NSO Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

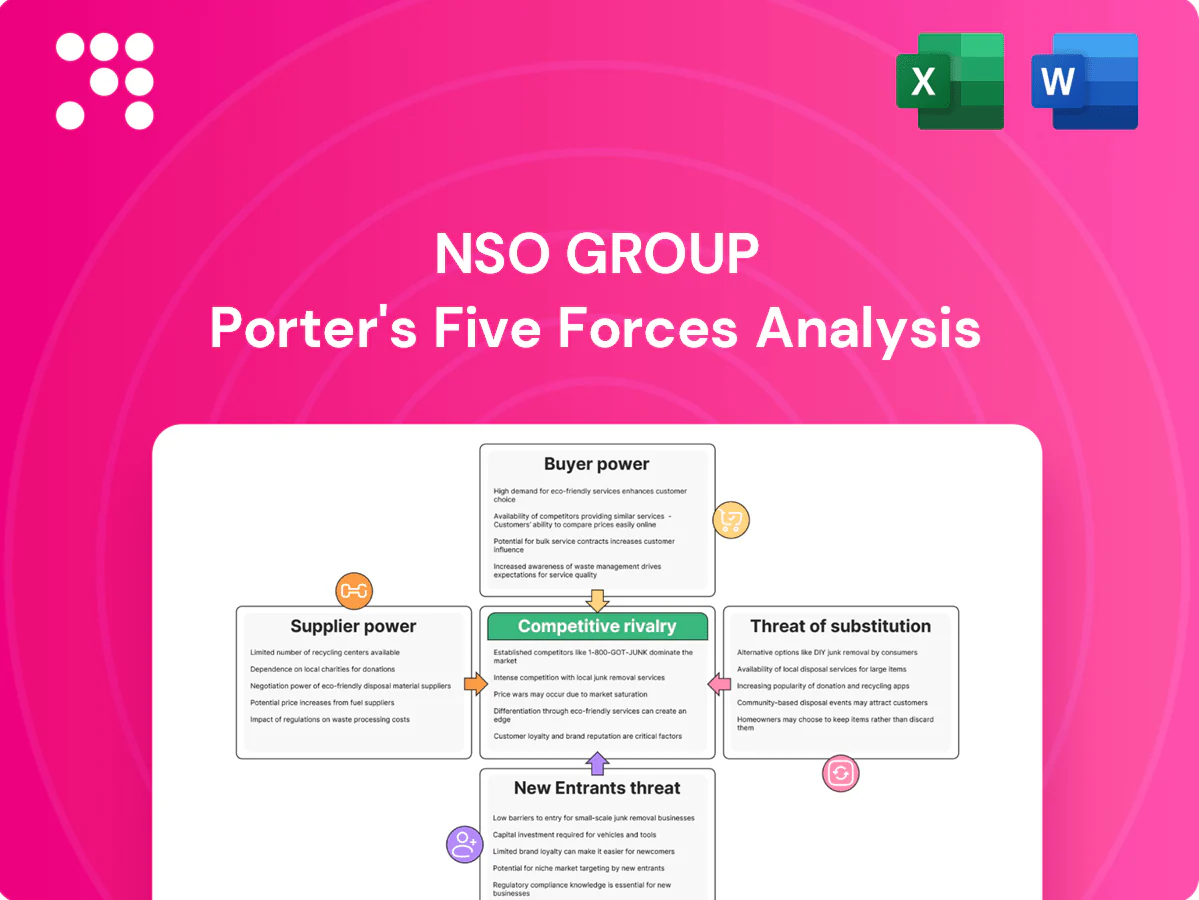

NSO Group faces intense supplier and regulatory pressure, high buyer scrutiny, moderate competitive rivalry from specialized cybersecurity firms, and a growing threat of substitutes via privacy-preserving tools. This Porter's Five Forces snapshot highlights key strategic risks and levers for value capture. Ready for deeper, force-by-force ratings, visuals, and actionable recommendations? Unlock the full analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Scarce zero-day exploit brokers

Access to high-quality undisclosed vulnerabilities is limited and costly, with broker payout listings (Zerodium) showing up to $2.5 million for high-end zero-click iOS exploits. That market leverage lets brokers dictate pricing and terms, and NSO depends on a steady pipeline of such reliable exploits to evade platform patches. Brokers can prioritize buyers or bundle deals, raising costs and dependence. Sanctions and disruptions (NSO was added to the US Entity List in Nov 2021) can directly impair product efficacy.

