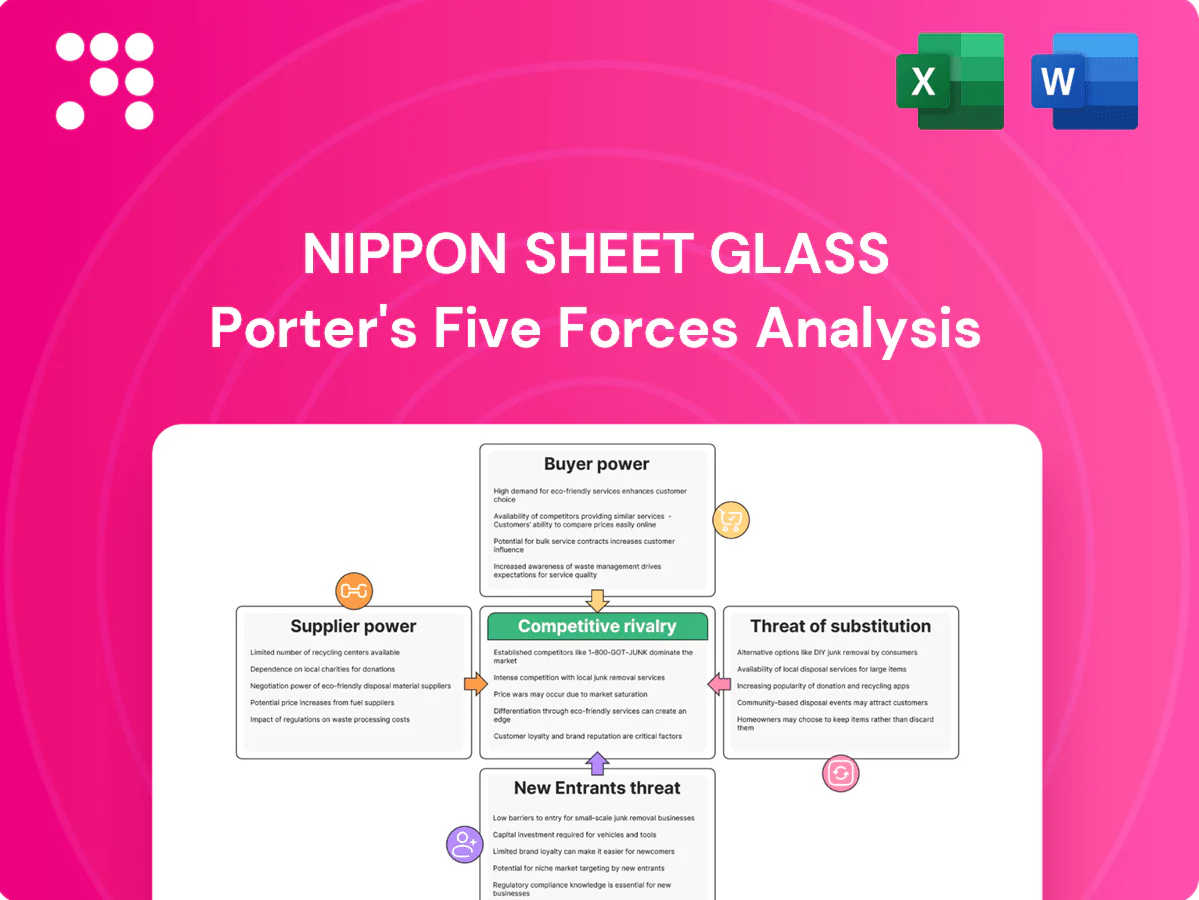

Nippon Sheet Glass Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Nippon Sheet Glass faces moderate rivalry driven by global glazing demand, scale advantages of larger players, and pressure from commodity glass suppliers, while buyer concentration in construction and automotive raises pricing sensitivity. Technological differentiation and integration lower threat of substitutes, but capital intensity and regulatory standards limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Sheet Glass’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

High-purity silica sand, soda ash and limestone for NSG are sourced from a small set of regionally concentrated suppliers, a structure that in 2024 sustained upward pricing pressure and reduced flexibility during regional disruptions.

