Nortech Porter's Five Forces Analysis

From Overview to Strategy Blueprint

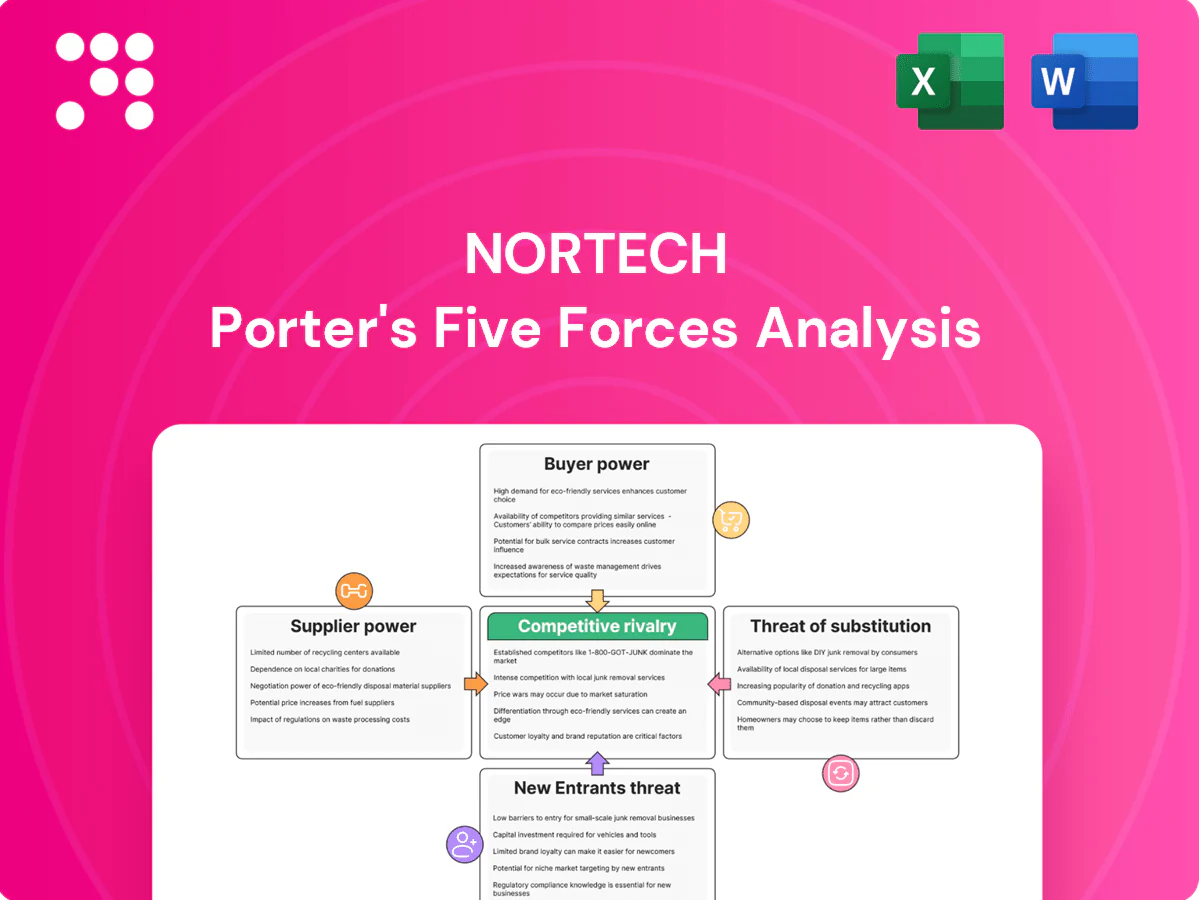

Nortech’s Porter's Five Forces snapshot highlights key pressures—supplier leverage, buyer sensitivity, competitive rivalry, new entrants, and substitutes—that shape its strategic options and margins. This concise view identifies risks and advantages, but the full Porter's Five Forces Analysis unlocks force-by-force ratings, visuals, and actionable recommendations to guide investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical components

Semiconductor, connector and specialty-cable suppliers remain concentrated, with the top vendors capturing well over half of key capacity, giving them leverage on price and allocation; long lead times (often 20–52 weeks) and allocation cycles can squeeze Nortech’s schedules and gross margins. Strategic forecasts, long-term agreements and buffer stocks can temper supplier power, while preferred-supplier programs and multi-sourcing reduce single-point exposure.

