NSD Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

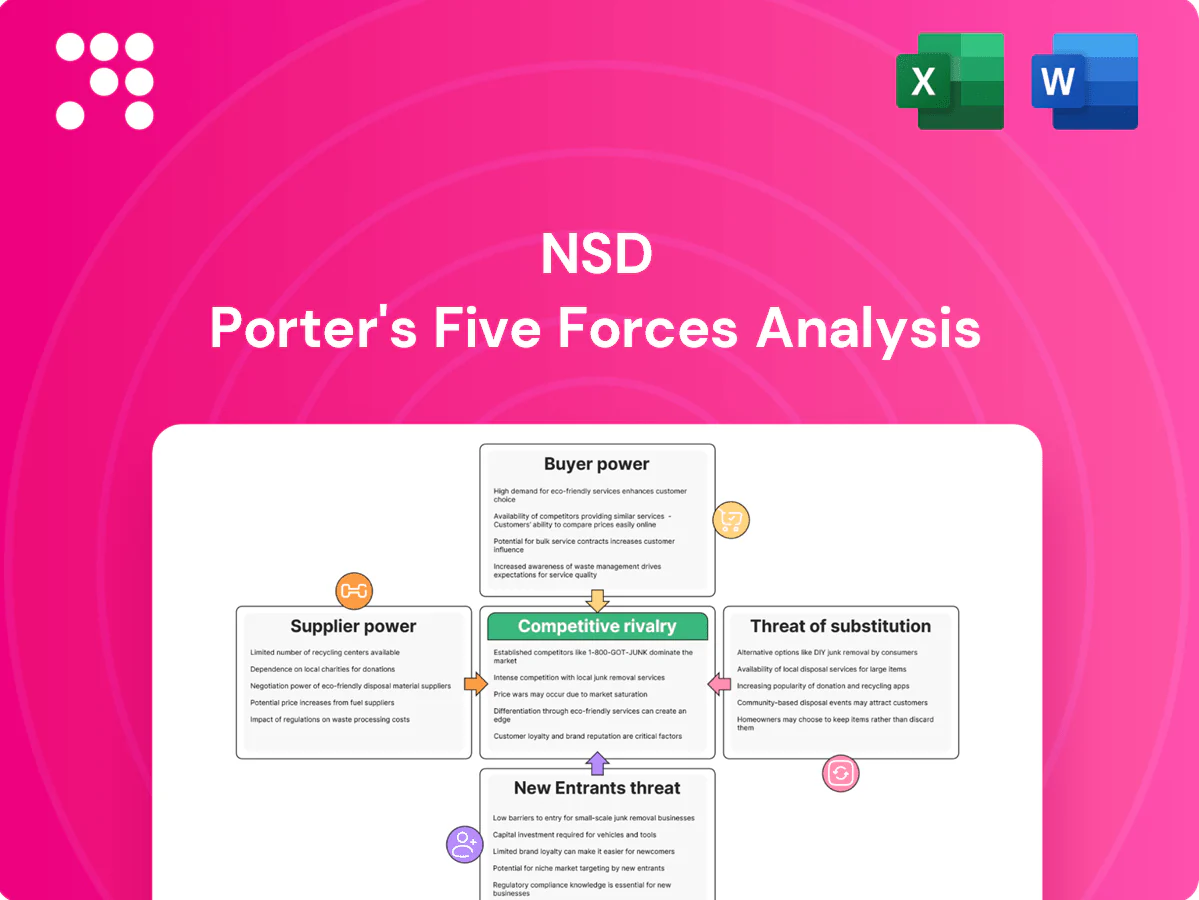

NSD’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of substitutes, and barriers to entry—key inputs for strategic planning and valuation. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for confident decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

NSD depends on a concentrated set of hyperscalers, database, middleware and cybersecurity vendors; in 2024 the top three hyperscalers held ~66% of the cloud IaaS/PaaS market (AWS 32%, Azure 23%, GCP 11%), amplifying switching costs and lock‑in via 3–5 year maintenance/contracts. Certification and proprietary stacks shift pricing power to suppliers, while multi‑vendor strategies and open‑source adoption can materially reduce dependency.

