NTT DATA Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

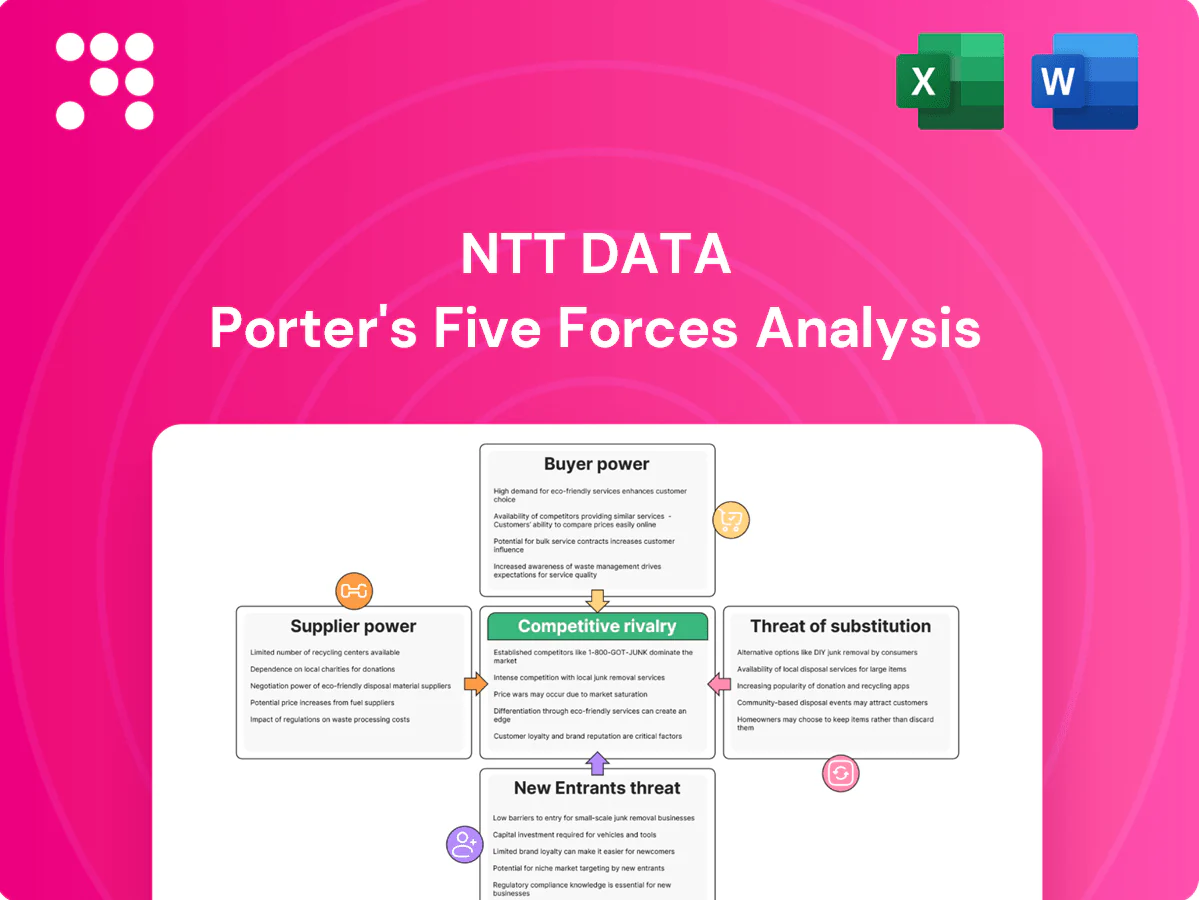

NTT DATA faces moderate buyer power, strong supplier partnerships, intense rivalry among global IT services firms, moderate threat of substitutes, and meaningful barriers that limit new entrants but not disruption. This snapshot highlights key competitive pressures and strategic levers. The complete report reveals the real forces shaping NTT DATA’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on hyperscalers

NTT DATA relies on AWS, Microsoft Azure and Google Cloud for core infrastructure services and certifications, with those hyperscalers holding roughly AWS 32%, Azure 23% and Google Cloud 11% of global cloud infrastructure market share (Canalys 2024). Hyperscalers’ pricing moves, partner tiers and roadmap shifts directly affect NTT DATA’s margins and solution design. Co-sell incentives and rebate programs partially rebalance bargaining power but deepen dependency. Multi‑cloud diversification reduces single‑vendor risk but does not eliminate hyperscaler leverage.