Elite security research talent

The market for top reverse engineers and offensive researchers is extremely tight, with the global cybersecurity workforce gap around 3.4 million in recent industry reports, giving this talent significant bargaining power.

Compensation and equity demands—often driving total pay packages above $300,000 for senior specialists—plus IP ownership terms can materially escalate costs for NSO.

Retention risk is high as competitors and state labs court the same experts; knowledge walkout can delay product roadmaps and lengthen maintenance cycles by months.

Platform and device ecosystem gatekeepers

Apple, Google and chipset vendors act as de facto suppliers of attack surface via their OS and hardware designs, controlling over 99% of global smartphone platforms. Rapid security hardening, lockdown modes and monthly patch cadences raise exploitation development costs and cut exploit shelf life to weeks. Vendors can litigate, notify targets and coordinate patches, increasing NSO’s operational burden. This dynamic compresses value-capture windows and amplifies platform-owner power.

Cloud, tooling, and infrastructure inputs

Specialized servers, C2 infrastructure, code-signing and telemetry tooling give suppliers leverage over NSO; major cloud providers held about 32% (AWS), 22% (Azure) and 12% (Google) of the IaaS/PaaS market in 2024, tightening KYC and abuse-detection which can force costly reconfigurations. Deplatforming raises switching and compliance costs and vendors can price in reputational or legal risk.

- High supplier concentration: AWS/Azure/Google ~66% (2024)

- Tighter KYC raises integration costs

- Deplatforming elevates switching/compliance costs

- Vendors may add risk premiums to pricing

Legal, export-control, and compliance advisors

Regulatory counsel and export-license consultants determine NSO Groups market access by interpreting sanctions, human-rights due diligence, and export controls; their structuring advice often dictates contract terms and geographic scope. Heightened scrutiny raised advisory demand and fees—legal/compliance spend rose ~12% in 2024—so withdrawal of counsel can halt deals or specific jurisdictions.

- High influence: licensing + contract shaping

- 2024: compliance/legal spend +12%

- Risk: advisory withdrawal stalls sales/geographies

Supplier leverage: payouts $2.5M, workforce gap 3.4M

Suppliers (exploit brokers, top researchers, cloud vendors, OS makers, legal advisers) hold high leverage: Zerodium payouts up to $2.5M, cybersecurity workforce gap ~3.4M (2024), senior pay >$300k, and AWS/Azure/GCP ~66% IaaS share. Sanctions and deplatforming raise costs; compliance spend rose ~12% in 2024.

| Supplier | Metric (2024) |

|---|---|

| Exploit brokers | $2.5M max payout |

| Talent | 3.4M gap; >$300k pay |

| Cloud | AWS/Azure/GCP ~66% |

| Compliance | +12% spend |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry—tailored to NSO Group’s unique position to assess pricing power, profitability risks, regulatory pressures, and strategic vulnerabilities.

A concise one-sheet Porter's Five Forces for NSO Group—instantly visualized in a radar chart to clarify strategic pressures and regulatory risk, ready to drop into decks or adapt with your data for scenario comparisons.

Customers Bargaining Power

Concentrated government clientele

Customers are few, large state agencies with strong procurement leverage, often accounting for the majority of revenues; deal sizes are typically multi-million-dollar, often >$1M, and lumpy, enabling hard price and performance negotiations. Buyers insist on bespoke features, on-site training and strict support SLAs, raising delivery costs. Vendor concentration risk amplifies discount pressure and contract dependency.

High switching costs but credible alternatives

Integration into lawful process, chain-of-custody and analyst workflows creates strong stickiness for NSO, yet in 2024 many states prefer 3–5 year procurement cycles that trigger re-bids and pilot programs; this, plus viable in-house buildouts or vendor rotation, constrains pricing power despite high switching friction.

Regulatory and reputational constraints

Agencies face political oversight, audits and human-rights scrutiny that can delay or cancel purchases; as of 2024 the US Entity List designation of NSO remains a material barrier to sales. Buyers demand stringent safeguards, independent usage monitoring and kill-switches, shifting operational and legal risk onto the vendor via warranties and compliance covenants. Vendors have offered concessions such as price reductions and extended multi-year support to salvage deals.