Regulated materials and compliance

As of 2024, suppliers meeting ITAR/DFARS, RoHS/REACH and ISO 13485/AS9100 remain a smaller subset, boosting vendor power and switching costs for medical and defense builds. Nortech’s rigorous quality systems and supplier audits expand the qualified vendor pool. Early compliance engineering reduces supplier gatekeeping and lowers time-to-market risk.

Specialized test and equipment vendors

ATE, conformal-coating and inspection-gear vendors wield leverage through proprietary ecosystems and multi-year service contracts; upgrades and spares commonly add 20–40% to lifecycle costs, raising total cost of ownership. Negotiating multi-year service bundles can cap annual price escalation and service fees. Choosing cross-compatible tooling preserves flexibility and reduces lock-in risk.

Geopolitical and logistics exposure

Geopolitical tariffs, export controls and freight volatility raised supplier leverage during 2024, with spot container-rate swings of ~30% and 42% of OEMs reporting tariff-related cost inflation; defense and medical contracts demand near-zero disruption and ITAR/sterility continuity, increasing switching costs for Nortech. Nearshoring and regional dual-sourcing cut single-vendor exposure, while scorecards tie penalties/rewards to OTIF and quality metrics.

- 2024 freight volatility ~30%

- 42% OEMs reported tariff cost hits

- Defense/medical continuity: near-zero tolerance

- Vendor scorecards link OTIF to incentives

Design influence and DFM leverage

Nortech’s DFM lets engineering substitute scarce parts with approved equivalents, cutting single-source exposure and enabling early BOM rationalization that historically trims supplier leverage by reducing part count and spend concentration.

Value engineering and AVL expansion lower dependency while co-development agreements share cost, yield and scrap transparency, improving negotiation positions and enabling joint savings capture in 2024 supply-chain recovery.

- DFM substitutes scarce parts

- Early BOM rationalization reduces supplier power

- AVL expansion and value engineering cut dependency

- Co-development shares costs, yields, scrap

Supply concentration, 20–52 wk lead times and ~30% freight volatility

Supplier concentration and 20–52 week lead times pressure Nortech’s margins; 2024 saw ~30% freight volatility and 42% of OEMs reporting tariff cost hits. ITAR/DFARS/ISO-qualified vendors are limited, raising switching costs for medical/defense. Mitigations: long-term contracts, DFM, multi-sourcing, nearshoring to cut single-vendor risk.

| Metric | 2024 |

|---|---|

| Freight volatility | ~30% |

| OEMs tariff impact | 42% |

| Lead times | 20–52 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Nortech that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and rivalry. Includes strategic implications, emerging threats, and editable insights for investor decks, business plans, or internal strategy.

A single-sheet, customizable Porter’s Five Forces tool that visualizes competitive pressure with radar charts and editable scores—ready for decks, scenario tabs, and integration into Excel without macros.

Customers Bargaining Power

Large OEMs with scale

Large medical, industrial and defense OEMs purchase at scale and use competitive RFPs to benchmark EMS pricing, creating significant price pressure on suppliers. Their regulatory validations and PPAP-like approvals typically require 6–24 months of requalification and can incur six-figure to low seven-figure costs, raising switching costs. Multi-year agreements, commonly 3–5 years, are used to trade lower unit prices for demand visibility and capacity commitments.

High qualification and switching costs

Transfers in MedTech and defense typically demand revalidation, tooling changes and process qualification taking 6–18 months, which materially reduces price-driven switching; dual-sourcing remains common for risk mitigation. Buyers value suppliers with superior quality metrics—many OEMs expect DPPM below 100 in MedTech and under 50 in aerospace—limiting buyer leverage.