Strategic software vendors

Relationships with SAP, Oracle, Microsoft, Salesforce and ServiceNow govern license access and delivery accreditation and thus are strategic bottlenecks; Microsoft Azure held ~23% and AWS ~32% of IaaS share in 2024 while Salesforce accounted for roughly 30% of CRM market share in 2024. Vendor-controlled certification and partner rebates materially affect project margins; roadmap and support policies can force upgrades/reimplementation, whereas co-innovation agreements reduce deployment risk and increase deal flow.

Talent as the primary input

Skilled labor is NTT DATA’s primary supplier: a global cybersecurity workforce gap of about 3.4 million (ISC2) and continued AI/cloud skill scarcity drive wage inflation (tech wages rose roughly 6% in 2023–24), pushing delivery costs higher. Certification premiums and attrition (industry attrition around 20–25%) inflate project staffing bills. Global delivery centers cushion cost spikes but do not eliminate scarcity. Strong employer branding and upskilling programs materially reduce churn pressure.

Niche tech and data providers

Specialist API, data and cybersecurity vendors can exert outsized leverage on specific NTT DATA deals, especially where bespoke integrations create material switching costs and mid-project lock-in; the global cybersecurity market was about 217 billion USD in 2024, underscoring vendor concentration in high-value niches. Volume across these suppliers is fragmented, limiting systemic risk, while framework agreements and multi-sourcing are commonly used to reduce single-point exposure.

- Vendor leverage: high on niche APIs/data/cyber

- Switching costs: material mid-project

- Systemic risk: limited by fragmentation

- Mitigation: framework deals + multi-sourcing

Subcontractors and partners

Subcontractors and boutique staff-augmentation partners provide surge capacity and specialized domain skills, but 2024 peak-demand cycles still show measurable rate volatility that can compress project margins; preferred-vendor lists and long-term MSAs help stabilize commercial terms, while robust vendor management limits delivery risk and cost creep.

- Surge capacity: staff-augmentation partners

- Rate volatility: compresses margins in peaks

- Stabilizers: preferred vendors and long-term MSAs

- Controls: vendor management reduces delivery risk and cost creep

Concentrated cloud power, skilled-labor gap 3.4M and wages +6% squeeze margins

Hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024) and specialist vendors exert high pricing and roadmap leverage; skilled‑labor gap ~3.4M (ISC2) and tech wages +6% (2023–24) raise delivery costs. Multi‑cloud, MSAs and co‑sell deals mitigate but do not remove supplier power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | AWS32%/Azure23%/GCP11% | High leverage |

| Skilled labor | Gap 3.4M; wages +6% | Higher costs |

| Cyber vendors | Market $217B | Outsized niche power |

What is included in the product

Tailored exclusively for NTT DATA, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, and market entry barriers that protect incumbents; it also identifies disruptive threats and substitutes that could erode market share and strategic recommendations to strengthen NTT DATA’s position.

A concise one-sheet Porter’s Five Forces for NTT DATA that instantly visualizes competitive pressure with customizable spider charts, no macros, and a clean slides-ready layout—swap in your data, duplicate scenarios, and embed into dashboards or the companion Word report for rapid strategic decisions.

Customers Bargaining Power

Large enterprise procurement

Large enterprise procurement drives heavy price pressure on NTT DATA: the global IT services market reached about $1.2 trillion in 2024 and 60% of global clients pursue vendor consolidation and rigorous RFP benchmarking. Multi-year, multi-tower deals, which account for roughly 40% of large outsourcing spend, amplify buyer leverage. Outcome-based and gainshare models appear in about 30% of major contracts, shifting risk to providers, though strong referenceability and proven outcomes can partially offset required discounts.

Switching costs vs. multi-vendor

Integration knowledge and embedded NTT DATA teams create significant mid-contract switching costs that reduce buyer leverage, while many clients still dual-source to keep competition active. According to Flexera 2024 State of the Cloud Report, 98% of enterprises use multi-cloud/multi-vendor strategies, which sustains supplier competition. Modular architectures and APIs gradually lower lock-in, and typical IT services contracts (commonly 3–5 year terms) make renewal cycles the primary moments of pricing tension.

