Nissha SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Explore Nissha's strategic position with our concise SWOT: clear strengths in precision printing and diversified customers, emerging risks from supply chains and competition, and growth drivers in medical and electronics segments. Purchase the full SWOT for a research-backed, editable Word + Excel package with strategic recommendations to inform investments and planning.

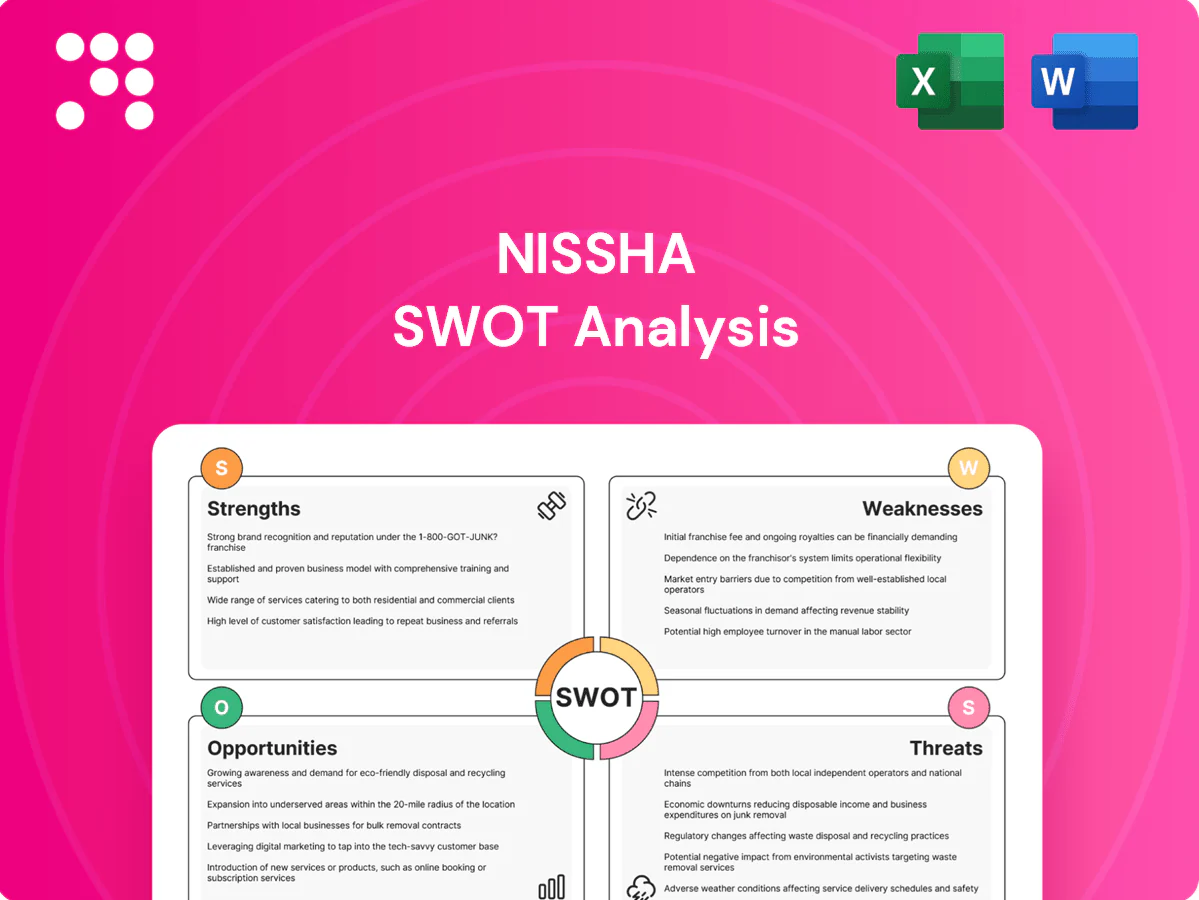

Strengths

Deep printing–coating–lamination know-how

Proprietary printing–coating–lamination processes give Nissha high-precision, scalable manufacturing that underpins performance surfaces and functional films with consistent quality. This technical base contributed to FY2024 consolidated revenue of about ¥160 billion and creates switching costs for OEMs dependent on tuned processes. The integrated stack shortens time-to-market for customized solutions, supporting repeat business and faster product launches.

