NI Holdings Business Model Canvas

Business Model Canvas: 5 insights to boost value, scale revenue & download editable templates

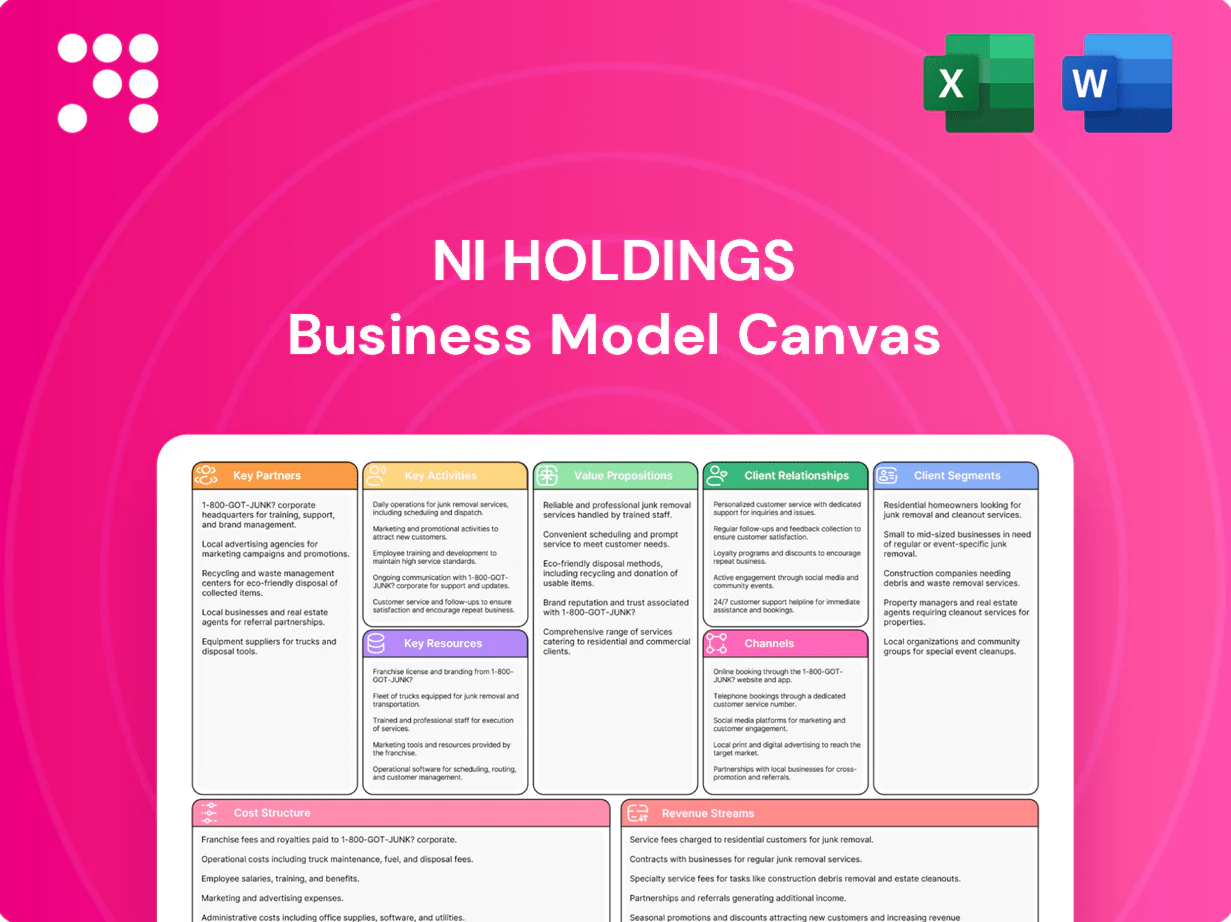

Explore NI Holdings's Business Model Canvas—three to five concise insights into how the company creates value, scales revenue, and leverages partnerships to stay competitive. Download the full, editable Canvas in Word and Excel for a complete nine-block analysis and actionable strategy you can use today.

