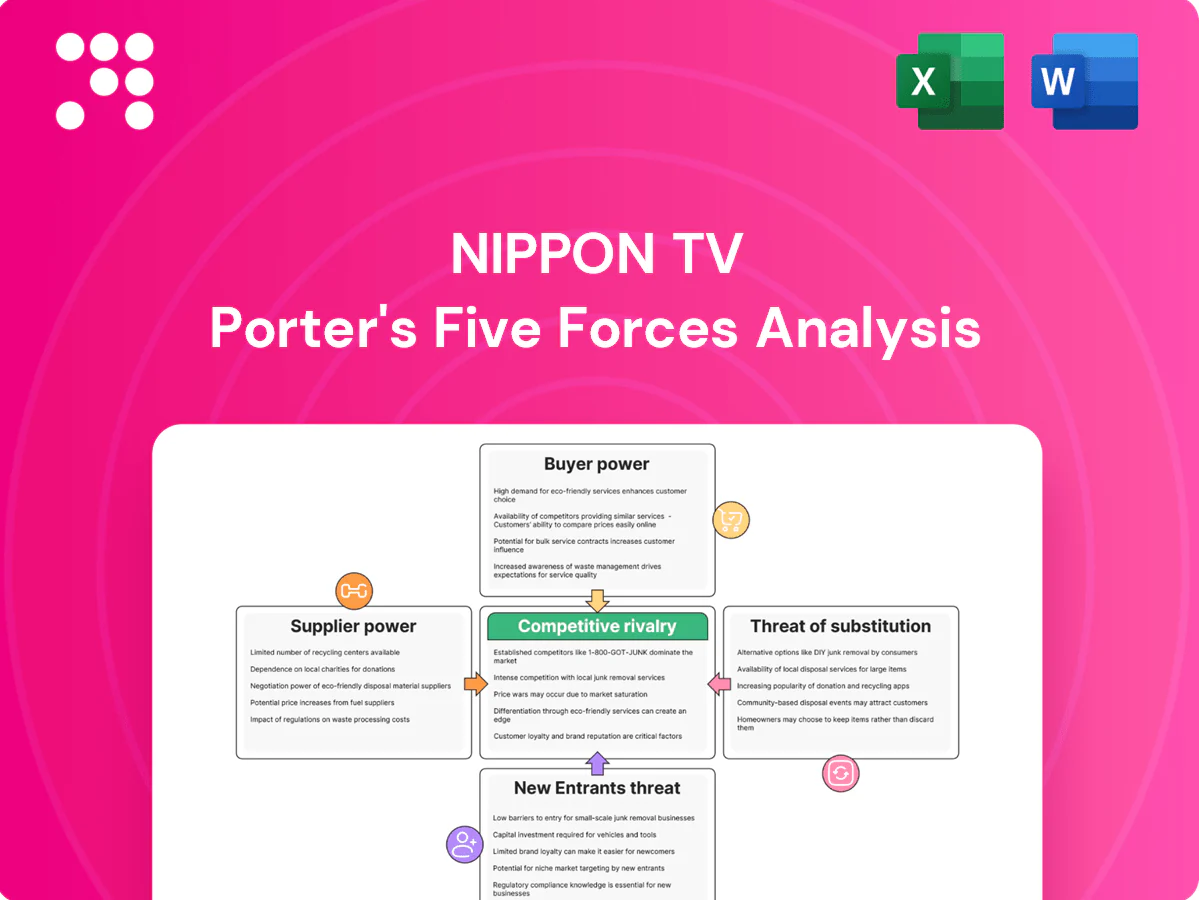

Nippon TV Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Nippon TV faces intense rivalry from streaming and legacy broadcasters, moderate supplier leverage, strong buyer choice, growing substitutes, and barriers that limit new entrants. Our snapshot highlights strategic pressure points and revenue risks. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable implications. Get the consultant-grade report to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated talent agencies

Japan’s top talent is concentrated in a few agencies, giving them strong leverage over casting and pricing and constraining scheduling for ratings-driven programs. Access to marquee hosts and actors directly affects viewership and ad revenue, making agency relationships strategic; Nippon TV reported consolidated revenue of JPY 396.7 billion in FY2023, underscoring stakes. This concentration can raise talent costs and limit programming flexibility. Nippon TV must sustain close agency ties to secure top talent.

