Nu Holdings SWOT Analysis

Your Strategic Toolkit Starts Here

Nu Holdings shows strong digital growth and brand loyalty but faces margin pressure, regulatory headwinds, and intense competition. Our full SWOT unpacks core capabilities, strategic risks, and expansion levers with clear recommendations. Purchase the editable report to plan, pitch, and invest with confidence.

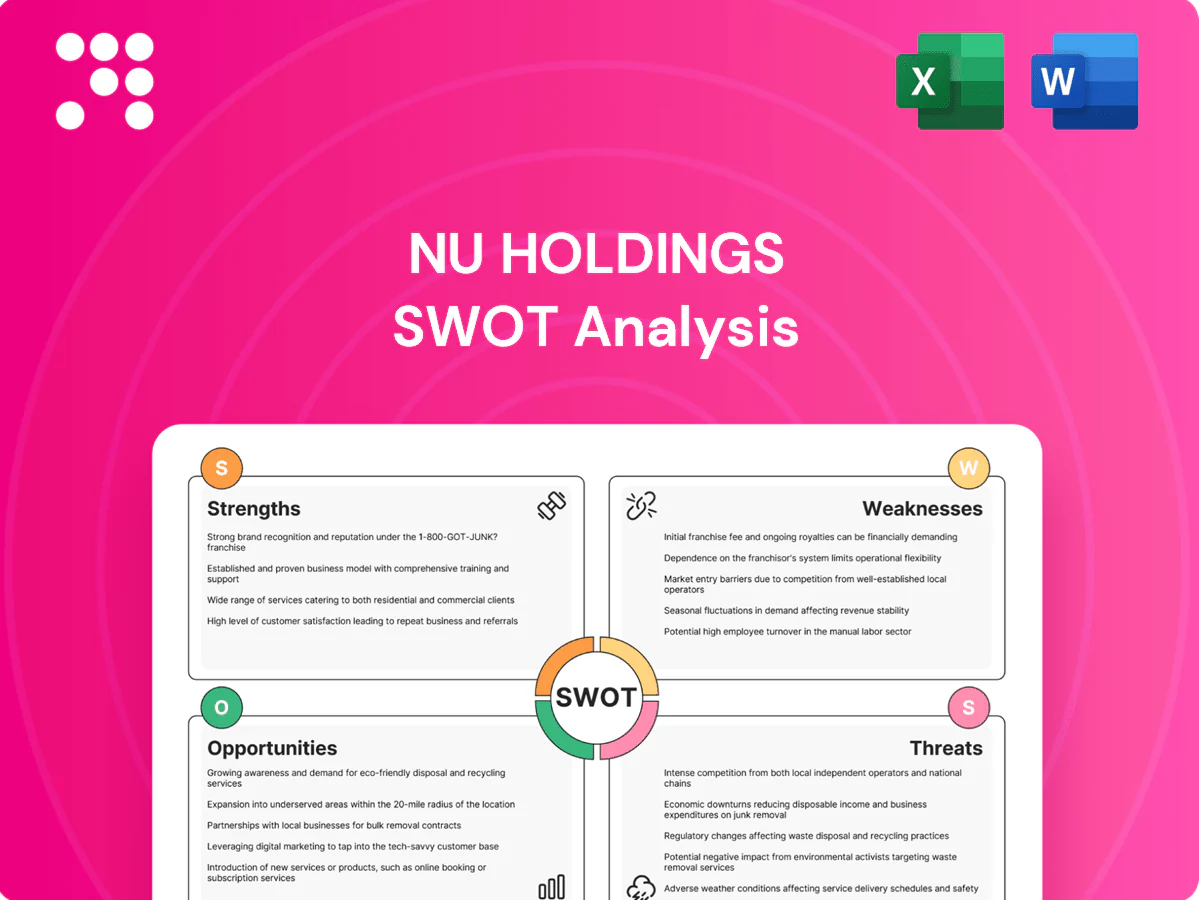

Strengths

Large, engaged customer base

Strong user growth—over 70 million customers as of 2024—plus high app engagement produces network effects and lowers marginal distribution costs. The broad base supports cross-sell and supplies stable, low-cost deposit funding. Rich engagement data enables better personalization and retention, and scale advantages widen the moat versus smaller challengers.

