NIO Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

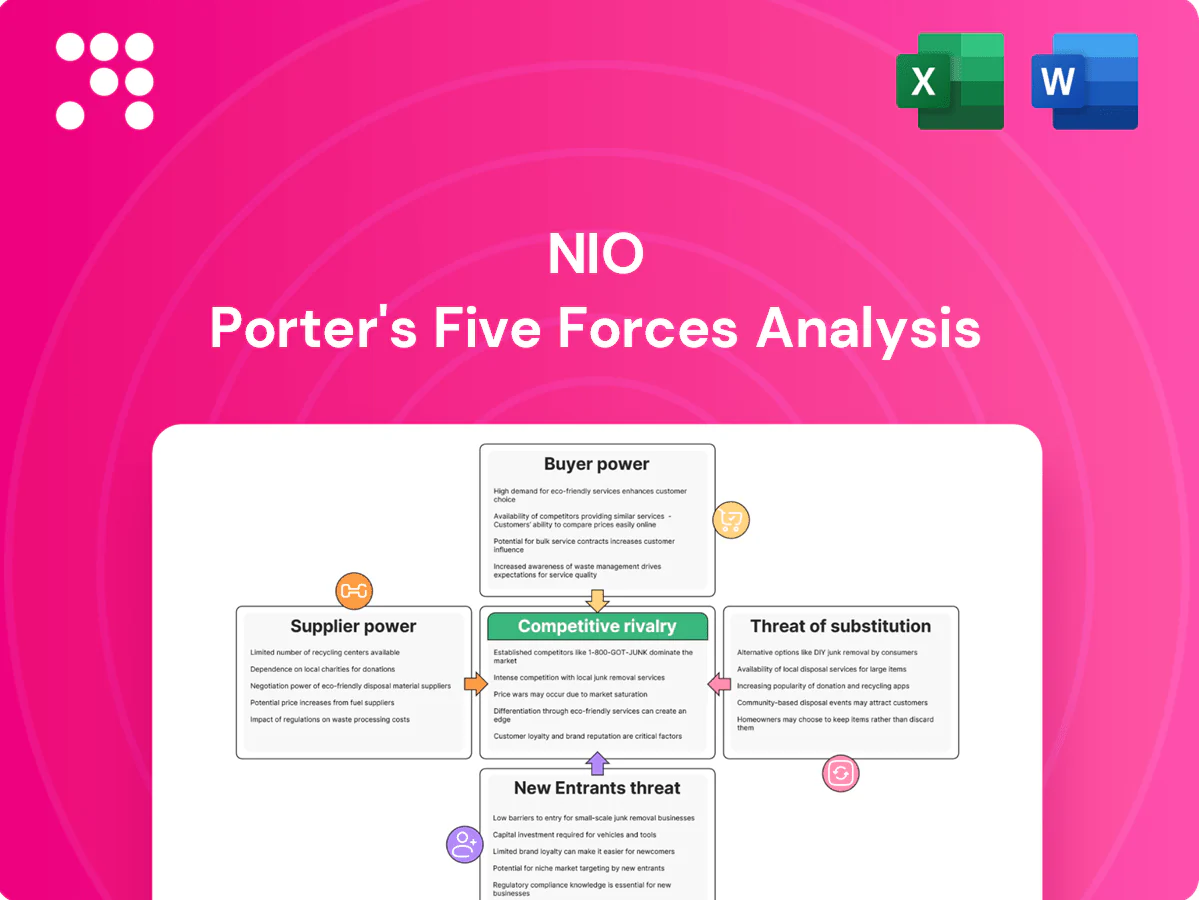

NIO faces intense competitive rivalry in the EV market, pressured by legacy automakers scaling EVs and deep-pocketed Chinese rivals, while supplier dynamics around batteries and semiconductors create episodic risks; buyer power is rising as consumers demand tech, price, and charging ecosystems. Threats from new entrants and substitutes hinge on EV adoption and alternative mobility services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NIO’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated battery and chip sources

Core cells and high-end ADAS chips are concentrated: CATL held about 30% of global EV cell shipments in 2024 (SNE Research), while US export controls on advanced AI chips to China tightened in 2023–24, raising allocation risk; NIO pursues partnerships and multi-sourcing and battery-swap options, but supplier leverage and dependence persist.