Premium sports rights

Sports leagues and rights holders hold high bargaining power for Nippon TV due to scarcity and live-viewership appeal, with streamers intensifying bids in 2024; long-term commercial contracts typically span 3–10 years, anchoring fees and scheduling. Inflating rights costs threaten prime-time ratings and ad yield if key properties are lost, and co-production or multi-year rights can mitigate short-term volatility.

Hit content producers

Independent studios and marquee creators command premiums for proven formats and IP, allowing successful drama and variety show producers to shop concepts to rival networks or streamers. This marketplace power has pushed acquisition and production costs up—broadcasters report double-digit increases in top-tier talent fees—while global streamers such as Netflix had about 260 million paid subscribers in 2024, intensifying competition. Co-developing IP and securing multi-title slates can lock in supply and cap cost inflation.

Tech and distribution vendors

Transmission, cloud and production tech providers directly shape Nippon TV’s cost base and uptime; major cloud players (AWS ~32% share in IaaS/PaaS, 2024) advertise SLAs of 99.99%+, making outages costly. Switching costs are moderate to high due to deep integration and regulatory compliance. Vendors passed through inflationary pressures in 2024, with reported vendor price hikes around 5–7%.

- Vendor concentration: cloud market leader ~32% (2024)

- Uptime: SLAs commonly 99.99%+

- Switching: moderate–high due to integration/compliance

- Mitigation: diversify vendors, in-house key capabilities

News and footage sources

Agencies, international feeds and archival partners shape Nippon TVs news breadth and speed, with exclusives and licensed footage becoming especially valuable during major 2024 events. Licensing premiums and blackout restrictions can erode competitiveness in breaking news windows, while delays from suppliers directly harm market share in live ratings. Investing in owned news‑gathering assets and bureaus in 2024 helped rebalance supplier leverage.

- Agencies drive reach and latency

- Exclusives command premiums in crises

- Restrictions delay breaking coverage

- Owned bureaus reduce supplier power

Suppliers squeeze broadcasters: talent fees, sports rights premiums and cloud price hikes

Suppliers exert high bargaining power: talent agencies and sports rights holders command premiums that directly affect Nippon TV’s ad revenue (consolidated revenue JPY 396.7bn FY2023). Tech/cloud vendors raise costs (vendor price hikes ~5–7% in 2024; AWS ~32% IaaS share 2024), while streamers (Netflix ~260M subs 2024) intensify competition for IP and rights.

| Supplier | Power | Metric (2024) |

|---|---|---|

| Talent/Agencies | High | Top fees ↑ (double-digit) |

| Sports/Rights | High | Multiyear deals 3–10 yrs |

| Cloud/Tech | Moderate–High | AWS ~32% share; vendor hikes 5–7% |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon TV that uncovers competitive drivers, buyer and supplier power, substitution risks, and entry barriers—highlighting disruptive threats and strategic levers to protect market share and profitability.

Clean, simplified Porter's Five Forces for Nippon TV—one-sheet view that instantly highlights competitive pressures and strategic levers, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Advertisers’ budget leverage

Major advertisers and agencies exert strong negotiating power in Japan’s mature ad market; total ad spend was about ¥7.9 trillion in 2024, letting buyers shift budgets rapidly across TV, digital and performance channels. As viewing fragments, CPM pressure rises for linear spots, pushing broadcasters to protect yield via bundled cross-media deals and data-driven targeting. Nippon TV leans on audience data and integrated packages to retain premium pricing amid rising digital share.

Audience fragmentation

Viewers face abundant alternatives across SVOD, AVOD and social platforms, with global SVOD subscriptions topping 1 billion by mid-2024 and Japan's population around 125 million. Low switching costs amplify sensitivity to content quality and scheduling. Declining linear viewership in advanced markets weakens inventory scarcity and raises buyer power. Strengthening Nippon TV's digital reach, with Japan smartphone penetration ≈84% in 2024, can rebalance attention.

Distributors and platforms

Cable, IPTV and OTT aggregators in Japan wield strong placement leverage, negotiating carriage fees and prominence that directly affect Nippon TVs catch-up and AVOD reach. Platform algorithms and homepage prominence determine discoverability and ad yields, while major app stores commonly enforce a roughly 30% revenue share on in‑app purchases. Aggregators also demand access to audience and viewing data for targeting. Multi-platform distribution mitigates reliance on any single gatekeeper.