Specialized talent scarcity

Highly skilled engineers, cloud architects, and cybersecurity specialists are scarce, with ISC2 reporting a 2024 global cybersecurity workforce gap of about 3.4 million; US cloud architect median pay reached roughly $140,000 in 2024, driving wage inflation and retention bonuses that strengthen staffing suppliers and contractors. Project timelines and SLAs hinge on access to these niche skills, increasing dependence, while internal academies and offshore benches are used to reduce exposure.

Licensing and compliance dependencies

Enterprise software licensing terms, audits, and 2024 compliance shifts have driven unexpected cost spikes, with industry reports noting roughly a 15% year-over-year rise in audit activity. Suppliers can enforce mandatory upgrade paths that force rework across integrated systems, adding 10–20% to multi-year program budgets. This creates significant budget unpredictability for multi-year programs. Strong contract governance and volume agreements can stabilize costs and deliver up to 20–25% savings.

Infrastructure and datacenter inputs

Hardware lead times for chips and network gear remain bottlenecks; semiconductor industry revenue was about 624 billion USD in 2023 and tightness persisted into 2024, keeping lead times elevated. Supply shocks and ESG demands from colocation partners can raise pricing and restrict availability, and managed services built on third-party facilities inherit those constraints. Cloud-first architectures and hyperscaler migration materially reduce direct physical supply exposure.

- Lead times: chips, network gear bottlenecks

- Supply shocks & ESG: alter pricing/availability

- Managed services inherit provider constraints

- Cloud-first: lowers physical supply exposure

Toolchain ecosystem interoperability

Integration toolchains (CI/CD, observability, DevSecOps) are highly interdependent; in 2024 the global DevOps/tools market was ~13 billion USD, so deprecation or repricing of a key tool can force cascading switches across pipelines. Vendors increasingly bundle features to raise effective lock-in, while standards-based, API-first tools preserve optionality and reduce migration costs.

- Interdependence: cascading migration risk

- Market scale: ~13B USD (2024)

- Lock-in: vendor bundling raises switching costs

- Mitigation: prefer standards/API-first

Hyperscalers ~66%; cyber skill gap 3.4M

Supplier power is high: top three hyperscalers hold ~66% (AWS 32%, Azure 23%, GCP 11%), raising lock‑in and switching costs. Skill shortages (2024 cyber workforce gap ~3.4M; US cloud architect median ~$140k) and rising licensing/audit activity (~+15% YoY) increase supplier leverage. Hardware tightness (semiconductors ~$624B 2023) and bundled tooling (DevOps market ~$13B 2024) amplify risk; multi‑vendor/open‑source and strong contracts reduce it.

| Metric | Value |

|---|---|

| Hyperscaler share | ~66% |

| Cyber workforce gap | 3.4M (2024) |

| Cloud architect pay (US) | $140k (median 2024) |

| Semiconductor revenue | $624B (2023) |

| DevOps/tools market | $13B (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for NSD that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics impacting pricing, profitability, and strategic positioning.

A concise one-sheet NSD Porter's Five Forces that maps competitive pressure with a spider chart—ready to drop into decks and easily customize for new data or scenarios without macros.

Customers Bargaining Power

Large enterprise procurement leverage

Financial services, manufacturing and telecom buyers run competitive RFPs that demand volume discounts, strict SLAs and penalty clauses, driving procurement-led price pressure. These terms compress system integration and managed services margins, often pushing gross margins into mid-single digits for commoditized projects. NSD resists pure price competition through differentiated domain solutions and outcome-based offerings that preserve premium pricing and long-term contracts.

High switching but multi-sourcing

Systems are sticky, yet buyers routinely multi-source by tower or project, reflecting a 2024 global outsourcing market near $520B where modular sourcing is common; benchmarking and periodic rebids can shave 5–15% off rates despite switching costs, and coexistence with rivals reduces dependency on any single vendor; long-term value realization and referenceability remain key to retaining share.

