NVIDIA Porter's Five Forces Analysis

From Overview to Strategy Blueprint

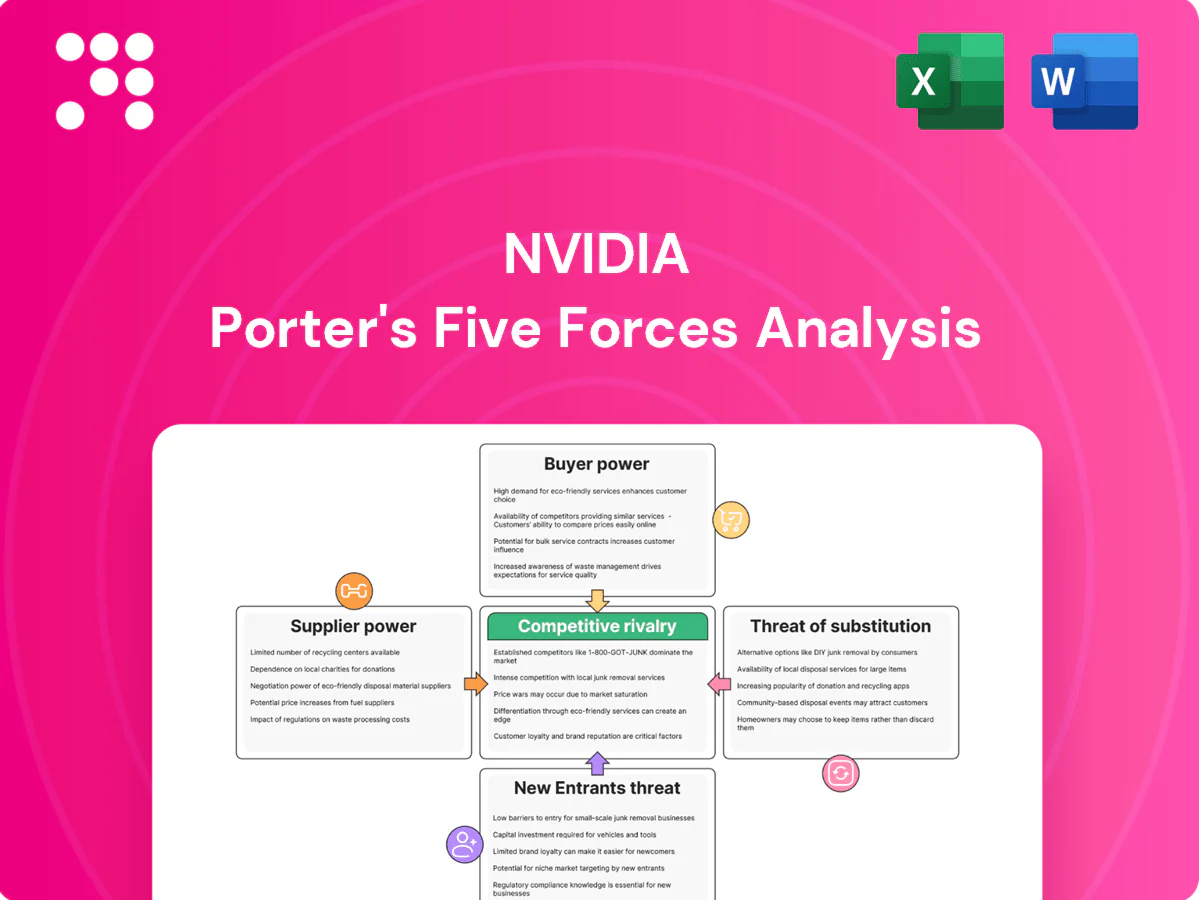

NVIDIA faces intense rivalry, significant supplier and buyer power within the semiconductor and AI ecosystems, and moderate threats from substitutes and new entrants as AI demand reshapes barriers; strategic partnerships and proprietary IP are key defenses. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NVIDIA’s competitive dynamics in detail.