Corporate sponsors in events

Corporate sponsors negotiating with Nippon TV can extract integrations, exclusivity and price concessions; in 2024 the global sponsorship market was about $80 billion, raising leverage for buyers who can shift spend across sports, pop culture and experiential activations. Economic cycles materially affect willingness to pay, while measurable outcomes and tiered packages lift renewal rates by ~15–25%, preserving demand.

- Negotiation levers: integrations, exclusivity, price

- Alternatives: sports, pop culture, experiential

- Macro sensitivity: cyclical spend shifts

- Retention: measurement + tiered offers → +15–25% renewals

International buyers of content

International buyers compare Nippon TV content directly with global offerings as paid streaming subscriptions topped about 1.6 billion worldwide in 2024, intensifying price pressure; yen weakness and localization costs (translation, dubbing) further squeeze margins; format licensing attracts multiple bidders, while proven IP catalogs and hit formats command stronger terms and upfront fees.

- Global subs 2024: ~1.6B

- Currency/localization raise effective costs

- Multiple bidders on format deals

- Strong IP = better licensing terms

Broadcaster pivots to data-driven bundles as advertisers shift budgets and streaming soars

Nippon TV faces strong buyer power as major advertisers (Japan ad spend ≈¥7.9T in 2024) shift budgets across TV, digital and performance channels, squeezing linear CPMs. Viewers and platform aggregators amplify switching and placement leverage amid global SVOD/streaming growth (global paid subs ≈1.6B in 2024) and Japan smartphone penetration ≈84% (2024), pushing Nippon TV toward data-driven bundles to defend yields.

| Metric | 2024 Value |

|---|---|

| Japan ad spend | ¥7.9 trillion |

| Global paid streaming subs | ≈1.6 billion |

| Japan smartphone penetration | ≈84% |

| Global sponsorship market | $80 billion |

Preview Before You Purchase

Nippon TV Porter's Five Forces Analysis

This preview shows the exact Nippon TV Porter’s Five Forces Analysis you’ll receive—no mockups or placeholders. The document displayed is the full, professionally formatted analysis, ready for immediate download and use upon purchase. You’re looking at the final file; once you buy, you’ll get instant access to this identical deliverable.

A Must-Have Tool for Decision-Makers

Nippon TV faces intense rivalry from streaming and legacy broadcasters, moderate supplier leverage, strong buyer choice, growing substitutes, and barriers that limit new entrants. Our snapshot highlights strategic pressure points and revenue risks. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable implications. Get the consultant-grade report to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated talent agencies

Japan’s top talent is concentrated in a few agencies, giving them strong leverage over casting and pricing and constraining scheduling for ratings-driven programs. Access to marquee hosts and actors directly affects viewership and ad revenue, making agency relationships strategic; Nippon TV reported consolidated revenue of JPY 396.7 billion in FY2023, underscoring stakes. This concentration can raise talent costs and limit programming flexibility. Nippon TV must sustain close agency ties to secure top talent.

Premium sports rights

Sports leagues and rights holders hold high bargaining power for Nippon TV due to scarcity and live-viewership appeal, with streamers intensifying bids in 2024; long-term commercial contracts typically span 3–10 years, anchoring fees and scheduling. Inflating rights costs threaten prime-time ratings and ad yield if key properties are lost, and co-production or multi-year rights can mitigate short-term volatility.

Hit content producers

Independent studios and marquee creators command premiums for proven formats and IP, allowing successful drama and variety show producers to shop concepts to rival networks or streamers. This marketplace power has pushed acquisition and production costs up—broadcasters report double-digit increases in top-tier talent fees—while global streamers such as Netflix had about 260 million paid subscribers in 2024, intensifying competition. Co-developing IP and securing multi-title slates can lock in supply and cap cost inflation.

Tech and distribution vendors

Transmission, cloud and production tech providers directly shape Nippon TV’s cost base and uptime; major cloud players (AWS ~32% share in IaaS/PaaS, 2024) advertise SLAs of 99.99%+, making outages costly. Switching costs are moderate to high due to deep integration and regulatory compliance. Vendors passed through inflationary pressures in 2024, with reported vendor price hikes around 5–7%.

