Nokia Boston Consulting Group Matrix

Actionable Strategy Starts Here

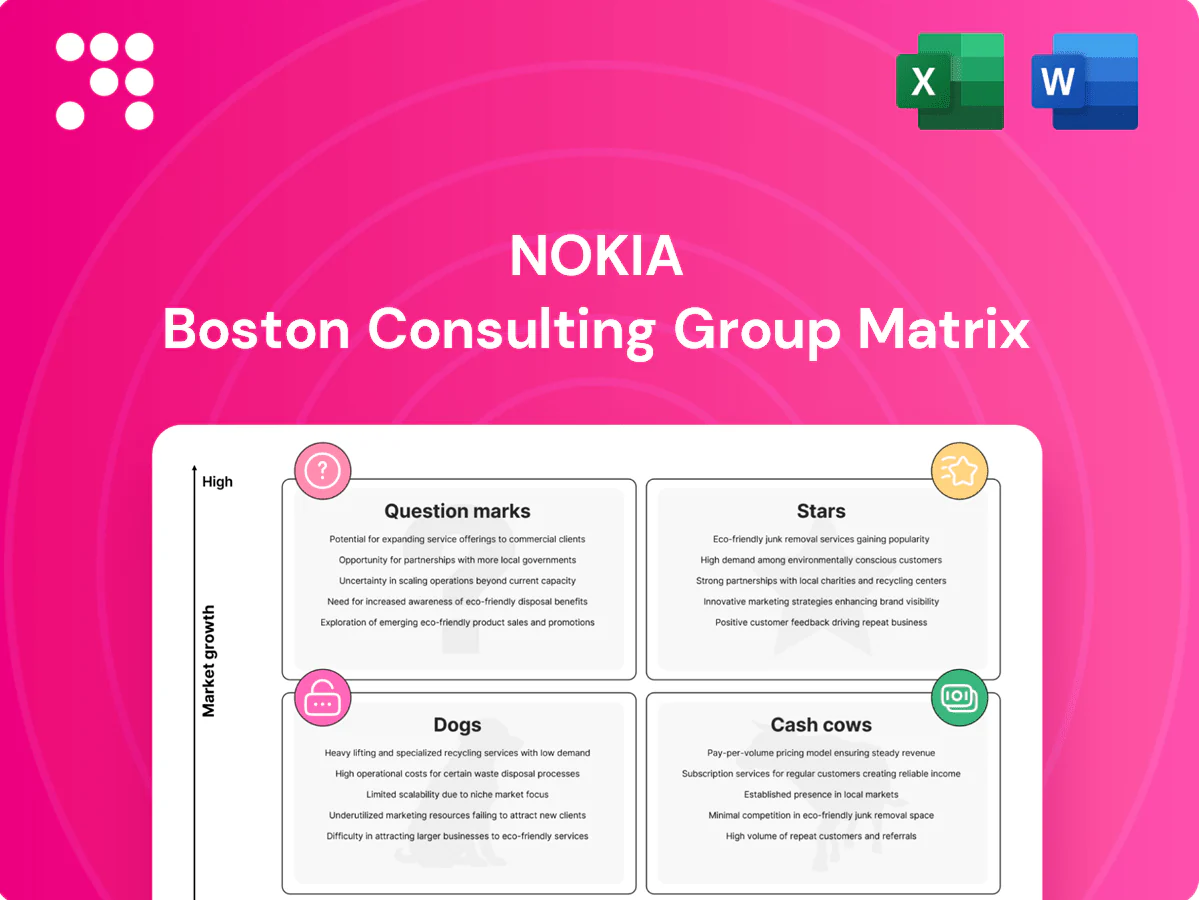

Nokia’s BCG Matrix snapshot shows which product lines are pulling their weight and which need a rethink — a quick read that already highlights potential Stars and stubborn Dogs. Want the full picture with quadrant-by-quadrant data, clear recommendations, and a realistic plan to reallocate capital? Purchase the complete BCG Matrix to get a polished Word report plus an editable Excel summary you can use in board decks. It’s the fast, practical way to turn insight into action.

