Nippon Paint Holdings Porter's Five Forces Analysis

From Overview to Strategy Blueprint

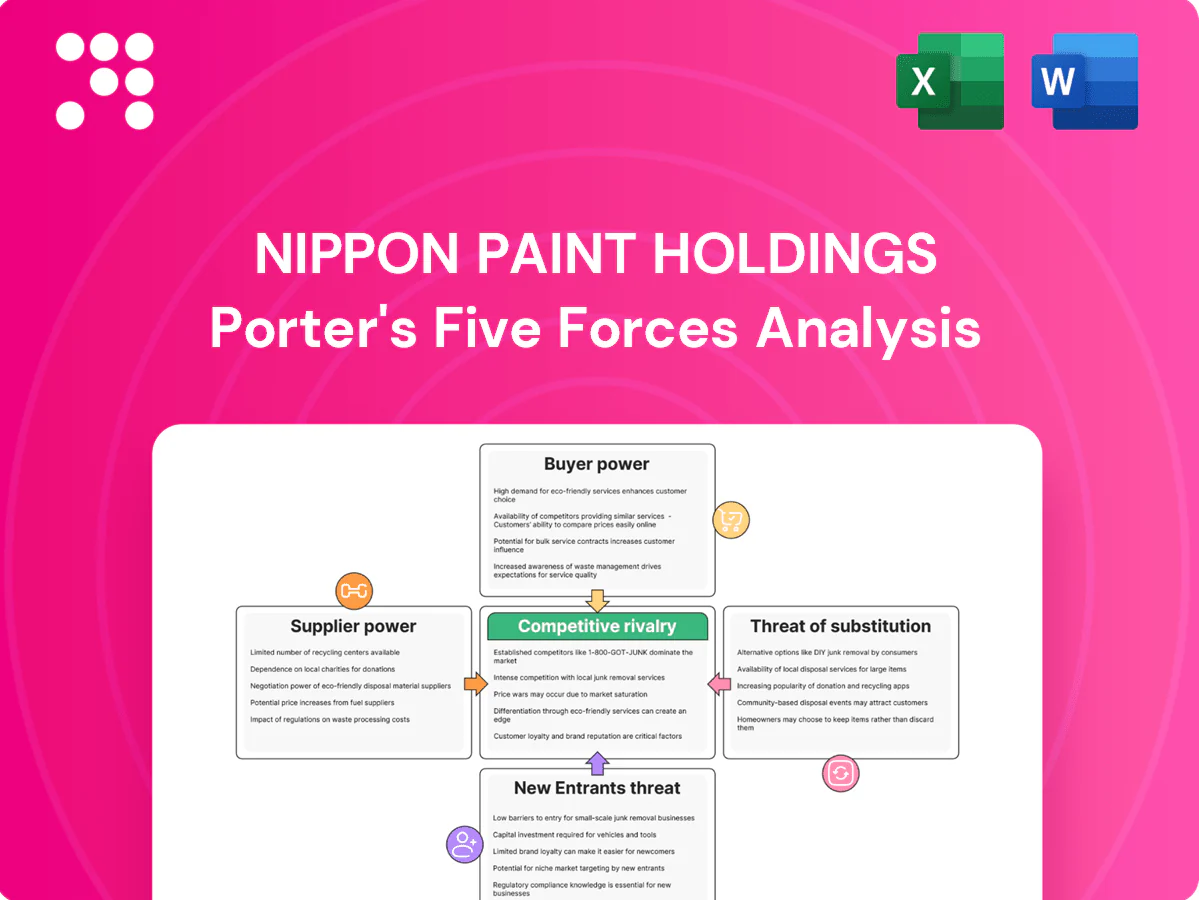

Nippon Paint Holdings faces moderate rivalry from established regional paintmakers, rising buyer price sensitivity, and manageable supplier power due to diversified raw material sources. Barriers to entry are medium—brand and distribution matter—but substitutes and regulatory shifts add pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Paint Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated key inputs (TiO2, resins, solvents)

Core paint inputs like titanium dioxide, specialty resins and solvents are supplied by a relatively concentrated set of global chemical firms; in 2024 the top four TiO2 producers held roughly 60% of global capacity, boosting supplier leverage during tight markets. Nippon Paint mitigates exposure via multi-sourcing and long-term supply contracts. Nonetheless, commodity-cycle spikes still transmit pricing pressure to margins.