Outcome-based expectations

Clients increasingly demand KPIs tied to uptime, defect rates and business outcomes, and in 2024 the global IT outsourcing market reached about 420 billion USD, amplifying stakes for vendors. Gain-share or fixed-bid models shift delivery risk to NSD and boost buyer negotiating power. This elevates price and contract leverage. Robust estimation, contingency buffers and strict risk allocation are essential.

Cloud cost transparency

FinOps visibility lets buyers scrutinize TCO and line-item spend; FinOps Foundation 2024 found 66% of enterprises rank cloud cost optimization as a top priority, enabling annual demands for cost-down roadmaps. Transparent unit economics empower renegotiation of rates and SLAs, while vendors offering proactive optimization services turn scrutiny into upsell opportunities by delivering measurable savings.

- FinOps 2024: 66% prioritize cost optimization

- Annual cost-down roadmaps demanded

- Unit economics enable renegotiation

- Proactive optimization = upsell

Security and compliance requirements

Regulated sectors impose stringent controls and audits, and failure to meet required certifications often disqualifies vendors from procurement; noncompliance risk is material given the IBM Cost of a Data Breach Report 2024 average cost of $4.45 million. Buyers increasingly demand continuous compliance reporting at no extra charge, so investing in attestations (SOC 2, ISO 27001, PCI DSS) reduces churn and mitigates price pressure.

- Mandatory certifications drive procurement filters

- Continuous reporting demanded at no extra cost

- Attestations lower churn and competitive pricing pressure

- Data breach average cost $4.45M (IBM 2024)

$520B market sees margin squeeze as buyers push 66% FinOps

Buyers exert strong price and contract leverage via competitive RFPs, multi-sourcing and outcome/KPI demands, compressing margins despite system stickiness. 2024 market dynamics—global outsourcing ~$520B, IT outsourcing ~$420B, FinOps priority 66%—heighten renegotiation and risk transfer. Certifications and breach costs (IBM 2024 $4.45M) further shape procurement.

| Metric | 2024 Value |

|---|---|

| Global outsourcing | $520B |

| IT outsourcing | $420B |

| FinOps priority | 66% |

| Avg breach cost | $4.45M |

Preview Before You Purchase

NSD Porter's Five Forces Analysis

This preview shows the exact NSD Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final version; instant access upon payment.

A Must-Have Tool for Decision-Makers

NSD’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of substitutes, and barriers to entry—key inputs for strategic planning and valuation. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for confident decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

NSD depends on a concentrated set of hyperscalers, database, middleware and cybersecurity vendors; in 2024 the top three hyperscalers held ~66% of the cloud IaaS/PaaS market (AWS 32%, Azure 23%, GCP 11%), amplifying switching costs and lock‑in via 3–5 year maintenance/contracts. Certification and proprietary stacks shift pricing power to suppliers, while multi‑vendor strategies and open‑source adoption can materially reduce dependency.

Specialized talent scarcity

Highly skilled engineers, cloud architects, and cybersecurity specialists are scarce, with ISC2 reporting a 2024 global cybersecurity workforce gap of about 3.4 million; US cloud architect median pay reached roughly $140,000 in 2024, driving wage inflation and retention bonuses that strengthen staffing suppliers and contractors. Project timelines and SLAs hinge on access to these niche skills, increasing dependence, while internal academies and offshore benches are used to reduce exposure.

Licensing and compliance dependencies

Enterprise software licensing terms, audits, and 2024 compliance shifts have driven unexpected cost spikes, with industry reports noting roughly a 15% year-over-year rise in audit activity. Suppliers can enforce mandatory upgrade paths that force rework across integrated systems, adding 10–20% to multi-year program budgets. This creates significant budget unpredictability for multi-year programs. Strong contract governance and volume agreements can stabilize costs and deliver up to 20–25% savings.