Demand for measurable outcomes

Clients now demand measurable ROI from digital transformation, cloud migration and AI, with 2024 surveys showing over 56% of enterprises requiring clear payback timelines. SLAs, KPIs and financial penalties are increasingly standard, raising accountability and shortening remediation cycles. Strong value articulation and industry-specific IP boost NTT DATAs pricing power. Poor outcomes trigger rapid scope cuts or re-bids, often within months.

Insourcing and captives

Some enterprises build captives or expand internal tech teams to reduce vendor reliance, giving buyers a credible alternative in negotiations and pressuring margins; in 2024 this trend intensified among large firms shifting to hybrid sourcing. NTT DATA must therefore sell higher-value services beyond commodity delivery, emphasizing IP, outcome-based contracts and industry expertise. Co-managed models and managed services can neutralize full insourcing threats by offering shared governance and cost transparency.

Security and compliance requirements

Buyers impose stringent data, sovereignty, and regulatory standards, with 2024 surveys showing about 65% of enterprises prioritise local data residency; this raises delivery costs and narrows vendor pools. Meeting advanced requirements allows NTT DATA to justify premium pricing, while breaches or audit failures rapidly erode bargaining position and revenue.

- Compliance-driven cost uplift: higher delivery margins

- Vendor shortlist shrinkage: fewer qualified bidders

- Premium pricing justification: advanced certifications

- Risk: breaches/audit failures → swift loss of trust

Enterprise buyers squeeze IT margins — 60% consolidation, 98% multi-cloud

Enterprise buyers exert strong price and risk pressure on NTT DATA: 2024 global IT services ~$1.2T, 60% seek vendor consolidation and 40% of large outsourcing is multi-tower, boosting buyer leverage. Multi-cloud (98%) and modular architectures reduce lock-in, though embedded teams raise switching costs. Outcome-based deals (≈30%) and ROI demands (56%) intensify performance-linked pricing; 65% prioritize data residency, enabling premium for compliant vendors.

| Metric | 2024 Value |

|---|---|

| Global IT services | $1.2T |

| Clients seeking consolidation | 60% |

| Multi-tower spend | 40% |

| Outcome-based deals | 30% |

| Multi-cloud adoption | 98% |

| Require ROI timelines | 56% |

| Data residency priority | 65% |

Preview Before You Purchase

NTT DATA Porter's Five Forces Analysis

This preview shows the exact NTT DATA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final document and will get instant access to this same deliverable.

A Must-Have Tool for Decision-Makers

NTT DATA faces moderate buyer power, strong supplier partnerships, intense rivalry among global IT services firms, moderate threat of substitutes, and meaningful barriers that limit new entrants but not disruption. This snapshot highlights key competitive pressures and strategic levers. The complete report reveals the real forces shaping NTT DATA’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on hyperscalers

NTT DATA relies on AWS, Microsoft Azure and Google Cloud for core infrastructure services and certifications, with those hyperscalers holding roughly AWS 32%, Azure 23% and Google Cloud 11% of global cloud infrastructure market share (Canalys 2024). Hyperscalers’ pricing moves, partner tiers and roadmap shifts directly affect NTT DATA’s margins and solution design. Co-sell incentives and rebate programs partially rebalance bargaining power but deepen dependency. Multi‑cloud diversification reduces single‑vendor risk but does not eliminate hyperscaler leverage.

Strategic software vendors

Relationships with SAP, Oracle, Microsoft, Salesforce and ServiceNow govern license access and delivery accreditation and thus are strategic bottlenecks; Microsoft Azure held ~23% and AWS ~32% of IaaS share in 2024 while Salesforce accounted for roughly 30% of CRM market share in 2024. Vendor-controlled certification and partner rebates materially affect project margins; roadmap and support policies can force upgrades/reimplementation, whereas co-innovation agreements reduce deployment risk and increase deal flow.

Talent as the primary input

Skilled labor is NTT DATA’s primary supplier: a global cybersecurity workforce gap of about 3.4 million (ISC2) and continued AI/cloud skill scarcity drive wage inflation (tech wages rose roughly 6% in 2023–24), pushing delivery costs higher. Certification premiums and attrition (industry attrition around 20–25%) inflate project staffing bills. Global delivery centers cushion cost spikes but do not eliminate scarcity. Strong employer branding and upskilling programs materially reduce churn pressure.

