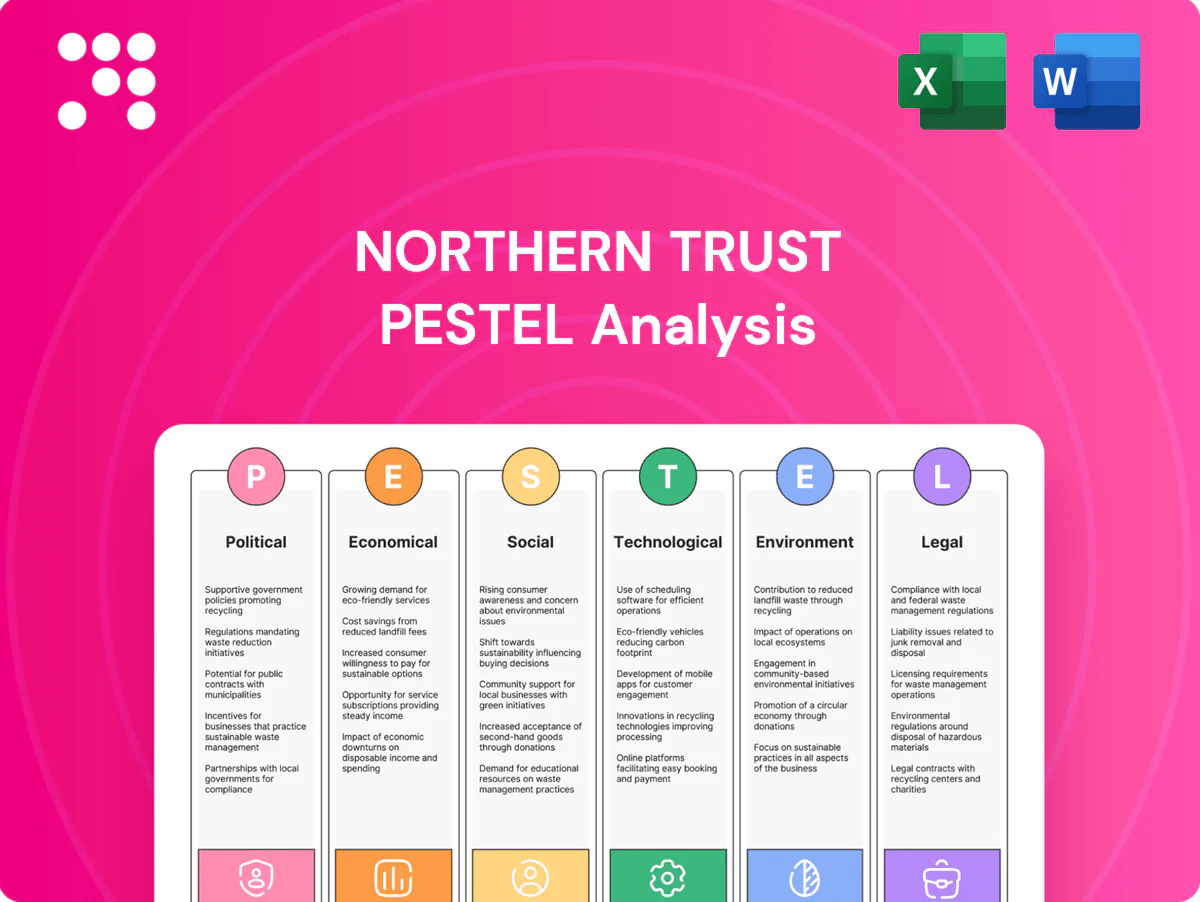

Northern Trust PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological change are reshaping Northern Trust’s competitive landscape in our concise PESTLE snapshot. This analysis highlights regulatory risks, ESG pressures, and market opportunities you need to know. Buy the full PESTLE to get the complete, actionable briefing for investment and strategy decisions.

Political factors

Geopolitical tensions and sanctions

Heightened geopolitical risk and evolving sanctions regimes increase complexity for Northern Trust's cross-border custody, payments and asset servicing, forcing continuous client and transaction screening, re-mapping of operating processes and investment guideline adjustments. Rapid sanctions updates — over 500 major listings in 2023–24 — raise operational complexity and legal exposure. Diversification of booking centers and contingency plans mitigate disruption to its roughly $15 trillion custody footprint.