Low-cost, scalable digital platform

Nu's end-to-end digital model cuts branch and servicing costs, supporting over 100 million customers across Brazil, Mexico, Colombia and Peru as of April 2024. Cloud-native, automated infrastructure enables rapid feature rollout and market scaling, lowering unit costs so competitive pricing doesn't erode customer experience. Operating leverage has strengthened as older cohorts mature, boosting profitability per customer.

Superior UX and brand trust

Simple design, transparent pricing and responsive support drive high satisfaction for Nu, reflected in a customer base of over 75 million as of 2024 and double-digit YoY growth that signals strong retention. A mission-led focus on financial inclusion builds loyalty and advocacy, cutting acquisition costs via positive word-of-mouth and making cross-sell of new products easier within the trusted ecosystem.

Data-driven underwriting and analytics

Nu Holdings (NYSE: NU) leverages proprietary data and machine learning across its Latin America operations to enhance credit decisioning for underserved segments, improving risk discrimination and tailoring offers.

Iterative risk models enable higher approval efficiency while controlling losses through continuous calibration and portfolio monitoring.

Granular behavioral and transactional insights support dynamic credit limits and pricing, improving unit economics and margin per account.

- Proprietary ML models

- Iterative risk calibration

- Dynamic limits & pricing

- Improved unit economics

Diversified product suite and deposits

Nu’s diversified suite across payments, accounts, lending and investments drives higher ARPU and stickiness; with over 70 million customers and customer deposits surpassing $20bn in 2024, deposits offer low‑cost, stable funding versus wholesale; cross‑product bundling in one unified app boosts retention and lifetime value by reducing friction across use cases.

- Multiple products → higher ARPU

- Deposits > $20bn (2024) → low‑cost funding

- Bundling → improved retention/LTV

- Unified app → reduced friction

Scale: ~75M, $20bn deposits fuel cloud growth

Scale: ~75M customers (2024) with >$20bn deposits provides low‑cost funding, cross‑sell base and network effects.

Digital, cloud‑native model and automation lower unit costs and speed rollouts, improving operating leverage as cohorts mature.

Proprietary ML risk models and behavioral data enable better credit selection, dynamic pricing and higher ARPU across payments, lending and investments.

| Metric | 2024 |

|---|---|

| Customers | ~75M |

| Deposits | >$20bn |

| Markets | Brazil, Mexico, Colombia, Peru |

| Growth | Double‑digit YoY |

What is included in the product

Delivers a strategic overview of Nu Holdings’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and growth prospects in digital banking and fintech.

Provides a concise SWOT snapshot for Nu Holdings that clarifies strategic risks and opportunities quickly, easing stakeholder alignment and accelerating decision-making.

Weaknesses

Exposure to unsecured credit risk

Core lending at Nu is concentrated in credit cards and personal loans, which by mid-2024 served over 60 million customers and drive most retail receivables. These segments are cyclical and sensitive to employment and income shocks, with Brazil's unemployment hovering around 8–9% in 2024 amplifying default risk. Loss volatility can compress margins in downturns, so risk control requires continual model tuning and conservative provisioning.

Macroeconomic and FX sensitivity

Operations concentrated in Latin America, chiefly Brazil and Mexico, leave Nu highly exposed to inflation and interest-rate swings; Brazil's Selic rate peaked at 13.75% in 2023, influencing loan pricing and funding costs. Currency fluctuations between BRL/MXN and USD distort reported revenue and CET1-equivalent ratios, complicating investor comparability. Consumer demand and credit performance can deteriorate rapidly in stress, and Nu's hedges only partially offset this volatility.