Niche tech and data providers

Specialist API, data and cybersecurity vendors can exert outsized leverage on specific NTT DATA deals, especially where bespoke integrations create material switching costs and mid-project lock-in; the global cybersecurity market was about 217 billion USD in 2024, underscoring vendor concentration in high-value niches. Volume across these suppliers is fragmented, limiting systemic risk, while framework agreements and multi-sourcing are commonly used to reduce single-point exposure.

- Vendor leverage: high on niche APIs/data/cyber

- Switching costs: material mid-project

- Systemic risk: limited by fragmentation

- Mitigation: framework deals + multi-sourcing

Subcontractors and partners

Subcontractors and boutique staff-augmentation partners provide surge capacity and specialized domain skills, but 2024 peak-demand cycles still show measurable rate volatility that can compress project margins; preferred-vendor lists and long-term MSAs help stabilize commercial terms, while robust vendor management limits delivery risk and cost creep.

- Surge capacity: staff-augmentation partners

- Rate volatility: compresses margins in peaks

- Stabilizers: preferred vendors and long-term MSAs

- Controls: vendor management reduces delivery risk and cost creep

Concentrated cloud power, skilled-labor gap 3.4M and wages +6% squeeze margins

Hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024) and specialist vendors exert high pricing and roadmap leverage; skilled‑labor gap ~3.4M (ISC2) and tech wages +6% (2023–24) raise delivery costs. Multi‑cloud, MSAs and co‑sell deals mitigate but do not remove supplier power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | AWS32%/Azure23%/GCP11% | High leverage |

| Skilled labor | Gap 3.4M; wages +6% | Higher costs |

| Cyber vendors | Market $217B | Outsized niche power |

What is included in the product

Tailored exclusively for NTT DATA, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, and market entry barriers that protect incumbents; it also identifies disruptive threats and substitutes that could erode market share and strategic recommendations to strengthen NTT DATA’s position.

A concise one-sheet Porter’s Five Forces for NTT DATA that instantly visualizes competitive pressure with customizable spider charts, no macros, and a clean slides-ready layout—swap in your data, duplicate scenarios, and embed into dashboards or the companion Word report for rapid strategic decisions.

Customers Bargaining Power

Large enterprise procurement

Large enterprise procurement drives heavy price pressure on NTT DATA: the global IT services market reached about $1.2 trillion in 2024 and 60% of global clients pursue vendor consolidation and rigorous RFP benchmarking. Multi-year, multi-tower deals, which account for roughly 40% of large outsourcing spend, amplify buyer leverage. Outcome-based and gainshare models appear in about 30% of major contracts, shifting risk to providers, though strong referenceability and proven outcomes can partially offset required discounts.

Switching costs vs. multi-vendor

Integration knowledge and embedded NTT DATA teams create significant mid-contract switching costs that reduce buyer leverage, while many clients still dual-source to keep competition active. According to Flexera 2024 State of the Cloud Report, 98% of enterprises use multi-cloud/multi-vendor strategies, which sustains supplier competition. Modular architectures and APIs gradually lower lock-in, and typical IT services contracts (commonly 3–5 year terms) make renewal cycles the primary moments of pricing tension.

Demand for measurable outcomes

Clients now demand measurable ROI from digital transformation, cloud migration and AI, with 2024 surveys showing over 56% of enterprises requiring clear payback timelines. SLAs, KPIs and financial penalties are increasingly standard, raising accountability and shortening remediation cycles. Strong value articulation and industry-specific IP boost NTT DATAs pricing power. Poor outcomes trigger rapid scope cuts or re-bids, often within months.

Insourcing and captives

Some enterprises build captives or expand internal tech teams to reduce vendor reliance, giving buyers a credible alternative in negotiations and pressuring margins; in 2024 this trend intensified among large firms shifting to hybrid sourcing. NTT DATA must therefore sell higher-value services beyond commodity delivery, emphasizing IP, outcome-based contracts and industry expertise. Co-managed models and managed services can neutralize full insourcing threats by offering shared governance and cost transparency.

Security and compliance requirements

Buyers impose stringent data, sovereignty, and regulatory standards, with 2024 surveys showing about 65% of enterprises prioritise local data residency; this raises delivery costs and narrows vendor pools. Meeting advanced requirements allows NTT DATA to justify premium pricing, while breaches or audit failures rapidly erode bargaining position and revenue.

