Nissha Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

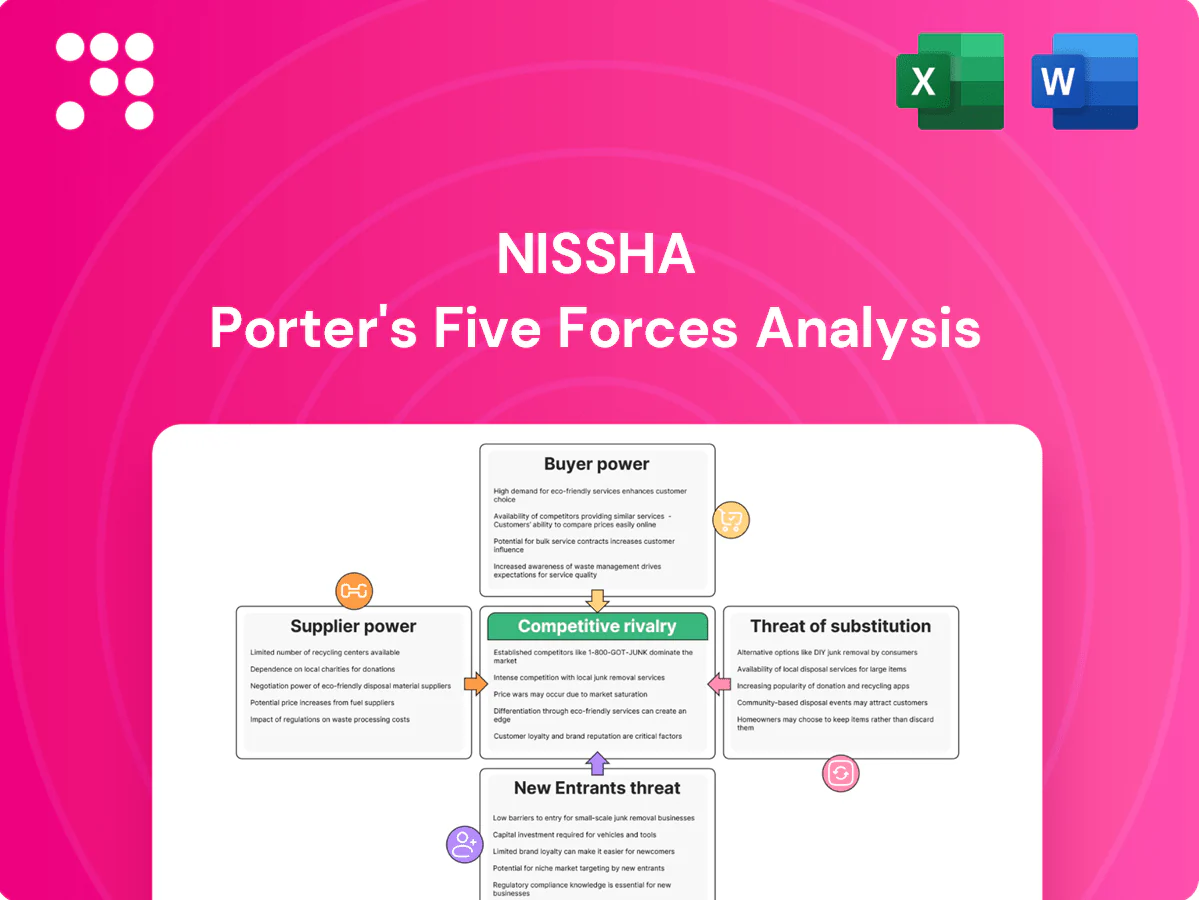

Nissha’s Porter's Five Forces snapshot highlights supplier leverage, moderate buyer power, niche entry barriers, competitive rivalry, and evolving substitute risks across its precision components and printed electronics segments. This concise view reveals where strategic pressure points lie for margin protection and growth. Ready for deeper, data-driven force ratings and visuals? Unlock the full Porter's Five Forces Analysis for Nissha to inform investment and strategy.