Infrastructure and datacenter inputs

Hardware lead times for chips and network gear remain bottlenecks; semiconductor industry revenue was about 624 billion USD in 2023 and tightness persisted into 2024, keeping lead times elevated. Supply shocks and ESG demands from colocation partners can raise pricing and restrict availability, and managed services built on third-party facilities inherit those constraints. Cloud-first architectures and hyperscaler migration materially reduce direct physical supply exposure.

- Lead times: chips, network gear bottlenecks

- Supply shocks & ESG: alter pricing/availability

- Managed services inherit provider constraints

- Cloud-first: lowers physical supply exposure

Toolchain ecosystem interoperability

Integration toolchains (CI/CD, observability, DevSecOps) are highly interdependent; in 2024 the global DevOps/tools market was ~13 billion USD, so deprecation or repricing of a key tool can force cascading switches across pipelines. Vendors increasingly bundle features to raise effective lock-in, while standards-based, API-first tools preserve optionality and reduce migration costs.

- Interdependence: cascading migration risk

- Market scale: ~13B USD (2024)

- Lock-in: vendor bundling raises switching costs

- Mitigation: prefer standards/API-first

Hyperscalers ~66%; cyber skill gap 3.4M

Supplier power is high: top three hyperscalers hold ~66% (AWS 32%, Azure 23%, GCP 11%), raising lock‑in and switching costs. Skill shortages (2024 cyber workforce gap ~3.4M; US cloud architect median ~$140k) and rising licensing/audit activity (~+15% YoY) increase supplier leverage. Hardware tightness (semiconductors ~$624B 2023) and bundled tooling (DevOps market ~$13B 2024) amplify risk; multi‑vendor/open‑source and strong contracts reduce it.

| Metric | Value |

|---|---|

| Hyperscaler share | ~66% |

| Cyber workforce gap | 3.4M (2024) |

| Cloud architect pay (US) | $140k (median 2024) |

| Semiconductor revenue | $624B (2023) |

| DevOps/tools market | $13B (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for NSD that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics impacting pricing, profitability, and strategic positioning.

A concise one-sheet NSD Porter's Five Forces that maps competitive pressure with a spider chart—ready to drop into decks and easily customize for new data or scenarios without macros.

Customers Bargaining Power

Large enterprise procurement leverage

Financial services, manufacturing and telecom buyers run competitive RFPs that demand volume discounts, strict SLAs and penalty clauses, driving procurement-led price pressure. These terms compress system integration and managed services margins, often pushing gross margins into mid-single digits for commoditized projects. NSD resists pure price competition through differentiated domain solutions and outcome-based offerings that preserve premium pricing and long-term contracts.

High switching but multi-sourcing

Systems are sticky, yet buyers routinely multi-source by tower or project, reflecting a 2024 global outsourcing market near $520B where modular sourcing is common; benchmarking and periodic rebids can shave 5–15% off rates despite switching costs, and coexistence with rivals reduces dependency on any single vendor; long-term value realization and referenceability remain key to retaining share.

Outcome-based expectations

Clients increasingly demand KPIs tied to uptime, defect rates and business outcomes, and in 2024 the global IT outsourcing market reached about 420 billion USD, amplifying stakes for vendors. Gain-share or fixed-bid models shift delivery risk to NSD and boost buyer negotiating power. This elevates price and contract leverage. Robust estimation, contingency buffers and strict risk allocation are essential.

Cloud cost transparency

FinOps visibility lets buyers scrutinize TCO and line-item spend; FinOps Foundation 2024 found 66% of enterprises rank cloud cost optimization as a top priority, enabling annual demands for cost-down roadmaps. Transparent unit economics empower renegotiation of rates and SLAs, while vendors offering proactive optimization services turn scrutiny into upsell opportunities by delivering measurable savings.

- FinOps 2024: 66% prioritize cost optimization

- Annual cost-down roadmaps demanded

- Unit economics enable renegotiation

- Proactive optimization = upsell

Security and compliance requirements

Regulated sectors impose stringent controls and audits, and failure to meet required certifications often disqualifies vendors from procurement; noncompliance risk is material given the IBM Cost of a Data Breach Report 2024 average cost of $4.45 million. Buyers increasingly demand continuous compliance reporting at no extra charge, so investing in attestations (SOC 2, ISO 27001, PCI DSS) reduces churn and mitigates price pressure.