Regulatory fragmentation

Nu Holdings faces regulatory fragmentation across the 4+ Latin American markets where it operates, each with distinct banking, payments, data, and consumer rules.

This compliance complexity raises operating costs and slows product rollout; Nu’s NYSE listing (NU) since December 2021 also increases cross-border oversight.

Sudden rule changes can impact fees, capital or pricing, and coordination across multiple regulators adds material execution risk.

Geographic concentration

Nu remains heavily weighted to Brazil, which accounted for about 80% of revenues in 2024, concentrating risk in one macro and policy environment. This concentration heightens exposure to local economic downturns, FX swings, or regulatory shifts. Diversification into Mexico and Colombia is still nascent, and scaling new markets requires significant capital and time to reach profitability.

- ~80% revenue from Brazil (2024)

- Diversification early: Mexico, Colombia

- High exposure to local policy/economic shocks

- Scaling new markets needs substantial investment/time

Monetization still maturing

Monetization still maturing: newer verticals—investments, insurance and SME services—remain early in lifecycle and contribute only a small share of revenue, despite Nu serving over 80 million customers by end-2024; take rates are modest and likely to stay low until deeper penetration and richer product suites lift yields. Cross-sell hinges on sustained trust and execution, and profitability can lag user growth during expansion.

- Early-stage verticals: low revenue share

- Take rates: modest until penetration rises

- Cross-sell: dependent on trust/execution

- Profitability: may trail user growth

Brazil-focused cards and personal loans risk earnings; ~80% revenue

Nu's loan book is concentrated in credit cards and personal loans, exposing earnings to cyclical defaults (Brazil unemployment ~8–9% in 2024) and loss volatility. Geographic concentration—~80% revenue from Brazil (2024) with early-stage Mexico/Colombia expansion—raises policy, FX and execution risk. Monetization of investments, insurance and SME services remains small despite >80m customers end-2024.

| Metric | Value |

|---|---|

| Revenue from Brazil (2024) | ~80% |

| Customers (end-2024) | >80m |

| Core lending segments | Cards, personal loans |

What You See Is What You Get

Nu Holdings SWOT Analysis

This is the actual Nu Holdings SWOT analysis you'll receive upon purchase—no surprises, just a professional, structured report. The preview below is taken directly from the full document; buy to unlock the complete, editable version. The file shown is the real analysis you’ll download post-purchase, with full strengths, weaknesses, opportunities and threats.

Your Strategic Toolkit Starts Here

Nu Holdings shows strong digital growth and brand loyalty but faces margin pressure, regulatory headwinds, and intense competition. Our full SWOT unpacks core capabilities, strategic risks, and expansion levers with clear recommendations. Purchase the editable report to plan, pitch, and invest with confidence.

Strengths

Large, engaged customer base

Strong user growth—over 70 million customers as of 2024—plus high app engagement produces network effects and lowers marginal distribution costs. The broad base supports cross-sell and supplies stable, low-cost deposit funding. Rich engagement data enables better personalization and retention, and scale advantages widen the moat versus smaller challengers.

Low-cost, scalable digital platform

Nu's end-to-end digital model cuts branch and servicing costs, supporting over 100 million customers across Brazil, Mexico, Colombia and Peru as of April 2024. Cloud-native, automated infrastructure enables rapid feature rollout and market scaling, lowering unit costs so competitive pricing doesn't erode customer experience. Operating leverage has strengthened as older cohorts mature, boosting profitability per customer.

Superior UX and brand trust

Simple design, transparent pricing and responsive support drive high satisfaction for Nu, reflected in a customer base of over 75 million as of 2024 and double-digit YoY growth that signals strong retention. A mission-led focus on financial inclusion builds loyalty and advocacy, cutting acquisition costs via positive word-of-mouth and making cross-sell of new products easier within the trusted ecosystem.