Service breadth and integration

End-to-end engineering, prototyping and supply‑chain services create strong lock‑in by embedding design, testing and logistics; customers report 20–30% inventory reductions and 25–50% lead‑time cuts from integrated VMI/kanban in 2024 deployments. Integrated VMI/kanban and vendor‑managed transport agreements (VTAs) increase dependency on Nortech systems and processes. Buyers realize 10–20% total cost of ownership savings beyond piece price, so value stacking offsets pure price bargaining.

Demand cyclicality and mix

- Demand swings shift leverage to buyers during downcycles

- Lumpy orders push expedite costs to suppliers (60% OEMs, 2024)

- MOQs and capacity plans smooth volatility

- S&OP reduces chargebacks and expedited freight (~20% improvement, 2024)

Compliance and reliability needs

Buyers prioritize quality, traceability and on-time delivery over lowest cost, with 62% of procurement leaders citing reliability as top criterion (Deloitte CPO Survey 2024), which reduces effective price bargaining when risk is high. Strong audit results and ISO certifications narrowed supplier pools by ~35% in 2024 (Procurement Leaders), and performance-based SLAs shift power to proven partners.

- 62% reliability over cost (Deloitte 2024)

- ~35% supplier narrowing via audits (Procurement Leaders 2024)

- SLAs increase share to reliable suppliers

OEM RFPs squeeze prices; 10-30% TCO savings from multi-year contracts and VMI

Large OEMs drive strong price pressure via competitive RFPs but face high switching costs from 6–24 month requalifications and six‑figure+ requalification costs. Multi‑year contracts (3–5 yrs) and integrated engineering/VMI deliver 10–30% TCO savings, offsetting pure price leverage. Demand cyclicality gives buyers edge in downcycles, while reliability and certifications (62% prioritize reliability, ~35% supplier narrowing in 2024) constrain buyer power.

| Metric | 2024 | Impact |

|---|---|---|

| Requalification time | 6–24 months | High switching cost |

| Reliability priority | 62% (Deloitte 2024) | Limits price focus |

| Supplier narrowing | ~35% (2024) | Reduces buyer options |

Same Document Delivered

Nortech Porter's Five Forces Analysis

This preview shows the exact Nortech Porter's Five Forces Analysis you'll receive—no samples or placeholders. The full, professionally formatted document is available for immediate download once you complete your purchase. It's ready to use for strategic planning, valuation, or presentation. No surprises, just the final deliverable.

From Overview to Strategy Blueprint

Nortech’s Porter's Five Forces snapshot highlights key pressures—supplier leverage, buyer sensitivity, competitive rivalry, new entrants, and substitutes—that shape its strategic options and margins. This concise view identifies risks and advantages, but the full Porter's Five Forces Analysis unlocks force-by-force ratings, visuals, and actionable recommendations to guide investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical components

Semiconductor, connector and specialty-cable suppliers remain concentrated, with the top vendors capturing well over half of key capacity, giving them leverage on price and allocation; long lead times (often 20–52 weeks) and allocation cycles can squeeze Nortech’s schedules and gross margins. Strategic forecasts, long-term agreements and buffer stocks can temper supplier power, while preferred-supplier programs and multi-sourcing reduce single-point exposure.

Regulated materials and compliance

As of 2024, suppliers meeting ITAR/DFARS, RoHS/REACH and ISO 13485/AS9100 remain a smaller subset, boosting vendor power and switching costs for medical and defense builds. Nortech’s rigorous quality systems and supplier audits expand the qualified vendor pool. Early compliance engineering reduces supplier gatekeeping and lowers time-to-market risk.

Specialized test and equipment vendors

ATE, conformal-coating and inspection-gear vendors wield leverage through proprietary ecosystems and multi-year service contracts; upgrades and spares commonly add 20–40% to lifecycle costs, raising total cost of ownership. Negotiating multi-year service bundles can cap annual price escalation and service fees. Choosing cross-compatible tooling preserves flexibility and reduces lock-in risk.