Suppliers Bargaining Power

HBM memory oligopoly constraints

HBM supply is concentrated among SK Hynix, Samsung and Micron, giving them allocation and pricing leverage over NVIDIA. AI accelerators increasingly use large HBM stacks (NVIDIA H100 variants use up to 80GB), putting pressure on constrained HBM capacity. NVIDIA frequently signs long-term agreements and makes prepayments to secure allocations, partially mitigating supplier risk. Yield shortfalls or process-node transitions at suppliers can directly delay NVIDIA delivery timelines.

Foundry dependence on advanced nodes

NVIDIA relies on TSMC for the bulk of N5/N4/N3-class wafers, with TSMC controlling roughly 80–90% of sub-5nm capacity in 2024, concentrating supplier power and pricing leverage. Limited alternative capacity at comparable performance tightens lead times and raises bargaining risk; past cycle lead times stretched 20–30+ weeks. Geopolitical or capacity shocks could sharply increase costs and delays. Shifting to Samsung is feasible but requires requalification and often yields or performance trade-offs.

Advanced packaging and substrate bottlenecks

CoWoS/SoIC capacity and high-end substrate supply remained scarce in 2024, empowering OSATs and substrate vendors as bottlenecks tightened and utilization climbed; reported lead times often exceeded 20 weeks. AI GPU modules need complex integration, raising supplier switching costs and locking NVIDIA into specialized OSAT/substrate chains. NVIDIA’s capacity reservations mitigate risk but do not remove these constraints, and delays in packaging can be more binding than wafer shortages.

EDA, IP, and equipment dependencies

Critical EDA tools and licensed IP are concentrated: Synopsys, Cadence and Siemens EDA control >85% of the EDA/IP market (2024), so tool pricing and license terms can materially influence NVIDIA’s R&D cadence and costs; US export controls since 2023 can limit tool availability for certain designs; vendor diversification exists but switching is time-consuming and operationally risky.

- Concentration: >85% EDA/IP (2024)

- Export limits: US controls since 2023

- Switching: months–years, high integration risk

Networking, optics, and component ecosystems

High-speed optics, controllers, power modules and interconnects are concentrated among specialized suppliers; 2024 industry reports show optics lead times often exceeding 16 weeks and strict qualification cycles, increasing supplier leverage. Shortages in optics or power modules can stall full system shipments and delay rack-scale deployments. NVIDIA reduces risk via vertical integration in networking (Mellanox acquisition) but still relies on select partners for key components.

- Lead times: >16 weeks (2024)

- Risk: shortages can stop system shipments

- Mitigation: vertical integration (networking) + selective sourcing

Supplier leverage rising: limited HBM sources, concentrated sub-5nm foundries and long lead times

Supplier power is high: HBM (SK Hynix, Samsung, Micron) and TSMC dominance (80–90% sub‑5nm in 2024) create allocation and pricing leverage, while scarce CoWoS/substrates and optics raise switching costs and lead times. NVIDIA mitigates via long‑term contracts, prepayments and reservations but material supply shocks can delay shipments and raise costs.

| Supplier | 2024 metric | Lead time |

|---|---|---|

| HBM | 3 suppliers | >20 weeks |

| TSMC | 80–90% sub‑5nm | 20–30+ weeks |

| EDA/IP | >85% market | months–years |

What is included in the product

Tailored Porter's Five Forces analysis of NVIDIA uncovering competitive intensity, supplier and buyer power, substitute threats, and barriers to entry—highlighting disruptive AI/hardware trends and strategic levers that protect market position and influence pricing and profitability.

Clear one-sheet Porter's Five Forces for NVIDIA—instantly visualize supplier, buyer, rivalry, entrant and substitute pressures with a radar chart for fast decisions. Customize force levels to reflect new chips, partnerships, or regulation and drop the chart into pitch decks or dashboards without macros.