- Compliance-driven cost uplift: higher delivery margins

- Vendor shortlist shrinkage: fewer qualified bidders

- Premium pricing justification: advanced certifications

- Risk: breaches/audit failures → swift loss of trust

Enterprise buyers squeeze IT margins — 60% consolidation, 98% multi-cloud

Enterprise buyers exert strong price and risk pressure on NTT DATA: 2024 global IT services ~$1.2T, 60% seek vendor consolidation and 40% of large outsourcing is multi-tower, boosting buyer leverage. Multi-cloud (98%) and modular architectures reduce lock-in, though embedded teams raise switching costs. Outcome-based deals (≈30%) and ROI demands (56%) intensify performance-linked pricing; 65% prioritize data residency, enabling premium for compliant vendors.

| Metric | 2024 Value |

|---|---|

| Global IT services | $1.2T |

| Clients seeking consolidation | 60% |

| Multi-tower spend | 40% |

| Outcome-based deals | 30% |

| Multi-cloud adoption | 98% |

| Require ROI timelines | 56% |

| Data residency priority | 65% |

Preview Before You Purchase

NTT DATA Porter's Five Forces Analysis

This preview shows the exact NTT DATA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final document and will get instant access to this same deliverable.

Description

A Must-Have Tool for Decision-Makers

NTT DATA faces moderate buyer power, strong supplier partnerships, intense rivalry among global IT services firms, moderate threat of substitutes, and meaningful barriers that limit new entrants but not disruption. This snapshot highlights key competitive pressures and strategic levers. The complete report reveals the real forces shaping NTT DATA’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Dependence on hyperscalers

NTT DATA relies on AWS, Microsoft Azure and Google Cloud for core infrastructure services and certifications, with those hyperscalers holding roughly AWS 32%, Azure 23% and Google Cloud 11% of global cloud infrastructure market share (Canalys 2024). Hyperscalers’ pricing moves, partner tiers and roadmap shifts directly affect NTT DATA’s margins and solution design. Co-sell incentives and rebate programs partially rebalance bargaining power but deepen dependency. Multi‑cloud diversification reduces single‑vendor risk but does not eliminate hyperscaler leverage.

Strategic software vendors

Relationships with SAP, Oracle, Microsoft, Salesforce and ServiceNow govern license access and delivery accreditation and thus are strategic bottlenecks; Microsoft Azure held ~23% and AWS ~32% of IaaS share in 2024 while Salesforce accounted for roughly 30% of CRM market share in 2024. Vendor-controlled certification and partner rebates materially affect project margins; roadmap and support policies can force upgrades/reimplementation, whereas co-innovation agreements reduce deployment risk and increase deal flow.

Talent as the primary input

Skilled labor is NTT DATA’s primary supplier: a global cybersecurity workforce gap of about 3.4 million (ISC2) and continued AI/cloud skill scarcity drive wage inflation (tech wages rose roughly 6% in 2023–24), pushing delivery costs higher. Certification premiums and attrition (industry attrition around 20–25%) inflate project staffing bills. Global delivery centers cushion cost spikes but do not eliminate scarcity. Strong employer branding and upskilling programs materially reduce churn pressure.

Niche tech and data providers

Specialist API, data and cybersecurity vendors can exert outsized leverage on specific NTT DATA deals, especially where bespoke integrations create material switching costs and mid-project lock-in; the global cybersecurity market was about 217 billion USD in 2024, underscoring vendor concentration in high-value niches. Volume across these suppliers is fragmented, limiting systemic risk, while framework agreements and multi-sourcing are commonly used to reduce single-point exposure.

- Vendor leverage: high on niche APIs/data/cyber

- Switching costs: material mid-project

- Systemic risk: limited by fragmentation

- Mitigation: framework deals + multi-sourcing

Subcontractors and partners

Subcontractors and boutique staff-augmentation partners provide surge capacity and specialized domain skills, but 2024 peak-demand cycles still show measurable rate volatility that can compress project margins; preferred-vendor lists and long-term MSAs help stabilize commercial terms, while robust vendor management limits delivery risk and cost creep.

