New Wave Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

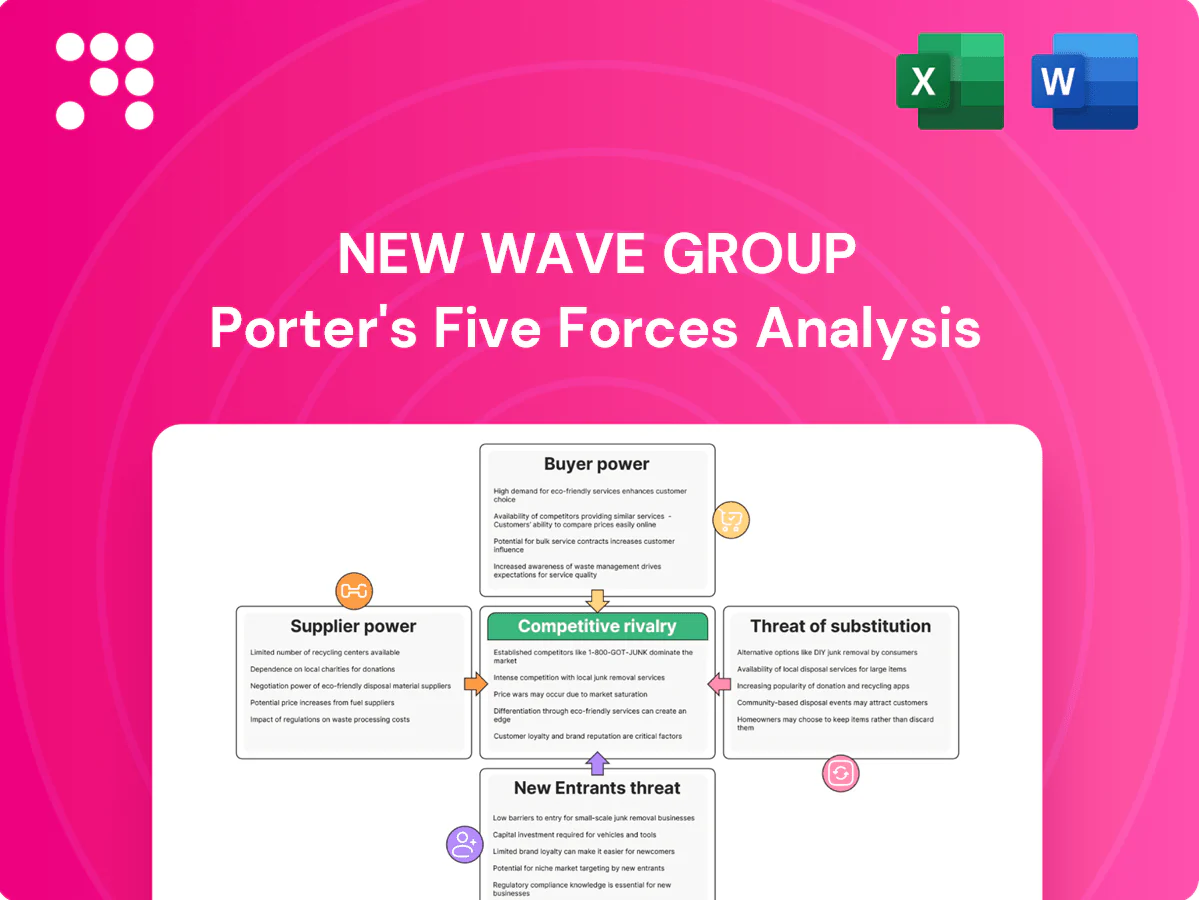

New Wave Group faces mixed competitive pressures—moderate supplier leverage, concentrated buyer segments, and evolving substitute threats that reshape margins and growth prospects. This snapshot highlights key tensions but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis for detailed visuals, ratings, and strategic recommendations to inform investment or corporate decisions.

Suppliers Bargaining Power

Input concentration

Many textiles, trims and packaging come from concentrated supplier bases in Asia and Europe, with China supplying roughly one-third of global textile exports as of 2024 and key European hubs in Turkey and Italy; specialty or certified sustainable materials narrow options and raise supplier leverage. New Wave can mitigate via multi-sourcing, but certification and quality consistency limit switching; long-term contracts and volume commitments temper pricing power.

