NRG Energy PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of NRG Energy reveals how political regulation, economic cycles, technological transitions, and environmental pressures converge to reshape its strategy and risk profile. Clear insights on regulatory and social trends highlight critical decision points for investors and managers. Whether preparing investment cases or strategic plans, this concise briefing points to where deeper intelligence matters. Purchase the full report to access the complete, actionable breakdown.

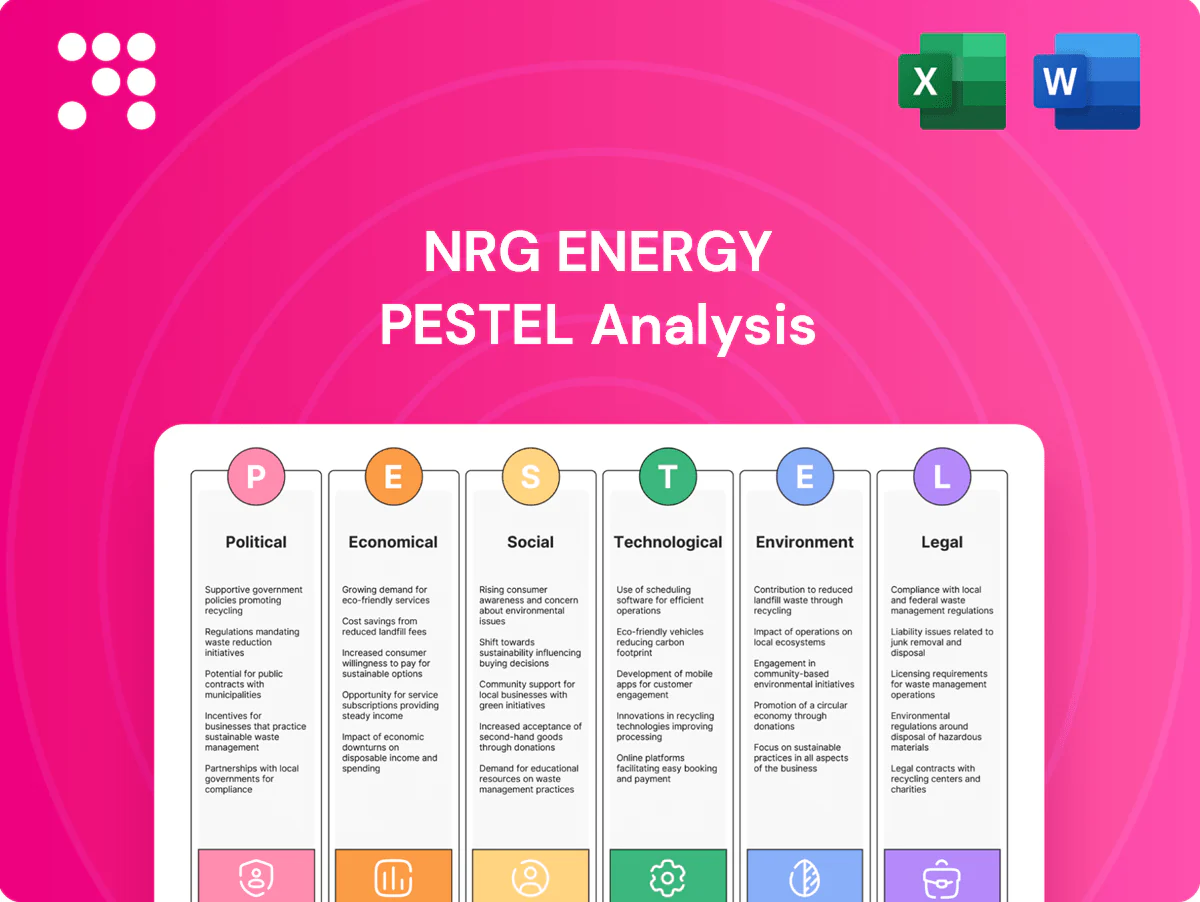

Political factors

Shifting U.S. energy policy and decarbonization agendas

Federal and state priorities — notably the Inflation Reduction Act of 2022 and the Biden goal of 100% clean electricity by 2035 — shift fuel mix, drive plant retirements and unlock tax credits for renewables and storage. Policy swings can rapidly accelerate renewables/storage deployment or revalue dispatchable thermal capacity. With renewables at roughly 22% of US generation in 2023 (EIA), NRG must stay agile across election cycles to capture credits while managing stranded-asset risk and engage to shape market rules and reliability standards.