Diversified across electronics, auto, and healthcare

Diversified exposure to electronics, automotive, and healthcare reduces single‑sector cyclicality, with decorative films, touch inputs and medical disposables showing offsetting demand patterns. Cross‑segment learning—materials know‑how from electronics applied to medical disposables and automotive coatings—fuels product innovation and faster time‑to‑market. Management can rebalance revenue toward more resilient categories as cycles shift.

Strong OEM co-development capabilities

Close engineering collaboration with global OEMs embeds Nissha in early design-in cycles, securing specification wins and extending product lifecycles. Early engagement improves forecast visibility and enables premium pricing for tailored parts. This tight integration raises replacement barriers and strengthens long-term customer retention.

Global production and supply network

Nissha's global production and supply network spans Asia, Europe and North America, supporting local delivery and logistics resilience. Proximity to customers shortens lead times for design tweaks and ramp-ups. Multi-site redundancy mitigates disruption risk and enables cost optimization through load balancing.

- Regional sites: local delivery

- Faster design-to-production

- Redundancy lowers disruption risk

- Load balancing reduces costs

Quality, reliability, and compliance track record

Nissha’s medical and automotive-grade manufacturing adheres to stringent QA and certification regimes, enabling qualification into regulated programs and accelerating time-to-market. Consistently reliable yields reduce customers’ total cost of ownership, supporting repeat orders and referral-driven growth.

- Regulated program access

- Faster qualification

- Lower customer TCO

- Stronger repeat business

Proprietary coating drives ≈¥160B FY2024 revenue and global resilience

Proprietary printing–coating–lamination processes enable high-precision, scalable manufacturing and contributed to FY2024 consolidated revenue of about ¥160 billion. Diversified exposure to electronics, automotive and healthcare reduces cyclicality and accelerates cross‑segment innovation. Global production in Asia, Europe and North America supports local delivery and supply resilience.

| Metric | Fact |

|---|---|

| FY2024 revenue | ≈¥160 billion |

| Key sectors | Electronics, Automotive, Healthcare |

| Global footprint | Asia, Europe, North America |

What is included in the product

Provides a concise SWOT analysis of Nissha, highlighting its internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and competitive positioning.

Provides a concise SWOT matrix of Nissha for fast, visual strategy alignment and risk-relief, ideal for executives needing a snapshot to streamline decisions and integrate into reports.

Weaknesses

Exposure to cyclical demand swings

Consumer electronics and automotive volumes are highly volatile, causing rapid inventory corrections that can compress orders and capacity utilization and strain Nissha’s margins and working capital. Sudden demand swings heighten the risk of underused production lines and elevated inventory write-downs. Short product cycles make forecasting accuracy difficult, exacerbating cash conversion and margin volatility.

Margin pressure from commoditization

Functional films and sensors face persistent price competition as components commoditize, and differentiation risks eroding when rivals scale similar production processes. Defending average selling prices requires sustained R&D investment and frequent design wins to embed Nissha into OEM roadmaps. Procurement-driven OEMs can reset pricing aggressively at contract renewals, pressuring margins and forcing cost-reduction cycles.

Capital- and process-intensive operations

Specialized coating and lamination lines force Nissha into steady capex — FY2024 capex was ¥6.5bn, underscoring continuous investment needs. High fixed costs raise operating leverage, amplifying profit declines in demand downturns. Scaling new programs ties cash in tooling and qualification, and when ramp schedules slip payback periods can extend materially beyond original forecasts.

Raw material cost volatility

Resins, adhesives, conductive inks and films expose Nissha to petrochemical- and metals-driven swings; Brent crude averaged about $85/bbl in 2024, amplifying feedstock cost pressure. Pass-through to customers is imperfect and laggy, compressing gross margins during rapid input spikes. Hedging is often limited for specialty inks and films, leaving short-term spread risk.

- Input categories: resins, adhesives, inks, films

- Driver: petrochemical/metal price volatility (Brent ≈ $85/bbl in 2024)

- Impact: laggy pass-through, compressed spreads

- Mitigation limits: restricted hedging for specialty inputs

Portfolio complexity and focus dilution

Serving multiple industrial and consumer segments increases operational and strategic complexity for Nissha, forcing trade-offs as management balances investment in growth bets versus established cash cows. This allocation challenge can slow internal coordination, delaying product launches and obscuring true segment-level profitability, which complicates capital allocation and performance assessment. Portfolio breadth risks diluting strategic focus and margin optimization.