Commodity volatility

Commodity volatility is high: ICE cotton averaged about $0.85/lb in 2024 and Brent crude averaged roughly $84/bbl, while container freight and polyester feedstock prices remained sensitive to global demand spikes, forcing suppliers to pass surcharges that squeeze margins on fixed-price B2B contracts. Hedging and dynamic-pricing clauses reduce but do not eliminate exposure, and active inventory planning is critical to smoothing cost volatility.

Customization capacity

Embroidery, screen print, heat-transfer and on-demand personalization depend on specialized equipment and skilled operators, with typical lead times ranging from 3–14 days depending on technique and order size. Capacity bottlenecks during peak seasons can push order backlogs up by 20–40%, giving decorators greater bargaining power. Vertical integration or preferred supplier networks reduce constraints and can cut lead times by weeks. Lead-time agility remains a key bargaining chip in negotiations.

Compliance and ESG

Audited, compliant factories command premiums as ESG and traceability requirements rise; 2024 industry surveys report supplier premiums of 5–20% in apparel and promotional goods. Limited availability of certified suppliers increases their pricing power and risks lost tenders in Europe and North America. Partnership programs can align incentives and stabilize terms.

- Audited suppliers: price premium 5–20%

- Certified capacity: scarce, upsupplier leverage

- Risk: lost EU/NA tenders if noncompliant

- Mitigation: partnership programs to stabilize terms

Logistics dependencies

Transcontinental shipping lanes and regional warehousing drive landed cost and service levels: seaborne trade still accounts for over 80% of global trade by volume in 2024 and Asia–Europe sailings typically take 30–40 days, making routing and inventory placement critical to cost. Disruptions shift bargaining power to carriers and freight forwarders during tight markets as capacity becomes the chokepoint; nearshoring and diversified routings reduce that exposure. Better forecast accuracy strengthens negotiation on space and rates by reducing emergency air/freight spend and improving contract leverage.

- Seaborne share 2024: >80% global trade by volume

- Asia–Europe transit: 30–40 days

- Nearshoring: cuts transit risk via shorter lanes

- Forecasting: reduces premium expedited spend and improves rate leverage

Rising supplier leverage: China share, ESG premiums, commodities and shipping constraints

Suppliers hold moderate to high power: China supplies ~1/3 of textile exports (2024) and certified materials are scarce, creating 5–20% ESG premiums and switching limits. Commodity moves (ICE cotton ~$0.85/lb, Brent ~$84/bbl in 2024) and peak-season bottlenecks (order backlogs +20–40%) amplify supplier leverage. Shipping (>80% seaborne; Asia–Europe 30–40 days) further shifts power to carriers during tight markets.

| Metric | 2024 Value |

|---|---|

| China share | ~33% |

| ICE cotton | $0.85/lb |

| Brent | $84/bbl |

| ESG premium | 5–20% |

| Seaborne trade | >80% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to New Wave Group; evaluates supplier and buyer power, rivalry, substitutes and entry barriers, highlights disruptive threats and strategic levers to protect margins and inform investor or management decision‑making.

Clear one-sheet Porter's Five Forces for New Wave Group—instantly visualize strategic pressure with a spider chart, customize force levels with your data, and drop the clean layout straight into pitch decks or dashboards without macros.

Customers Bargaining Power

Corporate bulk buyers

Large B2B clients buy promo goods via tenders and frame agreements, exerting strong price pressure and representing a large share of the roughly USD 24 billion global promotional-products market in 2024. They can switch among many suppliers, but offering integrated branding, service SLAs and data-driven replenishment raises switching costs. Multi-year frame agreements commonly span 3–5 years, locking in volume and margins.

Retail consumers

Retail consumers face high price transparency as B2C shoppers compare apparel and gifts across countless online brands, with online apparel penetration around 30% globally in 2024. Rapid fashion cycles and frequent discounting make demand highly promotion-sensitive. Strong brand identity and perceived quality help defend price points, while direct-to-consumer experiences and loyalty programs reduce pure price-driven switching.