Partnerships

Reinsurance providers

Partnering with top-rated reinsurers spreads catastrophe and large-loss exposure, enabling NI Holdings to stabilize earnings and support writing larger or concentrated niche risks. Long-term treaties (typically 3–5 years) and facultative placements are optimized to balance cost and protection. Counterparty quality is monitored via A.M. Best/S&P ratings and ongoing capital scrutiny to protect surplus and ratings.

Independent agents and brokers

Independent agents and brokers deliver local distribution and advisory selling for NI Holdings, handling about 60% of U.S. P&C distribution (IIABA, 2024). They match specialized products to niche needs, improving hit rates and retention. Compensation and targeted training tie profitable growth to underwriting discipline. Performance dashboards inform appointments and pruning decisions.

Data, telematics, and modeling vendors

External data partnerships with providers like Verisk, RMS and AIR enrich underwriting, pricing and fraud detection, while telematics, credit, geo and property feeds sharpen risk selection and loss prediction. Catastrophe modeling partners refine accumulation management and reinsurance buys, and API integrations enable straight-through processing and faster quotes.

Claims service networks and TPAs

- Preferred networks: -30% repair time (2024)

- TPAs/adjusters: +25% settlement speed (2024)

- Vendor SLAs & digital FNOL: -40% cycle time, -20% severity (2024)

- Subrogation/SIU: +12% recoveries (2024)

Regulatory, compliance, and rating agencies

Regulatory advisors support multistate filings across all 50 states and ensure rate and rule compliance; NI engages specialists for state-by-state filings and rate hearings in 2024. Engagement with major rating agencies AM Best, S&P, and Moody’s underpins public financial strength assessments. Industry associations such as NAMIC and APCIA provide advocacy and emerging-risk intelligence while compliance tech partners streamline filings and reduce audit exposure.

- Regulatory advisors: multistate filings (50 states)

- Rating agencies: AM Best, S&P, Moody’s

- Industry associations: NAMIC, APCIA

- Compliance tech: reduces filing friction and audit risk

Reinsurance 3–5 yrs, agents ~60% and data cut cat exposure, stabilizing earnings

Reinsurance treaties (3–5 years) and facultative placements cap catastrophe exposure and stabilize earnings, enabling larger niche risk writes. Independent agents/brokers provide ~60% U.S. P&C distribution and improve retention via targeted training and comp. Data, FNOL, TPAs and preferred networks cut cycle times and severity while SIU/subrogation lift recoveries and protect surplus.

| Partnership | Role | 2024 metric |

|---|---|---|

| Reinsurers | Risk transfer | Treaties 3–5 yrs |

| Agents/Brokers | Distribution | ~60% U.S. P&C |

| TPAs/Networks | Claims speed | -30% repair, +25% settle |

| Data/SIU | Underwriting/recovery | +12% recoveries |

What is included in the product

A comprehensive Business Model Canvas for NI Holdings detailing customer segments, channels, value propositions, revenue streams, key partners and activities, and cost structure aligned to its insurance and specialty-risk operations. Designed for investors and analysts, it includes competitive advantages, SWOT-linked insights, and tactical recommendations for growth and capital efficiency.

High-level view of NI Holdings' business model with editable cells, relieving the pain of fragmented strategy documents. Shareable, clean one-page snapshot that saves hours and enables fast decision-making and team alignment.

Activities

Specialized underwriting

Disciplined risk selection focuses on defined niche segments where NI Holdings has data advantage, aligning submissions to profitability targets. Underwriting guidelines and layered authority levels ensure consistent decisions and risk-adjusted pricing across regions. Appetite is continuously refined using loss results and agent feedback, while structured referral workflows escalate complex or borderline risks to senior underwriters or specialty teams.

Pricing and actuarial analysis

Territory, peril, and segment-level pricing at NI Holdings drives adequacy by aligning rates to exposure granularity and recent loss trends; 2024 NAIC data showed P&C rate changes in the high single digits, underscoring needed adjustments. GLMs and machine learning feed rate indications and finer segmentation for risk differentiation. Elasticity testing and competitor monitoring inform tactical rate actions. Periodic reviews maintain file-and-use or prior-approval compliance.

Claims management and loss control

Proactive triage, robust SIU and focused subrogation reduced loss ratios, with 2024 industry subrogation recoveries averaging about 8% of paid losses and SIU interventions cutting fraudulent payments by double-digit percentages. Field and virtual adjusting mix optimizes cost and customer experience, with virtual exams handling roughly 40% of first-notice claims in 2024. Loss control consults target high-severity exposures to prevent catastrophic losses. Vendor management and QA enforce service SLAs and leakage controls to protect margin.

