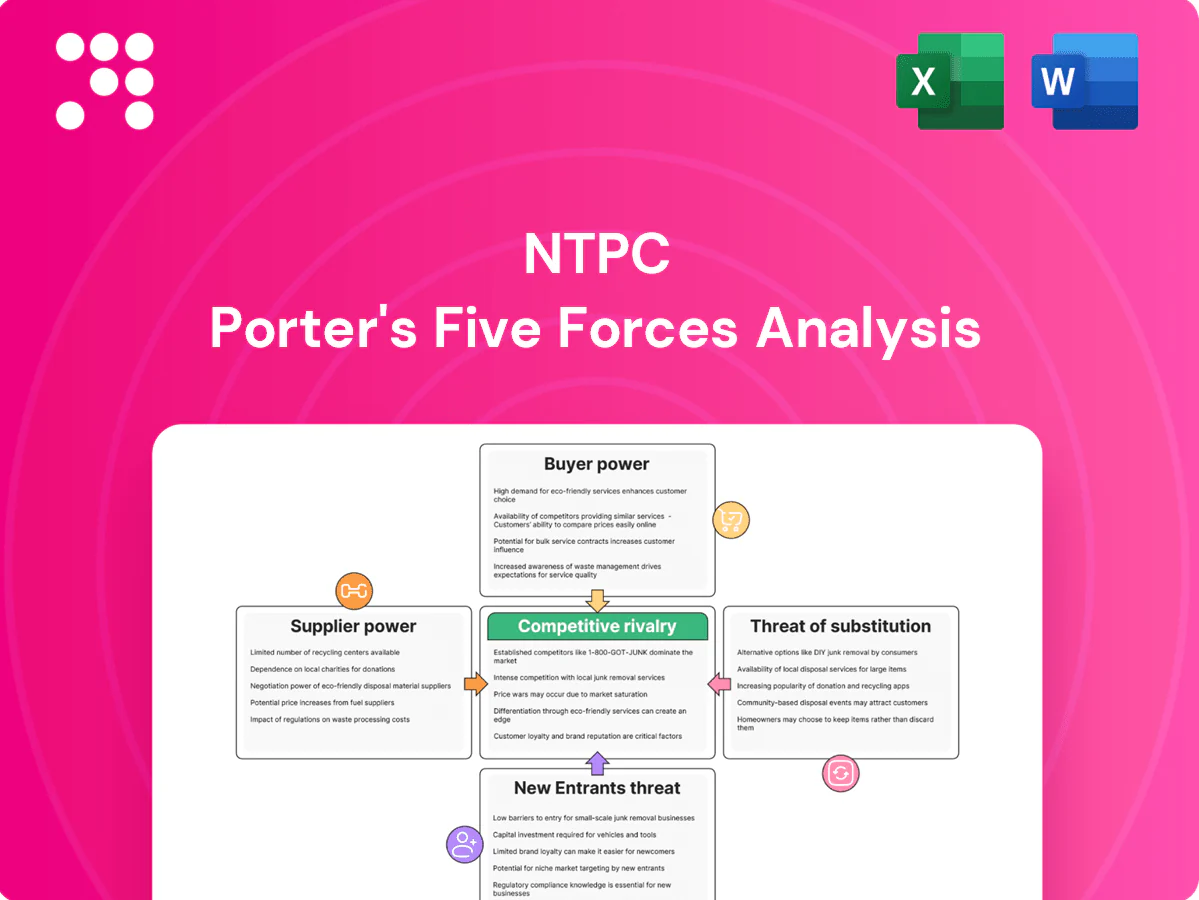

NTPC Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

NTPC faces moderate supplier power, regulated pricing pressures, and limited threat from substitutes but growing renewable competition; buyer power is muted by long-term contracts while industry rivalry hinges on capacity expansion and fuel costs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NTPC’s competitive dynamics in detail.

Suppliers Bargaining Power

Coal linkage and import dependency

NTPC’s thermal fleet sources over 60% of coal through Coal India linkages with roughly 10–15% met by imports, concentrating supplier leverage during domestic shortfalls; import-price swings in 2023–24 pushed landed coal costs up, squeezing margins despite tariff pass-through clauses; long-term fuel supply agreements cover base volumes but do not eliminate port, rail and mine logistics bottlenecks that can still trigger short-term supply shocks.