- Mandatory certifications drive procurement filters

- Continuous reporting demanded at no extra cost

- Attestations lower churn and competitive pricing pressure

- Data breach average cost $4.45M (IBM 2024)

$520B market sees margin squeeze as buyers push 66% FinOps

Buyers exert strong price and contract leverage via competitive RFPs, multi-sourcing and outcome/KPI demands, compressing margins despite system stickiness. 2024 market dynamics—global outsourcing ~$520B, IT outsourcing ~$420B, FinOps priority 66%—heighten renegotiation and risk transfer. Certifications and breach costs (IBM 2024 $4.45M) further shape procurement.

| Metric | 2024 Value |

|---|---|

| Global outsourcing | $520B |

| IT outsourcing | $420B |

| FinOps priority | 66% |

| Avg breach cost | $4.45M |

Preview Before You Purchase

NSD Porter's Five Forces Analysis

This preview shows the exact NSD Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final version; instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

NSD’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, threat of substitutes, and barriers to entry—key inputs for strategic planning and valuation. This brief only scratches the surface; unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations for confident decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

NSD depends on a concentrated set of hyperscalers, database, middleware and cybersecurity vendors; in 2024 the top three hyperscalers held ~66% of the cloud IaaS/PaaS market (AWS 32%, Azure 23%, GCP 11%), amplifying switching costs and lock‑in via 3–5 year maintenance/contracts. Certification and proprietary stacks shift pricing power to suppliers, while multi‑vendor strategies and open‑source adoption can materially reduce dependency.

Specialized talent scarcity

Highly skilled engineers, cloud architects, and cybersecurity specialists are scarce, with ISC2 reporting a 2024 global cybersecurity workforce gap of about 3.4 million; US cloud architect median pay reached roughly $140,000 in 2024, driving wage inflation and retention bonuses that strengthen staffing suppliers and contractors. Project timelines and SLAs hinge on access to these niche skills, increasing dependence, while internal academies and offshore benches are used to reduce exposure.

Licensing and compliance dependencies

Enterprise software licensing terms, audits, and 2024 compliance shifts have driven unexpected cost spikes, with industry reports noting roughly a 15% year-over-year rise in audit activity. Suppliers can enforce mandatory upgrade paths that force rework across integrated systems, adding 10–20% to multi-year program budgets. This creates significant budget unpredictability for multi-year programs. Strong contract governance and volume agreements can stabilize costs and deliver up to 20–25% savings.

Infrastructure and datacenter inputs

Hardware lead times for chips and network gear remain bottlenecks; semiconductor industry revenue was about 624 billion USD in 2023 and tightness persisted into 2024, keeping lead times elevated. Supply shocks and ESG demands from colocation partners can raise pricing and restrict availability, and managed services built on third-party facilities inherit those constraints. Cloud-first architectures and hyperscaler migration materially reduce direct physical supply exposure.

- Lead times: chips, network gear bottlenecks

- Supply shocks & ESG: alter pricing/availability

- Managed services inherit provider constraints

- Cloud-first: lowers physical supply exposure

Toolchain ecosystem interoperability

Integration toolchains (CI/CD, observability, DevSecOps) are highly interdependent; in 2024 the global DevOps/tools market was ~13 billion USD, so deprecation or repricing of a key tool can force cascading switches across pipelines. Vendors increasingly bundle features to raise effective lock-in, while standards-based, API-first tools preserve optionality and reduce migration costs.