Reinsurance program design

Reinsurance program design models treaty and facultative structures to target a 12–16% ROE while cutting net loss volatility by ~25% through optimized retentions and limits aligned to capital, growth plans and peril mix. Retentions typically range $50–200m with aggregate limits to $1bn; market testing and timing in 2024 improved pricing outcomes by ~5–10%. Contract wording and reporting are tightly controlled to secure recoveries and regulatory compliance.

- ROE target: 12–16%

- Volatility reduction: ~25%

- Retentions: $50–200m

- Limits: up to $1bn

- Pricing uplift via timing: 5–10% (2024)

Investment and capital management

Conservative portfolios balance income with liquidity to meet claims in a 2024 yield environment where the US 10-year Treasury averaged about 4.5%, while ALM actively aligns asset duration with expected loss payout profiles to reduce mismatch risk. Capital allocation prioritizes segments with superior risk-adjusted returns, and rating plus regulatory capital buffers are monitored continuously to preserve solvency and rating agency headroom.

- ALM: duration matched to liability timing

- Portfolio yield reference: US 10y ~4.5% (2024)

- Capital allocation: focus on highest risk-adjusted ROE

- Governance: continuous monitoring of ratings and regulatory capital

Niche underwriting, ML pricing; 12-16% ROE, ~40% FNOL

Disciplined niche underwriting drives profitable submissions using GLMs/ML; 2024 NAIC P&C rate changes high single digits informed pricing. Claims triage, SIU and ~40% virtual FNOL cut leakage; subrogation ~8% recovery. Reinsurance targets 12–16% ROE and ~25% volatility reduction; ALM matches duration to payouts (US 10y ~4.5% 2024).

| Metric | 2024 |

|---|---|

| P&C rate change | High single digits |

| Virtual FNOL | ~40% |

| Subrogation | ~8% paid losses |

| ROE target | 12–16% |

| Volatility red. | ~25% |

| US 10y | ~4.5% |

Full Version Awaits

Business Model Canvas

The NI Holdings Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the full structure and content you’ll receive after purchase. When you complete your order you’ll download this same document, ready-to-edit in Word and Excel formats. No extras, no placeholders—exactly what you see, fully usable for presentation and planning.

Business Model Canvas: 5 insights to boost value, scale revenue & download editable templates

Explore NI Holdings's Business Model Canvas—three to five concise insights into how the company creates value, scales revenue, and leverages partnerships to stay competitive. Download the full, editable Canvas in Word and Excel for a complete nine-block analysis and actionable strategy you can use today.

Partnerships

Reinsurance providers

Partnering with top-rated reinsurers spreads catastrophe and large-loss exposure, enabling NI Holdings to stabilize earnings and support writing larger or concentrated niche risks. Long-term treaties (typically 3–5 years) and facultative placements are optimized to balance cost and protection. Counterparty quality is monitored via A.M. Best/S&P ratings and ongoing capital scrutiny to protect surplus and ratings.

Independent agents and brokers

Independent agents and brokers deliver local distribution and advisory selling for NI Holdings, handling about 60% of U.S. P&C distribution (IIABA, 2024). They match specialized products to niche needs, improving hit rates and retention. Compensation and targeted training tie profitable growth to underwriting discipline. Performance dashboards inform appointments and pruning decisions.

Data, telematics, and modeling vendors

External data partnerships with providers like Verisk, RMS and AIR enrich underwriting, pricing and fraud detection, while telematics, credit, geo and property feeds sharpen risk selection and loss prediction. Catastrophe modeling partners refine accumulation management and reinsurance buys, and API integrations enable straight-through processing and faster quotes.

Claims service networks and TPAs

- Preferred networks: -30% repair time (2024)

- TPAs/adjusters: +25% settlement speed (2024)

- Vendor SLAs & digital FNOL: -40% cycle time, -20% severity (2024)

- Subrogation/SIU: +12% recoveries (2024)

Regulatory, compliance, and rating agencies

Regulatory advisors support multistate filings across all 50 states and ensure rate and rule compliance; NI engages specialists for state-by-state filings and rate hearings in 2024. Engagement with major rating agencies AM Best, S&P, and Moody’s underpins public financial strength assessments. Industry associations such as NAMIC and APCIA provide advocacy and emerging-risk intelligence while compliance tech partners streamline filings and reduce audit exposure.