Stars

5G RAN leadership

5G RAN leadership: Nokia supplies radios to major carriers with roughly one-fifth of the global RAN radio market (~20%), competing in a 5G market generating ~$40–45bn in RAN revenue in 2024; it requires heavy R&D and rollout cash but sets the pace. Continued investment is needed to defend share as the market expands; if growth slows, this star can convert into a cash cow.

Cloud-native 5G Core

Cloud-native 5G Core sits as a Star for Nokia in 2024: operators are actively migrating to cloud cores and Nokia reports strong pipeline in the multi-billion-dollar cloud-native 5G market with double-digit growth, intensifying competition so promotion and placement matter. Revenues are frequently reinvested into delivery and upgrades; staying on offense is necessary to cement leadership before growth normalizes.

Private wireless for enterprise

Factories, ports and energy companies are rapidly adopting private 4.9G/5G, and in 2024 Nokia holds a strong early position with multiple headline deployments in those verticals. The category is scaling fast but complex multi-stakeholder sales cycles still consume cash to win and deploy. Nail reference wins now and you reap steady, long-term returns as rollouts and services normalize.

IP/Optical in high-growth corridors

Backbone upgrades and explosive data traffic in 2024 concentrated in North America, Europe and APAC are driving outsized demand for high-capacity IP and optical systems; Nokia’s high-end routing and coherent optical portfolio has secured major multi-year tickets in these corridors.

Growth here justifies aggressive selling, professional services and field support to convert large trunk sales into recurring revenue and services attach.

Hold share through targeted investments and this IP/Optical stream becomes a durable, high-margin Stars contributor in Nokia’s portfolio.

- Tag: high-growth corridors

- Tag: aggressive selling required

- Tag: durable revenue potential

- Tag: Nokia wins big tickets

Network automation and Orchestration

Network automation and orchestration is a Star for Nokia as telcos demand closed-loop automation to manage denser 5G and edge fabrics; Nokia’s platforms are gaining traction in a rising automation market, pulling services and upsell while requiring continual R&D investment to keep pace.

- Lock in logos early to build long-term annuity

- Drives services revenue and higher ARPU

- Needs sustained capex and software updates

5G RAN, Cloud Core, Private Wireless: defend share, reinvest, scale deployments

Nokia’s 5G RAN is a Star with ~20% radio share in a $40–45bn 2024 RAN market, needing heavy R&D and rollout spend to defend share.

Cloud-native 5G Core is a Star in 2024 with multi-billion demand and double-digit growth; pipeline strong, reinvestment required.

Private wireless and IP/Optical are Stars with headline deployments and multi-year backbone tickets across NA/EU/APAC; aggressive sales and services investment needed.

| Segment | 2024 market | Nokia position | Key action |

|---|---|---|---|

| 5G RAN | $40–45bn | ~20% share | Defend via R&D |

| Cloud Core | Multi‑bn | Strong pipeline | Reinvest |

| Private/IP | Growing | Early wins | Scale deployments |

What is included in the product

Nokia BCG Matrix mapping products into Stars, Cash Cows, Question Marks, Dogs with clear invest, hold or divest guidance.

One-page Nokia BCG Matrix highlighting underperformers and growth bets for quick, C-level strategy decisions

Cash Cows

4G/LTE installed base

Nokia's 4G/LTE installed base spans 130+ countries and supports well over 4 billion devices globally, representing a massive, mature footprint. High-margin upgrades, spares and software maintenance continue to generate steady cash flow and contributed materially to Networks' FY 2024 service revenue. With limited new-build demand, promotional spend stays low while Nokia focuses on milking the base and guiding customers toward 5G migration.

Patent and brand licensing

Nokia’s patent and brand licensing is a cash cow, with royalties contributing over €1bn annually in the 2022–24 period, producing predictable, low-capex cash flows in a low-growth segment. These royalties fund R&D, cover corporate overhead and support dividend policy. Continued enforcement of IP and optimized licensing deals sustain margins and predictability.