Geopolitical and logistics exposure

Geopolitical tariffs, export controls and freight volatility raised supplier leverage during 2024, with spot container-rate swings of ~30% and 42% of OEMs reporting tariff-related cost inflation; defense and medical contracts demand near-zero disruption and ITAR/sterility continuity, increasing switching costs for Nortech. Nearshoring and regional dual-sourcing cut single-vendor exposure, while scorecards tie penalties/rewards to OTIF and quality metrics.

- 2024 freight volatility ~30%

- 42% OEMs reported tariff cost hits

- Defense/medical continuity: near-zero tolerance

- Vendor scorecards link OTIF to incentives

Design influence and DFM leverage

Nortech’s DFM lets engineering substitute scarce parts with approved equivalents, cutting single-source exposure and enabling early BOM rationalization that historically trims supplier leverage by reducing part count and spend concentration.

Value engineering and AVL expansion lower dependency while co-development agreements share cost, yield and scrap transparency, improving negotiation positions and enabling joint savings capture in 2024 supply-chain recovery.

- DFM substitutes scarce parts

- Early BOM rationalization reduces supplier power

- AVL expansion and value engineering cut dependency

- Co-development shares costs, yields, scrap

Supply concentration, 20–52 wk lead times and ~30% freight volatility

Supplier concentration and 20–52 week lead times pressure Nortech’s margins; 2024 saw ~30% freight volatility and 42% of OEMs reporting tariff cost hits. ITAR/DFARS/ISO-qualified vendors are limited, raising switching costs for medical/defense. Mitigations: long-term contracts, DFM, multi-sourcing, nearshoring to cut single-vendor risk.

| Metric | 2024 |

|---|---|

| Freight volatility | ~30% |

| OEMs tariff impact | 42% |

| Lead times | 20–52 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Nortech that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and rivalry. Includes strategic implications, emerging threats, and editable insights for investor decks, business plans, or internal strategy.

A single-sheet, customizable Porter’s Five Forces tool that visualizes competitive pressure with radar charts and editable scores—ready for decks, scenario tabs, and integration into Excel without macros.

Customers Bargaining Power

Large OEMs with scale

Large medical, industrial and defense OEMs purchase at scale and use competitive RFPs to benchmark EMS pricing, creating significant price pressure on suppliers. Their regulatory validations and PPAP-like approvals typically require 6–24 months of requalification and can incur six-figure to low seven-figure costs, raising switching costs. Multi-year agreements, commonly 3–5 years, are used to trade lower unit prices for demand visibility and capacity commitments.

High qualification and switching costs

Transfers in MedTech and defense typically demand revalidation, tooling changes and process qualification taking 6–18 months, which materially reduces price-driven switching; dual-sourcing remains common for risk mitigation. Buyers value suppliers with superior quality metrics—many OEMs expect DPPM below 100 in MedTech and under 50 in aerospace—limiting buyer leverage.

Service breadth and integration

End-to-end engineering, prototyping and supply‑chain services create strong lock‑in by embedding design, testing and logistics; customers report 20–30% inventory reductions and 25–50% lead‑time cuts from integrated VMI/kanban in 2024 deployments. Integrated VMI/kanban and vendor‑managed transport agreements (VTAs) increase dependency on Nortech systems and processes. Buyers realize 10–20% total cost of ownership savings beyond piece price, so value stacking offsets pure price bargaining.

Demand cyclicality and mix

- Demand swings shift leverage to buyers during downcycles

- Lumpy orders push expedite costs to suppliers (60% OEMs, 2024)

- MOQs and capacity plans smooth volatility

- S&OP reduces chargebacks and expedited freight (~20% improvement, 2024)

Compliance and reliability needs

Buyers prioritize quality, traceability and on-time delivery over lowest cost, with 62% of procurement leaders citing reliability as top criterion (Deloitte CPO Survey 2024), which reduces effective price bargaining when risk is high. Strong audit results and ISO certifications narrowed supplier pools by ~35% in 2024 (Procurement Leaders), and performance-based SLAs shift power to proven partners.