Customers Bargaining Power

Hyperscaler and OEM concentration

Large cloud providers and top OEMs drive the bulk of NVIDIA's data-center demand—fiscal 2024 data-center revenue was about $22.6 billion, with hyperscalers representing the lion's share—giving them substantial negotiation leverage. Their orders shape GPU roadmaps and release cadence, steering features and delivery priorities. Scarcity of top-tier accelerators, however, limits their pricing power. Volume commitments and co-design deals deepen mutual dependence.

High switching costs via CUDA ecosystem

CUDA and its libraries, compilers and tooling create substantial lock-in: NVIDIA held over 80% of data‑center GPU shipments in 2024 and a developer ecosystem size cited in recent filings, making migration costly. Porting to alternatives risks measurable performance loss and months of engineering effort, reducing buyer leverage even at scale. The richer the software stack, the stickier the customer.

Supply scarcity shifts pricing power

AI accelerator demand in 2024 far outstripped supply, letting NVIDIA command premium pricing (H100 list prices ~30,000 per card) and control allocations; Data Center revenue topped about 20 billion in fiscal 2024, reflecting tight pricing power. Buyers routinely accept bundled servers, networking and software to secure GPUs, reducing willingness to push for discounts. Discount expectations are compressed near-term, though added fab capacity over time could normalize terms; for now bargaining power favors NVIDIA.

Emerging multi-sourcing and in-house chips

Buyers increasingly pursue AMD, Intel, and custom ASICs to reduce dependence on NVIDIA; NVIDIA reported FY2024 revenue of $26.97B with data‑center driving ~$20.5B, while AMD's share of discrete data‑center GPUs was roughly 10% in 2024. Multi‑sourcing raises negotiating leverage on price and features, but performance parity and software maturity remain uneven, so buyers weigh diversification against execution risk.

- NVIDIA FY2024 revenue: $26.97B

- Data‑center revenue ~ $20.5B

- AMD discrete data‑center GPU share ~10% (2024)

- Multi‑sourcing → stronger buyer leverage

- Tradeoff: diversification vs execution/software risk

Gaming and PC channels remain price-sensitive

Retail gamers and OEM PC channels remain highly price-sensitive and promotion-driven, with frequent competitive SKU launches forcing price cuts and accelerated refresh timing; channel inventory swings in 2024 created periodic margin pressure for GPU cycles. However, Data Center/AI made up over 70% of NVIDIAs FY2024 revenue, diluting overall customer leverage from the gaming/PC segment.

- Price sensitivity: retail/OEM promotions drive elasticity

- SKU pressure: competitor refreshes force rapid price resets

- Inventory risk: channel swings compress gross margins

- Mix dilution: Data Center >70% of FY2024 revenue reduces segment leverage

Hyperscalers and OEMs Hold Leverage Over AI GPU Roadmaps Despite CUDA Lock-in

Large hyperscalers and OEMs hold substantial leverage over NVIDIA's AI GPU allocations and roadmaps, but CUDA lock-in and 2024 accelerator scarcity blunt buyer pricing power. Fiscal 2024 revenue was $26.97B with Data Center ≈ $22.6B; H100 list price ≈ 30,000 and AMD discrete GPU share ≈ 10% (2024). Volume contracts and co‑design deals deepen mutual dependence.

| Metric | 2024 |

|---|---|

| FY2024 revenue | $26.97B |

| Data Center revenue | ≈ $22.6B |

| H100 list price | ≈ $30,000 |

| AMD data-center GPU share | ≈ 10% |

Preview Before You Purchase

NVIDIA Porter's Five Forces Analysis

This preview shows the exact NVIDIA Porter’s Five Forces analysis you’ll receive—fully formatted and ready for immediate download after purchase. No placeholders or samples: the file you see is the final deliverable. Use it as-is for research, presentations, or decision-making.

From Overview to Strategy Blueprint

NVIDIA faces intense rivalry, significant supplier and buyer power within the semiconductor and AI ecosystems, and moderate threats from substitutes and new entrants as AI demand reshapes barriers; strategic partnerships and proprietary IP are key defenses. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NVIDIA’s competitive dynamics in detail.