Long-term contracts cover the majority of volumes, limiting short-term switching but capping spot-price spikes; NSG’s global footprint across Asia, Europe and the Americas provides some geographic diversification of supply.

Energy intensity exposure

Glass melting for Nippon Sheet Glass depends heavily on natural gas and electricity, making utilities a pivotal input and exposing margins to volatile fuel and carbon costs; the EU ETS averaged around €85/t CO2 in 2024, amplifying supplier leverage in regions under carbon pricing. Hedging and fuel‑switching or hybrid furnaces can dampen price shocks but require significant capex and operational complexity. Regional energy policy divergence creates differential margin stability across markets.

Specialty inputs scarcity

Specialty inputs for NSG—tin for float baths, PVB/EVA interlayers, silver/sputter targets and rare-earth coatings—are typically available from only 2–3 qualified suppliers in 2024, so quality-critical specs severely constrain substitution. Any disruption to these streams can halt high-value float and laminated lines within hours, magnifying revenue exposure. NSG must therefore maintain dual-sourcing contracts and larger inventory buffers to ensure continuity.

Logistics and heavy freight

Logistics and heavy freight raise supplier power for Nippon Sheet Glass because raw materials and finished glass are heavy, fragile and can push transport to as much as 20–25% of delivered cost in 2024, especially where local quarries or port access gives suppliers geographic leverage; tight freight markets in 2024 amplified delivered-cost pressure, though near-plant supply agreements partially offset this.

- Heavy freight increases delivered cost ~20–25% (2024)

- Proximity to quarries/ports boosts local supplier leverage

- 2024 tight freight markets raised price volatility

- Near-plant supply agreements reduce but do not eliminate risk

Qualification and switching costs

Automotive and coated glass require stringent supplier qualifications, with OEM requalification commonly taking 6–12 months; switching suppliers risks short-term yield loss and production delays, which increases supplier leverage over Nippon Sheet Glass.

- Requalification time: 6–12 months

- Switching risk: short-term yield loss and OEM delays

- Effect: higher supplier bargaining power

- Mitigation: structured supplier development over 24–36 months

Supplier squeeze: 2–3 specialty vendors, EU carbon €85/t and high freight

Suppliers exert medium–high power: critical inputs (tin, sputter targets, interlayers) often come from 2–3 qualified suppliers in 2024, limiting substitution. Energy and carbon costs (EU ETS ~€85/t CO2 in 2024) and heavy freight (20–25% of delivered cost) raise input volatility and margins exposure. Long-term contracts and NSG’s global footprint partly mitigate but do not eliminate supplier leverage.

| Factor | 2024 metric | Impact |

|---|---|---|

| Specialty suppliers | 2–3 qualified | High |

| EU carbon price | €85/t CO2 | Raises energy cost |

| Freight | 20–25% delivered cost | Elevates supplier power |

| OEM requalification | 6–12 months | Limits switching |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon Sheet Glass revealing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities from disruptive technologies and market shifts.

A concise, one-sheet Porter’s Five Forces for Nippon Sheet Glass—customize pressure levels, swap in your data, and export clean radar charts for decks or boardrooms to simplify strategic decisions.

Customers Bargaining Power

Automotive OEM leverage

In 2024 global automakers continued to exert strong leverage over suppliers, buying at scale and enforcing strict quality, cost and delivery terms; multi‑year sourcing cycles (typically 3–7 years) with periodic rebids (every 3–5 years) maintain relentless price pressure. Tooling and homologation create switching friction but do not prevent competitive rebids, while value‑added features such as HUD, acoustic glazing and ADAS integration can partially rebalance negotiation power.

Construction channel fragmentation

Architectural buyers—from developers to fabricators and distributors—are highly fragmented, yet spec-driven bidding creates high price visibility; the global architectural glass market was about USD 86.5 billion in 2024, intensifying competition.

Value engineering on large projects frequently de-specs premium coatings, eroding margins for suppliers like Nippon Sheet Glass.

Tight timelines make reliability and service breadth decisive: projects with compressed schedules favor suppliers offering technical support and local inventory, reducing buyer leverage.