Suppliers Bargaining Power

Specialty materials concentration

Many of Nissha’s inputs—specialty films, inks, resins, and conductive pastes—are supplied by a small set of qualified global vendors, concentrating supply and raising switching costs. This gives suppliers leverage on pricing and lead times, with automotive and medical qualification cycles typically taking 12–24 months and further locking in sources. Nissha mitigates risk through multi-sourcing strategies and proprietary in-house formulation know-how.

Equipment and tooling dependency

Precision coating, printing and lamination lines plus molds and dies come from a concentrated vendor base; in 2024 fewer than 20 global specialists supply high-end systems, giving suppliers leverage. Custom tooling with typical lead times of 12–24 weeks creates bargaining power during expansions or changeovers. Limited service and spare-parts availability can cut uptime and margins. Framework agreements and preventive maintenance reduce that supplier power.

Commodity input volatility

Petrochemical-derived substrates and adhesives expose Nissha to oil and naphtha swings, with Brent crude averaging about $86 per barrel in 2024, driving feedstock cost variability. Although many commodity suppliers exist, volatility allows vendors to exert pass-through pricing pressure, compressing margins. Hedging and formula pricing have partially stabilized input costs for manufacturers. Scale purchasing and inventory buffering further reduce short-term shock exposure.

Technology co-development

Technology co-development for advanced films and conductive materials creates joint IP and process recipes that deepen supplier dependence, elevating supplier power while raising competitor entry barriers; clear IP terms and dual-qualified specs are essential to limit overreliance.

- Co-development increases supplier leverage

- Joint IP deepens dependence

- Raises entry barriers

- Clear IP and dual-specs reduce risk

Regional supply chain risks

Cross-border logistics for chemicals and films face regulatory, ESG and geopolitical constraints that increase routing complexity and costs. Export controls and REACH compliance shrink the qualified supplier base; ECHA lists ≈22,000 REACH-registered substances (2024). Asian supplier clusters provide scale and lead-time advantages, while localizing critical inputs reduces regional risk exposure.

- Regulatory squeeze: REACH ≈22,000 substances (2024)

- Export controls narrow supplier pool

- Localization lowers regional supply risk

Supplier concentration lifts pricing and lead-time risk; tooling 12–24w, Brent $86/bbl

Suppliers of specialty films, inks and equipment are concentrated, raising pricing and lead-time leverage; tooling lead times 12–24 weeks, automotive/medical quals 12–24 months. Brent crude averaged $86/bbl in 2024, pressuring feedstock costs. Co-development/JV IP deepens dependence; dual-sourcing and hedging mitigate risk.

| Metric | Value |

|---|---|

| Tooling lead time | 12–24 weeks |

| Qualification time | 12–24 months |

| Brent 2024 | $86/bbl |

| REACH substances | ≈22,000 |

What is included in the product

Concise Porter's Five Forces analysis tailored to Nissha, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with strategic insights on disruptive threats and pricing pressures to guide investor and management decisions.

One-sheet Porter's Five Forces for Nissha that pinpoints supplier/customer pressure, rivalry, and entry/substitute threats—ideal for fast strategic fixes and boardroom decisions. Clean, customizable layout ready to drop into decks or evolve with new market data.

Customers Bargaining Power

Large OEM concentration

Automotive and consumer-electronics OEMs and Tier-1s are few and powerful: the top global automakers account for over 50% of vehicle output and the five largest consumer device OEMs hold roughly 70% share (2024), concentrating purchase power. Their scale, annual sourcing cycles and target-cost models drive persistent pricing pressure and squeeze supplier margins. Nissha’s design-win dependence amplifies buyer leverage over time. To mitigate, Nissha is diversifying into medical and industrial segments.

Qualification and specs lock-in

Stringent design and quality qualifications such as IATF 16949 and ISO 13485 are ubiquitous in 2024 supply chains, creating high switching costs and slow change once components are embedded, which moderates buyer power on continuity. OEMs continue to demand 3–5% annual cost-downs, keeping pressure on suppliers despite lock-in. Offering measurable performance upgrades that cut lifecycle costs enables value-based pricing and offsets cost-down demands.