Specialized sensors and materials

Lidar, high-spec semiconductors, rare earth magnets and precision aluminum body parts rely on niche vendors, concentrating supplier power. Switching costs are high because validation cycles and safety certifications prolong qualification. Suppliers can enforce longer lead times and minimum order volumes; China accounted for roughly 60% of global rare earth production in 2024. NIO’s design standardization broadens sourcing but does not fully offset supplier leverage.

Manufacturing partners and tooling

Contract manufacturing with JAC Motors for core models and dedicated tooling elevates supplier bargaining power for NIO; NIO delivered 122,486 vehicles in 2023, locking sizeable volumes. Capacity reservations and capex-recovery clauses fix pricing and make mid-model-cycle renegotiation costly, while co-investment and joint planning are used to better align incentives.

Software and data stack dependencies

- maps: HERE, TomTom dominant licensors

- cloud: AWS/Azure/GCP >66% (2024)

- risk: API/license terms, regional compliance

- mitigation: NIO in-house NIO Pilot, mapping/connectivity

Logistics and energy ecosystem inputs

Logistics and energy inputs give suppliers meaningful leverage over NIO because battery swapping hardware, cabinets and grid connections rely on utility and infrastructure vendors; by 2024 site permitting and regional power tariffs materially affect unit economics and rollout timing. Vendors can throttle pace and margins through component pricing and lead times, while long-term contracts and adoption of standard modular cabinets mitigate but do not eliminate supplier power.

- 2024: permitting and tariff variability drive capex/Opex

- Vendors control rollout speed and unit cost

- Long-term contracts reduce supply risk

Supplier power high: CATL ~30%, rare earths ~60%, cloud >66%

Supplier power is high: CATL ~30% global cell share (2024), rare earths ~60% China (2024), and cloud providers >66% market (2024) concentrate inputs. Niche lidar/chip vendors and JAC contract tooling raise switching costs and lead-time leverage. NIO mitigates via multi-sourcing, in-house software and long-term contracts but dependence persists.

| Metric | 2024 value | Impact |

|---|---|---|

| CATL share | ~30% | Cell allocation risk |

| Rare earths (China) | ~60% | Price/availability |

| Cloud | >66% | Licensing/switching |

What is included in the product

Tailored Porter’s Five Forces analysis for NIO that uncovers competitive intensity, supplier and buyer leverage, entry barriers, substitute threats, and disruptive forces shaping its EV market position.

Clear one-sheet Porter's Five Forces for NIO—instantly spot supplier/buyer pressure, rivalry, entry threats and substitutes to streamline strategic decisions and investor pitches.

Customers Bargaining Power

Premium buyers with high expectations

Premium buyers closely compare performance, tech, and after-sales and demand rapid OTA updates plus superior service; when perceived value slips churn risk rises sharply. NIO counters with user-centric services, fast OTA rollouts, subscription battery and charging options, and strong community engagement to retain loyalty and reduce defections.

Price transparency and incentives

Frequent price cuts and shifting subsidies (central NEV subsidies phased out by end-2023) have made pricing highly visible, prompting buyers to delay purchases until promotions or new trims appear; this behavior tightens dealer and OEM margins. Buyers thus bargain indirectly by waiting for markdowns, compressing NIO’s margin leverage. NIO’s Battery-as-a-Service (launched 2020) moved to more flexible pricing in 2024 to preserve perceived value and protect upfront price points.

Moderate switching costs offset by BaaS

EV buyers face low mechanical lock-in and can switch brands easily, but NIO’s battery-swap network—over 1,600 swap stations reported by the company—and bundled ecosystem services create tangible stickiness. Data profiles from telematics and subscription packages raise lifetime value and reduce price sensitivity. Over time this narrows buyer bargaining power despite initially moderate switching costs.

Fleet and corporate procurement

Fleet and corporate procurement exert strong bargaining power over NIO: they negotiate volume discounts (commonly 5–15%) and strict service SLAs, can push for prioritized delivery schedules, and influence feature roadmaps through bundled orders; concentration of large fleet accounts increases leverage, while dedicated account teams and customized support reduce churn.