Regulatory policymaking and oversight

Policy priorities of US, UK, EU and APAC authorities drive capital, liquidity and conduct standards across custody and asset management. Basel III endgame implementation continues across jurisdictions through 2023–2028, changing capital metrics. Supervisory focus on operational resilience and third‑party risk, highlighted by EU DORA effective 17 January 2025, raises compliance costs. Regulatory engagement shapes approvals for new services and can reprice fee models.

Tax policy and cross-border treaties

Changes in corporate, withholding, and wealth taxes shift client behavior and asset location, pressuring custodians to adapt servicing models and client reporting. OECD Pillar Two's 15% global minimum tax, adopted by about 137 jurisdictions, is already reshaping fund domiciles and cross-border flows. Northern Trust must keep tax-operational expertise to prevent leakage and errors in withholding and reporting. Political debates on wealth taxation can materially affect demand for trust and estate services.

Trade policy and market access

Tariffs, localization rules and market-access restrictions force custodians to reconfigure global operating models and redeploy staff and systems across jurisdictions.

Post-Brexit divergence necessitates parallel UK/EU capabilities for custody, tax and compliance flows; local data and outsourcing rules determine where services are booked and processed.

- Political shifts can affect sovereign/public mandates — sovereign wealth funds ≈$10.6 trillion (SWF Institute 2024)

- Increased compliance costs per jurisdiction

Public-sector investment priorities

Government agendas on infrastructure (US IIJA $1.2 trillion) and rising pension/healthcare liabilities drive institutional asset growth, creating demand for custody, fiduciary and liability-driven investment solutions; sovereign and public fund mandates hinge on policy stability and governance norms. Northern Trust can capture flows from public-private partnerships and pension reform, though political turnover can rapidly alter mandate criteria and allocations.

- IIJA $1.2T

- Global pension assets ~57T (2023)

- Sovereign wealth funds ≈$10.8T (2024)

- PPP and pension reform = client flows

Geopolitical sanctions, DORA and Pillar Two squeeze $15T custody model

Heightened geopolitical risk and sanctions (500+ listings 2023–24) raise custody, payments and compliance complexity for Northern Trust's ~$15T custody footprint, forcing booking diversification and continuous screening. Basel III endgame and DORA (effective 17 Jan 2025) increase capital and resilience costs. OECD Pillar Two (15%, ~137 jurisdictions) reshapes domiciles and reporting.

| Metric | Value |

|---|---|

| Custody AUA | $15T |

| Sanctions 2023–24 | 500+ |

| Pillar Two | 15% / ~137 jurisdictions |

| DORA effective | 17 Jan 2025 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Northern Trust, combining current data and trends to identify risks, opportunities and strategic implications. Delivered as actionable, forward‑looking insights formatted for reports, decks and scenario planning.

A concise, visually segmented PESTLE summary of Northern Trust that can be dropped into presentations, edited with region- or business‑line notes, and easily shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rates and yield curve

Northern Trusts net interest income and securities lending revenues are highly rate-sensitive; with the Fed funds target at 5.25–5.50% (July 2025) and the 2s10s roughly -40 bps, curve shape materially affects reinvestment yields. Steeper, stable curves lower deposit betas while inversions push betas toward 30–40% and compress margins. Rapid central bank pivots have reduced client cash balances and squeezed NII in past quarters. Active hedging and product-mix shifts remain critical to protect spreads.

Market levels and AUM/AUC volatility

Fee revenues at Northern Trust track equity and fixed‑income valuations; global equities fell ~20% in 2022 then rose ~25% in 2023, driving AUM-linked fees and servicing swings. Prolonged drawdowns in 2022 cut performance fees and transaction volumes, while rebalancing and flight‑to‑quality shifted client demand toward cash and government bonds. Operating leverage magnifies these revenue cycles for custody and asset servicing margins.