Customization vs standardization

Bespoke decorative films and touch modules reduce comparability and limit bidding because highly tailored specs raise switching costs and make direct price comparisons difficult. Where specs are standardized, buyers can pit suppliers to lower prices, increasing customer bargaining power. Nissha’s design assistance and prototyping enhance stickiness by embedding design IP and shortening development cycles. Modular platforms let Nissha balance customization with scale, preserving margins.

Demand cyclicality

Consumer electronics volumes are highly volatile—smartphone shipments fell about 11% in 2023 (IDC), letting buyers press for price concessions in downturns. Automotive platform cycles (global light-vehicle production ~80.8M in 2023, S&P Global) reset supplier terms periodically. Volume swings compress capacity utilization and margins, while Nissha’s diversified end-markets help smooth bargaining dynamics.

- Smartphones down 11% in 2023 (IDC)

- Light vehicles ~80.8M in 2023 (S&P Global)

- Downturns enable renegotiation

- Diversification reduces customer leverage

Medical procurement dynamics

- GPO penetration: >90% (US, 2024)

- Switching costs: sterility/biocompatibility drive premium

- Value drivers: supply assurance, regulatory compliance

- Trend: outcome-based procurement reduces unit price emphasis

OEM buyers (>50% auto) squeeze suppliers; certification limits switching

Concentrated OEM buyers (>50% auto, top5 CE ~70% 2024) exert strong price pressure, amplified by Nissha’s design-win dependence. Certification and bespoke specs raise switching costs, moderating leverage. Volume cyclicality (smartphones -11% 2023; LVs 80.8M 2023) enables renegotiation; GPOs >90% US hospitals shift focus to total cost of care.

| Metric | Value |

|---|---|

| Top OEM share | >50% auto |

| Top5 CE share (2024) | ~70% |

| Smartphones (2023) | -11% |

| Light vehicles (2023) | 80.8M |

| GPO penetration (US,2024) | >90% |

Preview the Actual Deliverable

Nissha Porter's Five Forces Analysis

This Nissha Porter's Five Forces analysis provides a concise evaluation of supplier power, buyer power, threat of substitutes, threat of new entrants, and competitive rivalry specific to Nissha’s markets and technologies, with implications for pricing, margins, and strategic positioning. The previewed file is the actual, fully formatted document you will receive immediately after purchase—no placeholders or samples. It’s ready to download and use for decision-making or presentation.

A Must-Have Tool for Decision-Makers

Nissha’s Porter's Five Forces snapshot highlights supplier leverage, moderate buyer power, niche entry barriers, competitive rivalry, and evolving substitute risks across its precision components and printed electronics segments. This concise view reveals where strategic pressure points lie for margin protection and growth. Ready for deeper, data-driven force ratings and visuals? Unlock the full Porter's Five Forces Analysis for Nissha to inform investment and strategy.

Suppliers Bargaining Power

Specialty materials concentration

Many of Nissha’s inputs—specialty films, inks, resins, and conductive pastes—are supplied by a small set of qualified global vendors, concentrating supply and raising switching costs. This gives suppliers leverage on pricing and lead times, with automotive and medical qualification cycles typically taking 12–24 months and further locking in sources. Nissha mitigates risk through multi-sourcing strategies and proprietary in-house formulation know-how.

Equipment and tooling dependency

Precision coating, printing and lamination lines plus molds and dies come from a concentrated vendor base; in 2024 fewer than 20 global specialists supply high-end systems, giving suppliers leverage. Custom tooling with typical lead times of 12–24 weeks creates bargaining power during expansions or changeovers. Limited service and spare-parts availability can cut uptime and margins. Framework agreements and preventive maintenance reduce that supplier power.

Commodity input volatility

Petrochemical-derived substrates and adhesives expose Nissha to oil and naphtha swings, with Brent crude averaging about $86 per barrel in 2024, driving feedstock cost variability. Although many commodity suppliers exist, volatility allows vendors to exert pass-through pricing pressure, compressing margins. Hedging and formula pricing have partially stabilized input costs for manufacturers. Scale purchasing and inventory buffering further reduce short-term shock exposure.