Rail and logistics constraints

Railways effectively act as a quasi-monopolistic logistics supplier for coal evacuation, with rake availability and freight tariff changes directly affecting NTPCs plant load factors and fuel costs. Disruptions in rail supply can curtail generation despite contracted coal volumes. NTPC mitigates this through pithead plants and blended sourcing strategies, but reliance on rail logistics remains a significant vulnerability.

OEMs and EPC vendors

For thermal, hydro and grid-scale renewables a concentrated set of OEMs/EPCs (turbines, boilers, inverters) gives suppliers strong bargaining power, especially where specialized spares and long-term service agreements are required. LTSAs commonly run 10–20 years, locking pricing and availability. NTPC’s use of scale-based tenders and multi-vendor panels improves leverage. India’s localization push since 2020 has broadened the renewables supplier base.

Renewable modules and storage

Solar module and battery prices are globally cyclical and policy-sensitive, with global solar module prices around $0.18–0.22/W in 2024 and battery pack prices at about $127/kWh (BNEF 2024). Import duties and ALMM norms raise costs and constrain supplier choice; NTPC uses bulk procurement to secure improved terms, though rapid tech shifts and periodic supply tightness can briefly increase supplier leverage.

- Prices 2024: modules ~$0.18–0.22/W; batteries ~$127/kWh

- Policy impact: import duties, ALMM

- NTPC: bulk procurement advantage

- Risk: tech shifts/supply tightness

Water, land, and environmental permits

Access to water, land, and environmental permits acts as a supplier constraint for NTPC, where scarcity or tighter norms raise compliance costs and can add months to project timelines; NTPC had roughly 72 GW of installed capacity in 2024, increasing the stakes for resource allocation. Delays shift leverage to contractors and can inflate capex, and NTPC’s central PSU status aids coordination but does not remove permitting risk.

- Resource constraint: water/land/permits

- 2024 scale: ~72 GW capacity

- Impact: higher compliance costs, delayed timelines

- Effect: increased contractor bargaining power

- Mitigation: PSU status helps but risk persists

Coal >60% CIL; imports 10–15% — import swings, rail rakes, module/battery costs pinch margins

NTPC sources >60% coal via Coal India linkages; imports 10–15%, 2023–24 import-price swings raised landed costs, squeezing margins.

Indian Railways' rake constraints and freight hikes act as a quasi-monopoly, affecting PLF despite long-term coal contracts.

OEM LTSAs and module/battery markets (modules $0.18–0.22/W; batteries $127/kWh in 2024) increase supplier leverage; bulk procurement helps.

| Metric | 2024 | Impact |

|---|---|---|

| Coal mix | >60% CIL, 10–15% imports | Supply risk, price exposure |

| Modules | $0.18–0.22/W | Procurement swings |

| Batteries | $127/kWh | Capex/Opex pressure |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry threats specific to NTPC, identifying substitutes and disruptive forces that challenge its market share and pricing power.

A clear, one-sheet summary of NTPC's five forces—ideal for swift strategic decisions, investor briefings, and spotting where regulatory or fuel-price pressures can be alleviated.

Customers Bargaining Power

State DISCOM dependence

NTPC’s primary customers remain state DISCOMs under long-term PPAs, creating high buyer concentration and political oversight that elevates buyer leverage; NTPC had ~72 GW capacity by Mar 2024 and relies heavily on these contracts. Persistent DISCOM dues—around Rs 1.5 lakh crore across the sector in 2024—cause payment delays that strain NTPC cash flows despite late-payment surcharge mechanisms. Credit enhancements and central pooling (e.g., PA/central guarantees) have reduced counterparty risk but have not eliminated default and liquidity exposure.

Tariff regulation and merit order

CERC/SERC tariff frameworks (RoE ~15.5% and strict pass-through rules) cap returns and limit NTPCs pricing discretion, while DISCOMs dispatch on merit order, favoring lower-variable-cost units and squeezing higher-cost coal stations. Buyers increasingly lean on cheaper renewables and short-term markets—India added ~40 GW renewables in 2023–24—pressuring baseload margins. NTPC offsets this with a ~75 GW diversified fleet, higher-efficiency plants and flexible contracts.

Auctions for new capacity

Competitive auctions for solar, wind and hybrid contracts have pushed average 2024 winning solar tariffs to about INR 2.20/kWh and wind-hybrid to ~INR 2.60/kWh, increasing buyer power as buyers benchmark NTPC against IPPs on tariff. Long-tenor PPAs (typically 25 years) still provide revenue visibility but compress margins, while NTPC’s ~72 GW scale and execution reliability help it win bids at competitive rates.