Suppliers Bargaining Power

HBM memory oligopoly constraints

HBM supply is concentrated among SK Hynix, Samsung and Micron, giving them allocation and pricing leverage over NVIDIA. AI accelerators increasingly use large HBM stacks (NVIDIA H100 variants use up to 80GB), putting pressure on constrained HBM capacity. NVIDIA frequently signs long-term agreements and makes prepayments to secure allocations, partially mitigating supplier risk. Yield shortfalls or process-node transitions at suppliers can directly delay NVIDIA delivery timelines.

Foundry dependence on advanced nodes

NVIDIA relies on TSMC for the bulk of N5/N4/N3-class wafers, with TSMC controlling roughly 80–90% of sub-5nm capacity in 2024, concentrating supplier power and pricing leverage. Limited alternative capacity at comparable performance tightens lead times and raises bargaining risk; past cycle lead times stretched 20–30+ weeks. Geopolitical or capacity shocks could sharply increase costs and delays. Shifting to Samsung is feasible but requires requalification and often yields or performance trade-offs.

Advanced packaging and substrate bottlenecks

CoWoS/SoIC capacity and high-end substrate supply remained scarce in 2024, empowering OSATs and substrate vendors as bottlenecks tightened and utilization climbed; reported lead times often exceeded 20 weeks. AI GPU modules need complex integration, raising supplier switching costs and locking NVIDIA into specialized OSAT/substrate chains. NVIDIA’s capacity reservations mitigate risk but do not remove these constraints, and delays in packaging can be more binding than wafer shortages.

EDA, IP, and equipment dependencies

Critical EDA tools and licensed IP are concentrated: Synopsys, Cadence and Siemens EDA control >85% of the EDA/IP market (2024), so tool pricing and license terms can materially influence NVIDIA’s R&D cadence and costs; US export controls since 2023 can limit tool availability for certain designs; vendor diversification exists but switching is time-consuming and operationally risky.

- Concentration: >85% EDA/IP (2024)

- Export limits: US controls since 2023

- Switching: months–years, high integration risk

Networking, optics, and component ecosystems

High-speed optics, controllers, power modules and interconnects are concentrated among specialized suppliers; 2024 industry reports show optics lead times often exceeding 16 weeks and strict qualification cycles, increasing supplier leverage. Shortages in optics or power modules can stall full system shipments and delay rack-scale deployments. NVIDIA reduces risk via vertical integration in networking (Mellanox acquisition) but still relies on select partners for key components.

- Lead times: >16 weeks (2024)

- Risk: shortages can stop system shipments

- Mitigation: vertical integration (networking) + selective sourcing

Supplier leverage rising: limited HBM sources, concentrated sub-5nm foundries and long lead times

Supplier power is high: HBM (SK Hynix, Samsung, Micron) and TSMC dominance (80–90% sub‑5nm in 2024) create allocation and pricing leverage, while scarce CoWoS/substrates and optics raise switching costs and lead times. NVIDIA mitigates via long‑term contracts, prepayments and reservations but material supply shocks can delay shipments and raise costs.

| Supplier | 2024 metric | Lead time |

|---|---|---|

| HBM | 3 suppliers | >20 weeks |

| TSMC | 80–90% sub‑5nm | 20–30+ weeks |

| EDA/IP | >85% market | months–years |

What is included in the product

Tailored Porter's Five Forces analysis of NVIDIA uncovering competitive intensity, supplier and buyer power, substitute threats, and barriers to entry—highlighting disruptive AI/hardware trends and strategic levers that protect market position and influence pricing and profitability.

Clear one-sheet Porter's Five Forces for NVIDIA—instantly visualize supplier, buyer, rivalry, entrant and substitute pressures with a radar chart for fast decisions. Customize force levels to reflect new chips, partnerships, or regulation and drop the chart into pitch decks or dashboards without macros.