Data-driven underwriting and analytics

Nu Holdings (NYSE: NU) leverages proprietary data and machine learning across its Latin America operations to enhance credit decisioning for underserved segments, improving risk discrimination and tailoring offers.

Iterative risk models enable higher approval efficiency while controlling losses through continuous calibration and portfolio monitoring.

Granular behavioral and transactional insights support dynamic credit limits and pricing, improving unit economics and margin per account.

- Proprietary ML models

- Iterative risk calibration

- Dynamic limits & pricing

- Improved unit economics

Diversified product suite and deposits

Nu’s diversified suite across payments, accounts, lending and investments drives higher ARPU and stickiness; with over 70 million customers and customer deposits surpassing $20bn in 2024, deposits offer low‑cost, stable funding versus wholesale; cross‑product bundling in one unified app boosts retention and lifetime value by reducing friction across use cases.

- Multiple products → higher ARPU

- Deposits > $20bn (2024) → low‑cost funding

- Bundling → improved retention/LTV

- Unified app → reduced friction

Scale: ~75M, $20bn deposits fuel cloud growth

Scale: ~75M customers (2024) with >$20bn deposits provides low‑cost funding, cross‑sell base and network effects.

Digital, cloud‑native model and automation lower unit costs and speed rollouts, improving operating leverage as cohorts mature.

Proprietary ML risk models and behavioral data enable better credit selection, dynamic pricing and higher ARPU across payments, lending and investments.

| Metric | 2024 |

|---|---|

| Customers | ~75M |

| Deposits | >$20bn |

| Markets | Brazil, Mexico, Colombia, Peru |

| Growth | Double‑digit YoY |

What is included in the product

Delivers a strategic overview of Nu Holdings’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and growth prospects in digital banking and fintech.

Provides a concise SWOT snapshot for Nu Holdings that clarifies strategic risks and opportunities quickly, easing stakeholder alignment and accelerating decision-making.

Weaknesses

Exposure to unsecured credit risk

Core lending at Nu is concentrated in credit cards and personal loans, which by mid-2024 served over 60 million customers and drive most retail receivables. These segments are cyclical and sensitive to employment and income shocks, with Brazil's unemployment hovering around 8–9% in 2024 amplifying default risk. Loss volatility can compress margins in downturns, so risk control requires continual model tuning and conservative provisioning.

Macroeconomic and FX sensitivity

Operations concentrated in Latin America, chiefly Brazil and Mexico, leave Nu highly exposed to inflation and interest-rate swings; Brazil's Selic rate peaked at 13.75% in 2023, influencing loan pricing and funding costs. Currency fluctuations between BRL/MXN and USD distort reported revenue and CET1-equivalent ratios, complicating investor comparability. Consumer demand and credit performance can deteriorate rapidly in stress, and Nu's hedges only partially offset this volatility.

Regulatory fragmentation

Nu Holdings faces regulatory fragmentation across the 4+ Latin American markets where it operates, each with distinct banking, payments, data, and consumer rules.

This compliance complexity raises operating costs and slows product rollout; Nu’s NYSE listing (NU) since December 2021 also increases cross-border oversight.

Sudden rule changes can impact fees, capital or pricing, and coordination across multiple regulators adds material execution risk.

Geographic concentration

Nu remains heavily weighted to Brazil, which accounted for about 80% of revenues in 2024, concentrating risk in one macro and policy environment. This concentration heightens exposure to local economic downturns, FX swings, or regulatory shifts. Diversification into Mexico and Colombia is still nascent, and scaling new markets requires significant capital and time to reach profitability.

- ~80% revenue from Brazil (2024)

- Diversification early: Mexico, Colombia

- High exposure to local policy/economic shocks

- Scaling new markets needs substantial investment/time

Monetization still maturing

Monetization still maturing: newer verticals—investments, insurance and SME services—remain early in lifecycle and contribute only a small share of revenue, despite Nu serving over 80 million customers by end-2024; take rates are modest and likely to stay low until deeper penetration and richer product suites lift yields. Cross-sell hinges on sustained trust and execution, and profitability can lag user growth during expansion.