Switching and alternatives

Open access and power exchanges provide buyers optionality at the margin, letting DISCOMs source spot cheaper power; seasonal demand swings enable curtailment of higher‑cost supply. NTPC's diversified portfolio (~75 GW consolidated in 2024) spans peaking, baseload and renewables, helping retain share; customization and track record on reliability reduce switching.

- Open access optionality: marginal sourcing via exchanges

- Seasonality: DISCOMs curtail costly supply in low demand months

- NTPC ~75 GW (2024): peaking, baseload, renewables

- Customization + reliability mitigate buyer switch

Service and consultancy pricing

In consultancy/EPC services government and utilities run competitive tenders where buyers weigh price and track record, forcing aggressive bids; in 2024 many public tenders favored lowest evaluated offers. NTPC (≈72 GW capacity; FY2024 revenue ₹1.45 trillion) leverages brand and domain expertise but can only secure modest premiums—EPC margins commonly 5–8%. Outcome-based KPIs tie payments to performance, keeping margins disciplined.

- Buyers: price + track record

- NTPC: strong brand, limited premium

- Margins: typically 5–8%; KPI-linked

DISCOM leverage and renewables squeeze cash flows of large power generator

NTPC customers (mainly DISCOMs) wield strong leverage via high buyer concentration, regulatory tariffs (CERC RoE ~15.5%) and dues (~Rs 1.5 lakh crore sectoral arrears in 2024), pressuring cash flows and margins. Competitive renewables (2023–24 additions ~40 GW; solar ~Rs 2.20/kWh) and exchanges increase buyer optionality. NTPC scale (~72–75 GW, FY24 revenue ₹1.45 tn) and reliability limit but do not eliminate buyer power.

| Metric | 2024 |

|---|---|

| Capacity | 72–75 GW |

| Revenue | ₹1.45 tn |

| DISCOM dues | ~₹1.5 lakh crore |

| Solar tariff | ~₹2.20/kWh |

| CERC RoE | ~15.5% |

What You See Is What You Get

NTPC Porter's Five Forces Analysis

This NTPC Porter's Five Forces Analysis assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to India's power sector, highlighting regulatory risks and scale advantages. It identifies strategic implications and actionable recommendations for investors and managers. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, no surprises.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

NTPC faces moderate supplier power, regulated pricing pressures, and limited threat from substitutes but growing renewable competition; buyer power is muted by long-term contracts while industry rivalry hinges on capacity expansion and fuel costs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NTPC’s competitive dynamics in detail.

Suppliers Bargaining Power

Coal linkage and import dependency

NTPC’s thermal fleet sources over 60% of coal through Coal India linkages with roughly 10–15% met by imports, concentrating supplier leverage during domestic shortfalls; import-price swings in 2023–24 pushed landed coal costs up, squeezing margins despite tariff pass-through clauses; long-term fuel supply agreements cover base volumes but do not eliminate port, rail and mine logistics bottlenecks that can still trigger short-term supply shocks.

Rail and logistics constraints

Railways effectively act as a quasi-monopolistic logistics supplier for coal evacuation, with rake availability and freight tariff changes directly affecting NTPCs plant load factors and fuel costs. Disruptions in rail supply can curtail generation despite contracted coal volumes. NTPC mitigates this through pithead plants and blended sourcing strategies, but reliance on rail logistics remains a significant vulnerability.

OEMs and EPC vendors

For thermal, hydro and grid-scale renewables a concentrated set of OEMs/EPCs (turbines, boilers, inverters) gives suppliers strong bargaining power, especially where specialized spares and long-term service agreements are required. LTSAs commonly run 10–20 years, locking pricing and availability. NTPC’s use of scale-based tenders and multi-vendor panels improves leverage. India’s localization push since 2020 has broadened the renewables supplier base.

Renewable modules and storage

Solar module and battery prices are globally cyclical and policy-sensitive, with global solar module prices around $0.18–0.22/W in 2024 and battery pack prices at about $127/kWh (BNEF 2024). Import duties and ALMM norms raise costs and constrain supplier choice; NTPC uses bulk procurement to secure improved terms, though rapid tech shifts and periodic supply tightness can briefly increase supplier leverage.