- Interdependence: cascading migration risk

- Market scale: ~13B USD (2024)

- Lock-in: vendor bundling raises switching costs

- Mitigation: prefer standards/API-first

Hyperscalers ~66%; cyber skill gap 3.4M

Supplier power is high: top three hyperscalers hold ~66% (AWS 32%, Azure 23%, GCP 11%), raising lock‑in and switching costs. Skill shortages (2024 cyber workforce gap ~3.4M; US cloud architect median ~$140k) and rising licensing/audit activity (~+15% YoY) increase supplier leverage. Hardware tightness (semiconductors ~$624B 2023) and bundled tooling (DevOps market ~$13B 2024) amplify risk; multi‑vendor/open‑source and strong contracts reduce it.

| Metric | Value |

|---|---|

| Hyperscaler share | ~66% |

| Cyber workforce gap | 3.4M (2024) |

| Cloud architect pay (US) | $140k (median 2024) |

| Semiconductor revenue | $624B (2023) |

| DevOps/tools market | $13B (2024) |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored for NSD that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and market dynamics impacting pricing, profitability, and strategic positioning.

A concise one-sheet NSD Porter's Five Forces that maps competitive pressure with a spider chart—ready to drop into decks and easily customize for new data or scenarios without macros.

Customers Bargaining Power

Large enterprise procurement leverage

Financial services, manufacturing and telecom buyers run competitive RFPs that demand volume discounts, strict SLAs and penalty clauses, driving procurement-led price pressure. These terms compress system integration and managed services margins, often pushing gross margins into mid-single digits for commoditized projects. NSD resists pure price competition through differentiated domain solutions and outcome-based offerings that preserve premium pricing and long-term contracts.

High switching but multi-sourcing

Systems are sticky, yet buyers routinely multi-source by tower or project, reflecting a 2024 global outsourcing market near $520B where modular sourcing is common; benchmarking and periodic rebids can shave 5–15% off rates despite switching costs, and coexistence with rivals reduces dependency on any single vendor; long-term value realization and referenceability remain key to retaining share.

Outcome-based expectations

Clients increasingly demand KPIs tied to uptime, defect rates and business outcomes, and in 2024 the global IT outsourcing market reached about 420 billion USD, amplifying stakes for vendors. Gain-share or fixed-bid models shift delivery risk to NSD and boost buyer negotiating power. This elevates price and contract leverage. Robust estimation, contingency buffers and strict risk allocation are essential.

Cloud cost transparency

FinOps visibility lets buyers scrutinize TCO and line-item spend; FinOps Foundation 2024 found 66% of enterprises rank cloud cost optimization as a top priority, enabling annual demands for cost-down roadmaps. Transparent unit economics empower renegotiation of rates and SLAs, while vendors offering proactive optimization services turn scrutiny into upsell opportunities by delivering measurable savings.

- FinOps 2024: 66% prioritize cost optimization

- Annual cost-down roadmaps demanded

- Unit economics enable renegotiation

- Proactive optimization = upsell

Security and compliance requirements

Regulated sectors impose stringent controls and audits, and failure to meet required certifications often disqualifies vendors from procurement; noncompliance risk is material given the IBM Cost of a Data Breach Report 2024 average cost of $4.45 million. Buyers increasingly demand continuous compliance reporting at no extra charge, so investing in attestations (SOC 2, ISO 27001, PCI DSS) reduces churn and mitigates price pressure.

- Mandatory certifications drive procurement filters

- Continuous reporting demanded at no extra cost

- Attestations lower churn and competitive pricing pressure

- Data breach average cost $4.45M (IBM 2024)

$520B market sees margin squeeze as buyers push 66% FinOps

Buyers exert strong price and contract leverage via competitive RFPs, multi-sourcing and outcome/KPI demands, compressing margins despite system stickiness. 2024 market dynamics—global outsourcing ~$520B, IT outsourcing ~$420B, FinOps priority 66%—heighten renegotiation and risk transfer. Certifications and breach costs (IBM 2024 $4.45M) further shape procurement.

| Metric | 2024 Value |

|---|---|

| Global outsourcing | $520B |

| IT outsourcing | $420B |

| FinOps priority | 66% |

| Avg breach cost | $4.45M |

Preview Before You Purchase

NSD Porter's Five Forces Analysis

This preview shows the exact NSD Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You're viewing the final version; instant access upon payment.