Inflation and expense dynamics

Rising inflation (US CPI ~3.4% in 2024) pushed salary growth near 4% and lifted technology and vendor contract costs, pressuring Northern Trusts efficiency metrics. Clients reallocated toward inflation-hedging assets like TIPS and commodities, changing custody and advisory servicing mixes. Real-return mandates tightened benchmarks and fee terms. Pricing discipline and accelerated automation reduced projected cost creep.

FX volatility and global flows

Currency swings affect translated revenues and client hedging demand, with global FX turnover at about 7.5 trillion USD daily per the BIS triennial survey (2022), boosting cross-border custody and collateral flows while increasing basis risk and margin calls that elevate operational and credit exposures; natural hedges and treasury strategies reduce earnings variability.

- FX turnover: 7.5T USD/day (BIS 2022)

- Higher hedging demand

- More custody/collateral activity

- Increased basis risk & margin calls

- Treasury/natural hedges mitigate earnings swings

Fee compression and competition

Indexing and passive adoption have pushed global ETF/AUM past $13 trillion by end-2024, compressing asset management fees and driving margin pressure on active mandates.

Asset servicers face price erosion on commoditized custody and administration functions, while value shifts to data, analytics, alternatives and outsourced middle-office solutions.

Differentiation now depends on scale, advanced technology and specialized expertise to capture higher-margin services.

- Passive AUM > $13T (end-2024)

- Fee compression hits core custody/admin

- Growth areas: data, analytics, alternatives, OMNI (outsourced middle office)

- Competitive edge: scale + tech + specialist teams

Geopolitical sanctions, DORA and Pillar Two squeeze $15T custody model

Northern Trusts NII and securities‑lending are highly rate‑sensitive; Fed funds 5.25–5.50% (Jul 2025) and a -40bps 2s10s compress margins and raise deposit betas. Fee revenue tracks markets—equity/fixed income swings drove AUM‑linked fees; passive AUM > $13T (end‑2024) pressures active fees. Inflation (~3.4% CPI 2024) lifts wage/tech costs, raising efficiency demands.

| Metric | Value |

|---|---|

| Fed funds (Jul 2025) | 5.25–5.50% |

| 2s10s | -40 bps |

| US CPI (2024) | ~3.4% |

| Passive AUM (end‑2024) | > $13T |

Same Document Delivered

Northern Trust PESTLE Analysis

The preview shown here is the exact Northern Trust PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This screenshot reflects the real product with no placeholders or teasers. After payment you’ll instantly download the same complete file. What you see is what you’ll be working with.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological change are reshaping Northern Trust’s competitive landscape in our concise PESTLE snapshot. This analysis highlights regulatory risks, ESG pressures, and market opportunities you need to know. Buy the full PESTLE to get the complete, actionable briefing for investment and strategy decisions.

Political factors

Geopolitical tensions and sanctions

Heightened geopolitical risk and evolving sanctions regimes increase complexity for Northern Trust's cross-border custody, payments and asset servicing, forcing continuous client and transaction screening, re-mapping of operating processes and investment guideline adjustments. Rapid sanctions updates — over 500 major listings in 2023–24 — raise operational complexity and legal exposure. Diversification of booking centers and contingency plans mitigate disruption to its roughly $15 trillion custody footprint.

Regulatory policymaking and oversight

Policy priorities of US, UK, EU and APAC authorities drive capital, liquidity and conduct standards across custody and asset management. Basel III endgame implementation continues across jurisdictions through 2023–2028, changing capital metrics. Supervisory focus on operational resilience and third‑party risk, highlighted by EU DORA effective 17 January 2025, raises compliance costs. Regulatory engagement shapes approvals for new services and can reprice fee models.

Tax policy and cross-border treaties

Changes in corporate, withholding, and wealth taxes shift client behavior and asset location, pressuring custodians to adapt servicing models and client reporting. OECD Pillar Two's 15% global minimum tax, adopted by about 137 jurisdictions, is already reshaping fund domiciles and cross-border flows. Northern Trust must keep tax-operational expertise to prevent leakage and errors in withholding and reporting. Political debates on wealth taxation can materially affect demand for trust and estate services.

Trade policy and market access

Tariffs, localization rules and market-access restrictions force custodians to reconfigure global operating models and redeploy staff and systems across jurisdictions.