Technology co-development

Technology co-development for advanced films and conductive materials creates joint IP and process recipes that deepen supplier dependence, elevating supplier power while raising competitor entry barriers; clear IP terms and dual-qualified specs are essential to limit overreliance.

- Co-development increases supplier leverage

- Joint IP deepens dependence

- Raises entry barriers

- Clear IP and dual-specs reduce risk

Regional supply chain risks

Cross-border logistics for chemicals and films face regulatory, ESG and geopolitical constraints that increase routing complexity and costs. Export controls and REACH compliance shrink the qualified supplier base; ECHA lists ≈22,000 REACH-registered substances (2024). Asian supplier clusters provide scale and lead-time advantages, while localizing critical inputs reduces regional risk exposure.

- Regulatory squeeze: REACH ≈22,000 substances (2024)

- Export controls narrow supplier pool

- Localization lowers regional supply risk

Supplier concentration lifts pricing and lead-time risk; tooling 12–24w, Brent $86/bbl

Suppliers of specialty films, inks and equipment are concentrated, raising pricing and lead-time leverage; tooling lead times 12–24 weeks, automotive/medical quals 12–24 months. Brent crude averaged $86/bbl in 2024, pressuring feedstock costs. Co-development/JV IP deepens dependence; dual-sourcing and hedging mitigate risk.

| Metric | Value |

|---|---|

| Tooling lead time | 12–24 weeks |

| Qualification time | 12–24 months |

| Brent 2024 | $86/bbl |

| REACH substances | ≈22,000 |

What is included in the product

Concise Porter's Five Forces analysis tailored to Nissha, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with strategic insights on disruptive threats and pricing pressures to guide investor and management decisions.

One-sheet Porter's Five Forces for Nissha that pinpoints supplier/customer pressure, rivalry, and entry/substitute threats—ideal for fast strategic fixes and boardroom decisions. Clean, customizable layout ready to drop into decks or evolve with new market data.

Customers Bargaining Power

Large OEM concentration

Automotive and consumer-electronics OEMs and Tier-1s are few and powerful: the top global automakers account for over 50% of vehicle output and the five largest consumer device OEMs hold roughly 70% share (2024), concentrating purchase power. Their scale, annual sourcing cycles and target-cost models drive persistent pricing pressure and squeeze supplier margins. Nissha’s design-win dependence amplifies buyer leverage over time. To mitigate, Nissha is diversifying into medical and industrial segments.

Qualification and specs lock-in

Stringent design and quality qualifications such as IATF 16949 and ISO 13485 are ubiquitous in 2024 supply chains, creating high switching costs and slow change once components are embedded, which moderates buyer power on continuity. OEMs continue to demand 3–5% annual cost-downs, keeping pressure on suppliers despite lock-in. Offering measurable performance upgrades that cut lifecycle costs enables value-based pricing and offsets cost-down demands.

Customization vs standardization

Bespoke decorative films and touch modules reduce comparability and limit bidding because highly tailored specs raise switching costs and make direct price comparisons difficult. Where specs are standardized, buyers can pit suppliers to lower prices, increasing customer bargaining power. Nissha’s design assistance and prototyping enhance stickiness by embedding design IP and shortening development cycles. Modular platforms let Nissha balance customization with scale, preserving margins.

Demand cyclicality

Consumer electronics volumes are highly volatile—smartphone shipments fell about 11% in 2023 (IDC), letting buyers press for price concessions in downturns. Automotive platform cycles (global light-vehicle production ~80.8M in 2023, S&P Global) reset supplier terms periodically. Volume swings compress capacity utilization and margins, while Nissha’s diversified end-markets help smooth bargaining dynamics.