Switching costs moderate but qualification needed

Suppliers can be switched, yet reformulation, quality validation and REACH/TSCA compliance testing typically take months and can cost hundreds of thousands, creating practical stickiness in critical grades where consistency is paramount. Supplier performance on batch-to-batch consistency and regulatory standing further narrows options, notably after 2024 pigment and additive supply shocks. As a result, leverage is balanced rather than fully fungible.

Scale purchasing offsets input leverage

Nippon Paint’s global volume and category breadth, operating in 25+ countries as of 2024, supports favorable contract terms and raw-material hedging. Aggregated procurement and vendor-managed inventory programs cut stockout and working-capital risks. Regional sourcing hubs in Asia, Europe and the Americas enable local price arbitrage. Overall scale partially neutralizes upstream supplier pricing power.

Sustainability and specialty inputs add dependency

Low-VOC binders, bio-based resins and specialty additives are sourced from a narrow supplier base, with the global bio-based resin market estimated at about USD 8–10 billion in 2024, limiting switching options. Stricter ESG specs and ecolabels (procurement for green products rose ~20% in 2024) further constrain substitutes. Co-development partnerships deepen technical ties but increase supplier leverage over pricing and lead times.

- Fewer qualified suppliers

- ESG/ecolabels limit substitution

- Co-development raises dependency

- Higher supplier influence on price & lead time

Logistics and energy volatility pass-through

Freight rates, Brent-driven energy costs (Brent averaged about 84 USD/bbl in 2024) and force majeure events constrict chemical input availability; suppliers commonly insert pass-through clauses during spikes. Nippon Paint mitigates with regional plants and higher inventories but cannot fully eliminate exposure, so supplier power transiently spikes during disruptions.

- 2024 Brent ~84 USD/bbl — raises production and transport costs

- Container freight normalization (~1,600 USD/40ft avg 2024) increases pass-through risk

- Regional plants + inventory = partial buffer; supplier power still rises in outages

TiO2 concentration, bio-resin stickiness and Brent spikes heighten pass-through risk

Core inputs like TiO2, resins and additives are concentrated (top‑4 TiO2 ~60% in 2024), giving suppliers intermittent pricing leverage; Nippon offsets via multi‑sourcing and long‑term contracts. Switching costs, compliance testing and co‑development create practical stickiness, especially for low‑VOC/bio resins. Scale, regional plants and procurement programs partly neutralize power but spikes (Brent USD 84/bbl, freight ~USD 1,600/40ft) raise pass‑through risk.

| Metric | 2024 |

|---|---|

| TiO2 top‑4 share | ~60% |

| Bio‑resin market | USD 9B |

| Brent avg | USD 84/bbl |

| Freight 40ft | ~USD 1,600 |

| Operating countries | 25+ |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Nippon Paint Holdings; analyzes supplier power, buyer bargaining, rivalry intensity, threat of substitutes, and barriers deterring new entrants, highlighting disruptive forces and strategic implications for pricing, profitability, and market share.

One-sheet Porter’s Five Forces for Nippon Paint Holdings—quickly visualise competitive pressure with a radar chart and customizable force levels to evaluate supply-chain risks, buyer power, new entrants and substitutes for faster, board-ready decisions.

Customers Bargaining Power

Diverse mix: OEMs, contractors, distributors, DIY

Automotive and industrial OEMs buy large volumes under negotiated contracts and exert strong price pressure, especially as the global coatings market reached about USD 166 billion in 2024. Trade distributors and big-box retailers push rebates and shelf-support deals that compress margins. Professional applicators prioritize performance and service, reducing pure price sensitivity. DIY buyers are fragmented and display high brand sensitivity.