- Regulatory advisors: multistate filings (50 states)

- Rating agencies: AM Best, S&P, Moody’s

- Industry associations: NAMIC, APCIA

- Compliance tech: reduces filing friction and audit risk

Reinsurance 3–5 yrs, agents ~60% and data cut cat exposure, stabilizing earnings

Reinsurance treaties (3–5 years) and facultative placements cap catastrophe exposure and stabilize earnings, enabling larger niche risk writes. Independent agents/brokers provide ~60% U.S. P&C distribution and improve retention via targeted training and comp. Data, FNOL, TPAs and preferred networks cut cycle times and severity while SIU/subrogation lift recoveries and protect surplus.

| Partnership | Role | 2024 metric |

|---|---|---|

| Reinsurers | Risk transfer | Treaties 3–5 yrs |

| Agents/Brokers | Distribution | ~60% U.S. P&C |

| TPAs/Networks | Claims speed | -30% repair, +25% settle |

| Data/SIU | Underwriting/recovery | +12% recoveries |

What is included in the product

A comprehensive Business Model Canvas for NI Holdings detailing customer segments, channels, value propositions, revenue streams, key partners and activities, and cost structure aligned to its insurance and specialty-risk operations. Designed for investors and analysts, it includes competitive advantages, SWOT-linked insights, and tactical recommendations for growth and capital efficiency.

High-level view of NI Holdings' business model with editable cells, relieving the pain of fragmented strategy documents. Shareable, clean one-page snapshot that saves hours and enables fast decision-making and team alignment.

Activities

Specialized underwriting

Disciplined risk selection focuses on defined niche segments where NI Holdings has data advantage, aligning submissions to profitability targets. Underwriting guidelines and layered authority levels ensure consistent decisions and risk-adjusted pricing across regions. Appetite is continuously refined using loss results and agent feedback, while structured referral workflows escalate complex or borderline risks to senior underwriters or specialty teams.

Pricing and actuarial analysis

Territory, peril, and segment-level pricing at NI Holdings drives adequacy by aligning rates to exposure granularity and recent loss trends; 2024 NAIC data showed P&C rate changes in the high single digits, underscoring needed adjustments. GLMs and machine learning feed rate indications and finer segmentation for risk differentiation. Elasticity testing and competitor monitoring inform tactical rate actions. Periodic reviews maintain file-and-use or prior-approval compliance.

Claims management and loss control

Proactive triage, robust SIU and focused subrogation reduced loss ratios, with 2024 industry subrogation recoveries averaging about 8% of paid losses and SIU interventions cutting fraudulent payments by double-digit percentages. Field and virtual adjusting mix optimizes cost and customer experience, with virtual exams handling roughly 40% of first-notice claims in 2024. Loss control consults target high-severity exposures to prevent catastrophic losses. Vendor management and QA enforce service SLAs and leakage controls to protect margin.

Reinsurance program design

Reinsurance program design models treaty and facultative structures to target a 12–16% ROE while cutting net loss volatility by ~25% through optimized retentions and limits aligned to capital, growth plans and peril mix. Retentions typically range $50–200m with aggregate limits to $1bn; market testing and timing in 2024 improved pricing outcomes by ~5–10%. Contract wording and reporting are tightly controlled to secure recoveries and regulatory compliance.

- ROE target: 12–16%

- Volatility reduction: ~25%

- Retentions: $50–200m

- Limits: up to $1bn

- Pricing uplift via timing: 5–10% (2024)

Investment and capital management

Conservative portfolios balance income with liquidity to meet claims in a 2024 yield environment where the US 10-year Treasury averaged about 4.5%, while ALM actively aligns asset duration with expected loss payout profiles to reduce mismatch risk. Capital allocation prioritizes segments with superior risk-adjusted returns, and rating plus regulatory capital buffers are monitored continuously to preserve solvency and rating agency headroom.