- Vendor concentration: cloud market leader ~32% (2024)

- Uptime: SLAs commonly 99.99%+

- Switching: moderate–high due to integration/compliance

- Mitigation: diversify vendors, in-house key capabilities

News and footage sources

Agencies, international feeds and archival partners shape Nippon TVs news breadth and speed, with exclusives and licensed footage becoming especially valuable during major 2024 events. Licensing premiums and blackout restrictions can erode competitiveness in breaking news windows, while delays from suppliers directly harm market share in live ratings. Investing in owned news‑gathering assets and bureaus in 2024 helped rebalance supplier leverage.

- Agencies drive reach and latency

- Exclusives command premiums in crises

- Restrictions delay breaking coverage

- Owned bureaus reduce supplier power

Suppliers squeeze broadcasters: talent fees, sports rights premiums and cloud price hikes

Suppliers exert high bargaining power: talent agencies and sports rights holders command premiums that directly affect Nippon TV’s ad revenue (consolidated revenue JPY 396.7bn FY2023). Tech/cloud vendors raise costs (vendor price hikes ~5–7% in 2024; AWS ~32% IaaS share 2024), while streamers (Netflix ~260M subs 2024) intensify competition for IP and rights.

| Supplier | Power | Metric (2024) |

|---|---|---|

| Talent/Agencies | High | Top fees ↑ (double-digit) |

| Sports/Rights | High | Multiyear deals 3–10 yrs |

| Cloud/Tech | Moderate–High | AWS ~32% share; vendor hikes 5–7% |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon TV that uncovers competitive drivers, buyer and supplier power, substitution risks, and entry barriers—highlighting disruptive threats and strategic levers to protect market share and profitability.

Clean, simplified Porter's Five Forces for Nippon TV—one-sheet view that instantly highlights competitive pressures and strategic levers, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Advertisers’ budget leverage

Major advertisers and agencies exert strong negotiating power in Japan’s mature ad market; total ad spend was about ¥7.9 trillion in 2024, letting buyers shift budgets rapidly across TV, digital and performance channels. As viewing fragments, CPM pressure rises for linear spots, pushing broadcasters to protect yield via bundled cross-media deals and data-driven targeting. Nippon TV leans on audience data and integrated packages to retain premium pricing amid rising digital share.

Audience fragmentation

Viewers face abundant alternatives across SVOD, AVOD and social platforms, with global SVOD subscriptions topping 1 billion by mid-2024 and Japan's population around 125 million. Low switching costs amplify sensitivity to content quality and scheduling. Declining linear viewership in advanced markets weakens inventory scarcity and raises buyer power. Strengthening Nippon TV's digital reach, with Japan smartphone penetration ≈84% in 2024, can rebalance attention.

Distributors and platforms

Cable, IPTV and OTT aggregators in Japan wield strong placement leverage, negotiating carriage fees and prominence that directly affect Nippon TVs catch-up and AVOD reach. Platform algorithms and homepage prominence determine discoverability and ad yields, while major app stores commonly enforce a roughly 30% revenue share on in‑app purchases. Aggregators also demand access to audience and viewing data for targeting. Multi-platform distribution mitigates reliance on any single gatekeeper.

Corporate sponsors in events

Corporate sponsors negotiating with Nippon TV can extract integrations, exclusivity and price concessions; in 2024 the global sponsorship market was about $80 billion, raising leverage for buyers who can shift spend across sports, pop culture and experiential activations. Economic cycles materially affect willingness to pay, while measurable outcomes and tiered packages lift renewal rates by ~15–25%, preserving demand.

- Negotiation levers: integrations, exclusivity, price

- Alternatives: sports, pop culture, experiential

- Macro sensitivity: cyclical spend shifts

- Retention: measurement + tiered offers → +15–25% renewals

International buyers of content

International buyers compare Nippon TV content directly with global offerings as paid streaming subscriptions topped about 1.6 billion worldwide in 2024, intensifying price pressure; yen weakness and localization costs (translation, dubbing) further squeeze margins; format licensing attracts multiple bidders, while proven IP catalogs and hit formats command stronger terms and upfront fees.