Customization stickiness

Artwork libraries, brand guidelines, and approved colorways create process lock-in by embedding assets and standards into procurement workflows, raising switching costs for buyers. Buyers prioritize consistency and speed for repeat orders, lowering churn when fulfillment is reliable. Self-service portals and API ordering deepen integration and drive higher lifetime value. If SLAs slip, however, buyers can pivot to alternatives with lower switching friction.

Channel intermediaries

Channel intermediaries aggregate demand and push hard on margins, shaping New Wave Groups product mix and retail placement; New Wave reported net sales of SEK 7,037 million in 2023, highlighting distributor-driven scale in promotional goods. They steer end-customer choices through curated assortments, while co-op marketing and exclusive ranges secure shelf space and visibility. Tiered pricing tied to volume and sell-through aligns incentives and improves sell-rate predictability.

- Distributors negotiate margins, compressing unit profit

- Influence brand mix and shelf placement

- Co-op marketing/exclusives secure visibility

- Tiered pricing links discounts to volume & sell-through

E-procurement pressure

Promo buyers squeeze margins 3-7%; bundles capture 5-12%

Customers wield strong price leverage in the ~USD 24bn promo-products market (2024) and via e-procurement (65% of large buyers, 2024), compressing commoditized SKU margins ~3–7%. Frame agreements (3–5 years) and integrated services raise switching costs; bundled/sustainability offers win premiums of 5–12%.

| Metric | Value | Impact |

|---|---|---|

| Market size (2024) | USD 24bn | High buyer leverage |

| E-procurement | 65% | Price transparency |

| Margin compression | 3–7% | On commoditized SKUs |

| Premiums | 5–12% | For bundles/sustainability |

What You See Is What You Get

New Wave Group Porter's Five Forces Analysis

This preview shows the exact New Wave Group Porter's Five Forces analysis you'll receive—no mockups, no placeholders. The document is fully formatted and ready for immediate download and use upon purchase. You're viewing the final deliverable, identical to the file you'll get.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

New Wave Group faces mixed competitive pressures—moderate supplier leverage, concentrated buyer segments, and evolving substitute threats that reshape margins and growth prospects. This snapshot highlights key tensions but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis for detailed visuals, ratings, and strategic recommendations to inform investment or corporate decisions.

Suppliers Bargaining Power

Input concentration

Many textiles, trims and packaging come from concentrated supplier bases in Asia and Europe, with China supplying roughly one-third of global textile exports as of 2024 and key European hubs in Turkey and Italy; specialty or certified sustainable materials narrow options and raise supplier leverage. New Wave can mitigate via multi-sourcing, but certification and quality consistency limit switching; long-term contracts and volume commitments temper pricing power.

Commodity volatility

Commodity volatility is high: ICE cotton averaged about $0.85/lb in 2024 and Brent crude averaged roughly $84/bbl, while container freight and polyester feedstock prices remained sensitive to global demand spikes, forcing suppliers to pass surcharges that squeeze margins on fixed-price B2B contracts. Hedging and dynamic-pricing clauses reduce but do not eliminate exposure, and active inventory planning is critical to smoothing cost volatility.

Customization capacity

Embroidery, screen print, heat-transfer and on-demand personalization depend on specialized equipment and skilled operators, with typical lead times ranging from 3–14 days depending on technique and order size. Capacity bottlenecks during peak seasons can push order backlogs up by 20–40%, giving decorators greater bargaining power. Vertical integration or preferred supplier networks reduce constraints and can cut lead times by weeks. Lead-time agility remains a key bargaining chip in negotiations.

Compliance and ESG

Audited, compliant factories command premiums as ESG and traceability requirements rise; 2024 industry surveys report supplier premiums of 5–20% in apparel and promotional goods. Limited availability of certified suppliers increases their pricing power and risks lost tenders in Europe and North America. Partnership programs can align incentives and stabilize terms.

- Audited suppliers: price premium 5–20%

- Certified capacity: scarce, upsupplier leverage

- Risk: lost EU/NA tenders if noncompliant

- Mitigation: partnership programs to stabilize terms

Logistics dependencies

Transcontinental shipping lanes and regional warehousing drive landed cost and service levels: seaborne trade still accounts for over 80% of global trade by volume in 2024 and Asia–Europe sailings typically take 30–40 days, making routing and inventory placement critical to cost. Disruptions shift bargaining power to carriers and freight forwarders during tight markets as capacity becomes the chokepoint; nearshoring and diversified routings reduce that exposure. Better forecast accuracy strengthens negotiation on space and rates by reducing emergency air/freight spend and improving contract leverage.