Post-Brexit divergence necessitates parallel UK/EU capabilities for custody, tax and compliance flows; local data and outsourcing rules determine where services are booked and processed.

- Political shifts can affect sovereign/public mandates — sovereign wealth funds ≈$10.6 trillion (SWF Institute 2024)

- Increased compliance costs per jurisdiction

Public-sector investment priorities

Government agendas on infrastructure (US IIJA $1.2 trillion) and rising pension/healthcare liabilities drive institutional asset growth, creating demand for custody, fiduciary and liability-driven investment solutions; sovereign and public fund mandates hinge on policy stability and governance norms. Northern Trust can capture flows from public-private partnerships and pension reform, though political turnover can rapidly alter mandate criteria and allocations.

- IIJA $1.2T

- Global pension assets ~57T (2023)

- Sovereign wealth funds ≈$10.8T (2024)

- PPP and pension reform = client flows

Geopolitical sanctions, DORA and Pillar Two squeeze $15T custody model

Heightened geopolitical risk and sanctions (500+ listings 2023–24) raise custody, payments and compliance complexity for Northern Trust's ~$15T custody footprint, forcing booking diversification and continuous screening. Basel III endgame and DORA (effective 17 Jan 2025) increase capital and resilience costs. OECD Pillar Two (15%, ~137 jurisdictions) reshapes domiciles and reporting.

| Metric | Value |

|---|---|

| Custody AUA | $15T |

| Sanctions 2023–24 | 500+ |

| Pillar Two | 15% / ~137 jurisdictions |

| DORA effective | 17 Jan 2025 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Northern Trust, combining current data and trends to identify risks, opportunities and strategic implications. Delivered as actionable, forward‑looking insights formatted for reports, decks and scenario planning.

A concise, visually segmented PESTLE summary of Northern Trust that can be dropped into presentations, edited with region- or business‑line notes, and easily shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rates and yield curve

Northern Trusts net interest income and securities lending revenues are highly rate-sensitive; with the Fed funds target at 5.25–5.50% (July 2025) and the 2s10s roughly -40 bps, curve shape materially affects reinvestment yields. Steeper, stable curves lower deposit betas while inversions push betas toward 30–40% and compress margins. Rapid central bank pivots have reduced client cash balances and squeezed NII in past quarters. Active hedging and product-mix shifts remain critical to protect spreads.

Market levels and AUM/AUC volatility

Fee revenues at Northern Trust track equity and fixed‑income valuations; global equities fell ~20% in 2022 then rose ~25% in 2023, driving AUM-linked fees and servicing swings. Prolonged drawdowns in 2022 cut performance fees and transaction volumes, while rebalancing and flight‑to‑quality shifted client demand toward cash and government bonds. Operating leverage magnifies these revenue cycles for custody and asset servicing margins.

Inflation and expense dynamics

Rising inflation (US CPI ~3.4% in 2024) pushed salary growth near 4% and lifted technology and vendor contract costs, pressuring Northern Trusts efficiency metrics. Clients reallocated toward inflation-hedging assets like TIPS and commodities, changing custody and advisory servicing mixes. Real-return mandates tightened benchmarks and fee terms. Pricing discipline and accelerated automation reduced projected cost creep.

FX volatility and global flows

Currency swings affect translated revenues and client hedging demand, with global FX turnover at about 7.5 trillion USD daily per the BIS triennial survey (2022), boosting cross-border custody and collateral flows while increasing basis risk and margin calls that elevate operational and credit exposures; natural hedges and treasury strategies reduce earnings variability.

- FX turnover: 7.5T USD/day (BIS 2022)

- Higher hedging demand

- More custody/collateral activity

- Increased basis risk & margin calls

- Treasury/natural hedges mitigate earnings swings

Fee compression and competition

Indexing and passive adoption have pushed global ETF/AUM past $13 trillion by end-2024, compressing asset management fees and driving margin pressure on active mandates.

Asset servicers face price erosion on commoditized custody and administration functions, while value shifts to data, analytics, alternatives and outsourced middle-office solutions.

Differentiation now depends on scale, advanced technology and specialized expertise to capture higher-margin services.