- Segmental trade-offs

- Slower launches

- Opaque profitability

- Focus dilution

High capex ¥6.5bn and Brent at $85/bbl amplify margin and working capital risk

High fixed costs and steady capex (FY2024 capex ¥6.5bn) increase operating leverage and extend payback if ramps slip. Feedstock exposure (Brent ≈ $85/bbl in 2024) compresses gross margins due to lagging pass-through. Volatile consumer-electronics/autotive volumes drive inventory corrections and margin swings, complicating forecasting and working capital.

| Weakness | Metric | 2024 datapoint | Impact |

|---|---|---|---|

| Capex intensity | Capex | ¥6.5bn | Higher leverage |

| Input volatility | Brent | $85/bbl | Compressed margins |

What You See Is What You Get

Nissha SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version ready for immediate download.

Elevate Your Analysis with the Complete SWOT Report

Explore Nissha's strategic position with our concise SWOT: clear strengths in precision printing and diversified customers, emerging risks from supply chains and competition, and growth drivers in medical and electronics segments. Purchase the full SWOT for a research-backed, editable Word + Excel package with strategic recommendations to inform investments and planning.

Strengths

Deep printing–coating–lamination know-how

Proprietary printing–coating–lamination processes give Nissha high-precision, scalable manufacturing that underpins performance surfaces and functional films with consistent quality. This technical base contributed to FY2024 consolidated revenue of about ¥160 billion and creates switching costs for OEMs dependent on tuned processes. The integrated stack shortens time-to-market for customized solutions, supporting repeat business and faster product launches.

Diversified across electronics, auto, and healthcare

Diversified exposure to electronics, automotive, and healthcare reduces single‑sector cyclicality, with decorative films, touch inputs and medical disposables showing offsetting demand patterns. Cross‑segment learning—materials know‑how from electronics applied to medical disposables and automotive coatings—fuels product innovation and faster time‑to‑market. Management can rebalance revenue toward more resilient categories as cycles shift.

Strong OEM co-development capabilities

Close engineering collaboration with global OEMs embeds Nissha in early design-in cycles, securing specification wins and extending product lifecycles. Early engagement improves forecast visibility and enables premium pricing for tailored parts. This tight integration raises replacement barriers and strengthens long-term customer retention.

Global production and supply network

Nissha's global production and supply network spans Asia, Europe and North America, supporting local delivery and logistics resilience. Proximity to customers shortens lead times for design tweaks and ramp-ups. Multi-site redundancy mitigates disruption risk and enables cost optimization through load balancing.

- Regional sites: local delivery

- Faster design-to-production

- Redundancy lowers disruption risk

- Load balancing reduces costs

Quality, reliability, and compliance track record

Nissha’s medical and automotive-grade manufacturing adheres to stringent QA and certification regimes, enabling qualification into regulated programs and accelerating time-to-market. Consistently reliable yields reduce customers’ total cost of ownership, supporting repeat orders and referral-driven growth.

- Regulated program access

- Faster qualification

- Lower customer TCO

- Stronger repeat business

Proprietary coating drives ≈¥160B FY2024 revenue and global resilience

Proprietary printing–coating–lamination processes enable high-precision, scalable manufacturing and contributed to FY2024 consolidated revenue of about ¥160 billion. Diversified exposure to electronics, automotive and healthcare reduces cyclicality and accelerates cross‑segment innovation. Global production in Asia, Europe and North America supports local delivery and supply resilience.

| Metric | Fact |

|---|---|

| FY2024 revenue | ≈¥160 billion |

| Key sectors | Electronics, Automotive, Healthcare |

| Global footprint | Asia, Europe, North America |

What is included in the product

Provides a concise SWOT analysis of Nissha, highlighting its internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and competitive positioning.

Provides a concise SWOT matrix of Nissha for fast, visual strategy alignment and risk-relief, ideal for executives needing a snapshot to streamline decisions and integrate into reports.

Weaknesses

Exposure to cyclical demand swings

Consumer electronics and automotive volumes are highly volatile, causing rapid inventory corrections that can compress orders and capacity utilization and strain Nissha’s margins and working capital. Sudden demand swings heighten the risk of underused production lines and elevated inventory write-downs. Short product cycles make forecasting accuracy difficult, exacerbating cash conversion and margin volatility.

