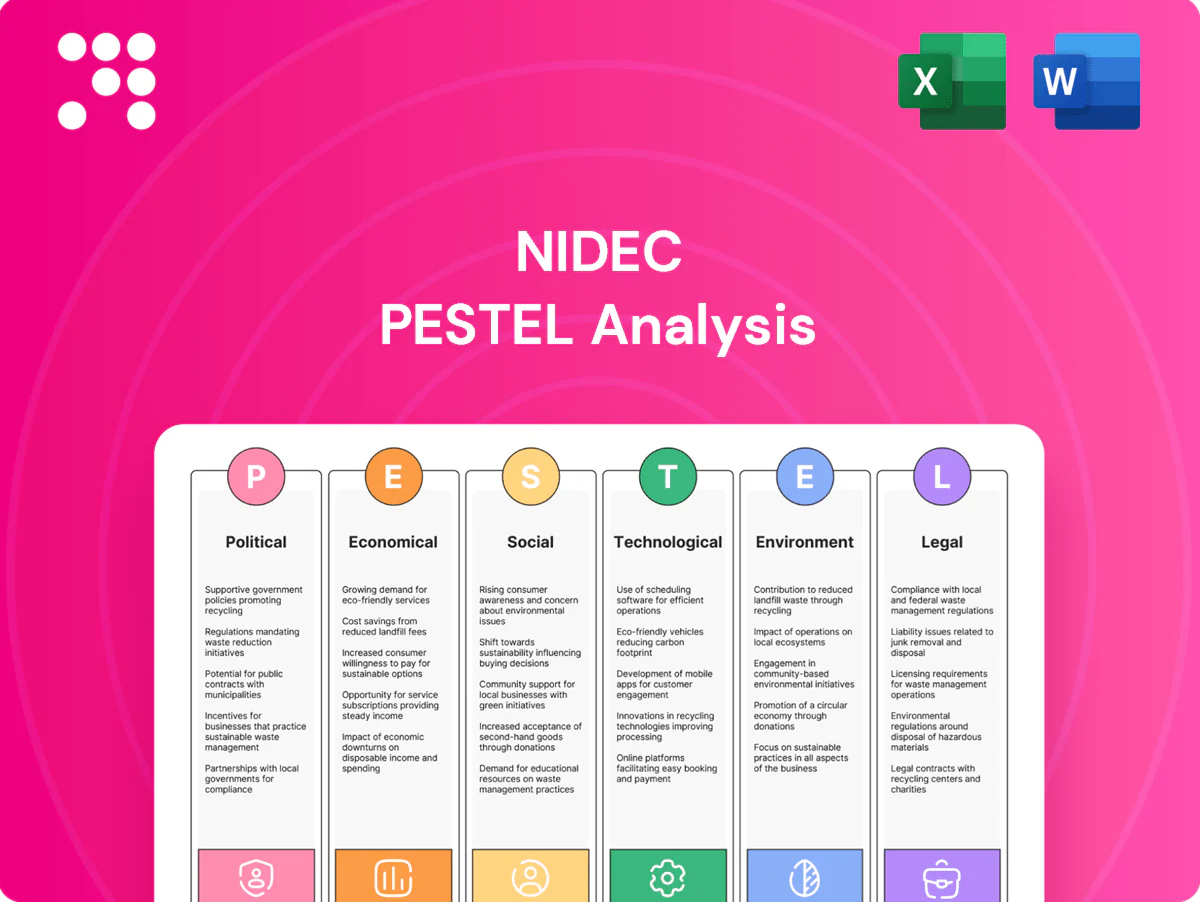

The Nidec PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors affecting Nidec with sourced insights and practical implications. What you see is the final file available for immediate download upon payment.

Your Shortcut to Market Insight Starts Here

Nidec's performance is being reshaped by political trade tensions, shifting economic cycles, rapid electrification and automation, social sustainability expectations, and tightening regulatory standards. Our concise PESTLE highlights these external pressures and strategic implications in plain terms. Purchase the full analysis to access actionable insights and detailed forecasts you can use immediately.

Political factors

Trade policy and tariffs

Shifts in US–China trade policy since 2018, notably US tariffs of up to 25% on about $250bn of Chinese goods, affect flows of motors, magnets and electronics into Nidec’s supply chain. Tariffs on components or finished motors can materially reshape margins and pricing for manufacturers with cross-border production. Proactive localization and diversified sourcing reduce exposure to tariff shocks. Monitoring FTAs such as the 11-member CPTPP can unlock duty savings and supply-chain flexibility.