- Volume discounts: 5–15%

- Service SLAs: prioritized repairs/logistics

- Delivery influence: schedule acceleration

- Mitigation: dedicated account support

Global reviews and social influence

- Online ratings: 87% of EV buyers influenced

- Negative sentiment: quick demand impact

- Transparency: pressures pricing/releases

- Community mgmt: stabilizes perception

OTA, services and battery-swap cut churn as price visibility delays purchases and compresses margins

Premium buyers demand cutting‑edge tech, rapid OTA and superior service, raising churn when value slips; NIO offsets with OTA, services and BaaS. Price visibility and promo timing push buyers to delay purchases, compressing margins; fleet buyers extract 5–15% discounts. Battery‑swap network (1,600+ stations) and subscriptions raise switching costs; online reviews influence ~87% of EV purchases.

| Metric | Value |

|---|---|

| Swap stations | 1,600+ |

| Fleet discounts | 5–15% |

| Online influence | 87% |

Full Version Awaits

NIO Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of NIO you’ll receive immediately after purchase—no placeholders or samples. The document is the full, professionally formatted analysis, ready for download and use the moment you buy. What you see here is precisely what will be delivered to you after payment.

Go Beyond the Preview—Access the Full Strategic Report

NIO faces intense competitive rivalry in the EV market, pressured by legacy automakers scaling EVs and deep-pocketed Chinese rivals, while supplier dynamics around batteries and semiconductors create episodic risks; buyer power is rising as consumers demand tech, price, and charging ecosystems. Threats from new entrants and substitutes hinge on EV adoption and alternative mobility services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NIO’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated battery and chip sources

Core cells and high-end ADAS chips are concentrated: CATL held about 30% of global EV cell shipments in 2024 (SNE Research), while US export controls on advanced AI chips to China tightened in 2023–24, raising allocation risk; NIO pursues partnerships and multi-sourcing and battery-swap options, but supplier leverage and dependence persist.

Specialized sensors and materials

Lidar, high-spec semiconductors, rare earth magnets and precision aluminum body parts rely on niche vendors, concentrating supplier power. Switching costs are high because validation cycles and safety certifications prolong qualification. Suppliers can enforce longer lead times and minimum order volumes; China accounted for roughly 60% of global rare earth production in 2024. NIO’s design standardization broadens sourcing but does not fully offset supplier leverage.

Manufacturing partners and tooling

Contract manufacturing with JAC Motors for core models and dedicated tooling elevates supplier bargaining power for NIO; NIO delivered 122,486 vehicles in 2023, locking sizeable volumes. Capacity reservations and capex-recovery clauses fix pricing and make mid-model-cycle renegotiation costly, while co-investment and joint planning are used to better align incentives.

Software and data stack dependencies

- maps: HERE, TomTom dominant licensors

- cloud: AWS/Azure/GCP >66% (2024)

- risk: API/license terms, regional compliance

- mitigation: NIO in-house NIO Pilot, mapping/connectivity

Logistics and energy ecosystem inputs

Logistics and energy inputs give suppliers meaningful leverage over NIO because battery swapping hardware, cabinets and grid connections rely on utility and infrastructure vendors; by 2024 site permitting and regional power tariffs materially affect unit economics and rollout timing. Vendors can throttle pace and margins through component pricing and lead times, while long-term contracts and adoption of standard modular cabinets mitigate but do not eliminate supplier power.

- 2024: permitting and tariff variability drive capex/Opex

- Vendors control rollout speed and unit cost

- Long-term contracts reduce supply risk

Supplier power high: CATL ~30%, rare earths ~60%, cloud >66%

Supplier power is high: CATL ~30% global cell share (2024), rare earths ~60% China (2024), and cloud providers >66% market (2024) concentrate inputs. Niche lidar/chip vendors and JAC contract tooling raise switching costs and lead-time leverage. NIO mitigates via multi-sourcing, in-house software and long-term contracts but dependence persists.

| Metric | 2024 value | Impact |

|---|---|---|

| CATL share | ~30% | Cell allocation risk |

| Rare earths (China) | ~60% | Price/availability |

| Cloud | >66% | Licensing/switching |

What is included in the product

Tailored Porter’s Five Forces analysis for NIO that uncovers competitive intensity, supplier and buyer leverage, entry barriers, substitute threats, and disruptive forces shaping its EV market position.

Clear one-sheet Porter's Five Forces for NIO—instantly spot supplier/buyer pressure, rivalry, entry threats and substitutes to streamline strategic decisions and investor pitches.