- Passive AUM > $13T (end-2024)

- Fee compression hits core custody/admin

- Growth areas: data, analytics, alternatives, OMNI (outsourced middle office)

- Competitive edge: scale + tech + specialist teams

Geopolitical sanctions, DORA and Pillar Two squeeze $15T custody model

Northern Trusts NII and securities‑lending are highly rate‑sensitive; Fed funds 5.25–5.50% (Jul 2025) and a -40bps 2s10s compress margins and raise deposit betas. Fee revenue tracks markets—equity/fixed income swings drove AUM‑linked fees; passive AUM > $13T (end‑2024) pressures active fees. Inflation (~3.4% CPI 2024) lifts wage/tech costs, raising efficiency demands.

| Metric | Value |

|---|---|

| Fed funds (Jul 2025) | 5.25–5.50% |

| 2s10s | -40 bps |

| US CPI (2024) | ~3.4% |

| Passive AUM (end‑2024) | > $13T |

Same Document Delivered

Northern Trust PESTLE Analysis

The preview shown here is the exact Northern Trust PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This screenshot reflects the real product with no placeholders or teasers. After payment you’ll instantly download the same complete file. What you see is what you’ll be working with.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and technological change are reshaping Northern Trust’s competitive landscape in our concise PESTLE snapshot. This analysis highlights regulatory risks, ESG pressures, and market opportunities you need to know. Buy the full PESTLE to get the complete, actionable briefing for investment and strategy decisions.

Political factors

Geopolitical tensions and sanctions

Heightened geopolitical risk and evolving sanctions regimes increase complexity for Northern Trust's cross-border custody, payments and asset servicing, forcing continuous client and transaction screening, re-mapping of operating processes and investment guideline adjustments. Rapid sanctions updates — over 500 major listings in 2023–24 — raise operational complexity and legal exposure. Diversification of booking centers and contingency plans mitigate disruption to its roughly $15 trillion custody footprint.

Regulatory policymaking and oversight

Policy priorities of US, UK, EU and APAC authorities drive capital, liquidity and conduct standards across custody and asset management. Basel III endgame implementation continues across jurisdictions through 2023–2028, changing capital metrics. Supervisory focus on operational resilience and third‑party risk, highlighted by EU DORA effective 17 January 2025, raises compliance costs. Regulatory engagement shapes approvals for new services and can reprice fee models.

Tax policy and cross-border treaties

Changes in corporate, withholding, and wealth taxes shift client behavior and asset location, pressuring custodians to adapt servicing models and client reporting. OECD Pillar Two's 15% global minimum tax, adopted by about 137 jurisdictions, is already reshaping fund domiciles and cross-border flows. Northern Trust must keep tax-operational expertise to prevent leakage and errors in withholding and reporting. Political debates on wealth taxation can materially affect demand for trust and estate services.

Trade policy and market access

Tariffs, localization rules and market-access restrictions force custodians to reconfigure global operating models and redeploy staff and systems across jurisdictions.

Post-Brexit divergence necessitates parallel UK/EU capabilities for custody, tax and compliance flows; local data and outsourcing rules determine where services are booked and processed.

- Political shifts can affect sovereign/public mandates — sovereign wealth funds ≈$10.6 trillion (SWF Institute 2024)

- Increased compliance costs per jurisdiction

Public-sector investment priorities

Government agendas on infrastructure (US IIJA $1.2 trillion) and rising pension/healthcare liabilities drive institutional asset growth, creating demand for custody, fiduciary and liability-driven investment solutions; sovereign and public fund mandates hinge on policy stability and governance norms. Northern Trust can capture flows from public-private partnerships and pension reform, though political turnover can rapidly alter mandate criteria and allocations.

- IIJA $1.2T

- Global pension assets ~57T (2023)

- Sovereign wealth funds ≈$10.8T (2024)

- PPP and pension reform = client flows

Geopolitical sanctions, DORA and Pillar Two squeeze $15T custody model

Heightened geopolitical risk and sanctions (500+ listings 2023–24) raise custody, payments and compliance complexity for Northern Trust's ~$15T custody footprint, forcing booking diversification and continuous screening. Basel III endgame and DORA (effective 17 Jan 2025) increase capital and resilience costs. OECD Pillar Two (15%, ~137 jurisdictions) reshapes domiciles and reporting.

| Metric | Value |

|---|---|

| Custody AUA | $15T |

| Sanctions 2023–24 | 500+ |

| Pillar Two | 15% / ~137 jurisdictions |

| DORA effective | 17 Jan 2025 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Northern Trust, combining current data and trends to identify risks, opportunities and strategic implications. Delivered as actionable, forward‑looking insights formatted for reports, decks and scenario planning.