Carrier services and maintenance

Carrier services and maintenance sit as a cash cow for Nokia with long-term support contracts with established operators delivering recurring revenue and stable margins; services comprised roughly 30% of Nokia’s net sales in 2023 (about €6bn), reflecting durable cash generation.

Growth is low but predictable, with renewals driving cashflow; operational efficiency initiatives in 2023 improved service margins, lifting free cash further.

Keep SLAs tight to protect margins and expand wallet share softly via upsells, field engineering, and multi‑vendor support to maximize lifetime value.

Fixed access in mature markets

Fixed access in mature markets remains a cash cow for Nokia in 2024. Fiber and PON shipments continue but markets are settled, so steady share converts to dependable returns. Investments target efficiency and cost-per-bit improvements rather than land-grab expansion. Harvest cash and prioritize profitable refresh cycles and upgrades.

- 2024 focus: efficiency over expansion

- Stable fiber/PON volumes, settled demand

- Market share = dependable cashflow

- Prioritize profitable refreshes

Legacy OSS/BSS support

Legacy OSS/BSS support generates steady recurring support fees from deployed stacks; in 2024 operators maintained high renewal behavior, making this a low-growth, sticky, cash-positive business for Nokia. Minimal promotion is required because uptime and SLA compliance drive retention. Streamlining delivery and automation can widen margins materially.

- Recurring fees: predictable cash flow

- Low growth, high stickiness

- Sales light; uptime-focused retention

- Operational streamlining boosts margin

Global 4G + recurring cash >€1bn royalties, services ~30%

Nokia's cash cows: mature 4G footprint (130+ countries, >4bn devices) and carrier services driving recurring cash; patent/brand royalties >€1bn pa (2022–24); services ~30% of net sales (~€6bn in 2023); fixed access/fiber stable in 2024, focus on efficiency and profitable refreshes.

| Item | 2023/24 |

|---|---|

| Services | ~30% sales (€6bn) |

| Royalties | >€1bn pa |

| 4G footprint | 130+ countries, >4bn devices |

Preview = Final Product

Nokia BCG Matrix

The file you're previewing is the exact Nokia BCG Matrix report you'll receive after purchase — no watermarks, no placeholders, just the finished, presentation-ready document. It’s crafted for strategic clarity with clear quadrants, actionable insights, and editable charts. Buy once and download immediately; the full file is ready to edit, print, or share with your team—no surprises, no extra steps.

Actionable Strategy Starts Here

Nokia’s BCG Matrix snapshot shows which product lines are pulling their weight and which need a rethink — a quick read that already highlights potential Stars and stubborn Dogs. Want the full picture with quadrant-by-quadrant data, clear recommendations, and a realistic plan to reallocate capital? Purchase the complete BCG Matrix to get a polished Word report plus an editable Excel summary you can use in board decks. It’s the fast, practical way to turn insight into action.

Stars

5G RAN leadership

5G RAN leadership: Nokia supplies radios to major carriers with roughly one-fifth of the global RAN radio market (~20%), competing in a 5G market generating ~$40–45bn in RAN revenue in 2024; it requires heavy R&D and rollout cash but sets the pace. Continued investment is needed to defend share as the market expands; if growth slows, this star can convert into a cash cow.

Cloud-native 5G Core

Cloud-native 5G Core sits as a Star for Nokia in 2024: operators are actively migrating to cloud cores and Nokia reports strong pipeline in the multi-billion-dollar cloud-native 5G market with double-digit growth, intensifying competition so promotion and placement matter. Revenues are frequently reinvested into delivery and upgrades; staying on offense is necessary to cement leadership before growth normalizes.

Private wireless for enterprise

Factories, ports and energy companies are rapidly adopting private 4.9G/5G, and in 2024 Nokia holds a strong early position with multiple headline deployments in those verticals. The category is scaling fast but complex multi-stakeholder sales cycles still consume cash to win and deploy. Nail reference wins now and you reap steady, long-term returns as rollouts and services normalize.