- 62% reliability over cost (Deloitte 2024)

- ~35% supplier narrowing via audits (Procurement Leaders 2024)

- SLAs increase share to reliable suppliers

OEM RFPs squeeze prices; 10-30% TCO savings from multi-year contracts and VMI

Large OEMs drive strong price pressure via competitive RFPs but face high switching costs from 6–24 month requalifications and six‑figure+ requalification costs. Multi‑year contracts (3–5 yrs) and integrated engineering/VMI deliver 10–30% TCO savings, offsetting pure price leverage. Demand cyclicality gives buyers edge in downcycles, while reliability and certifications (62% prioritize reliability, ~35% supplier narrowing in 2024) constrain buyer power.

| Metric | 2024 | Impact |

|---|---|---|

| Requalification time | 6–24 months | High switching cost |

| Reliability priority | 62% (Deloitte 2024) | Limits price focus |

| Supplier narrowing | ~35% (2024) | Reduces buyer options |

Same Document Delivered

Nortech Porter's Five Forces Analysis

This preview shows the exact Nortech Porter's Five Forces Analysis you'll receive—no samples or placeholders. The full, professionally formatted document is available for immediate download once you complete your purchase. It's ready to use for strategic planning, valuation, or presentation. No surprises, just the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Nortech’s Porter's Five Forces snapshot highlights key pressures—supplier leverage, buyer sensitivity, competitive rivalry, new entrants, and substitutes—that shape its strategic options and margins. This concise view identifies risks and advantages, but the full Porter's Five Forces Analysis unlocks force-by-force ratings, visuals, and actionable recommendations to guide investment and strategy decisions.

Suppliers Bargaining Power

Concentrated critical components

Semiconductor, connector and specialty-cable suppliers remain concentrated, with the top vendors capturing well over half of key capacity, giving them leverage on price and allocation; long lead times (often 20–52 weeks) and allocation cycles can squeeze Nortech’s schedules and gross margins. Strategic forecasts, long-term agreements and buffer stocks can temper supplier power, while preferred-supplier programs and multi-sourcing reduce single-point exposure.

Regulated materials and compliance

As of 2024, suppliers meeting ITAR/DFARS, RoHS/REACH and ISO 13485/AS9100 remain a smaller subset, boosting vendor power and switching costs for medical and defense builds. Nortech’s rigorous quality systems and supplier audits expand the qualified vendor pool. Early compliance engineering reduces supplier gatekeeping and lowers time-to-market risk.

Specialized test and equipment vendors

ATE, conformal-coating and inspection-gear vendors wield leverage through proprietary ecosystems and multi-year service contracts; upgrades and spares commonly add 20–40% to lifecycle costs, raising total cost of ownership. Negotiating multi-year service bundles can cap annual price escalation and service fees. Choosing cross-compatible tooling preserves flexibility and reduces lock-in risk.

Geopolitical and logistics exposure

Geopolitical tariffs, export controls and freight volatility raised supplier leverage during 2024, with spot container-rate swings of ~30% and 42% of OEMs reporting tariff-related cost inflation; defense and medical contracts demand near-zero disruption and ITAR/sterility continuity, increasing switching costs for Nortech. Nearshoring and regional dual-sourcing cut single-vendor exposure, while scorecards tie penalties/rewards to OTIF and quality metrics.

- 2024 freight volatility ~30%

- 42% OEMs reported tariff cost hits

- Defense/medical continuity: near-zero tolerance

- Vendor scorecards link OTIF to incentives

Design influence and DFM leverage

Nortech’s DFM lets engineering substitute scarce parts with approved equivalents, cutting single-source exposure and enabling early BOM rationalization that historically trims supplier leverage by reducing part count and spend concentration.

Value engineering and AVL expansion lower dependency while co-development agreements share cost, yield and scrap transparency, improving negotiation positions and enabling joint savings capture in 2024 supply-chain recovery.