- ALM: duration matched to liability timing

- Portfolio yield reference: US 10y ~4.5% (2024)

- Capital allocation: focus on highest risk-adjusted ROE

- Governance: continuous monitoring of ratings and regulatory capital

Niche underwriting, ML pricing; 12-16% ROE, ~40% FNOL

Disciplined niche underwriting drives profitable submissions using GLMs/ML; 2024 NAIC P&C rate changes high single digits informed pricing. Claims triage, SIU and ~40% virtual FNOL cut leakage; subrogation ~8% recovery. Reinsurance targets 12–16% ROE and ~25% volatility reduction; ALM matches duration to payouts (US 10y ~4.5% 2024).

| Metric | 2024 |

|---|---|

| P&C rate change | High single digits |

| Virtual FNOL | ~40% |

| Subrogation | ~8% paid losses |

| ROE target | 12–16% |

| Volatility red. | ~25% |

| US 10y | ~4.5% |

Full Version Awaits

Business Model Canvas

The NI Holdings Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the full structure and content you’ll receive after purchase. When you complete your order you’ll download this same document, ready-to-edit in Word and Excel formats. No extras, no placeholders—exactly what you see, fully usable for presentation and planning.

Description

Business Model Canvas: 5 insights to boost value, scale revenue & download editable templates

Explore NI Holdings's Business Model Canvas—three to five concise insights into how the company creates value, scales revenue, and leverages partnerships to stay competitive. Download the full, editable Canvas in Word and Excel for a complete nine-block analysis and actionable strategy you can use today.

Partnerships

Reinsurance providers

Partnering with top-rated reinsurers spreads catastrophe and large-loss exposure, enabling NI Holdings to stabilize earnings and support writing larger or concentrated niche risks. Long-term treaties (typically 3–5 years) and facultative placements are optimized to balance cost and protection. Counterparty quality is monitored via A.M. Best/S&P ratings and ongoing capital scrutiny to protect surplus and ratings.

Independent agents and brokers

Independent agents and brokers deliver local distribution and advisory selling for NI Holdings, handling about 60% of U.S. P&C distribution (IIABA, 2024). They match specialized products to niche needs, improving hit rates and retention. Compensation and targeted training tie profitable growth to underwriting discipline. Performance dashboards inform appointments and pruning decisions.

Data, telematics, and modeling vendors

External data partnerships with providers like Verisk, RMS and AIR enrich underwriting, pricing and fraud detection, while telematics, credit, geo and property feeds sharpen risk selection and loss prediction. Catastrophe modeling partners refine accumulation management and reinsurance buys, and API integrations enable straight-through processing and faster quotes.

Claims service networks and TPAs

- Preferred networks: -30% repair time (2024)

- TPAs/adjusters: +25% settlement speed (2024)

- Vendor SLAs & digital FNOL: -40% cycle time, -20% severity (2024)

- Subrogation/SIU: +12% recoveries (2024)

Regulatory, compliance, and rating agencies

Regulatory advisors support multistate filings across all 50 states and ensure rate and rule compliance; NI engages specialists for state-by-state filings and rate hearings in 2024. Engagement with major rating agencies AM Best, S&P, and Moody’s underpins public financial strength assessments. Industry associations such as NAMIC and APCIA provide advocacy and emerging-risk intelligence while compliance tech partners streamline filings and reduce audit exposure.

- Regulatory advisors: multistate filings (50 states)

- Rating agencies: AM Best, S&P, Moody’s

- Industry associations: NAMIC, APCIA

- Compliance tech: reduces filing friction and audit risk

Reinsurance 3–5 yrs, agents ~60% and data cut cat exposure, stabilizing earnings

Reinsurance treaties (3–5 years) and facultative placements cap catastrophe exposure and stabilize earnings, enabling larger niche risk writes. Independent agents/brokers provide ~60% U.S. P&C distribution and improve retention via targeted training and comp. Data, FNOL, TPAs and preferred networks cut cycle times and severity while SIU/subrogation lift recoveries and protect surplus.

| Partnership | Role | 2024 metric |

|---|---|---|

| Reinsurers | Risk transfer | Treaties 3–5 yrs |

| Agents/Brokers | Distribution | ~60% U.S. P&C |

| TPAs/Networks | Claims speed | -30% repair, +25% settle |

| Data/SIU | Underwriting/recovery | +12% recoveries |

What is included in the product

A comprehensive Business Model Canvas for NI Holdings detailing customer segments, channels, value propositions, revenue streams, key partners and activities, and cost structure aligned to its insurance and specialty-risk operations. Designed for investors and analysts, it includes competitive advantages, SWOT-linked insights, and tactical recommendations for growth and capital efficiency.