- Early-stage verticals: low revenue share

- Take rates: modest until penetration rises

- Cross-sell: dependent on trust/execution

- Profitability: may trail user growth

Brazil-focused cards and personal loans risk earnings; ~80% revenue

Nu's loan book is concentrated in credit cards and personal loans, exposing earnings to cyclical defaults (Brazil unemployment ~8–9% in 2024) and loss volatility. Geographic concentration—~80% revenue from Brazil (2024) with early-stage Mexico/Colombia expansion—raises policy, FX and execution risk. Monetization of investments, insurance and SME services remains small despite >80m customers end-2024.

| Metric | Value |

|---|---|

| Revenue from Brazil (2024) | ~80% |

| Customers (end-2024) | >80m |

| Core lending segments | Cards, personal loans |

What You See Is What You Get

Nu Holdings SWOT Analysis

This is the actual Nu Holdings SWOT analysis you'll receive upon purchase—no surprises, just a professional, structured report. The preview below is taken directly from the full document; buy to unlock the complete, editable version. The file shown is the real analysis you’ll download post-purchase, with full strengths, weaknesses, opportunities and threats.

Description

Your Strategic Toolkit Starts Here

Nu Holdings shows strong digital growth and brand loyalty but faces margin pressure, regulatory headwinds, and intense competition. Our full SWOT unpacks core capabilities, strategic risks, and expansion levers with clear recommendations. Purchase the editable report to plan, pitch, and invest with confidence.

Strengths

Large, engaged customer base

Strong user growth—over 70 million customers as of 2024—plus high app engagement produces network effects and lowers marginal distribution costs. The broad base supports cross-sell and supplies stable, low-cost deposit funding. Rich engagement data enables better personalization and retention, and scale advantages widen the moat versus smaller challengers.

Low-cost, scalable digital platform

Nu's end-to-end digital model cuts branch and servicing costs, supporting over 100 million customers across Brazil, Mexico, Colombia and Peru as of April 2024. Cloud-native, automated infrastructure enables rapid feature rollout and market scaling, lowering unit costs so competitive pricing doesn't erode customer experience. Operating leverage has strengthened as older cohorts mature, boosting profitability per customer.

Superior UX and brand trust

Simple design, transparent pricing and responsive support drive high satisfaction for Nu, reflected in a customer base of over 75 million as of 2024 and double-digit YoY growth that signals strong retention. A mission-led focus on financial inclusion builds loyalty and advocacy, cutting acquisition costs via positive word-of-mouth and making cross-sell of new products easier within the trusted ecosystem.

Data-driven underwriting and analytics

Nu Holdings (NYSE: NU) leverages proprietary data and machine learning across its Latin America operations to enhance credit decisioning for underserved segments, improving risk discrimination and tailoring offers.

Iterative risk models enable higher approval efficiency while controlling losses through continuous calibration and portfolio monitoring.

Granular behavioral and transactional insights support dynamic credit limits and pricing, improving unit economics and margin per account.

- Proprietary ML models

- Iterative risk calibration

- Dynamic limits & pricing

- Improved unit economics

Diversified product suite and deposits

Nu’s diversified suite across payments, accounts, lending and investments drives higher ARPU and stickiness; with over 70 million customers and customer deposits surpassing $20bn in 2024, deposits offer low‑cost, stable funding versus wholesale; cross‑product bundling in one unified app boosts retention and lifetime value by reducing friction across use cases.

- Multiple products → higher ARPU

- Deposits > $20bn (2024) → low‑cost funding

- Bundling → improved retention/LTV

- Unified app → reduced friction

Scale: ~75M, $20bn deposits fuel cloud growth

Scale: ~75M customers (2024) with >$20bn deposits provides low‑cost funding, cross‑sell base and network effects.

Digital, cloud‑native model and automation lower unit costs and speed rollouts, improving operating leverage as cohorts mature.