Specification and brand reduce switching

Project specifications, color libraries and approved-vendor lists anchor buyer relationships and make mid-project brand changes costly; warranty and multi-year performance histories further discourage switches. Nippon’s branded tinting systems and technical support increase stickiness; as of 2024 Nippon Paint is a top-five global coatings firm, which lowers buyer bargaining power in mission-critical uses.

Price transparency fosters negotiations

Price transparency in decorative commodity lines—visible across retail and online channels—lets buyers push for lower prices; in 2024 consumer searches and comparison shopping rose markedly, intensifying use of promotions and competitor quotes. Digital marketplaces increase comparability and channel-driven discounts, while Nippon counters through differentiated formulations, proprietary color-matching tech and loyalty programs to protect margins and repeat purchase rates.

Service, logistics, and credit terms as levers

- Negotiation levers: deliveries, consignment, credit

- Value-adds: technical support, on-site training

- Effect: bundling raises switching pain

- Risk: poor execution increases buyer power

ESG and compliance demands

Enterprise buyers increasingly demand low-VOC formulations, EHS documentation and material traceability, narrowing acceptable product sets and reducing buyer alternatives while raising compliance-driven costs that buyers seek to share or pass on.

- Compliance narrows choices

- Higher costs shifted to suppliers/buyers

- Power varies with uniqueness of compliant product

Buyers squeeze prices as DIY transparency grows; scale and service offset leverage

Buyers exert moderate power: large OEMs and distributors negotiate hard on price, delivery and credit while professional applicators prioritize service, raising switching costs. DIY and retail channels increase price transparency across a ~USD 166 billion coatings market (2024). Nippon Paint, a top-five global firm with ¥1.05 trillion revenue (FY2023), uses scale and technical support to blunt buyer leverage.

| Metric | 2023/2024 |

|---|---|

| Global coatings market | USD 166bn (2024) |

| Nippon Paint revenue | ¥1.05tn (FY2023) |

Same Document Delivered

Nippon Paint Holdings Porter's Five Forces Analysis

This preview displays the full Porter’s Five Forces analysis for Nippon Paint Holdings—the exact, professionally formatted document you will receive upon purchase. It covers competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications. No samples, no placeholders; buy and download this same file instantly for immediate use.

From Overview to Strategy Blueprint

Nippon Paint Holdings faces moderate rivalry from established regional paintmakers, rising buyer price sensitivity, and manageable supplier power due to diversified raw material sources. Barriers to entry are medium—brand and distribution matter—but substitutes and regulatory shifts add pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Paint Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated key inputs (TiO2, resins, solvents)

Core paint inputs like titanium dioxide, specialty resins and solvents are supplied by a relatively concentrated set of global chemical firms; in 2024 the top four TiO2 producers held roughly 60% of global capacity, boosting supplier leverage during tight markets. Nippon Paint mitigates exposure via multi-sourcing and long-term supply contracts. Nonetheless, commodity-cycle spikes still transmit pricing pressure to margins.

Switching costs moderate but qualification needed

Suppliers can be switched, yet reformulation, quality validation and REACH/TSCA compliance testing typically take months and can cost hundreds of thousands, creating practical stickiness in critical grades where consistency is paramount. Supplier performance on batch-to-batch consistency and regulatory standing further narrows options, notably after 2024 pigment and additive supply shocks. As a result, leverage is balanced rather than fully fungible.

Scale purchasing offsets input leverage

Nippon Paint’s global volume and category breadth, operating in 25+ countries as of 2024, supports favorable contract terms and raw-material hedging. Aggregated procurement and vendor-managed inventory programs cut stockout and working-capital risks. Regional sourcing hubs in Asia, Europe and the Americas enable local price arbitrage. Overall scale partially neutralizes upstream supplier pricing power.