- Prices 2024: modules ~$0.18–0.22/W; batteries ~$127/kWh

- Policy impact: import duties, ALMM

- NTPC: bulk procurement advantage

- Risk: tech shifts/supply tightness

Water, land, and environmental permits

Access to water, land, and environmental permits acts as a supplier constraint for NTPC, where scarcity or tighter norms raise compliance costs and can add months to project timelines; NTPC had roughly 72 GW of installed capacity in 2024, increasing the stakes for resource allocation. Delays shift leverage to contractors and can inflate capex, and NTPC’s central PSU status aids coordination but does not remove permitting risk.

- Resource constraint: water/land/permits

- 2024 scale: ~72 GW capacity

- Impact: higher compliance costs, delayed timelines

- Effect: increased contractor bargaining power

- Mitigation: PSU status helps but risk persists

Coal >60% CIL; imports 10–15% — import swings, rail rakes, module/battery costs pinch margins

NTPC sources >60% coal via Coal India linkages; imports 10–15%, 2023–24 import-price swings raised landed costs, squeezing margins.

Indian Railways' rake constraints and freight hikes act as a quasi-monopoly, affecting PLF despite long-term coal contracts.

OEM LTSAs and module/battery markets (modules $0.18–0.22/W; batteries $127/kWh in 2024) increase supplier leverage; bulk procurement helps.

| Metric | 2024 | Impact |

|---|---|---|

| Coal mix | >60% CIL, 10–15% imports | Supply risk, price exposure |

| Modules | $0.18–0.22/W | Procurement swings |

| Batteries | $127/kWh | Capex/Opex pressure |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry threats specific to NTPC, identifying substitutes and disruptive forces that challenge its market share and pricing power.

A clear, one-sheet summary of NTPC's five forces—ideal for swift strategic decisions, investor briefings, and spotting where regulatory or fuel-price pressures can be alleviated.

Customers Bargaining Power

State DISCOM dependence

NTPC’s primary customers remain state DISCOMs under long-term PPAs, creating high buyer concentration and political oversight that elevates buyer leverage; NTPC had ~72 GW capacity by Mar 2024 and relies heavily on these contracts. Persistent DISCOM dues—around Rs 1.5 lakh crore across the sector in 2024—cause payment delays that strain NTPC cash flows despite late-payment surcharge mechanisms. Credit enhancements and central pooling (e.g., PA/central guarantees) have reduced counterparty risk but have not eliminated default and liquidity exposure.

Tariff regulation and merit order

CERC/SERC tariff frameworks (RoE ~15.5% and strict pass-through rules) cap returns and limit NTPCs pricing discretion, while DISCOMs dispatch on merit order, favoring lower-variable-cost units and squeezing higher-cost coal stations. Buyers increasingly lean on cheaper renewables and short-term markets—India added ~40 GW renewables in 2023–24—pressuring baseload margins. NTPC offsets this with a ~75 GW diversified fleet, higher-efficiency plants and flexible contracts.

Auctions for new capacity

Competitive auctions for solar, wind and hybrid contracts have pushed average 2024 winning solar tariffs to about INR 2.20/kWh and wind-hybrid to ~INR 2.60/kWh, increasing buyer power as buyers benchmark NTPC against IPPs on tariff. Long-tenor PPAs (typically 25 years) still provide revenue visibility but compress margins, while NTPC’s ~72 GW scale and execution reliability help it win bids at competitive rates.

Switching and alternatives

Open access and power exchanges provide buyers optionality at the margin, letting DISCOMs source spot cheaper power; seasonal demand swings enable curtailment of higher‑cost supply. NTPC's diversified portfolio (~75 GW consolidated in 2024) spans peaking, baseload and renewables, helping retain share; customization and track record on reliability reduce switching.

- Open access optionality: marginal sourcing via exchanges

- Seasonality: DISCOMs curtail costly supply in low demand months

- NTPC ~75 GW (2024): peaking, baseload, renewables

- Customization + reliability mitigate buyer switch

Service and consultancy pricing

In consultancy/EPC services government and utilities run competitive tenders where buyers weigh price and track record, forcing aggressive bids; in 2024 many public tenders favored lowest evaluated offers. NTPC (≈72 GW capacity; FY2024 revenue ₹1.45 trillion) leverages brand and domain expertise but can only secure modest premiums—EPC margins commonly 5–8%. Outcome-based KPIs tie payments to performance, keeping margins disciplined.