Industrial policy and subsidies

Industrial policy and subsidies — notably the US Inflation Reduction Act's roughly $369 billion clean-energy package and up to $7,500 EV tax credit — plus China (≈60% of global EV sales in 2023), EU and Japan green incentives, are steering capital into e-axles, batteries and efficient motors. Subsidy access can materially cut project paybacks; alignment with local partners and strict compliance are prerequisites to secure funds. Policy reversals and geopolitical shifts raise execution and cash-flow risks for Nidec.

Geopolitical tensions and supply chain

Geopolitics can disrupt rare-earth magnet and controller supply chains: China accounts for over 60% of global rare‑earth processing capacity (USGS 2023). Sanctions or export restrictions can delay deliveries and raise input costs for motor and controller makers. Nidec’s multi-region production footprint across Asia, Europe and the Americas, combined with scenario planning, supports continuity for automotive and industrial customers.

Energy and infrastructure policy

Policy shifts toward higher grid efficiency and electrification are raising demand for premium motors—global electric vehicle sales reached about 14.2 million in 2023, expanding motor content and aftermarket opportunities. Public spending such as the US Infrastructure Investment and Jobs Act ($1.2 trillion) accelerates factory and logistics automation, while renewable buildouts favor specialized drive systems and converging standards ease cross-border deployment.

- Electrification: 14.2M EVs (2023)

- Public spend: IIJA $1.2T

- Renewables: drives demand for specialized inverters/drives

- Standards convergence: simplifies global rollouts

Local content and FDI rules

Local content mandates in automotive and industrial projects (often requiring significant domestic value addition) shape Nidec plant siting and supplier strategies, especially in growth markets where localisation targets can exceed 30%. FDI reviews in over 50 major markets can prolong acquisitions central to Nidec’s external-growth model, raising deal timelines and costs. Supplier qualification under public-procurement rules directly affects share gains in electrification contracts. Early regulatory engagement reduces approval friction and shortens time-to-contract.

- Localisation pressure: >30% targets

- FDI screening: >50 markets

- Procurement rules shape supplier wins

- Proactive regulator outreach cuts delays

Tariffs, FDI screening and rare-earth risks lift e-motor costs as IRA fuels EV demand

US–China tariffs on ~$250bn of goods and FDI screening in >50 markets raise sourcing and M&A costs for Nidec. Clean-energy incentives (IRA ~$369bn; up to $7,500 EV credit) and 14.2M EVs (2023) boost e-motor demand but require localisation (>30% in some projects). China controls ~60% of rare‑earth processing, creating supply risk mitigated by multi-region plants and allied sourcing.

| Metric | Value |

|---|---|

| Tariff base | $250bn |

| IRA size | $369bn |

| EV sales (2023) | 14.2M |

| China rare‑earth share | ≈60% |

What is included in the product

Provides a concise PESTLE analysis of Nidec, examining Political, Economic, Social, Technological, Environmental and Legal forces with data-backed trends and region-specific examples to reveal risks, opportunities and strategic implications for executives, investors and planners.

Concise Nidec PESTLE summary isolating regulatory, technological, and supply‑chain risks by category for quick reference in meetings, enabling teams to align mitigation plans and add region‑ or business‑specific notes.

Economic factors

Global demand cycles

Cyclicality in electronics, appliances and autos drives sharp volume swings—global auto production ~80 million units (2023) causing demand volatility for traction and small motors; HDD and consumer-goods inventory corrections periodically depress small motor lines; industrial capex cycles boost demand for larger motors and factory automation; Nidec’s diversified end-market mix helps cushion downturns.

FX and yen sensitivity

Nidec generates roughly 90% of revenue outside Japan while a portion of costs (HQ, R&D, some supply contracts) remain yen-denominated, so yen swings materially affect margins and pricing competitiveness. Active FX hedging, geographic cost matching and local sourcing have reduced realized exposure in recent years. Currency moves also alter acquisition valuations and cross-border deal economics, impacting reported goodwill and purchase price in yen terms.

Interest rates and capex

Higher global policy rates, with the US federal funds rate at 5.25–5.50% in 2024–25, raise borrowing costs and dampen customer capex for automation, lengthening payback periods for efficiency upgrades and delaying orders; conversely lower rates can reaccelerate project pipelines, while disciplined capital allocation helps Nidec preserve ROIC through cycles.

Input costs and materials

Copper (~9,500 USD/ton LME 2024), hot‑rolled steel (~800 USD/ton 2024) and NdPr rare‑earths (~70 USD/kg 2024) drive Nidec’s BOM volatility; swings inflate motor costs and margin pressure. Long‑term supply contracts and design optimization (efficiency/part count reduction) defend margins. Substitution, increased magnet recycling and transparent commodity surcharges enable pass‑through of spikes.