- DFM substitutes scarce parts

- Early BOM rationalization reduces supplier power

- AVL expansion and value engineering cut dependency

- Co-development shares costs, yields, scrap

Supply concentration, 20–52 wk lead times and ~30% freight volatility

Supplier concentration and 20–52 week lead times pressure Nortech’s margins; 2024 saw ~30% freight volatility and 42% of OEMs reporting tariff cost hits. ITAR/DFARS/ISO-qualified vendors are limited, raising switching costs for medical/defense. Mitigations: long-term contracts, DFM, multi-sourcing, nearshoring to cut single-vendor risk.

| Metric | 2024 |

|---|---|

| Freight volatility | ~30% |

| OEMs tariff impact | 42% |

| Lead times | 20–52 wks |

What is included in the product

Tailored Porter's Five Forces analysis for Nortech that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and rivalry. Includes strategic implications, emerging threats, and editable insights for investor decks, business plans, or internal strategy.

A single-sheet, customizable Porter’s Five Forces tool that visualizes competitive pressure with radar charts and editable scores—ready for decks, scenario tabs, and integration into Excel without macros.

Customers Bargaining Power

Large OEMs with scale

Large medical, industrial and defense OEMs purchase at scale and use competitive RFPs to benchmark EMS pricing, creating significant price pressure on suppliers. Their regulatory validations and PPAP-like approvals typically require 6–24 months of requalification and can incur six-figure to low seven-figure costs, raising switching costs. Multi-year agreements, commonly 3–5 years, are used to trade lower unit prices for demand visibility and capacity commitments.

High qualification and switching costs

Transfers in MedTech and defense typically demand revalidation, tooling changes and process qualification taking 6–18 months, which materially reduces price-driven switching; dual-sourcing remains common for risk mitigation. Buyers value suppliers with superior quality metrics—many OEMs expect DPPM below 100 in MedTech and under 50 in aerospace—limiting buyer leverage.

Service breadth and integration

End-to-end engineering, prototyping and supply‑chain services create strong lock‑in by embedding design, testing and logistics; customers report 20–30% inventory reductions and 25–50% lead‑time cuts from integrated VMI/kanban in 2024 deployments. Integrated VMI/kanban and vendor‑managed transport agreements (VTAs) increase dependency on Nortech systems and processes. Buyers realize 10–20% total cost of ownership savings beyond piece price, so value stacking offsets pure price bargaining.

Demand cyclicality and mix

- Demand swings shift leverage to buyers during downcycles

- Lumpy orders push expedite costs to suppliers (60% OEMs, 2024)

- MOQs and capacity plans smooth volatility

- S&OP reduces chargebacks and expedited freight (~20% improvement, 2024)

Compliance and reliability needs

Buyers prioritize quality, traceability and on-time delivery over lowest cost, with 62% of procurement leaders citing reliability as top criterion (Deloitte CPO Survey 2024), which reduces effective price bargaining when risk is high. Strong audit results and ISO certifications narrowed supplier pools by ~35% in 2024 (Procurement Leaders), and performance-based SLAs shift power to proven partners.

- 62% reliability over cost (Deloitte 2024)

- ~35% supplier narrowing via audits (Procurement Leaders 2024)

- SLAs increase share to reliable suppliers

OEM RFPs squeeze prices; 10-30% TCO savings from multi-year contracts and VMI

Large OEMs drive strong price pressure via competitive RFPs but face high switching costs from 6–24 month requalifications and six‑figure+ requalification costs. Multi‑year contracts (3–5 yrs) and integrated engineering/VMI deliver 10–30% TCO savings, offsetting pure price leverage. Demand cyclicality gives buyers edge in downcycles, while reliability and certifications (62% prioritize reliability, ~35% supplier narrowing in 2024) constrain buyer power.

| Metric | 2024 | Impact |

|---|---|---|

| Requalification time | 6–24 months | High switching cost |

| Reliability priority | 62% (Deloitte 2024) | Limits price focus |

| Supplier narrowing | ~35% (2024) | Reduces buyer options |

Same Document Delivered

Nortech Porter's Five Forces Analysis

This preview shows the exact Nortech Porter's Five Forces Analysis you'll receive—no samples or placeholders. The full, professionally formatted document is available for immediate download once you complete your purchase. It's ready to use for strategic planning, valuation, or presentation. No surprises, just the final deliverable.