State-by-state market fragmentation

NRG must navigate a patchwork of regulated and deregulated states where pricing, tariffs and oversight vary widely, from retail competition to utility-led rates. ERCOT, which covers roughly 90% of Texas load, contrasts with Northeast ISOs (PJM supplies about 65 million people, ISO‑NE about 14 million) and vertically regulated markets, requiring tailored commercial and regulatory strategies. Portfolio optimization hinges on disparate capacity markets and retail rules across regions. State political shifts—legislation, regulator changes or subsidy moves—can rapidly alter project economics and competitive dynamics.

Incentives and subsidies for clean energy

Tax credits and grants such as the Inflation Reduction Act’s 30% ITC for standalone storage and the option of 10-year PTC/ITC for renewables can materially boost returns on NRG’s renewables, storage and demand-side investments. Accessing these incentives lowers effective capex, reduces cost of capital and accelerates deployment timelines. Shifts in program design—domestic content and wage rules—require proactive structuring. Competition for finite incentive pools compresses timelines and strains supply chains.

Grid reliability as a political priority

Outages and extreme weather have pushed grid reliability into a policy imperative; NERCs 2024 Long-Term Reliability Assessment flagged heightened resource adequacy risks in parts of the Western Interconnection and Rockies, prompting regulators to consider mandated reserve margins, winterization, and performance standards that raise compliance costs but favor reliable assets and retail offerings.

- Regulatory tools: reserve margins, winterization, performance standards

- Cost impact: higher capex/O&M vs premium for reliable assets

- Political focus: resource adequacy, consumer protection (NERC 2024)

Trade policies and supply security

Tariffs on solar modules, batteries and a 25% Section 232 steel tariff raise project costs and can delay timelines; AD/CVD actions and supply-chain scrutiny increase price volatility. Buy American and the IRA domestic-content bonus (up to 10 percentage points) reshape procurement, while geopolitical tensions (China, Red Sea) risk equipment availability. NRG must diversify suppliers and scale domestic alternatives to reduce shocks.

- 25% steel tariff increases capex and lead times

- IRA domestic-content bonus up to 10pp shifts sourcing

- Geopolitical risks create intermittent supply disruptions

- Recommendation: diversify suppliers, expand U.S. procurement

NERC warnings and IRA push utilities to renewables/storage; 30% ITC, 25% tariff

Federal/state policy (IRA: 30% standalone storage ITC; 10-yr PTC/ITC option) and NERC 2024 reliability warnings push NRG toward renewables/storage while raising stranded-asset risk for thermal plants; regional markets (ERCOT ~90% TX load; PJM ~65M; ISO‑NE ~14M) require tailored strategies. 25% steel tariff and IRA domestic-content bonus up to 10pp increase capex and sourcing shifts.

| Metric | Value | Impact |

|---|---|---|

| US renewables share (2023) | ~22% | Growth opportunity |

| Storage ITC | 30% | Lowers effective capex |

| Steel tariff | 25% | Raises capex |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect NRG Energy, using data-driven trends and regional regulatory context to identify risks, opportunities, and forward-looking scenarios for executives and investors.

A clean, summarized PESTLE of NRG Energy, visually segmented for quick interpretation and easy insertion into presentations, helping teams align rapidly on external risks and market positioning during planning sessions.

Economic factors

Commodity price volatility (gas, power)

Power margins hinge on spark spreads and basis dynamics, with extreme wholesale caps like ERCOT’s $9,000/MWh shaping upside risk for generators.

Gas price swings—against a backdrop of US LNG exports near 12.5 Bcf/d in 2024—drive dispatch patterns, hedge demand and retail rate adjustments.

Volatility offers trading opportunities but raises counterparty risk and collateral needs, so robust risk management and customer pass-through mechanisms are critical.

Interest rates and cost of capital

Higher benchmark rates (Fed funds 5.25–5.50% and 10-year Treasury ~4.3% in 2024) squeeze project IRRs and retail working capital, intensifying financing costs for NRG’s capital-intensive generation and customer-acquisition spend. Disciplined financing matters as NRG carries substantial project capex needs while S&P rates NRG BB- and the company reported liquidity around $2.5 billion, supporting resilience. Lower rates would revive refinancing and growth capex options by reducing weighted average cost of capital.