Customers Bargaining Power

Premium buyers with high expectations

Premium buyers closely compare performance, tech, and after-sales and demand rapid OTA updates plus superior service; when perceived value slips churn risk rises sharply. NIO counters with user-centric services, fast OTA rollouts, subscription battery and charging options, and strong community engagement to retain loyalty and reduce defections.

Price transparency and incentives

Frequent price cuts and shifting subsidies (central NEV subsidies phased out by end-2023) have made pricing highly visible, prompting buyers to delay purchases until promotions or new trims appear; this behavior tightens dealer and OEM margins. Buyers thus bargain indirectly by waiting for markdowns, compressing NIO’s margin leverage. NIO’s Battery-as-a-Service (launched 2020) moved to more flexible pricing in 2024 to preserve perceived value and protect upfront price points.

Moderate switching costs offset by BaaS

EV buyers face low mechanical lock-in and can switch brands easily, but NIO’s battery-swap network—over 1,600 swap stations reported by the company—and bundled ecosystem services create tangible stickiness. Data profiles from telematics and subscription packages raise lifetime value and reduce price sensitivity. Over time this narrows buyer bargaining power despite initially moderate switching costs.

Fleet and corporate procurement

Fleet and corporate procurement exert strong bargaining power over NIO: they negotiate volume discounts (commonly 5–15%) and strict service SLAs, can push for prioritized delivery schedules, and influence feature roadmaps through bundled orders; concentration of large fleet accounts increases leverage, while dedicated account teams and customized support reduce churn.

- Volume discounts: 5–15%

- Service SLAs: prioritized repairs/logistics

- Delivery influence: schedule acceleration

- Mitigation: dedicated account support

Global reviews and social influence

- Online ratings: 87% of EV buyers influenced

- Negative sentiment: quick demand impact

- Transparency: pressures pricing/releases

- Community mgmt: stabilizes perception

OTA, services and battery-swap cut churn as price visibility delays purchases and compresses margins

Premium buyers demand cutting‑edge tech, rapid OTA and superior service, raising churn when value slips; NIO offsets with OTA, services and BaaS. Price visibility and promo timing push buyers to delay purchases, compressing margins; fleet buyers extract 5–15% discounts. Battery‑swap network (1,600+ stations) and subscriptions raise switching costs; online reviews influence ~87% of EV purchases.

| Metric | Value |

|---|---|

| Swap stations | 1,600+ |

| Fleet discounts | 5–15% |

| Online influence | 87% |

Full Version Awaits

NIO Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of NIO you’ll receive immediately after purchase—no placeholders or samples. The document is the full, professionally formatted analysis, ready for download and use the moment you buy. What you see here is precisely what will be delivered to you after payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

NIO faces intense competitive rivalry in the EV market, pressured by legacy automakers scaling EVs and deep-pocketed Chinese rivals, while supplier dynamics around batteries and semiconductors create episodic risks; buyer power is rising as consumers demand tech, price, and charging ecosystems. Threats from new entrants and substitutes hinge on EV adoption and alternative mobility services. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NIO’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated battery and chip sources

Core cells and high-end ADAS chips are concentrated: CATL held about 30% of global EV cell shipments in 2024 (SNE Research), while US export controls on advanced AI chips to China tightened in 2023–24, raising allocation risk; NIO pursues partnerships and multi-sourcing and battery-swap options, but supplier leverage and dependence persist.

Specialized sensors and materials

Lidar, high-spec semiconductors, rare earth magnets and precision aluminum body parts rely on niche vendors, concentrating supplier power. Switching costs are high because validation cycles and safety certifications prolong qualification. Suppliers can enforce longer lead times and minimum order volumes; China accounted for roughly 60% of global rare earth production in 2024. NIO’s design standardization broadens sourcing but does not fully offset supplier leverage.

Manufacturing partners and tooling

Contract manufacturing with JAC Motors for core models and dedicated tooling elevates supplier bargaining power for NIO; NIO delivered 122,486 vehicles in 2023, locking sizeable volumes. Capacity reservations and capex-recovery clauses fix pricing and make mid-model-cycle renegotiation costly, while co-investment and joint planning are used to better align incentives.