- Smartphones down 11% in 2023 (IDC)

- Light vehicles ~80.8M in 2023 (S&P Global)

- Downturns enable renegotiation

- Diversification reduces customer leverage

Medical procurement dynamics

- GPO penetration: >90% (US, 2024)

- Switching costs: sterility/biocompatibility drive premium

- Value drivers: supply assurance, regulatory compliance

- Trend: outcome-based procurement reduces unit price emphasis

OEM buyers (>50% auto) squeeze suppliers; certification limits switching

Concentrated OEM buyers (>50% auto, top5 CE ~70% 2024) exert strong price pressure, amplified by Nissha’s design-win dependence. Certification and bespoke specs raise switching costs, moderating leverage. Volume cyclicality (smartphones -11% 2023; LVs 80.8M 2023) enables renegotiation; GPOs >90% US hospitals shift focus to total cost of care.

| Metric | Value |

|---|---|

| Top OEM share | >50% auto |

| Top5 CE share (2024) | ~70% |

| Smartphones (2023) | -11% |

| Light vehicles (2023) | 80.8M |

| GPO penetration (US,2024) | >90% |

Preview the Actual Deliverable

Nissha Porter's Five Forces Analysis

This Nissha Porter's Five Forces analysis provides a concise evaluation of supplier power, buyer power, threat of substitutes, threat of new entrants, and competitive rivalry specific to Nissha’s markets and technologies, with implications for pricing, margins, and strategic positioning. The previewed file is the actual, fully formatted document you will receive immediately after purchase—no placeholders or samples. It’s ready to download and use for decision-making or presentation.

Description

A Must-Have Tool for Decision-Makers

Nissha’s Porter's Five Forces snapshot highlights supplier leverage, moderate buyer power, niche entry barriers, competitive rivalry, and evolving substitute risks across its precision components and printed electronics segments. This concise view reveals where strategic pressure points lie for margin protection and growth. Ready for deeper, data-driven force ratings and visuals? Unlock the full Porter's Five Forces Analysis for Nissha to inform investment and strategy.

Suppliers Bargaining Power

Specialty materials concentration

Many of Nissha’s inputs—specialty films, inks, resins, and conductive pastes—are supplied by a small set of qualified global vendors, concentrating supply and raising switching costs. This gives suppliers leverage on pricing and lead times, with automotive and medical qualification cycles typically taking 12–24 months and further locking in sources. Nissha mitigates risk through multi-sourcing strategies and proprietary in-house formulation know-how.

Equipment and tooling dependency

Precision coating, printing and lamination lines plus molds and dies come from a concentrated vendor base; in 2024 fewer than 20 global specialists supply high-end systems, giving suppliers leverage. Custom tooling with typical lead times of 12–24 weeks creates bargaining power during expansions or changeovers. Limited service and spare-parts availability can cut uptime and margins. Framework agreements and preventive maintenance reduce that supplier power.

Commodity input volatility

Petrochemical-derived substrates and adhesives expose Nissha to oil and naphtha swings, with Brent crude averaging about $86 per barrel in 2024, driving feedstock cost variability. Although many commodity suppliers exist, volatility allows vendors to exert pass-through pricing pressure, compressing margins. Hedging and formula pricing have partially stabilized input costs for manufacturers. Scale purchasing and inventory buffering further reduce short-term shock exposure.

Technology co-development

Technology co-development for advanced films and conductive materials creates joint IP and process recipes that deepen supplier dependence, elevating supplier power while raising competitor entry barriers; clear IP terms and dual-qualified specs are essential to limit overreliance.

- Co-development increases supplier leverage

- Joint IP deepens dependence

- Raises entry barriers

- Clear IP and dual-specs reduce risk

Regional supply chain risks

Cross-border logistics for chemicals and films face regulatory, ESG and geopolitical constraints that increase routing complexity and costs. Export controls and REACH compliance shrink the qualified supplier base; ECHA lists ≈22,000 REACH-registered substances (2024). Asian supplier clusters provide scale and lead-time advantages, while localizing critical inputs reduces regional risk exposure.