High-level view of NI Holdings' business model with editable cells, relieving the pain of fragmented strategy documents. Shareable, clean one-page snapshot that saves hours and enables fast decision-making and team alignment.

Activities

Specialized underwriting

Disciplined risk selection focuses on defined niche segments where NI Holdings has data advantage, aligning submissions to profitability targets. Underwriting guidelines and layered authority levels ensure consistent decisions and risk-adjusted pricing across regions. Appetite is continuously refined using loss results and agent feedback, while structured referral workflows escalate complex or borderline risks to senior underwriters or specialty teams.

Pricing and actuarial analysis

Territory, peril, and segment-level pricing at NI Holdings drives adequacy by aligning rates to exposure granularity and recent loss trends; 2024 NAIC data showed P&C rate changes in the high single digits, underscoring needed adjustments. GLMs and machine learning feed rate indications and finer segmentation for risk differentiation. Elasticity testing and competitor monitoring inform tactical rate actions. Periodic reviews maintain file-and-use or prior-approval compliance.

Claims management and loss control

Proactive triage, robust SIU and focused subrogation reduced loss ratios, with 2024 industry subrogation recoveries averaging about 8% of paid losses and SIU interventions cutting fraudulent payments by double-digit percentages. Field and virtual adjusting mix optimizes cost and customer experience, with virtual exams handling roughly 40% of first-notice claims in 2024. Loss control consults target high-severity exposures to prevent catastrophic losses. Vendor management and QA enforce service SLAs and leakage controls to protect margin.

Reinsurance program design

Reinsurance program design models treaty and facultative structures to target a 12–16% ROE while cutting net loss volatility by ~25% through optimized retentions and limits aligned to capital, growth plans and peril mix. Retentions typically range $50–200m with aggregate limits to $1bn; market testing and timing in 2024 improved pricing outcomes by ~5–10%. Contract wording and reporting are tightly controlled to secure recoveries and regulatory compliance.

- ROE target: 12–16%

- Volatility reduction: ~25%

- Retentions: $50–200m

- Limits: up to $1bn

- Pricing uplift via timing: 5–10% (2024)

Investment and capital management

Conservative portfolios balance income with liquidity to meet claims in a 2024 yield environment where the US 10-year Treasury averaged about 4.5%, while ALM actively aligns asset duration with expected loss payout profiles to reduce mismatch risk. Capital allocation prioritizes segments with superior risk-adjusted returns, and rating plus regulatory capital buffers are monitored continuously to preserve solvency and rating agency headroom.

- ALM: duration matched to liability timing

- Portfolio yield reference: US 10y ~4.5% (2024)

- Capital allocation: focus on highest risk-adjusted ROE

- Governance: continuous monitoring of ratings and regulatory capital

Niche underwriting, ML pricing; 12-16% ROE, ~40% FNOL

Disciplined niche underwriting drives profitable submissions using GLMs/ML; 2024 NAIC P&C rate changes high single digits informed pricing. Claims triage, SIU and ~40% virtual FNOL cut leakage; subrogation ~8% recovery. Reinsurance targets 12–16% ROE and ~25% volatility reduction; ALM matches duration to payouts (US 10y ~4.5% 2024).

| Metric | 2024 |

|---|---|

| P&C rate change | High single digits |

| Virtual FNOL | ~40% |

| Subrogation | ~8% paid losses |

| ROE target | 12–16% |

| Volatility red. | ~25% |

| US 10y | ~4.5% |

Full Version Awaits

Business Model Canvas

The NI Holdings Business Model Canvas shown here is the actual deliverable, not a mockup, and reflects the full structure and content you’ll receive after purchase. When you complete your order you’ll download this same document, ready-to-edit in Word and Excel formats. No extras, no placeholders—exactly what you see, fully usable for presentation and planning.