Sustainability and specialty inputs add dependency

Low-VOC binders, bio-based resins and specialty additives are sourced from a narrow supplier base, with the global bio-based resin market estimated at about USD 8–10 billion in 2024, limiting switching options. Stricter ESG specs and ecolabels (procurement for green products rose ~20% in 2024) further constrain substitutes. Co-development partnerships deepen technical ties but increase supplier leverage over pricing and lead times.

- Fewer qualified suppliers

- ESG/ecolabels limit substitution

- Co-development raises dependency

- Higher supplier influence on price & lead time

Logistics and energy volatility pass-through

Freight rates, Brent-driven energy costs (Brent averaged about 84 USD/bbl in 2024) and force majeure events constrict chemical input availability; suppliers commonly insert pass-through clauses during spikes. Nippon Paint mitigates with regional plants and higher inventories but cannot fully eliminate exposure, so supplier power transiently spikes during disruptions.

- 2024 Brent ~84 USD/bbl — raises production and transport costs

- Container freight normalization (~1,600 USD/40ft avg 2024) increases pass-through risk

- Regional plants + inventory = partial buffer; supplier power still rises in outages

TiO2 concentration, bio-resin stickiness and Brent spikes heighten pass-through risk

Core inputs like TiO2, resins and additives are concentrated (top‑4 TiO2 ~60% in 2024), giving suppliers intermittent pricing leverage; Nippon offsets via multi‑sourcing and long‑term contracts. Switching costs, compliance testing and co‑development create practical stickiness, especially for low‑VOC/bio resins. Scale, regional plants and procurement programs partly neutralize power but spikes (Brent USD 84/bbl, freight ~USD 1,600/40ft) raise pass‑through risk.

| Metric | 2024 |

|---|---|

| TiO2 top‑4 share | ~60% |

| Bio‑resin market | USD 9B |

| Brent avg | USD 84/bbl |

| Freight 40ft | ~USD 1,600 |

| Operating countries | 25+ |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Nippon Paint Holdings; analyzes supplier power, buyer bargaining, rivalry intensity, threat of substitutes, and barriers deterring new entrants, highlighting disruptive forces and strategic implications for pricing, profitability, and market share.

One-sheet Porter’s Five Forces for Nippon Paint Holdings—quickly visualise competitive pressure with a radar chart and customizable force levels to evaluate supply-chain risks, buyer power, new entrants and substitutes for faster, board-ready decisions.

Customers Bargaining Power

Diverse mix: OEMs, contractors, distributors, DIY

Automotive and industrial OEMs buy large volumes under negotiated contracts and exert strong price pressure, especially as the global coatings market reached about USD 166 billion in 2024. Trade distributors and big-box retailers push rebates and shelf-support deals that compress margins. Professional applicators prioritize performance and service, reducing pure price sensitivity. DIY buyers are fragmented and display high brand sensitivity.

Specification and brand reduce switching

Project specifications, color libraries and approved-vendor lists anchor buyer relationships and make mid-project brand changes costly; warranty and multi-year performance histories further discourage switches. Nippon’s branded tinting systems and technical support increase stickiness; as of 2024 Nippon Paint is a top-five global coatings firm, which lowers buyer bargaining power in mission-critical uses.

Price transparency fosters negotiations

Price transparency in decorative commodity lines—visible across retail and online channels—lets buyers push for lower prices; in 2024 consumer searches and comparison shopping rose markedly, intensifying use of promotions and competitor quotes. Digital marketplaces increase comparability and channel-driven discounts, while Nippon counters through differentiated formulations, proprietary color-matching tech and loyalty programs to protect margins and repeat purchase rates.

Service, logistics, and credit terms as levers

- Negotiation levers: deliveries, consignment, credit

- Value-adds: technical support, on-site training

- Effect: bundling raises switching pain

- Risk: poor execution increases buyer power

ESG and compliance demands

Enterprise buyers increasingly demand low-VOC formulations, EHS documentation and material traceability, narrowing acceptable product sets and reducing buyer alternatives while raising compliance-driven costs that buyers seek to share or pass on.