Aftermarket vs OEM mix

Automotive aftermarket glazing typically delivers higher margins (2024 industry estimates: aftermarket gross margins ~15–25% versus OEM ~5–10%) and therefore exhibits lower buyer power, while OEM volumes — roughly 70–80% of total glazing volumes in 2024 — drive scale and set pricing benchmarks. Balancing a higher-margin aftermarket mix and proprietary Pilkington models helps NSG soften OEM pricing pressure, and Pilkington’s brand reputation sustains aftermarket pull.

Technical glass specialization

Specialty customers in electronics, solar and optics prioritize performance over price, enabling Nippon Sheet Glass to capture performance premiums often in the 10–30% range; custom specs and co-development further reduce buyer leverage by embedding products into customers’ designs. Qualification cycles of 12–24 months create periodic price reset points, while IP and application know-how increase customer stickiness.

- Performance-led demand — premiums 10–30%

- Co-development lowers buyer power

- Qualification cycles 12–24 months

- IP/application know-how raises switching costs

Global sourcing options

Buyers can source glass from AGC, Saint-Gobain, Guardian and large Chinese producers, expanding leverage as overcapacity in certain regions offers alternatives. Practical switching is limited by trade barriers, tariffs and logistics costs, which raise effective switching costs. NSG and competitors retain accounts through regional footprints, technical service networks and just-in-time supply.

- Sources: AGC, Saint-Gobain, Guardian, Chinese mills

- Limiting factors: tariffs, transport, lead times

- Retention: regional presence, service networks

OEM ~75% volumes cut OEM margin ~7%; aftermarket margin ~20%

Customers wield strong OEM leverage (OEM ~75% volumes in 2024) with multi‑year sourcing and relentless price pressure; aftermarket and specialty demand (aftermarket gross margins ~20% vs OEM ~7% in 2024) provide higher margins and lower buyer power. Fragmented architectural buyers and overcapacity raise price visibility, while co‑development and long qualification (12–24m) reduce switching.

| Metric | 2024 |

|---|---|

| OEM share | ~75% |

| Aftermarket gross margin | ~20% |

| OEM gross margin | ~7% |

| Architectural market | USD 86.5B |

Preview the Actual Deliverable

Nippon Sheet Glass Porter's Five Forces Analysis

This preview shows the exact Nippon Sheet Glass Porter's Five Forces analysis you'll receive—no placeholders or mockups. It provides a full, professionally formatted evaluation of competitive rivalry, supplier and buyer power, and threats of entry and substitutes, with clear strategic implications. Instant download and use after purchase.

Go Beyond the Preview—Access the Full Strategic Report

Nippon Sheet Glass faces moderate rivalry driven by global glazing demand, scale advantages of larger players, and pressure from commodity glass suppliers, while buyer concentration in construction and automotive raises pricing sensitivity. Technological differentiation and integration lower threat of substitutes, but capital intensity and regulatory standards limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Sheet Glass’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

High-purity silica sand, soda ash and limestone for NSG are sourced from a small set of regionally concentrated suppliers, a structure that in 2024 sustained upward pricing pressure and reduced flexibility during regional disruptions.

Long-term contracts cover the majority of volumes, limiting short-term switching but capping spot-price spikes; NSG’s global footprint across Asia, Europe and the Americas provides some geographic diversification of supply.

Energy intensity exposure

Glass melting for Nippon Sheet Glass depends heavily on natural gas and electricity, making utilities a pivotal input and exposing margins to volatile fuel and carbon costs; the EU ETS averaged around €85/t CO2 in 2024, amplifying supplier leverage in regions under carbon pricing. Hedging and fuel‑switching or hybrid furnaces can dampen price shocks but require significant capex and operational complexity. Regional energy policy divergence creates differential margin stability across markets.

Specialty inputs scarcity

Specialty inputs for NSG—tin for float baths, PVB/EVA interlayers, silver/sputter targets and rare-earth coatings—are typically available from only 2–3 qualified suppliers in 2024, so quality-critical specs severely constrain substitution. Any disruption to these streams can halt high-value float and laminated lines within hours, magnifying revenue exposure. NSG must therefore maintain dual-sourcing contracts and larger inventory buffers to ensure continuity.

Logistics and heavy freight

Logistics and heavy freight raise supplier power for Nippon Sheet Glass because raw materials and finished glass are heavy, fragile and can push transport to as much as 20–25% of delivered cost in 2024, especially where local quarries or port access gives suppliers geographic leverage; tight freight markets in 2024 amplified delivered-cost pressure, though near-plant supply agreements partially offset this.