- Copper price 2024: ~9,500 USD/ton

- Steel HRC 2024: ~800 USD/ton

- NdPr 2024: ~70 USD/kg

- Defensive levers: contracts, design, substitution, recycling, surcharges

Labor markets and productivity

Tight labor markets—Japan unemployment ~2.5% in 2024—push wage costs at Nidec plants and suppliers, while automation (industrial robot installations rose sharply through 2023) and lean initiatives mitigate unit-cost inflation; regional talent availability influences site choices and training programs maintain quality as volume scales.

- Wage pressure: Japan unemployment ~2.5% (2024)

- Automation: rising robot adoption reduces unit costs

- Footprint: talent pools drive location decisions

- Training: sustains quality at higher output

Tariffs, FDI screening and rare-earth risks lift e-motor costs as IRA fuels EV demand

Cyclicality in autos (global production ~80M units in 2023), HDD and consumer inventory swings drive motor demand volatility; Nidec’s diversified end markets cushion downturns.

About 90% of revenue is generated outside Japan, so yen moves matter; FX hedging and local sourcing have reduced realized exposure.

Higher rates (US funds 5.25–5.50% in 2024–25) and commodity costs (Cu ~9,500 USD/t; HRC ~800 USD/t; NdPr ~70 USD/kg in 2024) squeeze margins; contracts, design and recycling mitigate.

| Metric | Value (2024) |

|---|---|

| Global auto prod. | ~80M units (2023) |

| Revenue ex-Japan | ~90% |

| US rate | 5.25–5.50% |

| Copper | ~9,500 USD/t |

| NdPr | ~70 USD/kg |

What You See Is What You Get

Nidec PESTLE Analysis

The Nidec PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors affecting Nidec with sourced insights and practical implications. What you see is the final file available for immediate download upon payment.

Description

Your Shortcut to Market Insight Starts Here

Nidec's performance is being reshaped by political trade tensions, shifting economic cycles, rapid electrification and automation, social sustainability expectations, and tightening regulatory standards. Our concise PESTLE highlights these external pressures and strategic implications in plain terms. Purchase the full analysis to access actionable insights and detailed forecasts you can use immediately.

Political factors

Trade policy and tariffs

Shifts in US–China trade policy since 2018, notably US tariffs of up to 25% on about $250bn of Chinese goods, affect flows of motors, magnets and electronics into Nidec’s supply chain. Tariffs on components or finished motors can materially reshape margins and pricing for manufacturers with cross-border production. Proactive localization and diversified sourcing reduce exposure to tariff shocks. Monitoring FTAs such as the 11-member CPTPP can unlock duty savings and supply-chain flexibility.

Industrial policy and subsidies

Industrial policy and subsidies — notably the US Inflation Reduction Act's roughly $369 billion clean-energy package and up to $7,500 EV tax credit — plus China (≈60% of global EV sales in 2023), EU and Japan green incentives, are steering capital into e-axles, batteries and efficient motors. Subsidy access can materially cut project paybacks; alignment with local partners and strict compliance are prerequisites to secure funds. Policy reversals and geopolitical shifts raise execution and cash-flow risks for Nidec.

Geopolitical tensions and supply chain

Geopolitics can disrupt rare-earth magnet and controller supply chains: China accounts for over 60% of global rare‑earth processing capacity (USGS 2023). Sanctions or export restrictions can delay deliveries and raise input costs for motor and controller makers. Nidec’s multi-region production footprint across Asia, Europe and the Americas, combined with scenario planning, supports continuity for automotive and industrial customers.

Energy and infrastructure policy

Policy shifts toward higher grid efficiency and electrification are raising demand for premium motors—global electric vehicle sales reached about 14.2 million in 2023, expanding motor content and aftermarket opportunities. Public spending such as the US Infrastructure Investment and Jobs Act ($1.2 trillion) accelerates factory and logistics automation, while renewable buildouts favor specialized drive systems and converging standards ease cross-border deployment.

- Electrification: 14.2M EVs (2023)

- Public spend: IIJA $1.2T

- Renewables: drives demand for specialized inverters/drives

- Standards convergence: simplifies global rollouts

Local content and FDI rules

Local content mandates in automotive and industrial projects (often requiring significant domestic value addition) shape Nidec plant siting and supplier strategies, especially in growth markets where localisation targets can exceed 30%. FDI reviews in over 50 major markets can prolong acquisitions central to Nidec’s external-growth model, raising deal timelines and costs. Supplier qualification under public-procurement rules directly affects share gains in electrification contracts. Early regulatory engagement reduces approval friction and shortens time-to-contract.