Customers Bargaining Power

Hyperscaler and OEM concentration

Large cloud providers and top OEMs drive the bulk of NVIDIA's data-center demand—fiscal 2024 data-center revenue was about $22.6 billion, with hyperscalers representing the lion's share—giving them substantial negotiation leverage. Their orders shape GPU roadmaps and release cadence, steering features and delivery priorities. Scarcity of top-tier accelerators, however, limits their pricing power. Volume commitments and co-design deals deepen mutual dependence.

High switching costs via CUDA ecosystem

CUDA and its libraries, compilers and tooling create substantial lock-in: NVIDIA held over 80% of data‑center GPU shipments in 2024 and a developer ecosystem size cited in recent filings, making migration costly. Porting to alternatives risks measurable performance loss and months of engineering effort, reducing buyer leverage even at scale. The richer the software stack, the stickier the customer.

Supply scarcity shifts pricing power

AI accelerator demand in 2024 far outstripped supply, letting NVIDIA command premium pricing (H100 list prices ~30,000 per card) and control allocations; Data Center revenue topped about 20 billion in fiscal 2024, reflecting tight pricing power. Buyers routinely accept bundled servers, networking and software to secure GPUs, reducing willingness to push for discounts. Discount expectations are compressed near-term, though added fab capacity over time could normalize terms; for now bargaining power favors NVIDIA.

Emerging multi-sourcing and in-house chips

Buyers increasingly pursue AMD, Intel, and custom ASICs to reduce dependence on NVIDIA; NVIDIA reported FY2024 revenue of $26.97B with data‑center driving ~$20.5B, while AMD's share of discrete data‑center GPUs was roughly 10% in 2024. Multi‑sourcing raises negotiating leverage on price and features, but performance parity and software maturity remain uneven, so buyers weigh diversification against execution risk.

- NVIDIA FY2024 revenue: $26.97B

- Data‑center revenue ~ $20.5B

- AMD discrete data‑center GPU share ~10% (2024)

- Multi‑sourcing → stronger buyer leverage

- Tradeoff: diversification vs execution/software risk

Gaming and PC channels remain price-sensitive

Retail gamers and OEM PC channels remain highly price-sensitive and promotion-driven, with frequent competitive SKU launches forcing price cuts and accelerated refresh timing; channel inventory swings in 2024 created periodic margin pressure for GPU cycles. However, Data Center/AI made up over 70% of NVIDIAs FY2024 revenue, diluting overall customer leverage from the gaming/PC segment.

- Price sensitivity: retail/OEM promotions drive elasticity

- SKU pressure: competitor refreshes force rapid price resets

- Inventory risk: channel swings compress gross margins

- Mix dilution: Data Center >70% of FY2024 revenue reduces segment leverage

Hyperscalers and OEMs Hold Leverage Over AI GPU Roadmaps Despite CUDA Lock-in

Large hyperscalers and OEMs hold substantial leverage over NVIDIA's AI GPU allocations and roadmaps, but CUDA lock-in and 2024 accelerator scarcity blunt buyer pricing power. Fiscal 2024 revenue was $26.97B with Data Center ≈ $22.6B; H100 list price ≈ 30,000 and AMD discrete GPU share ≈ 10% (2024). Volume contracts and co‑design deals deepen mutual dependence.

| Metric | 2024 |

|---|---|

| FY2024 revenue | $26.97B |

| Data Center revenue | ≈ $22.6B |

| H100 list price | ≈ $30,000 |

| AMD data-center GPU share | ≈ 10% |

Preview Before You Purchase

NVIDIA Porter's Five Forces Analysis

This preview shows the exact NVIDIA Porter’s Five Forces analysis you’ll receive—fully formatted and ready for immediate download after purchase. No placeholders or samples: the file you see is the final deliverable. Use it as-is for research, presentations, or decision-making.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

NVIDIA faces intense rivalry, significant supplier and buyer power within the semiconductor and AI ecosystems, and moderate threats from substitutes and new entrants as AI demand reshapes barriers; strategic partnerships and proprietary IP are key defenses. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore NVIDIA’s competitive dynamics in detail.