- Regulatory squeeze: REACH ≈22,000 substances (2024)

- Export controls narrow supplier pool

- Localization lowers regional supply risk

Supplier concentration lifts pricing and lead-time risk; tooling 12–24w, Brent $86/bbl

Suppliers of specialty films, inks and equipment are concentrated, raising pricing and lead-time leverage; tooling lead times 12–24 weeks, automotive/medical quals 12–24 months. Brent crude averaged $86/bbl in 2024, pressuring feedstock costs. Co-development/JV IP deepens dependence; dual-sourcing and hedging mitigate risk.

| Metric | Value |

|---|---|

| Tooling lead time | 12–24 weeks |

| Qualification time | 12–24 months |

| Brent 2024 | $86/bbl |

| REACH substances | ≈22,000 |

What is included in the product

Concise Porter's Five Forces analysis tailored to Nissha, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with strategic insights on disruptive threats and pricing pressures to guide investor and management decisions.

One-sheet Porter's Five Forces for Nissha that pinpoints supplier/customer pressure, rivalry, and entry/substitute threats—ideal for fast strategic fixes and boardroom decisions. Clean, customizable layout ready to drop into decks or evolve with new market data.

Customers Bargaining Power

Large OEM concentration

Automotive and consumer-electronics OEMs and Tier-1s are few and powerful: the top global automakers account for over 50% of vehicle output and the five largest consumer device OEMs hold roughly 70% share (2024), concentrating purchase power. Their scale, annual sourcing cycles and target-cost models drive persistent pricing pressure and squeeze supplier margins. Nissha’s design-win dependence amplifies buyer leverage over time. To mitigate, Nissha is diversifying into medical and industrial segments.

Qualification and specs lock-in

Stringent design and quality qualifications such as IATF 16949 and ISO 13485 are ubiquitous in 2024 supply chains, creating high switching costs and slow change once components are embedded, which moderates buyer power on continuity. OEMs continue to demand 3–5% annual cost-downs, keeping pressure on suppliers despite lock-in. Offering measurable performance upgrades that cut lifecycle costs enables value-based pricing and offsets cost-down demands.

Customization vs standardization

Bespoke decorative films and touch modules reduce comparability and limit bidding because highly tailored specs raise switching costs and make direct price comparisons difficult. Where specs are standardized, buyers can pit suppliers to lower prices, increasing customer bargaining power. Nissha’s design assistance and prototyping enhance stickiness by embedding design IP and shortening development cycles. Modular platforms let Nissha balance customization with scale, preserving margins.

Demand cyclicality

Consumer electronics volumes are highly volatile—smartphone shipments fell about 11% in 2023 (IDC), letting buyers press for price concessions in downturns. Automotive platform cycles (global light-vehicle production ~80.8M in 2023, S&P Global) reset supplier terms periodically. Volume swings compress capacity utilization and margins, while Nissha’s diversified end-markets help smooth bargaining dynamics.

- Smartphones down 11% in 2023 (IDC)

- Light vehicles ~80.8M in 2023 (S&P Global)

- Downturns enable renegotiation

- Diversification reduces customer leverage

Medical procurement dynamics

- GPO penetration: >90% (US, 2024)

- Switching costs: sterility/biocompatibility drive premium

- Value drivers: supply assurance, regulatory compliance

- Trend: outcome-based procurement reduces unit price emphasis

OEM buyers (>50% auto) squeeze suppliers; certification limits switching

Concentrated OEM buyers (>50% auto, top5 CE ~70% 2024) exert strong price pressure, amplified by Nissha’s design-win dependence. Certification and bespoke specs raise switching costs, moderating leverage. Volume cyclicality (smartphones -11% 2023; LVs 80.8M 2023) enables renegotiation; GPOs >90% US hospitals shift focus to total cost of care.

| Metric | Value |

|---|---|

| Top OEM share | >50% auto |

| Top5 CE share (2024) | ~70% |

| Smartphones (2023) | -11% |

| Light vehicles (2023) | 80.8M |

| GPO penetration (US,2024) | >90% |

Preview the Actual Deliverable

Nissha Porter's Five Forces Analysis

This Nissha Porter's Five Forces analysis provides a concise evaluation of supplier power, buyer power, threat of substitutes, threat of new entrants, and competitive rivalry specific to Nissha’s markets and technologies, with implications for pricing, margins, and strategic positioning. The previewed file is the actual, fully formatted document you will receive immediately after purchase—no placeholders or samples. It’s ready to download and use for decision-making or presentation.