Margin pressure from commoditization

Functional films and sensors face persistent price competition as components commoditize, and differentiation risks eroding when rivals scale similar production processes. Defending average selling prices requires sustained R&D investment and frequent design wins to embed Nissha into OEM roadmaps. Procurement-driven OEMs can reset pricing aggressively at contract renewals, pressuring margins and forcing cost-reduction cycles.

Capital- and process-intensive operations

Specialized coating and lamination lines force Nissha into steady capex — FY2024 capex was ¥6.5bn, underscoring continuous investment needs. High fixed costs raise operating leverage, amplifying profit declines in demand downturns. Scaling new programs ties cash in tooling and qualification, and when ramp schedules slip payback periods can extend materially beyond original forecasts.

Raw material cost volatility

Resins, adhesives, conductive inks and films expose Nissha to petrochemical- and metals-driven swings; Brent crude averaged about $85/bbl in 2024, amplifying feedstock cost pressure. Pass-through to customers is imperfect and laggy, compressing gross margins during rapid input spikes. Hedging is often limited for specialty inks and films, leaving short-term spread risk.

- Input categories: resins, adhesives, inks, films

- Driver: petrochemical/metal price volatility (Brent ≈ $85/bbl in 2024)

- Impact: laggy pass-through, compressed spreads

- Mitigation limits: restricted hedging for specialty inputs

Portfolio complexity and focus dilution

Serving multiple industrial and consumer segments increases operational and strategic complexity for Nissha, forcing trade-offs as management balances investment in growth bets versus established cash cows. This allocation challenge can slow internal coordination, delaying product launches and obscuring true segment-level profitability, which complicates capital allocation and performance assessment. Portfolio breadth risks diluting strategic focus and margin optimization.

- Segmental trade-offs

- Slower launches

- Opaque profitability

- Focus dilution

High capex ¥6.5bn and Brent at $85/bbl amplify margin and working capital risk

High fixed costs and steady capex (FY2024 capex ¥6.5bn) increase operating leverage and extend payback if ramps slip. Feedstock exposure (Brent ≈ $85/bbl in 2024) compresses gross margins due to lagging pass-through. Volatile consumer-electronics/autotive volumes drive inventory corrections and margin swings, complicating forecasting and working capital.

| Weakness | Metric | 2024 datapoint | Impact |

|---|---|---|---|

| Capex intensity | Capex | ¥6.5bn | Higher leverage |

| Input volatility | Brent | $85/bbl | Compressed margins |

What You See Is What You Get

Nissha SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version ready for immediate download.

Description

Elevate Your Analysis with the Complete SWOT Report

Explore Nissha's strategic position with our concise SWOT: clear strengths in precision printing and diversified customers, emerging risks from supply chains and competition, and growth drivers in medical and electronics segments. Purchase the full SWOT for a research-backed, editable Word + Excel package with strategic recommendations to inform investments and planning.

Strengths

Deep printing–coating–lamination know-how

Proprietary printing–coating–lamination processes give Nissha high-precision, scalable manufacturing that underpins performance surfaces and functional films with consistent quality. This technical base contributed to FY2024 consolidated revenue of about ¥160 billion and creates switching costs for OEMs dependent on tuned processes. The integrated stack shortens time-to-market for customized solutions, supporting repeat business and faster product launches.

Diversified across electronics, auto, and healthcare

Diversified exposure to electronics, automotive, and healthcare reduces single‑sector cyclicality, with decorative films, touch inputs and medical disposables showing offsetting demand patterns. Cross‑segment learning—materials know‑how from electronics applied to medical disposables and automotive coatings—fuels product innovation and faster time‑to‑market. Management can rebalance revenue toward more resilient categories as cycles shift.

Strong OEM co-development capabilities

Close engineering collaboration with global OEMs embeds Nissha in early design-in cycles, securing specification wins and extending product lifecycles. Early engagement improves forecast visibility and enables premium pricing for tailored parts. This tight integration raises replacement barriers and strengthens long-term customer retention.

Global production and supply network

Nissha's global production and supply network spans Asia, Europe and North America, supporting local delivery and logistics resilience. Proximity to customers shortens lead times for design tweaks and ramp-ups. Multi-site redundancy mitigates disruption risk and enables cost optimization through load balancing.