Outcome-based performance demands

Procurement now demands demonstrable efficacy against hardened targets and minimal detectability, with buyers negotiating performance-based milestones, penalties, and service credits; the 2021 Pegasus leak of over 50,000 exposed numbers underscores detection risk and buyer leverage. False positives, detections, or patch-driven degradation commonly trigger credits or churn, forcing continuous improvement at tighter margins and shifting pricing toward milestone-based fees.

- Performance milestones tie up to material fee portions

- Detections/patches -> credits or contract termination

- Continuous R&D pressure compresses margins

Budget cyclicality and geopolitics

Defense and interior budgets are cyclic and politicized—US FY2024 defense discretionary funding was about 858 billion USD and global military expenditure was 2.24 trillion USD in 2023 (SIPRI), affecting timing and scale of NSO sales; sanctions and alliance constraints (NSO placed on US Commerce Entity List in 2021) limit eligible buyers and contract terms. Buyers time purchases to fiscal cycles to extract discounts and frequently push for vendor financing or staggered licensing when budgets are constrained.

- Budget volatility: tag=US_FY2024_858B

- Global spend: tag=SIPRI_2023_2.24T

- Sanctions impact: tag=US_EntityList_2021

- Procurement leverage: tag=vendor_financing

Few giant state buyers, > $1M lumpy deals, 3–5yr re-bids compress margins

Customers are few, large state agencies with multi-million-dollar, lumpy deals (> $1M) and strong procurement leverage that forces performance milestones and concessions. High switching friction from workflow integration is offset by 3–5 year re-bids, in-house build alternatives and US 2021 Entity List sanctions that limit eligible buyers. Detection risks and continuous R&D compress margins and trigger credits or terminations.

| Metric | Value |

|---|---|

| Deal size | > $1M |

| US defense budget FY2024 | $858B |

| Global military spend 2023 (SIPRI) | $2.24T |

Preview Before You Purchase

NSO Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of NSO Group evaluates industry rivalry, supplier and buyer power, threat of substitutes, and entry barriers to clarify strategic pressures and value drivers. The preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or samples. It’s ready for download and use the moment you buy. The analysis is concise, actionable, and designed for immediate application.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

NSO Group faces intense supplier and regulatory pressure, high buyer scrutiny, moderate competitive rivalry from specialized cybersecurity firms, and a growing threat of substitutes via privacy-preserving tools. This Porter's Five Forces snapshot highlights key strategic risks and levers for value capture. Ready for deeper, force-by-force ratings, visuals, and actionable recommendations? Unlock the full analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Scarce zero-day exploit brokers

Access to high-quality undisclosed vulnerabilities is limited and costly, with broker payout listings (Zerodium) showing up to $2.5 million for high-end zero-click iOS exploits. That market leverage lets brokers dictate pricing and terms, and NSO depends on a steady pipeline of such reliable exploits to evade platform patches. Brokers can prioritize buyers or bundle deals, raising costs and dependence. Sanctions and disruptions (NSO was added to the US Entity List in Nov 2021) can directly impair product efficacy.

Elite security research talent

The market for top reverse engineers and offensive researchers is extremely tight, with the global cybersecurity workforce gap around 3.4 million in recent industry reports, giving this talent significant bargaining power.

Compensation and equity demands—often driving total pay packages above $300,000 for senior specialists—plus IP ownership terms can materially escalate costs for NSO.

Retention risk is high as competitors and state labs court the same experts; knowledge walkout can delay product roadmaps and lengthen maintenance cycles by months.

Platform and device ecosystem gatekeepers

Apple, Google and chipset vendors act as de facto suppliers of attack surface via their OS and hardware designs, controlling over 99% of global smartphone platforms. Rapid security hardening, lockdown modes and monthly patch cadences raise exploitation development costs and cut exploit shelf life to weeks. Vendors can litigate, notify targets and coordinate patches, increasing NSO’s operational burden. This dynamic compresses value-capture windows and amplifies platform-owner power.