- Buyers: price + track record

- NTPC: strong brand, limited premium

- Margins: typically 5–8%; KPI-linked

DISCOM leverage and renewables squeeze cash flows of large power generator

NTPC customers (mainly DISCOMs) wield strong leverage via high buyer concentration, regulatory tariffs (CERC RoE ~15.5%) and dues (~Rs 1.5 lakh crore sectoral arrears in 2024), pressuring cash flows and margins. Competitive renewables (2023–24 additions ~40 GW; solar ~Rs 2.20/kWh) and exchanges increase buyer optionality. NTPC scale (~72–75 GW, FY24 revenue ₹1.45 tn) and reliability limit but do not eliminate buyer power.

| Metric | 2024 |

|---|---|

| Capacity | 72–75 GW |

| Revenue | ₹1.45 tn |

| DISCOM dues | ~₹1.5 lakh crore |

| Solar tariff | ~₹2.20/kWh |

| CERC RoE | ~15.5% |

What You See Is What You Get

NTPC Porter's Five Forces Analysis

This NTPC Porter's Five Forces Analysis assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to India's power sector, highlighting regulatory risks and scale advantages. It identifies strategic implications and actionable recommendations for investors and managers. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, no surprises.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

NTPC faces moderate supplier power, regulated pricing pressures, and limited threat from substitutes but growing renewable competition; buyer power is muted by long-term contracts while industry rivalry hinges on capacity expansion and fuel costs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NTPC’s competitive dynamics in detail.

Suppliers Bargaining Power

Coal linkage and import dependency

NTPC’s thermal fleet sources over 60% of coal through Coal India linkages with roughly 10–15% met by imports, concentrating supplier leverage during domestic shortfalls; import-price swings in 2023–24 pushed landed coal costs up, squeezing margins despite tariff pass-through clauses; long-term fuel supply agreements cover base volumes but do not eliminate port, rail and mine logistics bottlenecks that can still trigger short-term supply shocks.

Rail and logistics constraints

Railways effectively act as a quasi-monopolistic logistics supplier for coal evacuation, with rake availability and freight tariff changes directly affecting NTPCs plant load factors and fuel costs. Disruptions in rail supply can curtail generation despite contracted coal volumes. NTPC mitigates this through pithead plants and blended sourcing strategies, but reliance on rail logistics remains a significant vulnerability.

OEMs and EPC vendors

For thermal, hydro and grid-scale renewables a concentrated set of OEMs/EPCs (turbines, boilers, inverters) gives suppliers strong bargaining power, especially where specialized spares and long-term service agreements are required. LTSAs commonly run 10–20 years, locking pricing and availability. NTPC’s use of scale-based tenders and multi-vendor panels improves leverage. India’s localization push since 2020 has broadened the renewables supplier base.

Renewable modules and storage

Solar module and battery prices are globally cyclical and policy-sensitive, with global solar module prices around $0.18–0.22/W in 2024 and battery pack prices at about $127/kWh (BNEF 2024). Import duties and ALMM norms raise costs and constrain supplier choice; NTPC uses bulk procurement to secure improved terms, though rapid tech shifts and periodic supply tightness can briefly increase supplier leverage.

- Prices 2024: modules ~$0.18–0.22/W; batteries ~$127/kWh

- Policy impact: import duties, ALMM

- NTPC: bulk procurement advantage

- Risk: tech shifts/supply tightness

Water, land, and environmental permits

Access to water, land, and environmental permits acts as a supplier constraint for NTPC, where scarcity or tighter norms raise compliance costs and can add months to project timelines; NTPC had roughly 72 GW of installed capacity in 2024, increasing the stakes for resource allocation. Delays shift leverage to contractors and can inflate capex, and NTPC’s central PSU status aids coordination but does not remove permitting risk.

- Resource constraint: water/land/permits

- 2024 scale: ~72 GW capacity

- Impact: higher compliance costs, delayed timelines

- Effect: increased contractor bargaining power

- Mitigation: PSU status helps but risk persists

Coal >60% CIL; imports 10–15% — import swings, rail rakes, module/battery costs pinch margins

NTPC sources >60% coal via Coal India linkages; imports 10–15%, 2023–24 import-price swings raised landed costs, squeezing margins.

Indian Railways' rake constraints and freight hikes act as a quasi-monopoly, affecting PLF despite long-term coal contracts.