IP/Optical in high-growth corridors

Backbone upgrades and explosive data traffic in 2024 concentrated in North America, Europe and APAC are driving outsized demand for high-capacity IP and optical systems; Nokia’s high-end routing and coherent optical portfolio has secured major multi-year tickets in these corridors.

Growth here justifies aggressive selling, professional services and field support to convert large trunk sales into recurring revenue and services attach.

Hold share through targeted investments and this IP/Optical stream becomes a durable, high-margin Stars contributor in Nokia’s portfolio.

- Tag: high-growth corridors

- Tag: aggressive selling required

- Tag: durable revenue potential

- Tag: Nokia wins big tickets

Network automation and Orchestration

Network automation and orchestration is a Star for Nokia as telcos demand closed-loop automation to manage denser 5G and edge fabrics; Nokia’s platforms are gaining traction in a rising automation market, pulling services and upsell while requiring continual R&D investment to keep pace.

- Lock in logos early to build long-term annuity

- Drives services revenue and higher ARPU

- Needs sustained capex and software updates

5G RAN, Cloud Core, Private Wireless: defend share, reinvest, scale deployments

Nokia’s 5G RAN is a Star with ~20% radio share in a $40–45bn 2024 RAN market, needing heavy R&D and rollout spend to defend share.

Cloud-native 5G Core is a Star in 2024 with multi-billion demand and double-digit growth; pipeline strong, reinvestment required.

Private wireless and IP/Optical are Stars with headline deployments and multi-year backbone tickets across NA/EU/APAC; aggressive sales and services investment needed.

| Segment | 2024 market | Nokia position | Key action |

|---|---|---|---|

| 5G RAN | $40–45bn | ~20% share | Defend via R&D |

| Cloud Core | Multi‑bn | Strong pipeline | Reinvest |

| Private/IP | Growing | Early wins | Scale deployments |

What is included in the product

Nokia BCG Matrix mapping products into Stars, Cash Cows, Question Marks, Dogs with clear invest, hold or divest guidance.

One-page Nokia BCG Matrix highlighting underperformers and growth bets for quick, C-level strategy decisions

Cash Cows

4G/LTE installed base

Nokia's 4G/LTE installed base spans 130+ countries and supports well over 4 billion devices globally, representing a massive, mature footprint. High-margin upgrades, spares and software maintenance continue to generate steady cash flow and contributed materially to Networks' FY 2024 service revenue. With limited new-build demand, promotional spend stays low while Nokia focuses on milking the base and guiding customers toward 5G migration.

Patent and brand licensing

Nokia’s patent and brand licensing is a cash cow, with royalties contributing over €1bn annually in the 2022–24 period, producing predictable, low-capex cash flows in a low-growth segment. These royalties fund R&D, cover corporate overhead and support dividend policy. Continued enforcement of IP and optimized licensing deals sustain margins and predictability.

Carrier services and maintenance

Carrier services and maintenance sit as a cash cow for Nokia with long-term support contracts with established operators delivering recurring revenue and stable margins; services comprised roughly 30% of Nokia’s net sales in 2023 (about €6bn), reflecting durable cash generation.

Growth is low but predictable, with renewals driving cashflow; operational efficiency initiatives in 2023 improved service margins, lifting free cash further.

Keep SLAs tight to protect margins and expand wallet share softly via upsells, field engineering, and multi‑vendor support to maximize lifetime value.

Fixed access in mature markets

Fixed access in mature markets remains a cash cow for Nokia in 2024. Fiber and PON shipments continue but markets are settled, so steady share converts to dependable returns. Investments target efficiency and cost-per-bit improvements rather than land-grab expansion. Harvest cash and prioritize profitable refresh cycles and upgrades.

- 2024 focus: efficiency over expansion

- Stable fiber/PON volumes, settled demand

- Market share = dependable cashflow

- Prioritize profitable refreshes

Legacy OSS/BSS support

Legacy OSS/BSS support generates steady recurring support fees from deployed stacks; in 2024 operators maintained high renewal behavior, making this a low-growth, sticky, cash-positive business for Nokia. Minimal promotion is required because uptime and SLA compliance drive retention. Streamlining delivery and automation can widen margins materially.