Cloud, tooling, and infrastructure inputs

Specialized servers, C2 infrastructure, code-signing and telemetry tooling give suppliers leverage over NSO; major cloud providers held about 32% (AWS), 22% (Azure) and 12% (Google) of the IaaS/PaaS market in 2024, tightening KYC and abuse-detection which can force costly reconfigurations. Deplatforming raises switching and compliance costs and vendors can price in reputational or legal risk.

- High supplier concentration: AWS/Azure/Google ~66% (2024)

- Tighter KYC raises integration costs

- Deplatforming elevates switching/compliance costs

- Vendors may add risk premiums to pricing

Legal, export-control, and compliance advisors

Regulatory counsel and export-license consultants determine NSO Groups market access by interpreting sanctions, human-rights due diligence, and export controls; their structuring advice often dictates contract terms and geographic scope. Heightened scrutiny raised advisory demand and fees—legal/compliance spend rose ~12% in 2024—so withdrawal of counsel can halt deals or specific jurisdictions.

- High influence: licensing + contract shaping

- 2024: compliance/legal spend +12%

- Risk: advisory withdrawal stalls sales/geographies

Supplier leverage: payouts $2.5M, workforce gap 3.4M

Suppliers (exploit brokers, top researchers, cloud vendors, OS makers, legal advisers) hold high leverage: Zerodium payouts up to $2.5M, cybersecurity workforce gap ~3.4M (2024), senior pay >$300k, and AWS/Azure/GCP ~66% IaaS share. Sanctions and deplatforming raise costs; compliance spend rose ~12% in 2024.

| Supplier | Metric (2024) |

|---|---|

| Exploit brokers | $2.5M max payout |

| Talent | 3.4M gap; >$300k pay |

| Cloud | AWS/Azure/GCP ~66% |

| Compliance | +12% spend |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry—tailored to NSO Group’s unique position to assess pricing power, profitability risks, regulatory pressures, and strategic vulnerabilities.

A concise one-sheet Porter's Five Forces for NSO Group—instantly visualized in a radar chart to clarify strategic pressures and regulatory risk, ready to drop into decks or adapt with your data for scenario comparisons.

Customers Bargaining Power

Concentrated government clientele

Customers are few, large state agencies with strong procurement leverage, often accounting for the majority of revenues; deal sizes are typically multi-million-dollar, often >$1M, and lumpy, enabling hard price and performance negotiations. Buyers insist on bespoke features, on-site training and strict support SLAs, raising delivery costs. Vendor concentration risk amplifies discount pressure and contract dependency.

High switching costs but credible alternatives

Integration into lawful process, chain-of-custody and analyst workflows creates strong stickiness for NSO, yet in 2024 many states prefer 3–5 year procurement cycles that trigger re-bids and pilot programs; this, plus viable in-house buildouts or vendor rotation, constrains pricing power despite high switching friction.

Regulatory and reputational constraints

Agencies face political oversight, audits and human-rights scrutiny that can delay or cancel purchases; as of 2024 the US Entity List designation of NSO remains a material barrier to sales. Buyers demand stringent safeguards, independent usage monitoring and kill-switches, shifting operational and legal risk onto the vendor via warranties and compliance covenants. Vendors have offered concessions such as price reductions and extended multi-year support to salvage deals.

Outcome-based performance demands

Procurement now demands demonstrable efficacy against hardened targets and minimal detectability, with buyers negotiating performance-based milestones, penalties, and service credits; the 2021 Pegasus leak of over 50,000 exposed numbers underscores detection risk and buyer leverage. False positives, detections, or patch-driven degradation commonly trigger credits or churn, forcing continuous improvement at tighter margins and shifting pricing toward milestone-based fees.

- Performance milestones tie up to material fee portions

- Detections/patches -> credits or contract termination

- Continuous R&D pressure compresses margins

Budget cyclicality and geopolitics

Defense and interior budgets are cyclic and politicized—US FY2024 defense discretionary funding was about 858 billion USD and global military expenditure was 2.24 trillion USD in 2023 (SIPRI), affecting timing and scale of NSO sales; sanctions and alliance constraints (NSO placed on US Commerce Entity List in 2021) limit eligible buyers and contract terms. Buyers time purchases to fiscal cycles to extract discounts and frequently push for vendor financing or staggered licensing when budgets are constrained.