Retail competition and customer churn

Retail competition compresses margins and raises customer acquisition costs for NRG, forcing tighter pricing and higher marketing spend. Product differentiation through fixed-rate contracts, green plans and bundled home services improves retention and reduces churn. Pricing power hinges on brand trust and service reliability, while analytics-driven segmentation can lift customer lifetime value by targeting high-margin cohorts.

Load growth from electrification

- EVs: 26 million global EVs (IEA, 2023)

- Data centers: ~2% of U.S. electricity

- Strategy: flexible generation, DR, bundled retail offerings

Supply chain and labor costs

Equipment, construction, and O&M inflation pressured project economics, with sector input costs up about 7% year-over-year in 2024, compressing margins on new builds and retrofits. Skilled labor scarcity lengthened timelines and pushed construction wages roughly 4–5% higher in 2024, increasing capex and financing needs. NRG mitigates via long-term contracts, standardization, strategic inventory and vendor partnerships to limit disruptions and lock input pricing.

- Equipment inflation ~7% (2024)

- Wage growth 4–5% (2024)

- Long-term contracts = cost visibility

- Inventory & vendor partnerships reduce delay risk

NERC warnings and IRA push utilities to renewables/storage; 30% ITC, 25% tariff

Power margins depend on spark spreads and extreme caps (ERCOT $9,000/MWh) plus gas-driven dispatch as U.S. LNG ~12.5 Bcf/d (2024).

Higher rates (Fed funds 5.25–5.50%, 10yr ~4.3% in 2024) raise WACC, pressuring IRRs; NRG liquidity ~ $2.5B, S&P BB-.

Electrification (26M EVs 2023; data centers ~2% US load) boosts demand, favoring flexible generation and retail bundles.

| Metric | Value |

|---|---|

| U.S. LNG exports (2024) | ~12.5 Bcf/d |

| Fed funds (2024) | 5.25–5.50% |

| 10‑yr Treasury (2024) | ~4.3% |

| NRG liquidity | ~$2.5B |

| S&P rating | BB- |

| Global EVs (2023) | 26M |

| Equipment inflation (2024) | ~7% |

Same Document Delivered

NRG Energy PESTLE Analysis

The NRG Energy PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with complete political, economic, social, technological, legal, and environmental insights specific to NRG Energy, not a teaser or placeholder. After checkout you’ll instantly download the exact same document displayed here.

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of NRG Energy reveals how political regulation, economic cycles, technological transitions, and environmental pressures converge to reshape its strategy and risk profile. Clear insights on regulatory and social trends highlight critical decision points for investors and managers. Whether preparing investment cases or strategic plans, this concise briefing points to where deeper intelligence matters. Purchase the full report to access the complete, actionable breakdown.

Political factors

Shifting U.S. energy policy and decarbonization agendas

Federal and state priorities — notably the Inflation Reduction Act of 2022 and the Biden goal of 100% clean electricity by 2035 — shift fuel mix, drive plant retirements and unlock tax credits for renewables and storage. Policy swings can rapidly accelerate renewables/storage deployment or revalue dispatchable thermal capacity. With renewables at roughly 22% of US generation in 2023 (EIA), NRG must stay agile across election cycles to capture credits while managing stranded-asset risk and engage to shape market rules and reliability standards.

State-by-state market fragmentation

NRG must navigate a patchwork of regulated and deregulated states where pricing, tariffs and oversight vary widely, from retail competition to utility-led rates. ERCOT, which covers roughly 90% of Texas load, contrasts with Northeast ISOs (PJM supplies about 65 million people, ISO‑NE about 14 million) and vertically regulated markets, requiring tailored commercial and regulatory strategies. Portfolio optimization hinges on disparate capacity markets and retail rules across regions. State political shifts—legislation, regulator changes or subsidy moves—can rapidly alter project economics and competitive dynamics.

Incentives and subsidies for clean energy

Tax credits and grants such as the Inflation Reduction Act’s 30% ITC for standalone storage and the option of 10-year PTC/ITC for renewables can materially boost returns on NRG’s renewables, storage and demand-side investments. Accessing these incentives lowers effective capex, reduces cost of capital and accelerates deployment timelines. Shifts in program design—domestic content and wage rules—require proactive structuring. Competition for finite incentive pools compresses timelines and strains supply chains.