- Global subs 2024: ~1.6B

- Currency/localization raise effective costs

- Multiple bidders on format deals

- Strong IP = better licensing terms

Broadcaster pivots to data-driven bundles as advertisers shift budgets and streaming soars

Nippon TV faces strong buyer power as major advertisers (Japan ad spend ≈¥7.9T in 2024) shift budgets across TV, digital and performance channels, squeezing linear CPMs. Viewers and platform aggregators amplify switching and placement leverage amid global SVOD/streaming growth (global paid subs ≈1.6B in 2024) and Japan smartphone penetration ≈84% (2024), pushing Nippon TV toward data-driven bundles to defend yields.

| Metric | 2024 Value |

|---|---|

| Japan ad spend | ¥7.9 trillion |

| Global paid streaming subs | ≈1.6 billion |

| Japan smartphone penetration | ≈84% |

| Global sponsorship market | $80 billion |

Preview Before You Purchase

Nippon TV Porter's Five Forces Analysis

This preview shows the exact Nippon TV Porter’s Five Forces Analysis you’ll receive—no mockups or placeholders. The document displayed is the full, professionally formatted analysis, ready for immediate download and use upon purchase. You’re looking at the final file; once you buy, you’ll get instant access to this identical deliverable.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Nippon TV faces intense rivalry from streaming and legacy broadcasters, moderate supplier leverage, strong buyer choice, growing substitutes, and barriers that limit new entrants. Our snapshot highlights strategic pressure points and revenue risks. This preview only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, visuals, and actionable implications. Get the consultant-grade report to inform investment or strategy decisions.

Suppliers Bargaining Power

Concentrated talent agencies

Japan’s top talent is concentrated in a few agencies, giving them strong leverage over casting and pricing and constraining scheduling for ratings-driven programs. Access to marquee hosts and actors directly affects viewership and ad revenue, making agency relationships strategic; Nippon TV reported consolidated revenue of JPY 396.7 billion in FY2023, underscoring stakes. This concentration can raise talent costs and limit programming flexibility. Nippon TV must sustain close agency ties to secure top talent.

Premium sports rights

Sports leagues and rights holders hold high bargaining power for Nippon TV due to scarcity and live-viewership appeal, with streamers intensifying bids in 2024; long-term commercial contracts typically span 3–10 years, anchoring fees and scheduling. Inflating rights costs threaten prime-time ratings and ad yield if key properties are lost, and co-production or multi-year rights can mitigate short-term volatility.

Hit content producers

Independent studios and marquee creators command premiums for proven formats and IP, allowing successful drama and variety show producers to shop concepts to rival networks or streamers. This marketplace power has pushed acquisition and production costs up—broadcasters report double-digit increases in top-tier talent fees—while global streamers such as Netflix had about 260 million paid subscribers in 2024, intensifying competition. Co-developing IP and securing multi-title slates can lock in supply and cap cost inflation.

Tech and distribution vendors

Transmission, cloud and production tech providers directly shape Nippon TV’s cost base and uptime; major cloud players (AWS ~32% share in IaaS/PaaS, 2024) advertise SLAs of 99.99%+, making outages costly. Switching costs are moderate to high due to deep integration and regulatory compliance. Vendors passed through inflationary pressures in 2024, with reported vendor price hikes around 5–7%.

- Vendor concentration: cloud market leader ~32% (2024)

- Uptime: SLAs commonly 99.99%+

- Switching: moderate–high due to integration/compliance

- Mitigation: diversify vendors, in-house key capabilities

News and footage sources

Agencies, international feeds and archival partners shape Nippon TVs news breadth and speed, with exclusives and licensed footage becoming especially valuable during major 2024 events. Licensing premiums and blackout restrictions can erode competitiveness in breaking news windows, while delays from suppliers directly harm market share in live ratings. Investing in owned news‑gathering assets and bureaus in 2024 helped rebalance supplier leverage.