- Budget volatility: tag=US_FY2024_858B

- Global spend: tag=SIPRI_2023_2.24T

- Sanctions impact: tag=US_EntityList_2021

- Procurement leverage: tag=vendor_financing

Few giant state buyers, > $1M lumpy deals, 3–5yr re-bids compress margins

Customers are few, large state agencies with multi-million-dollar, lumpy deals (> $1M) and strong procurement leverage that forces performance milestones and concessions. High switching friction from workflow integration is offset by 3–5 year re-bids, in-house build alternatives and US 2021 Entity List sanctions that limit eligible buyers. Detection risks and continuous R&D compress margins and trigger credits or terminations.

| Metric | Value |

|---|---|

| Deal size | > $1M |

| US defense budget FY2024 | $858B |

| Global military spend 2023 (SIPRI) | $2.24T |

Preview Before You Purchase

NSO Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of NSO Group evaluates industry rivalry, supplier and buyer power, threat of substitutes, and entry barriers to clarify strategic pressures and value drivers. The preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or samples. It’s ready for download and use the moment you buy. The analysis is concise, actionable, and designed for immediate application.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

NSO Group faces intense supplier and regulatory pressure, high buyer scrutiny, moderate competitive rivalry from specialized cybersecurity firms, and a growing threat of substitutes via privacy-preserving tools. This Porter's Five Forces snapshot highlights key strategic risks and levers for value capture. Ready for deeper, force-by-force ratings, visuals, and actionable recommendations? Unlock the full analysis to inform investment and strategy decisions.

Suppliers Bargaining Power

Scarce zero-day exploit brokers

Access to high-quality undisclosed vulnerabilities is limited and costly, with broker payout listings (Zerodium) showing up to $2.5 million for high-end zero-click iOS exploits. That market leverage lets brokers dictate pricing and terms, and NSO depends on a steady pipeline of such reliable exploits to evade platform patches. Brokers can prioritize buyers or bundle deals, raising costs and dependence. Sanctions and disruptions (NSO was added to the US Entity List in Nov 2021) can directly impair product efficacy.

Elite security research talent

The market for top reverse engineers and offensive researchers is extremely tight, with the global cybersecurity workforce gap around 3.4 million in recent industry reports, giving this talent significant bargaining power.

Compensation and equity demands—often driving total pay packages above $300,000 for senior specialists—plus IP ownership terms can materially escalate costs for NSO.

Retention risk is high as competitors and state labs court the same experts; knowledge walkout can delay product roadmaps and lengthen maintenance cycles by months.

Platform and device ecosystem gatekeepers

Apple, Google and chipset vendors act as de facto suppliers of attack surface via their OS and hardware designs, controlling over 99% of global smartphone platforms. Rapid security hardening, lockdown modes and monthly patch cadences raise exploitation development costs and cut exploit shelf life to weeks. Vendors can litigate, notify targets and coordinate patches, increasing NSO’s operational burden. This dynamic compresses value-capture windows and amplifies platform-owner power.

Cloud, tooling, and infrastructure inputs

Specialized servers, C2 infrastructure, code-signing and telemetry tooling give suppliers leverage over NSO; major cloud providers held about 32% (AWS), 22% (Azure) and 12% (Google) of the IaaS/PaaS market in 2024, tightening KYC and abuse-detection which can force costly reconfigurations. Deplatforming raises switching and compliance costs and vendors can price in reputational or legal risk.

- High supplier concentration: AWS/Azure/Google ~66% (2024)

- Tighter KYC raises integration costs

- Deplatforming elevates switching/compliance costs

- Vendors may add risk premiums to pricing

Legal, export-control, and compliance advisors

Regulatory counsel and export-license consultants determine NSO Groups market access by interpreting sanctions, human-rights due diligence, and export controls; their structuring advice often dictates contract terms and geographic scope. Heightened scrutiny raised advisory demand and fees—legal/compliance spend rose ~12% in 2024—so withdrawal of counsel can halt deals or specific jurisdictions.