Suppliers Bargaining Power

HBM memory oligopoly constraints

HBM supply is concentrated among SK Hynix, Samsung and Micron, giving them allocation and pricing leverage over NVIDIA. AI accelerators increasingly use large HBM stacks (NVIDIA H100 variants use up to 80GB), putting pressure on constrained HBM capacity. NVIDIA frequently signs long-term agreements and makes prepayments to secure allocations, partially mitigating supplier risk. Yield shortfalls or process-node transitions at suppliers can directly delay NVIDIA delivery timelines.

Foundry dependence on advanced nodes

NVIDIA relies on TSMC for the bulk of N5/N4/N3-class wafers, with TSMC controlling roughly 80–90% of sub-5nm capacity in 2024, concentrating supplier power and pricing leverage. Limited alternative capacity at comparable performance tightens lead times and raises bargaining risk; past cycle lead times stretched 20–30+ weeks. Geopolitical or capacity shocks could sharply increase costs and delays. Shifting to Samsung is feasible but requires requalification and often yields or performance trade-offs.

Advanced packaging and substrate bottlenecks

CoWoS/SoIC capacity and high-end substrate supply remained scarce in 2024, empowering OSATs and substrate vendors as bottlenecks tightened and utilization climbed; reported lead times often exceeded 20 weeks. AI GPU modules need complex integration, raising supplier switching costs and locking NVIDIA into specialized OSAT/substrate chains. NVIDIA’s capacity reservations mitigate risk but do not remove these constraints, and delays in packaging can be more binding than wafer shortages.

EDA, IP, and equipment dependencies

Critical EDA tools and licensed IP are concentrated: Synopsys, Cadence and Siemens EDA control >85% of the EDA/IP market (2024), so tool pricing and license terms can materially influence NVIDIA’s R&D cadence and costs; US export controls since 2023 can limit tool availability for certain designs; vendor diversification exists but switching is time-consuming and operationally risky.

- Concentration: >85% EDA/IP (2024)

- Export limits: US controls since 2023

- Switching: months–years, high integration risk

Networking, optics, and component ecosystems

High-speed optics, controllers, power modules and interconnects are concentrated among specialized suppliers; 2024 industry reports show optics lead times often exceeding 16 weeks and strict qualification cycles, increasing supplier leverage. Shortages in optics or power modules can stall full system shipments and delay rack-scale deployments. NVIDIA reduces risk via vertical integration in networking (Mellanox acquisition) but still relies on select partners for key components.

- Lead times: >16 weeks (2024)

- Risk: shortages can stop system shipments

- Mitigation: vertical integration (networking) + selective sourcing

Supplier leverage rising: limited HBM sources, concentrated sub-5nm foundries and long lead times

Supplier power is high: HBM (SK Hynix, Samsung, Micron) and TSMC dominance (80–90% sub‑5nm in 2024) create allocation and pricing leverage, while scarce CoWoS/substrates and optics raise switching costs and lead times. NVIDIA mitigates via long‑term contracts, prepayments and reservations but material supply shocks can delay shipments and raise costs.

| Supplier | 2024 metric | Lead time |

|---|---|---|

| HBM | 3 suppliers | >20 weeks |

| TSMC | 80–90% sub‑5nm | 20–30+ weeks |

| EDA/IP | >85% market | months–years |

What is included in the product

Tailored Porter's Five Forces analysis of NVIDIA uncovering competitive intensity, supplier and buyer power, substitute threats, and barriers to entry—highlighting disruptive AI/hardware trends and strategic levers that protect market position and influence pricing and profitability.

Clear one-sheet Porter's Five Forces for NVIDIA—instantly visualize supplier, buyer, rivalry, entrant and substitute pressures with a radar chart for fast decisions. Customize force levels to reflect new chips, partnerships, or regulation and drop the chart into pitch decks or dashboards without macros.