- Recurring fees: predictable cash flow

- Low growth, high stickiness

- Sales light; uptime-focused retention

- Operational streamlining boosts margin

Global 4G + recurring cash >€1bn royalties, services ~30%

Nokia's cash cows: mature 4G footprint (130+ countries, >4bn devices) and carrier services driving recurring cash; patent/brand royalties >€1bn pa (2022–24); services ~30% of net sales (~€6bn in 2023); fixed access/fiber stable in 2024, focus on efficiency and profitable refreshes.

| Item | 2023/24 |

|---|---|

| Services | ~30% sales (€6bn) |

| Royalties | >€1bn pa |

| 4G footprint | 130+ countries, >4bn devices |

Preview = Final Product

Nokia BCG Matrix

The file you're previewing is the exact Nokia BCG Matrix report you'll receive after purchase — no watermarks, no placeholders, just the finished, presentation-ready document. It’s crafted for strategic clarity with clear quadrants, actionable insights, and editable charts. Buy once and download immediately; the full file is ready to edit, print, or share with your team—no surprises, no extra steps.

Description

Actionable Strategy Starts Here

Nokia’s BCG Matrix snapshot shows which product lines are pulling their weight and which need a rethink — a quick read that already highlights potential Stars and stubborn Dogs. Want the full picture with quadrant-by-quadrant data, clear recommendations, and a realistic plan to reallocate capital? Purchase the complete BCG Matrix to get a polished Word report plus an editable Excel summary you can use in board decks. It’s the fast, practical way to turn insight into action.

Stars

5G RAN leadership

5G RAN leadership: Nokia supplies radios to major carriers with roughly one-fifth of the global RAN radio market (~20%), competing in a 5G market generating ~$40–45bn in RAN revenue in 2024; it requires heavy R&D and rollout cash but sets the pace. Continued investment is needed to defend share as the market expands; if growth slows, this star can convert into a cash cow.

Cloud-native 5G Core

Cloud-native 5G Core sits as a Star for Nokia in 2024: operators are actively migrating to cloud cores and Nokia reports strong pipeline in the multi-billion-dollar cloud-native 5G market with double-digit growth, intensifying competition so promotion and placement matter. Revenues are frequently reinvested into delivery and upgrades; staying on offense is necessary to cement leadership before growth normalizes.

Private wireless for enterprise

Factories, ports and energy companies are rapidly adopting private 4.9G/5G, and in 2024 Nokia holds a strong early position with multiple headline deployments in those verticals. The category is scaling fast but complex multi-stakeholder sales cycles still consume cash to win and deploy. Nail reference wins now and you reap steady, long-term returns as rollouts and services normalize.

IP/Optical in high-growth corridors

Backbone upgrades and explosive data traffic in 2024 concentrated in North America, Europe and APAC are driving outsized demand for high-capacity IP and optical systems; Nokia’s high-end routing and coherent optical portfolio has secured major multi-year tickets in these corridors.

Growth here justifies aggressive selling, professional services and field support to convert large trunk sales into recurring revenue and services attach.

Hold share through targeted investments and this IP/Optical stream becomes a durable, high-margin Stars contributor in Nokia’s portfolio.

- Tag: high-growth corridors

- Tag: aggressive selling required

- Tag: durable revenue potential

- Tag: Nokia wins big tickets

Network automation and Orchestration

Network automation and orchestration is a Star for Nokia as telcos demand closed-loop automation to manage denser 5G and edge fabrics; Nokia’s platforms are gaining traction in a rising automation market, pulling services and upsell while requiring continual R&D investment to keep pace.

- Lock in logos early to build long-term annuity

- Drives services revenue and higher ARPU

- Needs sustained capex and software updates

5G RAN, Cloud Core, Private Wireless: defend share, reinvest, scale deployments

Nokia’s 5G RAN is a Star with ~20% radio share in a $40–45bn 2024 RAN market, needing heavy R&D and rollout spend to defend share.