Grid reliability as a political priority

Outages and extreme weather have pushed grid reliability into a policy imperative; NERCs 2024 Long-Term Reliability Assessment flagged heightened resource adequacy risks in parts of the Western Interconnection and Rockies, prompting regulators to consider mandated reserve margins, winterization, and performance standards that raise compliance costs but favor reliable assets and retail offerings.

- Regulatory tools: reserve margins, winterization, performance standards

- Cost impact: higher capex/O&M vs premium for reliable assets

- Political focus: resource adequacy, consumer protection (NERC 2024)

Trade policies and supply security

Tariffs on solar modules, batteries and a 25% Section 232 steel tariff raise project costs and can delay timelines; AD/CVD actions and supply-chain scrutiny increase price volatility. Buy American and the IRA domestic-content bonus (up to 10 percentage points) reshape procurement, while geopolitical tensions (China, Red Sea) risk equipment availability. NRG must diversify suppliers and scale domestic alternatives to reduce shocks.

- 25% steel tariff increases capex and lead times

- IRA domestic-content bonus up to 10pp shifts sourcing

- Geopolitical risks create intermittent supply disruptions

- Recommendation: diversify suppliers, expand U.S. procurement

NERC warnings and IRA push utilities to renewables/storage; 30% ITC, 25% tariff

Federal/state policy (IRA: 30% standalone storage ITC; 10-yr PTC/ITC option) and NERC 2024 reliability warnings push NRG toward renewables/storage while raising stranded-asset risk for thermal plants; regional markets (ERCOT ~90% TX load; PJM ~65M; ISO‑NE ~14M) require tailored strategies. 25% steel tariff and IRA domestic-content bonus up to 10pp increase capex and sourcing shifts.

| Metric | Value | Impact |

|---|---|---|

| US renewables share (2023) | ~22% | Growth opportunity |

| Storage ITC | 30% | Lowers effective capex |

| Steel tariff | 25% | Raises capex |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect NRG Energy, using data-driven trends and regional regulatory context to identify risks, opportunities, and forward-looking scenarios for executives and investors.

A clean, summarized PESTLE of NRG Energy, visually segmented for quick interpretation and easy insertion into presentations, helping teams align rapidly on external risks and market positioning during planning sessions.

Economic factors

Commodity price volatility (gas, power)

Power margins hinge on spark spreads and basis dynamics, with extreme wholesale caps like ERCOT’s $9,000/MWh shaping upside risk for generators.

Gas price swings—against a backdrop of US LNG exports near 12.5 Bcf/d in 2024—drive dispatch patterns, hedge demand and retail rate adjustments.

Volatility offers trading opportunities but raises counterparty risk and collateral needs, so robust risk management and customer pass-through mechanisms are critical.

Interest rates and cost of capital

Higher benchmark rates (Fed funds 5.25–5.50% and 10-year Treasury ~4.3% in 2024) squeeze project IRRs and retail working capital, intensifying financing costs for NRG’s capital-intensive generation and customer-acquisition spend. Disciplined financing matters as NRG carries substantial project capex needs while S&P rates NRG BB- and the company reported liquidity around $2.5 billion, supporting resilience. Lower rates would revive refinancing and growth capex options by reducing weighted average cost of capital.

Retail competition and customer churn

Retail competition compresses margins and raises customer acquisition costs for NRG, forcing tighter pricing and higher marketing spend. Product differentiation through fixed-rate contracts, green plans and bundled home services improves retention and reduces churn. Pricing power hinges on brand trust and service reliability, while analytics-driven segmentation can lift customer lifetime value by targeting high-margin cohorts.

Load growth from electrification

- EVs: 26 million global EVs (IEA, 2023)

- Data centers: ~2% of U.S. electricity

- Strategy: flexible generation, DR, bundled retail offerings

Supply chain and labor costs

Equipment, construction, and O&M inflation pressured project economics, with sector input costs up about 7% year-over-year in 2024, compressing margins on new builds and retrofits. Skilled labor scarcity lengthened timelines and pushed construction wages roughly 4–5% higher in 2024, increasing capex and financing needs. NRG mitigates via long-term contracts, standardization, strategic inventory and vendor partnerships to limit disruptions and lock input pricing.