Customers Bargaining Power

Hyperscaler and OEM concentration

Large cloud providers and top OEMs drive the bulk of NVIDIA's data-center demand—fiscal 2024 data-center revenue was about $22.6 billion, with hyperscalers representing the lion's share—giving them substantial negotiation leverage. Their orders shape GPU roadmaps and release cadence, steering features and delivery priorities. Scarcity of top-tier accelerators, however, limits their pricing power. Volume commitments and co-design deals deepen mutual dependence.

High switching costs via CUDA ecosystem

CUDA and its libraries, compilers and tooling create substantial lock-in: NVIDIA held over 80% of data‑center GPU shipments in 2024 and a developer ecosystem size cited in recent filings, making migration costly. Porting to alternatives risks measurable performance loss and months of engineering effort, reducing buyer leverage even at scale. The richer the software stack, the stickier the customer.

Supply scarcity shifts pricing power

AI accelerator demand in 2024 far outstripped supply, letting NVIDIA command premium pricing (H100 list prices ~30,000 per card) and control allocations; Data Center revenue topped about 20 billion in fiscal 2024, reflecting tight pricing power. Buyers routinely accept bundled servers, networking and software to secure GPUs, reducing willingness to push for discounts. Discount expectations are compressed near-term, though added fab capacity over time could normalize terms; for now bargaining power favors NVIDIA.

Emerging multi-sourcing and in-house chips

Buyers increasingly pursue AMD, Intel, and custom ASICs to reduce dependence on NVIDIA; NVIDIA reported FY2024 revenue of $26.97B with data‑center driving ~$20.5B, while AMD's share of discrete data‑center GPUs was roughly 10% in 2024. Multi‑sourcing raises negotiating leverage on price and features, but performance parity and software maturity remain uneven, so buyers weigh diversification against execution risk.

- NVIDIA FY2024 revenue: $26.97B

- Data‑center revenue ~ $20.5B

- AMD discrete data‑center GPU share ~10% (2024)

- Multi‑sourcing → stronger buyer leverage

- Tradeoff: diversification vs execution/software risk

Gaming and PC channels remain price-sensitive

Retail gamers and OEM PC channels remain highly price-sensitive and promotion-driven, with frequent competitive SKU launches forcing price cuts and accelerated refresh timing; channel inventory swings in 2024 created periodic margin pressure for GPU cycles. However, Data Center/AI made up over 70% of NVIDIAs FY2024 revenue, diluting overall customer leverage from the gaming/PC segment.

- Price sensitivity: retail/OEM promotions drive elasticity

- SKU pressure: competitor refreshes force rapid price resets

- Inventory risk: channel swings compress gross margins

- Mix dilution: Data Center >70% of FY2024 revenue reduces segment leverage

Hyperscalers and OEMs Hold Leverage Over AI GPU Roadmaps Despite CUDA Lock-in

Large hyperscalers and OEMs hold substantial leverage over NVIDIA's AI GPU allocations and roadmaps, but CUDA lock-in and 2024 accelerator scarcity blunt buyer pricing power. Fiscal 2024 revenue was $26.97B with Data Center ≈ $22.6B; H100 list price ≈ 30,000 and AMD discrete GPU share ≈ 10% (2024). Volume contracts and co‑design deals deepen mutual dependence.

| Metric | 2024 |

|---|---|

| FY2024 revenue | $26.97B |

| Data Center revenue | ≈ $22.6B |

| H100 list price | ≈ $30,000 |

| AMD data-center GPU share | ≈ 10% |

Preview Before You Purchase

NVIDIA Porter's Five Forces Analysis

This preview shows the exact NVIDIA Porter’s Five Forces analysis you’ll receive—fully formatted and ready for immediate download after purchase. No placeholders or samples: the file you see is the final deliverable. Use it as-is for research, presentations, or decision-making.