Proprietary ML risk models and behavioral data enable better credit selection, dynamic pricing and higher ARPU across payments, lending and investments.

| Metric | 2024 |

|---|---|

| Customers | ~75M |

| Deposits | >$20bn |

| Markets | Brazil, Mexico, Colombia, Peru |

| Growth | Double‑digit YoY |

What is included in the product

Delivers a strategic overview of Nu Holdings’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and growth prospects in digital banking and fintech.

Provides a concise SWOT snapshot for Nu Holdings that clarifies strategic risks and opportunities quickly, easing stakeholder alignment and accelerating decision-making.

Weaknesses

Exposure to unsecured credit risk

Core lending at Nu is concentrated in credit cards and personal loans, which by mid-2024 served over 60 million customers and drive most retail receivables. These segments are cyclical and sensitive to employment and income shocks, with Brazil's unemployment hovering around 8–9% in 2024 amplifying default risk. Loss volatility can compress margins in downturns, so risk control requires continual model tuning and conservative provisioning.

Macroeconomic and FX sensitivity

Operations concentrated in Latin America, chiefly Brazil and Mexico, leave Nu highly exposed to inflation and interest-rate swings; Brazil's Selic rate peaked at 13.75% in 2023, influencing loan pricing and funding costs. Currency fluctuations between BRL/MXN and USD distort reported revenue and CET1-equivalent ratios, complicating investor comparability. Consumer demand and credit performance can deteriorate rapidly in stress, and Nu's hedges only partially offset this volatility.

Regulatory fragmentation

Nu Holdings faces regulatory fragmentation across the 4+ Latin American markets where it operates, each with distinct banking, payments, data, and consumer rules.

This compliance complexity raises operating costs and slows product rollout; Nu’s NYSE listing (NU) since December 2021 also increases cross-border oversight.

Sudden rule changes can impact fees, capital or pricing, and coordination across multiple regulators adds material execution risk.

Geographic concentration

Nu remains heavily weighted to Brazil, which accounted for about 80% of revenues in 2024, concentrating risk in one macro and policy environment. This concentration heightens exposure to local economic downturns, FX swings, or regulatory shifts. Diversification into Mexico and Colombia is still nascent, and scaling new markets requires significant capital and time to reach profitability.

- ~80% revenue from Brazil (2024)

- Diversification early: Mexico, Colombia

- High exposure to local policy/economic shocks

- Scaling new markets needs substantial investment/time

Monetization still maturing

Monetization still maturing: newer verticals—investments, insurance and SME services—remain early in lifecycle and contribute only a small share of revenue, despite Nu serving over 80 million customers by end-2024; take rates are modest and likely to stay low until deeper penetration and richer product suites lift yields. Cross-sell hinges on sustained trust and execution, and profitability can lag user growth during expansion.

- Early-stage verticals: low revenue share

- Take rates: modest until penetration rises

- Cross-sell: dependent on trust/execution

- Profitability: may trail user growth

Brazil-focused cards and personal loans risk earnings; ~80% revenue

Nu's loan book is concentrated in credit cards and personal loans, exposing earnings to cyclical defaults (Brazil unemployment ~8–9% in 2024) and loss volatility. Geographic concentration—~80% revenue from Brazil (2024) with early-stage Mexico/Colombia expansion—raises policy, FX and execution risk. Monetization of investments, insurance and SME services remains small despite >80m customers end-2024.

| Metric | Value |

|---|---|

| Revenue from Brazil (2024) | ~80% |

| Customers (end-2024) | >80m |

| Core lending segments | Cards, personal loans |

What You See Is What You Get

Nu Holdings SWOT Analysis

This is the actual Nu Holdings SWOT analysis you'll receive upon purchase—no surprises, just a professional, structured report. The preview below is taken directly from the full document; buy to unlock the complete, editable version. The file shown is the real analysis you’ll download post-purchase, with full strengths, weaknesses, opportunities and threats.