- Equipment inflation ~7% (2024)

- Wage growth 4–5% (2024)

- Long-term contracts = cost visibility

- Inventory & vendor partnerships reduce delay risk

NERC warnings and IRA push utilities to renewables/storage; 30% ITC, 25% tariff

Power margins depend on spark spreads and extreme caps (ERCOT $9,000/MWh) plus gas-driven dispatch as U.S. LNG ~12.5 Bcf/d (2024).

Higher rates (Fed funds 5.25–5.50%, 10yr ~4.3% in 2024) raise WACC, pressuring IRRs; NRG liquidity ~ $2.5B, S&P BB-.

Electrification (26M EVs 2023; data centers ~2% US load) boosts demand, favoring flexible generation and retail bundles.

| Metric | Value |

|---|---|

| U.S. LNG exports (2024) | ~12.5 Bcf/d |

| Fed funds (2024) | 5.25–5.50% |

| 10‑yr Treasury (2024) | ~4.3% |

| NRG liquidity | ~$2.5B |

| S&P rating | BB- |

| Global EVs (2023) | 26M |

| Equipment inflation (2024) | ~7% |

Same Document Delivered

NRG Energy PESTLE Analysis

The NRG Energy PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with complete political, economic, social, technological, legal, and environmental insights specific to NRG Energy, not a teaser or placeholder. After checkout you’ll instantly download the exact same document displayed here.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of NRG Energy reveals how political regulation, economic cycles, technological transitions, and environmental pressures converge to reshape its strategy and risk profile. Clear insights on regulatory and social trends highlight critical decision points for investors and managers. Whether preparing investment cases or strategic plans, this concise briefing points to where deeper intelligence matters. Purchase the full report to access the complete, actionable breakdown.

Political factors

Shifting U.S. energy policy and decarbonization agendas

Federal and state priorities — notably the Inflation Reduction Act of 2022 and the Biden goal of 100% clean electricity by 2035 — shift fuel mix, drive plant retirements and unlock tax credits for renewables and storage. Policy swings can rapidly accelerate renewables/storage deployment or revalue dispatchable thermal capacity. With renewables at roughly 22% of US generation in 2023 (EIA), NRG must stay agile across election cycles to capture credits while managing stranded-asset risk and engage to shape market rules and reliability standards.

State-by-state market fragmentation

NRG must navigate a patchwork of regulated and deregulated states where pricing, tariffs and oversight vary widely, from retail competition to utility-led rates. ERCOT, which covers roughly 90% of Texas load, contrasts with Northeast ISOs (PJM supplies about 65 million people, ISO‑NE about 14 million) and vertically regulated markets, requiring tailored commercial and regulatory strategies. Portfolio optimization hinges on disparate capacity markets and retail rules across regions. State political shifts—legislation, regulator changes or subsidy moves—can rapidly alter project economics and competitive dynamics.

Incentives and subsidies for clean energy

Tax credits and grants such as the Inflation Reduction Act’s 30% ITC for standalone storage and the option of 10-year PTC/ITC for renewables can materially boost returns on NRG’s renewables, storage and demand-side investments. Accessing these incentives lowers effective capex, reduces cost of capital and accelerates deployment timelines. Shifts in program design—domestic content and wage rules—require proactive structuring. Competition for finite incentive pools compresses timelines and strains supply chains.

Grid reliability as a political priority

Outages and extreme weather have pushed grid reliability into a policy imperative; NERCs 2024 Long-Term Reliability Assessment flagged heightened resource adequacy risks in parts of the Western Interconnection and Rockies, prompting regulators to consider mandated reserve margins, winterization, and performance standards that raise compliance costs but favor reliable assets and retail offerings.

- Regulatory tools: reserve margins, winterization, performance standards

- Cost impact: higher capex/O&M vs premium for reliable assets

- Political focus: resource adequacy, consumer protection (NERC 2024)

Trade policies and supply security

Tariffs on solar modules, batteries and a 25% Section 232 steel tariff raise project costs and can delay timelines; AD/CVD actions and supply-chain scrutiny increase price volatility. Buy American and the IRA domestic-content bonus (up to 10 percentage points) reshape procurement, while geopolitical tensions (China, Red Sea) risk equipment availability. NRG must diversify suppliers and scale domestic alternatives to reduce shocks.