Cloud-native 5G Core is a Star in 2024 with multi-billion demand and double-digit growth; pipeline strong, reinvestment required.

Private wireless and IP/Optical are Stars with headline deployments and multi-year backbone tickets across NA/EU/APAC; aggressive sales and services investment needed.

| Segment | 2024 market | Nokia position | Key action |

|---|---|---|---|

| 5G RAN | $40–45bn | ~20% share | Defend via R&D |

| Cloud Core | Multi‑bn | Strong pipeline | Reinvest |

| Private/IP | Growing | Early wins | Scale deployments |

What is included in the product

Nokia BCG Matrix mapping products into Stars, Cash Cows, Question Marks, Dogs with clear invest, hold or divest guidance.

One-page Nokia BCG Matrix highlighting underperformers and growth bets for quick, C-level strategy decisions

Cash Cows

4G/LTE installed base

Nokia's 4G/LTE installed base spans 130+ countries and supports well over 4 billion devices globally, representing a massive, mature footprint. High-margin upgrades, spares and software maintenance continue to generate steady cash flow and contributed materially to Networks' FY 2024 service revenue. With limited new-build demand, promotional spend stays low while Nokia focuses on milking the base and guiding customers toward 5G migration.

Patent and brand licensing

Nokia’s patent and brand licensing is a cash cow, with royalties contributing over €1bn annually in the 2022–24 period, producing predictable, low-capex cash flows in a low-growth segment. These royalties fund R&D, cover corporate overhead and support dividend policy. Continued enforcement of IP and optimized licensing deals sustain margins and predictability.

Carrier services and maintenance

Carrier services and maintenance sit as a cash cow for Nokia with long-term support contracts with established operators delivering recurring revenue and stable margins; services comprised roughly 30% of Nokia’s net sales in 2023 (about €6bn), reflecting durable cash generation.

Growth is low but predictable, with renewals driving cashflow; operational efficiency initiatives in 2023 improved service margins, lifting free cash further.

Keep SLAs tight to protect margins and expand wallet share softly via upsells, field engineering, and multi‑vendor support to maximize lifetime value.

Fixed access in mature markets

Fixed access in mature markets remains a cash cow for Nokia in 2024. Fiber and PON shipments continue but markets are settled, so steady share converts to dependable returns. Investments target efficiency and cost-per-bit improvements rather than land-grab expansion. Harvest cash and prioritize profitable refresh cycles and upgrades.

- 2024 focus: efficiency over expansion

- Stable fiber/PON volumes, settled demand

- Market share = dependable cashflow

- Prioritize profitable refreshes

Legacy OSS/BSS support

Legacy OSS/BSS support generates steady recurring support fees from deployed stacks; in 2024 operators maintained high renewal behavior, making this a low-growth, sticky, cash-positive business for Nokia. Minimal promotion is required because uptime and SLA compliance drive retention. Streamlining delivery and automation can widen margins materially.

- Recurring fees: predictable cash flow

- Low growth, high stickiness

- Sales light; uptime-focused retention

- Operational streamlining boosts margin

Global 4G + recurring cash >€1bn royalties, services ~30%

Nokia's cash cows: mature 4G footprint (130+ countries, >4bn devices) and carrier services driving recurring cash; patent/brand royalties >€1bn pa (2022–24); services ~30% of net sales (~€6bn in 2023); fixed access/fiber stable in 2024, focus on efficiency and profitable refreshes.

| Item | 2023/24 |

|---|---|

| Services | ~30% sales (€6bn) |

| Royalties | >€1bn pa |

| 4G footprint | 130+ countries, >4bn devices |

Preview = Final Product

Nokia BCG Matrix

The file you're previewing is the exact Nokia BCG Matrix report you'll receive after purchase — no watermarks, no placeholders, just the finished, presentation-ready document. It’s crafted for strategic clarity with clear quadrants, actionable insights, and editable charts. Buy once and download immediately; the full file is ready to edit, print, or share with your team—no surprises, no extra steps.