- Heavy freight increases delivered cost ~20–25% (2024)

- Proximity to quarries/ports boosts local supplier leverage

- 2024 tight freight markets raised price volatility

- Near-plant supply agreements reduce but do not eliminate risk

Qualification and switching costs

Automotive and coated glass require stringent supplier qualifications, with OEM requalification commonly taking 6–12 months; switching suppliers risks short-term yield loss and production delays, which increases supplier leverage over Nippon Sheet Glass.

- Requalification time: 6–12 months

- Switching risk: short-term yield loss and OEM delays

- Effect: higher supplier bargaining power

- Mitigation: structured supplier development over 24–36 months

Supplier squeeze: 2–3 specialty vendors, EU carbon €85/t and high freight

Suppliers exert medium–high power: critical inputs (tin, sputter targets, interlayers) often come from 2–3 qualified suppliers in 2024, limiting substitution. Energy and carbon costs (EU ETS ~€85/t CO2 in 2024) and heavy freight (20–25% of delivered cost) raise input volatility and margins exposure. Long-term contracts and NSG’s global footprint partly mitigate but do not eliminate supplier leverage.

| Factor | 2024 metric | Impact |

|---|---|---|

| Specialty suppliers | 2–3 qualified | High |

| EU carbon price | €85/t CO2 | Raises energy cost |

| Freight | 20–25% delivered cost | Elevates supplier power |

| OEM requalification | 6–12 months | Limits switching |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon Sheet Glass revealing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities from disruptive technologies and market shifts.

A concise, one-sheet Porter’s Five Forces for Nippon Sheet Glass—customize pressure levels, swap in your data, and export clean radar charts for decks or boardrooms to simplify strategic decisions.

Customers Bargaining Power

Automotive OEM leverage

In 2024 global automakers continued to exert strong leverage over suppliers, buying at scale and enforcing strict quality, cost and delivery terms; multi‑year sourcing cycles (typically 3–7 years) with periodic rebids (every 3–5 years) maintain relentless price pressure. Tooling and homologation create switching friction but do not prevent competitive rebids, while value‑added features such as HUD, acoustic glazing and ADAS integration can partially rebalance negotiation power.

Construction channel fragmentation

Architectural buyers—from developers to fabricators and distributors—are highly fragmented, yet spec-driven bidding creates high price visibility; the global architectural glass market was about USD 86.5 billion in 2024, intensifying competition.

Value engineering on large projects frequently de-specs premium coatings, eroding margins for suppliers like Nippon Sheet Glass.

Tight timelines make reliability and service breadth decisive: projects with compressed schedules favor suppliers offering technical support and local inventory, reducing buyer leverage.

Aftermarket vs OEM mix

Automotive aftermarket glazing typically delivers higher margins (2024 industry estimates: aftermarket gross margins ~15–25% versus OEM ~5–10%) and therefore exhibits lower buyer power, while OEM volumes — roughly 70–80% of total glazing volumes in 2024 — drive scale and set pricing benchmarks. Balancing a higher-margin aftermarket mix and proprietary Pilkington models helps NSG soften OEM pricing pressure, and Pilkington’s brand reputation sustains aftermarket pull.

Technical glass specialization

Specialty customers in electronics, solar and optics prioritize performance over price, enabling Nippon Sheet Glass to capture performance premiums often in the 10–30% range; custom specs and co-development further reduce buyer leverage by embedding products into customers’ designs. Qualification cycles of 12–24 months create periodic price reset points, while IP and application know-how increase customer stickiness.

- Performance-led demand — premiums 10–30%

- Co-development lowers buyer power

- Qualification cycles 12–24 months

- IP/application know-how raises switching costs

Global sourcing options

Buyers can source glass from AGC, Saint-Gobain, Guardian and large Chinese producers, expanding leverage as overcapacity in certain regions offers alternatives. Practical switching is limited by trade barriers, tariffs and logistics costs, which raise effective switching costs. NSG and competitors retain accounts through regional footprints, technical service networks and just-in-time supply.