- Compliance narrows choices

- Higher costs shifted to suppliers/buyers

- Power varies with uniqueness of compliant product

Buyers squeeze prices as DIY transparency grows; scale and service offset leverage

Buyers exert moderate power: large OEMs and distributors negotiate hard on price, delivery and credit while professional applicators prioritize service, raising switching costs. DIY and retail channels increase price transparency across a ~USD 166 billion coatings market (2024). Nippon Paint, a top-five global firm with ¥1.05 trillion revenue (FY2023), uses scale and technical support to blunt buyer leverage.

| Metric | 2023/2024 |

|---|---|

| Global coatings market | USD 166bn (2024) |

| Nippon Paint revenue | ¥1.05tn (FY2023) |

Same Document Delivered

Nippon Paint Holdings Porter's Five Forces Analysis

This preview displays the full Porter’s Five Forces analysis for Nippon Paint Holdings—the exact, professionally formatted document you will receive upon purchase. It covers competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications. No samples, no placeholders; buy and download this same file instantly for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Nippon Paint Holdings faces moderate rivalry from established regional paintmakers, rising buyer price sensitivity, and manageable supplier power due to diversified raw material sources. Barriers to entry are medium—brand and distribution matter—but substitutes and regulatory shifts add pressure. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Paint Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated key inputs (TiO2, resins, solvents)

Core paint inputs like titanium dioxide, specialty resins and solvents are supplied by a relatively concentrated set of global chemical firms; in 2024 the top four TiO2 producers held roughly 60% of global capacity, boosting supplier leverage during tight markets. Nippon Paint mitigates exposure via multi-sourcing and long-term supply contracts. Nonetheless, commodity-cycle spikes still transmit pricing pressure to margins.

Switching costs moderate but qualification needed

Suppliers can be switched, yet reformulation, quality validation and REACH/TSCA compliance testing typically take months and can cost hundreds of thousands, creating practical stickiness in critical grades where consistency is paramount. Supplier performance on batch-to-batch consistency and regulatory standing further narrows options, notably after 2024 pigment and additive supply shocks. As a result, leverage is balanced rather than fully fungible.

Scale purchasing offsets input leverage

Nippon Paint’s global volume and category breadth, operating in 25+ countries as of 2024, supports favorable contract terms and raw-material hedging. Aggregated procurement and vendor-managed inventory programs cut stockout and working-capital risks. Regional sourcing hubs in Asia, Europe and the Americas enable local price arbitrage. Overall scale partially neutralizes upstream supplier pricing power.

Sustainability and specialty inputs add dependency

Low-VOC binders, bio-based resins and specialty additives are sourced from a narrow supplier base, with the global bio-based resin market estimated at about USD 8–10 billion in 2024, limiting switching options. Stricter ESG specs and ecolabels (procurement for green products rose ~20% in 2024) further constrain substitutes. Co-development partnerships deepen technical ties but increase supplier leverage over pricing and lead times.

- Fewer qualified suppliers

- ESG/ecolabels limit substitution

- Co-development raises dependency

- Higher supplier influence on price & lead time

Logistics and energy volatility pass-through

Freight rates, Brent-driven energy costs (Brent averaged about 84 USD/bbl in 2024) and force majeure events constrict chemical input availability; suppliers commonly insert pass-through clauses during spikes. Nippon Paint mitigates with regional plants and higher inventories but cannot fully eliminate exposure, so supplier power transiently spikes during disruptions.