- Agencies drive reach and latency

- Exclusives command premiums in crises

- Restrictions delay breaking coverage

- Owned bureaus reduce supplier power

Suppliers squeeze broadcasters: talent fees, sports rights premiums and cloud price hikes

Suppliers exert high bargaining power: talent agencies and sports rights holders command premiums that directly affect Nippon TV’s ad revenue (consolidated revenue JPY 396.7bn FY2023). Tech/cloud vendors raise costs (vendor price hikes ~5–7% in 2024; AWS ~32% IaaS share 2024), while streamers (Netflix ~260M subs 2024) intensify competition for IP and rights.

| Supplier | Power | Metric (2024) |

|---|---|---|

| Talent/Agencies | High | Top fees ↑ (double-digit) |

| Sports/Rights | High | Multiyear deals 3–10 yrs |

| Cloud/Tech | Moderate–High | AWS ~32% share; vendor hikes 5–7% |

What is included in the product

Tailored Porter's Five Forces analysis for Nippon TV that uncovers competitive drivers, buyer and supplier power, substitution risks, and entry barriers—highlighting disruptive threats and strategic levers to protect market share and profitability.

Clean, simplified Porter's Five Forces for Nippon TV—one-sheet view that instantly highlights competitive pressures and strategic levers, ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Advertisers’ budget leverage

Major advertisers and agencies exert strong negotiating power in Japan’s mature ad market; total ad spend was about ¥7.9 trillion in 2024, letting buyers shift budgets rapidly across TV, digital and performance channels. As viewing fragments, CPM pressure rises for linear spots, pushing broadcasters to protect yield via bundled cross-media deals and data-driven targeting. Nippon TV leans on audience data and integrated packages to retain premium pricing amid rising digital share.

Audience fragmentation

Viewers face abundant alternatives across SVOD, AVOD and social platforms, with global SVOD subscriptions topping 1 billion by mid-2024 and Japan's population around 125 million. Low switching costs amplify sensitivity to content quality and scheduling. Declining linear viewership in advanced markets weakens inventory scarcity and raises buyer power. Strengthening Nippon TV's digital reach, with Japan smartphone penetration ≈84% in 2024, can rebalance attention.

Distributors and platforms

Cable, IPTV and OTT aggregators in Japan wield strong placement leverage, negotiating carriage fees and prominence that directly affect Nippon TVs catch-up and AVOD reach. Platform algorithms and homepage prominence determine discoverability and ad yields, while major app stores commonly enforce a roughly 30% revenue share on in‑app purchases. Aggregators also demand access to audience and viewing data for targeting. Multi-platform distribution mitigates reliance on any single gatekeeper.

Corporate sponsors in events

Corporate sponsors negotiating with Nippon TV can extract integrations, exclusivity and price concessions; in 2024 the global sponsorship market was about $80 billion, raising leverage for buyers who can shift spend across sports, pop culture and experiential activations. Economic cycles materially affect willingness to pay, while measurable outcomes and tiered packages lift renewal rates by ~15–25%, preserving demand.

- Negotiation levers: integrations, exclusivity, price

- Alternatives: sports, pop culture, experiential

- Macro sensitivity: cyclical spend shifts

- Retention: measurement + tiered offers → +15–25% renewals

International buyers of content

International buyers compare Nippon TV content directly with global offerings as paid streaming subscriptions topped about 1.6 billion worldwide in 2024, intensifying price pressure; yen weakness and localization costs (translation, dubbing) further squeeze margins; format licensing attracts multiple bidders, while proven IP catalogs and hit formats command stronger terms and upfront fees.

- Global subs 2024: ~1.6B

- Currency/localization raise effective costs

- Multiple bidders on format deals

- Strong IP = better licensing terms

Broadcaster pivots to data-driven bundles as advertisers shift budgets and streaming soars

Nippon TV faces strong buyer power as major advertisers (Japan ad spend ≈¥7.9T in 2024) shift budgets across TV, digital and performance channels, squeezing linear CPMs. Viewers and platform aggregators amplify switching and placement leverage amid global SVOD/streaming growth (global paid subs ≈1.6B in 2024) and Japan smartphone penetration ≈84% (2024), pushing Nippon TV toward data-driven bundles to defend yields.

| Metric | 2024 Value |

|---|---|

| Japan ad spend | ¥7.9 trillion |

| Global paid streaming subs | ≈1.6 billion |

| Japan smartphone penetration | ≈84% |

| Global sponsorship market | $80 billion |

Preview Before You Purchase

Nippon TV Porter's Five Forces Analysis

This preview shows the exact Nippon TV Porter’s Five Forces Analysis you’ll receive—no mockups or placeholders. The document displayed is the full, professionally formatted analysis, ready for immediate download and use upon purchase. You’re looking at the final file; once you buy, you’ll get instant access to this identical deliverable.