- Sources: AGC, Saint-Gobain, Guardian, Chinese mills

- Limiting factors: tariffs, transport, lead times

- Retention: regional presence, service networks

OEM ~75% volumes cut OEM margin ~7%; aftermarket margin ~20%

Customers wield strong OEM leverage (OEM ~75% volumes in 2024) with multi‑year sourcing and relentless price pressure; aftermarket and specialty demand (aftermarket gross margins ~20% vs OEM ~7% in 2024) provide higher margins and lower buyer power. Fragmented architectural buyers and overcapacity raise price visibility, while co‑development and long qualification (12–24m) reduce switching.

| Metric | 2024 |

|---|---|

| OEM share | ~75% |

| Aftermarket gross margin | ~20% |

| OEM gross margin | ~7% |

| Architectural market | USD 86.5B |

Preview the Actual Deliverable

Nippon Sheet Glass Porter's Five Forces Analysis

This preview shows the exact Nippon Sheet Glass Porter's Five Forces analysis you'll receive—no placeholders or mockups. It provides a full, professionally formatted evaluation of competitive rivalry, supplier and buyer power, and threats of entry and substitutes, with clear strategic implications. Instant download and use after purchase.

Description

Go Beyond the Preview—Access the Full Strategic Report

Nippon Sheet Glass faces moderate rivalry driven by global glazing demand, scale advantages of larger players, and pressure from commodity glass suppliers, while buyer concentration in construction and automotive raises pricing sensitivity. Technological differentiation and integration lower threat of substitutes, but capital intensity and regulatory standards limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Nippon Sheet Glass’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated raw materials

High-purity silica sand, soda ash and limestone for NSG are sourced from a small set of regionally concentrated suppliers, a structure that in 2024 sustained upward pricing pressure and reduced flexibility during regional disruptions.

Long-term contracts cover the majority of volumes, limiting short-term switching but capping spot-price spikes; NSG’s global footprint across Asia, Europe and the Americas provides some geographic diversification of supply.

Energy intensity exposure

Glass melting for Nippon Sheet Glass depends heavily on natural gas and electricity, making utilities a pivotal input and exposing margins to volatile fuel and carbon costs; the EU ETS averaged around €85/t CO2 in 2024, amplifying supplier leverage in regions under carbon pricing. Hedging and fuel‑switching or hybrid furnaces can dampen price shocks but require significant capex and operational complexity. Regional energy policy divergence creates differential margin stability across markets.

Specialty inputs scarcity

Specialty inputs for NSG—tin for float baths, PVB/EVA interlayers, silver/sputter targets and rare-earth coatings—are typically available from only 2–3 qualified suppliers in 2024, so quality-critical specs severely constrain substitution. Any disruption to these streams can halt high-value float and laminated lines within hours, magnifying revenue exposure. NSG must therefore maintain dual-sourcing contracts and larger inventory buffers to ensure continuity.

Logistics and heavy freight

Logistics and heavy freight raise supplier power for Nippon Sheet Glass because raw materials and finished glass are heavy, fragile and can push transport to as much as 20–25% of delivered cost in 2024, especially where local quarries or port access gives suppliers geographic leverage; tight freight markets in 2024 amplified delivered-cost pressure, though near-plant supply agreements partially offset this.

- Heavy freight increases delivered cost ~20–25% (2024)

- Proximity to quarries/ports boosts local supplier leverage

- 2024 tight freight markets raised price volatility

- Near-plant supply agreements reduce but do not eliminate risk

Qualification and switching costs

Automotive and coated glass require stringent supplier qualifications, with OEM requalification commonly taking 6–12 months; switching suppliers risks short-term yield loss and production delays, which increases supplier leverage over Nippon Sheet Glass.

- Requalification time: 6–12 months

- Switching risk: short-term yield loss and OEM delays

- Effect: higher supplier bargaining power

- Mitigation: structured supplier development over 24–36 months

Supplier squeeze: 2–3 specialty vendors, EU carbon €85/t and high freight

Suppliers exert medium–high power: critical inputs (tin, sputter targets, interlayers) often come from 2–3 qualified suppliers in 2024, limiting substitution. Energy and carbon costs (EU ETS ~€85/t CO2 in 2024) and heavy freight (20–25% of delivered cost) raise input volatility and margins exposure. Long-term contracts and NSG’s global footprint partly mitigate but do not eliminate supplier leverage.

| Factor | 2024 metric | Impact |

|---|---|---|

| Specialty suppliers | 2–3 qualified | High |

| EU carbon price | €85/t CO2 | Raises energy cost |

| Freight | 20–25% delivered cost | Elevates supplier power |

| OEM requalification | 6–12 months | Limits switching |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon Sheet Glass revealing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities from disruptive technologies and market shifts.