- High influence: licensing + contract shaping

- 2024: compliance/legal spend +12%

- Risk: advisory withdrawal stalls sales/geographies

Supplier leverage: payouts $2.5M, workforce gap 3.4M

Suppliers (exploit brokers, top researchers, cloud vendors, OS makers, legal advisers) hold high leverage: Zerodium payouts up to $2.5M, cybersecurity workforce gap ~3.4M (2024), senior pay >$300k, and AWS/Azure/GCP ~66% IaaS share. Sanctions and deplatforming raise costs; compliance spend rose ~12% in 2024.

| Supplier | Metric (2024) |

|---|---|

| Exploit brokers | $2.5M max payout |

| Talent | 3.4M gap; >$300k pay |

| Cloud | AWS/Azure/GCP ~66% |

| Compliance | +12% spend |

What is included in the product

Uncovers key competitive drivers—supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry—tailored to NSO Group’s unique position to assess pricing power, profitability risks, regulatory pressures, and strategic vulnerabilities.

A concise one-sheet Porter's Five Forces for NSO Group—instantly visualized in a radar chart to clarify strategic pressures and regulatory risk, ready to drop into decks or adapt with your data for scenario comparisons.

Customers Bargaining Power

Concentrated government clientele

Customers are few, large state agencies with strong procurement leverage, often accounting for the majority of revenues; deal sizes are typically multi-million-dollar, often >$1M, and lumpy, enabling hard price and performance negotiations. Buyers insist on bespoke features, on-site training and strict support SLAs, raising delivery costs. Vendor concentration risk amplifies discount pressure and contract dependency.

High switching costs but credible alternatives

Integration into lawful process, chain-of-custody and analyst workflows creates strong stickiness for NSO, yet in 2024 many states prefer 3–5 year procurement cycles that trigger re-bids and pilot programs; this, plus viable in-house buildouts or vendor rotation, constrains pricing power despite high switching friction.

Regulatory and reputational constraints

Agencies face political oversight, audits and human-rights scrutiny that can delay or cancel purchases; as of 2024 the US Entity List designation of NSO remains a material barrier to sales. Buyers demand stringent safeguards, independent usage monitoring and kill-switches, shifting operational and legal risk onto the vendor via warranties and compliance covenants. Vendors have offered concessions such as price reductions and extended multi-year support to salvage deals.

Outcome-based performance demands

Procurement now demands demonstrable efficacy against hardened targets and minimal detectability, with buyers negotiating performance-based milestones, penalties, and service credits; the 2021 Pegasus leak of over 50,000 exposed numbers underscores detection risk and buyer leverage. False positives, detections, or patch-driven degradation commonly trigger credits or churn, forcing continuous improvement at tighter margins and shifting pricing toward milestone-based fees.

- Performance milestones tie up to material fee portions

- Detections/patches -> credits or contract termination

- Continuous R&D pressure compresses margins

Budget cyclicality and geopolitics

Defense and interior budgets are cyclic and politicized—US FY2024 defense discretionary funding was about 858 billion USD and global military expenditure was 2.24 trillion USD in 2023 (SIPRI), affecting timing and scale of NSO sales; sanctions and alliance constraints (NSO placed on US Commerce Entity List in 2021) limit eligible buyers and contract terms. Buyers time purchases to fiscal cycles to extract discounts and frequently push for vendor financing or staggered licensing when budgets are constrained.

- Budget volatility: tag=US_FY2024_858B

- Global spend: tag=SIPRI_2023_2.24T

- Sanctions impact: tag=US_EntityList_2021

- Procurement leverage: tag=vendor_financing

Few giant state buyers, > $1M lumpy deals, 3–5yr re-bids compress margins

Customers are few, large state agencies with multi-million-dollar, lumpy deals (> $1M) and strong procurement leverage that forces performance milestones and concessions. High switching friction from workflow integration is offset by 3–5 year re-bids, in-house build alternatives and US 2021 Entity List sanctions that limit eligible buyers. Detection risks and continuous R&D compress margins and trigger credits or terminations.

| Metric | Value |

|---|---|

| Deal size | > $1M |

| US defense budget FY2024 | $858B |

| Global military spend 2023 (SIPRI) | $2.24T |

Preview Before You Purchase

NSO Group Porter's Five Forces Analysis

This Porter's Five Forces analysis of NSO Group evaluates industry rivalry, supplier and buyer power, threat of substitutes, and entry barriers to clarify strategic pressures and value drivers. The preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or samples. It’s ready for download and use the moment you buy. The analysis is concise, actionable, and designed for immediate application.