- 2024 Brent ~84 USD/bbl — raises production and transport costs

- Container freight normalization (~1,600 USD/40ft avg 2024) increases pass-through risk

- Regional plants + inventory = partial buffer; supplier power still rises in outages

TiO2 concentration, bio-resin stickiness and Brent spikes heighten pass-through risk

Core inputs like TiO2, resins and additives are concentrated (top‑4 TiO2 ~60% in 2024), giving suppliers intermittent pricing leverage; Nippon offsets via multi‑sourcing and long‑term contracts. Switching costs, compliance testing and co‑development create practical stickiness, especially for low‑VOC/bio resins. Scale, regional plants and procurement programs partly neutralize power but spikes (Brent USD 84/bbl, freight ~USD 1,600/40ft) raise pass‑through risk.

| Metric | 2024 |

|---|---|

| TiO2 top‑4 share | ~60% |

| Bio‑resin market | USD 9B |

| Brent avg | USD 84/bbl |

| Freight 40ft | ~USD 1,600 |

| Operating countries | 25+ |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Nippon Paint Holdings; analyzes supplier power, buyer bargaining, rivalry intensity, threat of substitutes, and barriers deterring new entrants, highlighting disruptive forces and strategic implications for pricing, profitability, and market share.

One-sheet Porter’s Five Forces for Nippon Paint Holdings—quickly visualise competitive pressure with a radar chart and customizable force levels to evaluate supply-chain risks, buyer power, new entrants and substitutes for faster, board-ready decisions.

Customers Bargaining Power

Diverse mix: OEMs, contractors, distributors, DIY

Automotive and industrial OEMs buy large volumes under negotiated contracts and exert strong price pressure, especially as the global coatings market reached about USD 166 billion in 2024. Trade distributors and big-box retailers push rebates and shelf-support deals that compress margins. Professional applicators prioritize performance and service, reducing pure price sensitivity. DIY buyers are fragmented and display high brand sensitivity.

Specification and brand reduce switching

Project specifications, color libraries and approved-vendor lists anchor buyer relationships and make mid-project brand changes costly; warranty and multi-year performance histories further discourage switches. Nippon’s branded tinting systems and technical support increase stickiness; as of 2024 Nippon Paint is a top-five global coatings firm, which lowers buyer bargaining power in mission-critical uses.

Price transparency fosters negotiations

Price transparency in decorative commodity lines—visible across retail and online channels—lets buyers push for lower prices; in 2024 consumer searches and comparison shopping rose markedly, intensifying use of promotions and competitor quotes. Digital marketplaces increase comparability and channel-driven discounts, while Nippon counters through differentiated formulations, proprietary color-matching tech and loyalty programs to protect margins and repeat purchase rates.

Service, logistics, and credit terms as levers

- Negotiation levers: deliveries, consignment, credit

- Value-adds: technical support, on-site training

- Effect: bundling raises switching pain

- Risk: poor execution increases buyer power

ESG and compliance demands

Enterprise buyers increasingly demand low-VOC formulations, EHS documentation and material traceability, narrowing acceptable product sets and reducing buyer alternatives while raising compliance-driven costs that buyers seek to share or pass on.

- Compliance narrows choices

- Higher costs shifted to suppliers/buyers

- Power varies with uniqueness of compliant product

Buyers squeeze prices as DIY transparency grows; scale and service offset leverage

Buyers exert moderate power: large OEMs and distributors negotiate hard on price, delivery and credit while professional applicators prioritize service, raising switching costs. DIY and retail channels increase price transparency across a ~USD 166 billion coatings market (2024). Nippon Paint, a top-five global firm with ¥1.05 trillion revenue (FY2023), uses scale and technical support to blunt buyer leverage.

| Metric | 2023/2024 |

|---|---|

| Global coatings market | USD 166bn (2024) |

| Nippon Paint revenue | ¥1.05tn (FY2023) |

Same Document Delivered

Nippon Paint Holdings Porter's Five Forces Analysis

This preview displays the full Porter’s Five Forces analysis for Nippon Paint Holdings—the exact, professionally formatted document you will receive upon purchase. It covers competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications. No samples, no placeholders; buy and download this same file instantly for immediate use.