A concise, one-sheet Porter’s Five Forces for Nippon Sheet Glass—customize pressure levels, swap in your data, and export clean radar charts for decks or boardrooms to simplify strategic decisions.

Customers Bargaining Power

Automotive OEM leverage

In 2024 global automakers continued to exert strong leverage over suppliers, buying at scale and enforcing strict quality, cost and delivery terms; multi‑year sourcing cycles (typically 3–7 years) with periodic rebids (every 3–5 years) maintain relentless price pressure. Tooling and homologation create switching friction but do not prevent competitive rebids, while value‑added features such as HUD, acoustic glazing and ADAS integration can partially rebalance negotiation power.

Construction channel fragmentation

Architectural buyers—from developers to fabricators and distributors—are highly fragmented, yet spec-driven bidding creates high price visibility; the global architectural glass market was about USD 86.5 billion in 2024, intensifying competition.

Value engineering on large projects frequently de-specs premium coatings, eroding margins for suppliers like Nippon Sheet Glass.

Tight timelines make reliability and service breadth decisive: projects with compressed schedules favor suppliers offering technical support and local inventory, reducing buyer leverage.

Aftermarket vs OEM mix

Automotive aftermarket glazing typically delivers higher margins (2024 industry estimates: aftermarket gross margins ~15–25% versus OEM ~5–10%) and therefore exhibits lower buyer power, while OEM volumes — roughly 70–80% of total glazing volumes in 2024 — drive scale and set pricing benchmarks. Balancing a higher-margin aftermarket mix and proprietary Pilkington models helps NSG soften OEM pricing pressure, and Pilkington’s brand reputation sustains aftermarket pull.

Technical glass specialization

Specialty customers in electronics, solar and optics prioritize performance over price, enabling Nippon Sheet Glass to capture performance premiums often in the 10–30% range; custom specs and co-development further reduce buyer leverage by embedding products into customers’ designs. Qualification cycles of 12–24 months create periodic price reset points, while IP and application know-how increase customer stickiness.

- Performance-led demand — premiums 10–30%

- Co-development lowers buyer power

- Qualification cycles 12–24 months

- IP/application know-how raises switching costs

Global sourcing options

Buyers can source glass from AGC, Saint-Gobain, Guardian and large Chinese producers, expanding leverage as overcapacity in certain regions offers alternatives. Practical switching is limited by trade barriers, tariffs and logistics costs, which raise effective switching costs. NSG and competitors retain accounts through regional footprints, technical service networks and just-in-time supply.

- Sources: AGC, Saint-Gobain, Guardian, Chinese mills

- Limiting factors: tariffs, transport, lead times

- Retention: regional presence, service networks

OEM ~75% volumes cut OEM margin ~7%; aftermarket margin ~20%

Customers wield strong OEM leverage (OEM ~75% volumes in 2024) with multi‑year sourcing and relentless price pressure; aftermarket and specialty demand (aftermarket gross margins ~20% vs OEM ~7% in 2024) provide higher margins and lower buyer power. Fragmented architectural buyers and overcapacity raise price visibility, while co‑development and long qualification (12–24m) reduce switching.

| Metric | 2024 |

|---|---|

| OEM share | ~75% |

| Aftermarket gross margin | ~20% |

| OEM gross margin | ~7% |

| Architectural market | USD 86.5B |

Preview the Actual Deliverable

Nippon Sheet Glass Porter's Five Forces Analysis

This preview shows the exact Nippon Sheet Glass Porter's Five Forces analysis you'll receive—no placeholders or mockups. It provides a full, professionally formatted evaluation of competitive rivalry, supplier and buyer power, and threats of entry and substitutes, with clear strategic implications. Instant download and use after purchase.