OEM LTSAs and module/battery markets (modules $0.18–0.22/W; batteries $127/kWh in 2024) increase supplier leverage; bulk procurement helps.

| Metric | 2024 | Impact |

|---|---|---|

| Coal mix | >60% CIL, 10–15% imports | Supply risk, price exposure |

| Modules | $0.18–0.22/W | Procurement swings |

| Batteries | $127/kWh | Capex/Opex pressure |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, and entry threats specific to NTPC, identifying substitutes and disruptive forces that challenge its market share and pricing power.

A clear, one-sheet summary of NTPC's five forces—ideal for swift strategic decisions, investor briefings, and spotting where regulatory or fuel-price pressures can be alleviated.

Customers Bargaining Power

State DISCOM dependence

NTPC’s primary customers remain state DISCOMs under long-term PPAs, creating high buyer concentration and political oversight that elevates buyer leverage; NTPC had ~72 GW capacity by Mar 2024 and relies heavily on these contracts. Persistent DISCOM dues—around Rs 1.5 lakh crore across the sector in 2024—cause payment delays that strain NTPC cash flows despite late-payment surcharge mechanisms. Credit enhancements and central pooling (e.g., PA/central guarantees) have reduced counterparty risk but have not eliminated default and liquidity exposure.

Tariff regulation and merit order

CERC/SERC tariff frameworks (RoE ~15.5% and strict pass-through rules) cap returns and limit NTPCs pricing discretion, while DISCOMs dispatch on merit order, favoring lower-variable-cost units and squeezing higher-cost coal stations. Buyers increasingly lean on cheaper renewables and short-term markets—India added ~40 GW renewables in 2023–24—pressuring baseload margins. NTPC offsets this with a ~75 GW diversified fleet, higher-efficiency plants and flexible contracts.

Auctions for new capacity

Competitive auctions for solar, wind and hybrid contracts have pushed average 2024 winning solar tariffs to about INR 2.20/kWh and wind-hybrid to ~INR 2.60/kWh, increasing buyer power as buyers benchmark NTPC against IPPs on tariff. Long-tenor PPAs (typically 25 years) still provide revenue visibility but compress margins, while NTPC’s ~72 GW scale and execution reliability help it win bids at competitive rates.

Switching and alternatives

Open access and power exchanges provide buyers optionality at the margin, letting DISCOMs source spot cheaper power; seasonal demand swings enable curtailment of higher‑cost supply. NTPC's diversified portfolio (~75 GW consolidated in 2024) spans peaking, baseload and renewables, helping retain share; customization and track record on reliability reduce switching.

- Open access optionality: marginal sourcing via exchanges

- Seasonality: DISCOMs curtail costly supply in low demand months

- NTPC ~75 GW (2024): peaking, baseload, renewables

- Customization + reliability mitigate buyer switch

Service and consultancy pricing

In consultancy/EPC services government and utilities run competitive tenders where buyers weigh price and track record, forcing aggressive bids; in 2024 many public tenders favored lowest evaluated offers. NTPC (≈72 GW capacity; FY2024 revenue ₹1.45 trillion) leverages brand and domain expertise but can only secure modest premiums—EPC margins commonly 5–8%. Outcome-based KPIs tie payments to performance, keeping margins disciplined.

- Buyers: price + track record

- NTPC: strong brand, limited premium

- Margins: typically 5–8%; KPI-linked

DISCOM leverage and renewables squeeze cash flows of large power generator

NTPC customers (mainly DISCOMs) wield strong leverage via high buyer concentration, regulatory tariffs (CERC RoE ~15.5%) and dues (~Rs 1.5 lakh crore sectoral arrears in 2024), pressuring cash flows and margins. Competitive renewables (2023–24 additions ~40 GW; solar ~Rs 2.20/kWh) and exchanges increase buyer optionality. NTPC scale (~72–75 GW, FY24 revenue ₹1.45 tn) and reliability limit but do not eliminate buyer power.

| Metric | 2024 |

|---|---|

| Capacity | 72–75 GW |

| Revenue | ₹1.45 tn |

| DISCOM dues | ~₹1.5 lakh crore |

| Solar tariff | ~₹2.20/kWh |

| CERC RoE | ~15.5% |

What You See Is What You Get

NTPC Porter's Five Forces Analysis

This NTPC Porter's Five Forces Analysis assesses competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry specific to India's power sector, highlighting regulatory risks and scale advantages. It identifies strategic implications and actionable recommendations for investors and managers. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, no surprises.