Software and data stack dependencies

- maps: HERE, TomTom dominant licensors

- cloud: AWS/Azure/GCP >66% (2024)

- risk: API/license terms, regional compliance

- mitigation: NIO in-house NIO Pilot, mapping/connectivity

Logistics and energy ecosystem inputs

Logistics and energy inputs give suppliers meaningful leverage over NIO because battery swapping hardware, cabinets and grid connections rely on utility and infrastructure vendors; by 2024 site permitting and regional power tariffs materially affect unit economics and rollout timing. Vendors can throttle pace and margins through component pricing and lead times, while long-term contracts and adoption of standard modular cabinets mitigate but do not eliminate supplier power.

- 2024: permitting and tariff variability drive capex/Opex

- Vendors control rollout speed and unit cost

- Long-term contracts reduce supply risk

Supplier power high: CATL ~30%, rare earths ~60%, cloud >66%

Supplier power is high: CATL ~30% global cell share (2024), rare earths ~60% China (2024), and cloud providers >66% market (2024) concentrate inputs. Niche lidar/chip vendors and JAC contract tooling raise switching costs and lead-time leverage. NIO mitigates via multi-sourcing, in-house software and long-term contracts but dependence persists.

| Metric | 2024 value | Impact |

|---|---|---|

| CATL share | ~30% | Cell allocation risk |

| Rare earths (China) | ~60% | Price/availability |

| Cloud | >66% | Licensing/switching |

What is included in the product

Tailored Porter’s Five Forces analysis for NIO that uncovers competitive intensity, supplier and buyer leverage, entry barriers, substitute threats, and disruptive forces shaping its EV market position.

Clear one-sheet Porter's Five Forces for NIO—instantly spot supplier/buyer pressure, rivalry, entry threats and substitutes to streamline strategic decisions and investor pitches.

Customers Bargaining Power

Premium buyers with high expectations

Premium buyers closely compare performance, tech, and after-sales and demand rapid OTA updates plus superior service; when perceived value slips churn risk rises sharply. NIO counters with user-centric services, fast OTA rollouts, subscription battery and charging options, and strong community engagement to retain loyalty and reduce defections.

Price transparency and incentives

Frequent price cuts and shifting subsidies (central NEV subsidies phased out by end-2023) have made pricing highly visible, prompting buyers to delay purchases until promotions or new trims appear; this behavior tightens dealer and OEM margins. Buyers thus bargain indirectly by waiting for markdowns, compressing NIO’s margin leverage. NIO’s Battery-as-a-Service (launched 2020) moved to more flexible pricing in 2024 to preserve perceived value and protect upfront price points.

Moderate switching costs offset by BaaS

EV buyers face low mechanical lock-in and can switch brands easily, but NIO’s battery-swap network—over 1,600 swap stations reported by the company—and bundled ecosystem services create tangible stickiness. Data profiles from telematics and subscription packages raise lifetime value and reduce price sensitivity. Over time this narrows buyer bargaining power despite initially moderate switching costs.

Fleet and corporate procurement

Fleet and corporate procurement exert strong bargaining power over NIO: they negotiate volume discounts (commonly 5–15%) and strict service SLAs, can push for prioritized delivery schedules, and influence feature roadmaps through bundled orders; concentration of large fleet accounts increases leverage, while dedicated account teams and customized support reduce churn.

- Volume discounts: 5–15%

- Service SLAs: prioritized repairs/logistics

- Delivery influence: schedule acceleration

- Mitigation: dedicated account support

Global reviews and social influence

- Online ratings: 87% of EV buyers influenced

- Negative sentiment: quick demand impact

- Transparency: pressures pricing/releases

- Community mgmt: stabilizes perception

OTA, services and battery-swap cut churn as price visibility delays purchases and compresses margins

Premium buyers demand cutting‑edge tech, rapid OTA and superior service, raising churn when value slips; NIO offsets with OTA, services and BaaS. Price visibility and promo timing push buyers to delay purchases, compressing margins; fleet buyers extract 5–15% discounts. Battery‑swap network (1,600+ stations) and subscriptions raise switching costs; online reviews influence ~87% of EV purchases.

| Metric | Value |

|---|---|

| Swap stations | 1,600+ |

| Fleet discounts | 5–15% |

| Online influence | 87% |

Full Version Awaits

NIO Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of NIO you’ll receive immediately after purchase—no placeholders or samples. The document is the full, professionally formatted analysis, ready for download and use the moment you buy. What you see here is precisely what will be delivered to you after payment.