A concise, visually segmented PESTLE summary of Northern Trust that can be dropped into presentations, edited with region- or business‑line notes, and easily shared across teams to streamline external risk discussions and strategic planning.

Economic factors

Interest rates and yield curve

Northern Trusts net interest income and securities lending revenues are highly rate-sensitive; with the Fed funds target at 5.25–5.50% (July 2025) and the 2s10s roughly -40 bps, curve shape materially affects reinvestment yields. Steeper, stable curves lower deposit betas while inversions push betas toward 30–40% and compress margins. Rapid central bank pivots have reduced client cash balances and squeezed NII in past quarters. Active hedging and product-mix shifts remain critical to protect spreads.

Market levels and AUM/AUC volatility

Fee revenues at Northern Trust track equity and fixed‑income valuations; global equities fell ~20% in 2022 then rose ~25% in 2023, driving AUM-linked fees and servicing swings. Prolonged drawdowns in 2022 cut performance fees and transaction volumes, while rebalancing and flight‑to‑quality shifted client demand toward cash and government bonds. Operating leverage magnifies these revenue cycles for custody and asset servicing margins.

Inflation and expense dynamics

Rising inflation (US CPI ~3.4% in 2024) pushed salary growth near 4% and lifted technology and vendor contract costs, pressuring Northern Trusts efficiency metrics. Clients reallocated toward inflation-hedging assets like TIPS and commodities, changing custody and advisory servicing mixes. Real-return mandates tightened benchmarks and fee terms. Pricing discipline and accelerated automation reduced projected cost creep.

FX volatility and global flows

Currency swings affect translated revenues and client hedging demand, with global FX turnover at about 7.5 trillion USD daily per the BIS triennial survey (2022), boosting cross-border custody and collateral flows while increasing basis risk and margin calls that elevate operational and credit exposures; natural hedges and treasury strategies reduce earnings variability.

- FX turnover: 7.5T USD/day (BIS 2022)

- Higher hedging demand

- More custody/collateral activity

- Increased basis risk & margin calls

- Treasury/natural hedges mitigate earnings swings

Fee compression and competition

Indexing and passive adoption have pushed global ETF/AUM past $13 trillion by end-2024, compressing asset management fees and driving margin pressure on active mandates.

Asset servicers face price erosion on commoditized custody and administration functions, while value shifts to data, analytics, alternatives and outsourced middle-office solutions.

Differentiation now depends on scale, advanced technology and specialized expertise to capture higher-margin services.

- Passive AUM > $13T (end-2024)

- Fee compression hits core custody/admin

- Growth areas: data, analytics, alternatives, OMNI (outsourced middle office)

- Competitive edge: scale + tech + specialist teams

Geopolitical sanctions, DORA and Pillar Two squeeze $15T custody model

Northern Trusts NII and securities‑lending are highly rate‑sensitive; Fed funds 5.25–5.50% (Jul 2025) and a -40bps 2s10s compress margins and raise deposit betas. Fee revenue tracks markets—equity/fixed income swings drove AUM‑linked fees; passive AUM > $13T (end‑2024) pressures active fees. Inflation (~3.4% CPI 2024) lifts wage/tech costs, raising efficiency demands.

| Metric | Value |

|---|---|

| Fed funds (Jul 2025) | 5.25–5.50% |

| 2s10s | -40 bps |

| US CPI (2024) | ~3.4% |

| Passive AUM (end‑2024) | > $13T |

Same Document Delivered

Northern Trust PESTLE Analysis

The preview shown here is the exact Northern Trust PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This screenshot reflects the real product with no placeholders or teasers. After payment you’ll instantly download the same complete file. What you see is what you’ll be working with.