- Localisation pressure: >30% targets

- FDI screening: >50 markets

- Procurement rules shape supplier wins

- Proactive regulator outreach cuts delays

Tariffs, FDI screening and rare-earth risks lift e-motor costs as IRA fuels EV demand

US–China tariffs on ~$250bn of goods and FDI screening in >50 markets raise sourcing and M&A costs for Nidec. Clean-energy incentives (IRA ~$369bn; up to $7,500 EV credit) and 14.2M EVs (2023) boost e-motor demand but require localisation (>30% in some projects). China controls ~60% of rare‑earth processing, creating supply risk mitigated by multi-region plants and allied sourcing.

| Metric | Value |

|---|---|

| Tariff base | $250bn |

| IRA size | $369bn |

| EV sales (2023) | 14.2M |

| China rare‑earth share | ≈60% |

What is included in the product

Provides a concise PESTLE analysis of Nidec, examining Political, Economic, Social, Technological, Environmental and Legal forces with data-backed trends and region-specific examples to reveal risks, opportunities and strategic implications for executives, investors and planners.

Concise Nidec PESTLE summary isolating regulatory, technological, and supply‑chain risks by category for quick reference in meetings, enabling teams to align mitigation plans and add region‑ or business‑specific notes.

Economic factors

Global demand cycles

Cyclicality in electronics, appliances and autos drives sharp volume swings—global auto production ~80 million units (2023) causing demand volatility for traction and small motors; HDD and consumer-goods inventory corrections periodically depress small motor lines; industrial capex cycles boost demand for larger motors and factory automation; Nidec’s diversified end-market mix helps cushion downturns.

FX and yen sensitivity

Nidec generates roughly 90% of revenue outside Japan while a portion of costs (HQ, R&D, some supply contracts) remain yen-denominated, so yen swings materially affect margins and pricing competitiveness. Active FX hedging, geographic cost matching and local sourcing have reduced realized exposure in recent years. Currency moves also alter acquisition valuations and cross-border deal economics, impacting reported goodwill and purchase price in yen terms.

Interest rates and capex

Higher global policy rates, with the US federal funds rate at 5.25–5.50% in 2024–25, raise borrowing costs and dampen customer capex for automation, lengthening payback periods for efficiency upgrades and delaying orders; conversely lower rates can reaccelerate project pipelines, while disciplined capital allocation helps Nidec preserve ROIC through cycles.

Input costs and materials

Copper (~9,500 USD/ton LME 2024), hot‑rolled steel (~800 USD/ton 2024) and NdPr rare‑earths (~70 USD/kg 2024) drive Nidec’s BOM volatility; swings inflate motor costs and margin pressure. Long‑term supply contracts and design optimization (efficiency/part count reduction) defend margins. Substitution, increased magnet recycling and transparent commodity surcharges enable pass‑through of spikes.

- Copper price 2024: ~9,500 USD/ton

- Steel HRC 2024: ~800 USD/ton

- NdPr 2024: ~70 USD/kg

- Defensive levers: contracts, design, substitution, recycling, surcharges

Labor markets and productivity

Tight labor markets—Japan unemployment ~2.5% in 2024—push wage costs at Nidec plants and suppliers, while automation (industrial robot installations rose sharply through 2023) and lean initiatives mitigate unit-cost inflation; regional talent availability influences site choices and training programs maintain quality as volume scales.

- Wage pressure: Japan unemployment ~2.5% (2024)

- Automation: rising robot adoption reduces unit costs

- Footprint: talent pools drive location decisions

- Training: sustains quality at higher output

Tariffs, FDI screening and rare-earth risks lift e-motor costs as IRA fuels EV demand

Cyclicality in autos (global production ~80M units in 2023), HDD and consumer inventory swings drive motor demand volatility; Nidec’s diversified end markets cushion downturns.

About 90% of revenue is generated outside Japan, so yen moves matter; FX hedging and local sourcing have reduced realized exposure.

Higher rates (US funds 5.25–5.50% in 2024–25) and commodity costs (Cu ~9,500 USD/t; HRC ~800 USD/t; NdPr ~70 USD/kg in 2024) squeeze margins; contracts, design and recycling mitigate.

| Metric | Value (2024) |

|---|---|

| Global auto prod. | ~80M units (2023) |

| Revenue ex-Japan | ~90% |

| US rate | 5.25–5.50% |

| Copper | ~9,500 USD/t |

| NdPr | ~70 USD/kg |

What You See Is What You Get

Nidec PESTLE Analysis

The Nidec PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors affecting Nidec with sourced insights and practical implications. What you see is the final file available for immediate download upon payment.