- Surge capacity: staff-augmentation partners

- Rate volatility: compresses margins in peaks

- Stabilizers: preferred vendors and long-term MSAs

- Controls: vendor management reduces delivery risk and cost creep

Concentrated cloud power, skilled-labor gap 3.4M and wages +6% squeeze margins

Hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024) and specialist vendors exert high pricing and roadmap leverage; skilled‑labor gap ~3.4M (ISC2) and tech wages +6% (2023–24) raise delivery costs. Multi‑cloud, MSAs and co‑sell deals mitigate but do not remove supplier power.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Hyperscalers | AWS32%/Azure23%/GCP11% | High leverage |

| Skilled labor | Gap 3.4M; wages +6% | Higher costs |

| Cyber vendors | Market $217B | Outsized niche power |

What is included in the product

Tailored exclusively for NTT DATA, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence on pricing and profitability, and market entry barriers that protect incumbents; it also identifies disruptive threats and substitutes that could erode market share and strategic recommendations to strengthen NTT DATA’s position.

A concise one-sheet Porter’s Five Forces for NTT DATA that instantly visualizes competitive pressure with customizable spider charts, no macros, and a clean slides-ready layout—swap in your data, duplicate scenarios, and embed into dashboards or the companion Word report for rapid strategic decisions.

Customers Bargaining Power

Large enterprise procurement

Large enterprise procurement drives heavy price pressure on NTT DATA: the global IT services market reached about $1.2 trillion in 2024 and 60% of global clients pursue vendor consolidation and rigorous RFP benchmarking. Multi-year, multi-tower deals, which account for roughly 40% of large outsourcing spend, amplify buyer leverage. Outcome-based and gainshare models appear in about 30% of major contracts, shifting risk to providers, though strong referenceability and proven outcomes can partially offset required discounts.

Switching costs vs. multi-vendor

Integration knowledge and embedded NTT DATA teams create significant mid-contract switching costs that reduce buyer leverage, while many clients still dual-source to keep competition active. According to Flexera 2024 State of the Cloud Report, 98% of enterprises use multi-cloud/multi-vendor strategies, which sustains supplier competition. Modular architectures and APIs gradually lower lock-in, and typical IT services contracts (commonly 3–5 year terms) make renewal cycles the primary moments of pricing tension.

Demand for measurable outcomes

Clients now demand measurable ROI from digital transformation, cloud migration and AI, with 2024 surveys showing over 56% of enterprises requiring clear payback timelines. SLAs, KPIs and financial penalties are increasingly standard, raising accountability and shortening remediation cycles. Strong value articulation and industry-specific IP boost NTT DATAs pricing power. Poor outcomes trigger rapid scope cuts or re-bids, often within months.

Insourcing and captives

Some enterprises build captives or expand internal tech teams to reduce vendor reliance, giving buyers a credible alternative in negotiations and pressuring margins; in 2024 this trend intensified among large firms shifting to hybrid sourcing. NTT DATA must therefore sell higher-value services beyond commodity delivery, emphasizing IP, outcome-based contracts and industry expertise. Co-managed models and managed services can neutralize full insourcing threats by offering shared governance and cost transparency.

Security and compliance requirements

Buyers impose stringent data, sovereignty, and regulatory standards, with 2024 surveys showing about 65% of enterprises prioritise local data residency; this raises delivery costs and narrows vendor pools. Meeting advanced requirements allows NTT DATA to justify premium pricing, while breaches or audit failures rapidly erode bargaining position and revenue.

- Compliance-driven cost uplift: higher delivery margins

- Vendor shortlist shrinkage: fewer qualified bidders

- Premium pricing justification: advanced certifications

- Risk: breaches/audit failures → swift loss of trust

Enterprise buyers squeeze IT margins — 60% consolidation, 98% multi-cloud

Enterprise buyers exert strong price and risk pressure on NTT DATA: 2024 global IT services ~$1.2T, 60% seek vendor consolidation and 40% of large outsourcing is multi-tower, boosting buyer leverage. Multi-cloud (98%) and modular architectures reduce lock-in, though embedded teams raise switching costs. Outcome-based deals (≈30%) and ROI demands (56%) intensify performance-linked pricing; 65% prioritize data residency, enabling premium for compliant vendors.

| Metric | 2024 Value |

|---|---|

| Global IT services | $1.2T |

| Clients seeking consolidation | 60% |

| Multi-tower spend | 40% |

| Outcome-based deals | 30% |

| Multi-cloud adoption | 98% |

| Require ROI timelines | 56% |

| Data residency priority | 65% |

Preview Before You Purchase

NTT DATA Porter's Five Forces Analysis

This preview shows the exact NTT DATA Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final document and will get instant access to this same deliverable.