- Regional sites: local delivery

- Faster design-to-production

- Redundancy lowers disruption risk

- Load balancing reduces costs

Quality, reliability, and compliance track record

Nissha’s medical and automotive-grade manufacturing adheres to stringent QA and certification regimes, enabling qualification into regulated programs and accelerating time-to-market. Consistently reliable yields reduce customers’ total cost of ownership, supporting repeat orders and referral-driven growth.

- Regulated program access

- Faster qualification

- Lower customer TCO

- Stronger repeat business

Proprietary coating drives ≈¥160B FY2024 revenue and global resilience

Proprietary printing–coating–lamination processes enable high-precision, scalable manufacturing and contributed to FY2024 consolidated revenue of about ¥160 billion. Diversified exposure to electronics, automotive and healthcare reduces cyclicality and accelerates cross‑segment innovation. Global production in Asia, Europe and North America supports local delivery and supply resilience.

| Metric | Fact |

|---|---|

| FY2024 revenue | ≈¥160 billion |

| Key sectors | Electronics, Automotive, Healthcare |

| Global footprint | Asia, Europe, North America |

What is included in the product

Provides a concise SWOT analysis of Nissha, highlighting its internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and competitive positioning.

Provides a concise SWOT matrix of Nissha for fast, visual strategy alignment and risk-relief, ideal for executives needing a snapshot to streamline decisions and integrate into reports.

Weaknesses

Exposure to cyclical demand swings

Consumer electronics and automotive volumes are highly volatile, causing rapid inventory corrections that can compress orders and capacity utilization and strain Nissha’s margins and working capital. Sudden demand swings heighten the risk of underused production lines and elevated inventory write-downs. Short product cycles make forecasting accuracy difficult, exacerbating cash conversion and margin volatility.

Margin pressure from commoditization

Functional films and sensors face persistent price competition as components commoditize, and differentiation risks eroding when rivals scale similar production processes. Defending average selling prices requires sustained R&D investment and frequent design wins to embed Nissha into OEM roadmaps. Procurement-driven OEMs can reset pricing aggressively at contract renewals, pressuring margins and forcing cost-reduction cycles.

Capital- and process-intensive operations

Specialized coating and lamination lines force Nissha into steady capex — FY2024 capex was ¥6.5bn, underscoring continuous investment needs. High fixed costs raise operating leverage, amplifying profit declines in demand downturns. Scaling new programs ties cash in tooling and qualification, and when ramp schedules slip payback periods can extend materially beyond original forecasts.

Raw material cost volatility

Resins, adhesives, conductive inks and films expose Nissha to petrochemical- and metals-driven swings; Brent crude averaged about $85/bbl in 2024, amplifying feedstock cost pressure. Pass-through to customers is imperfect and laggy, compressing gross margins during rapid input spikes. Hedging is often limited for specialty inks and films, leaving short-term spread risk.

- Input categories: resins, adhesives, inks, films

- Driver: petrochemical/metal price volatility (Brent ≈ $85/bbl in 2024)

- Impact: laggy pass-through, compressed spreads

- Mitigation limits: restricted hedging for specialty inputs

Portfolio complexity and focus dilution

Serving multiple industrial and consumer segments increases operational and strategic complexity for Nissha, forcing trade-offs as management balances investment in growth bets versus established cash cows. This allocation challenge can slow internal coordination, delaying product launches and obscuring true segment-level profitability, which complicates capital allocation and performance assessment. Portfolio breadth risks diluting strategic focus and margin optimization.

- Segmental trade-offs

- Slower launches

- Opaque profitability

- Focus dilution

High capex ¥6.5bn and Brent at $85/bbl amplify margin and working capital risk

High fixed costs and steady capex (FY2024 capex ¥6.5bn) increase operating leverage and extend payback if ramps slip. Feedstock exposure (Brent ≈ $85/bbl in 2024) compresses gross margins due to lagging pass-through. Volatile consumer-electronics/autotive volumes drive inventory corrections and margin swings, complicating forecasting and working capital.

| Weakness | Metric | 2024 datapoint | Impact |

|---|---|---|---|

| Capex intensity | Capex | ¥6.5bn | Higher leverage |

| Input volatility | Brent | $85/bbl | Compressed margins |

What You See Is What You Get

Nissha SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version ready for immediate download.