- 25% steel tariff increases capex and lead times

- IRA domestic-content bonus up to 10pp shifts sourcing

- Geopolitical risks create intermittent supply disruptions

- Recommendation: diversify suppliers, expand U.S. procurement

NERC warnings and IRA push utilities to renewables/storage; 30% ITC, 25% tariff

Federal/state policy (IRA: 30% standalone storage ITC; 10-yr PTC/ITC option) and NERC 2024 reliability warnings push NRG toward renewables/storage while raising stranded-asset risk for thermal plants; regional markets (ERCOT ~90% TX load; PJM ~65M; ISO‑NE ~14M) require tailored strategies. 25% steel tariff and IRA domestic-content bonus up to 10pp increase capex and sourcing shifts.

| Metric | Value | Impact |

|---|---|---|

| US renewables share (2023) | ~22% | Growth opportunity |

| Storage ITC | 30% | Lowers effective capex |

| Steel tariff | 25% | Raises capex |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely affect NRG Energy, using data-driven trends and regional regulatory context to identify risks, opportunities, and forward-looking scenarios for executives and investors.

A clean, summarized PESTLE of NRG Energy, visually segmented for quick interpretation and easy insertion into presentations, helping teams align rapidly on external risks and market positioning during planning sessions.

Economic factors

Commodity price volatility (gas, power)

Power margins hinge on spark spreads and basis dynamics, with extreme wholesale caps like ERCOT’s $9,000/MWh shaping upside risk for generators.

Gas price swings—against a backdrop of US LNG exports near 12.5 Bcf/d in 2024—drive dispatch patterns, hedge demand and retail rate adjustments.

Volatility offers trading opportunities but raises counterparty risk and collateral needs, so robust risk management and customer pass-through mechanisms are critical.

Interest rates and cost of capital

Higher benchmark rates (Fed funds 5.25–5.50% and 10-year Treasury ~4.3% in 2024) squeeze project IRRs and retail working capital, intensifying financing costs for NRG’s capital-intensive generation and customer-acquisition spend. Disciplined financing matters as NRG carries substantial project capex needs while S&P rates NRG BB- and the company reported liquidity around $2.5 billion, supporting resilience. Lower rates would revive refinancing and growth capex options by reducing weighted average cost of capital.

Retail competition and customer churn

Retail competition compresses margins and raises customer acquisition costs for NRG, forcing tighter pricing and higher marketing spend. Product differentiation through fixed-rate contracts, green plans and bundled home services improves retention and reduces churn. Pricing power hinges on brand trust and service reliability, while analytics-driven segmentation can lift customer lifetime value by targeting high-margin cohorts.

Load growth from electrification

- EVs: 26 million global EVs (IEA, 2023)

- Data centers: ~2% of U.S. electricity

- Strategy: flexible generation, DR, bundled retail offerings

Supply chain and labor costs

Equipment, construction, and O&M inflation pressured project economics, with sector input costs up about 7% year-over-year in 2024, compressing margins on new builds and retrofits. Skilled labor scarcity lengthened timelines and pushed construction wages roughly 4–5% higher in 2024, increasing capex and financing needs. NRG mitigates via long-term contracts, standardization, strategic inventory and vendor partnerships to limit disruptions and lock input pricing.

- Equipment inflation ~7% (2024)

- Wage growth 4–5% (2024)

- Long-term contracts = cost visibility

- Inventory & vendor partnerships reduce delay risk

NERC warnings and IRA push utilities to renewables/storage; 30% ITC, 25% tariff

Power margins depend on spark spreads and extreme caps (ERCOT $9,000/MWh) plus gas-driven dispatch as U.S. LNG ~12.5 Bcf/d (2024).

Higher rates (Fed funds 5.25–5.50%, 10yr ~4.3% in 2024) raise WACC, pressuring IRRs; NRG liquidity ~ $2.5B, S&P BB-.

Electrification (26M EVs 2023; data centers ~2% US load) boosts demand, favoring flexible generation and retail bundles.

| Metric | Value |

|---|---|

| U.S. LNG exports (2024) | ~12.5 Bcf/d |

| Fed funds (2024) | 5.25–5.50% |

| 10‑yr Treasury (2024) | ~4.3% |

| NRG liquidity | ~$2.5B |

| S&P rating | BB- |

| Global EVs (2023) | 26M |

| Equipment inflation (2024) | ~7% |

Same Document Delivered

NRG Energy PESTLE Analysis

The NRG Energy PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is the real file with complete political, economic, social, technological, legal, and environmental insights specific to NRG Energy, not a teaser or placeholder. After checkout you’ll instantly download the exact same document displayed here.