- Seaborne share 2024: >80% global trade by volume

- Asia–Europe transit: 30–40 days

- Nearshoring: cuts transit risk via shorter lanes

- Forecasting: reduces premium expedited spend and improves rate leverage

Rising supplier leverage: China share, ESG premiums, commodities and shipping constraints

Suppliers hold moderate to high power: China supplies ~1/3 of textile exports (2024) and certified materials are scarce, creating 5–20% ESG premiums and switching limits. Commodity moves (ICE cotton ~$0.85/lb, Brent ~$84/bbl in 2024) and peak-season bottlenecks (order backlogs +20–40%) amplify supplier leverage. Shipping (>80% seaborne; Asia–Europe 30–40 days) further shifts power to carriers during tight markets.

| Metric | 2024 Value |

|---|---|

| China share | ~33% |

| ICE cotton | $0.85/lb |

| Brent | $84/bbl |

| ESG premium | 5–20% |

| Seaborne trade | >80% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to New Wave Group; evaluates supplier and buyer power, rivalry, substitutes and entry barriers, highlights disruptive threats and strategic levers to protect margins and inform investor or management decision‑making.

Clear one-sheet Porter's Five Forces for New Wave Group—instantly visualize strategic pressure with a spider chart, customize force levels with your data, and drop the clean layout straight into pitch decks or dashboards without macros.

Customers Bargaining Power

Corporate bulk buyers

Large B2B clients buy promo goods via tenders and frame agreements, exerting strong price pressure and representing a large share of the roughly USD 24 billion global promotional-products market in 2024. They can switch among many suppliers, but offering integrated branding, service SLAs and data-driven replenishment raises switching costs. Multi-year frame agreements commonly span 3–5 years, locking in volume and margins.

Retail consumers

Retail consumers face high price transparency as B2C shoppers compare apparel and gifts across countless online brands, with online apparel penetration around 30% globally in 2024. Rapid fashion cycles and frequent discounting make demand highly promotion-sensitive. Strong brand identity and perceived quality help defend price points, while direct-to-consumer experiences and loyalty programs reduce pure price-driven switching.

Customization stickiness

Artwork libraries, brand guidelines, and approved colorways create process lock-in by embedding assets and standards into procurement workflows, raising switching costs for buyers. Buyers prioritize consistency and speed for repeat orders, lowering churn when fulfillment is reliable. Self-service portals and API ordering deepen integration and drive higher lifetime value. If SLAs slip, however, buyers can pivot to alternatives with lower switching friction.

Channel intermediaries

Channel intermediaries aggregate demand and push hard on margins, shaping New Wave Groups product mix and retail placement; New Wave reported net sales of SEK 7,037 million in 2023, highlighting distributor-driven scale in promotional goods. They steer end-customer choices through curated assortments, while co-op marketing and exclusive ranges secure shelf space and visibility. Tiered pricing tied to volume and sell-through aligns incentives and improves sell-rate predictability.

- Distributors negotiate margins, compressing unit profit

- Influence brand mix and shelf placement

- Co-op marketing/exclusives secure visibility

- Tiered pricing links discounts to volume & sell-through

E-procurement pressure

Promo buyers squeeze margins 3-7%; bundles capture 5-12%

Customers wield strong price leverage in the ~USD 24bn promo-products market (2024) and via e-procurement (65% of large buyers, 2024), compressing commoditized SKU margins ~3–7%. Frame agreements (3–5 years) and integrated services raise switching costs; bundled/sustainability offers win premiums of 5–12%.

| Metric | Value | Impact |

|---|---|---|

| Market size (2024) | USD 24bn | High buyer leverage |

| E-procurement | 65% | Price transparency |

| Margin compression | 3–7% | On commoditized SKUs |

| Premiums | 5–12% | For bundles/sustainability |

What You See Is What You Get

New Wave Group Porter's Five Forces Analysis

This preview shows the exact New Wave Group Porter's Five Forces analysis you'll receive—no mockups, no placeholders. The document is fully formatted and ready for immediate download and use upon purchase. You're viewing the final deliverable, identical to the file you'll get.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

New Wave Group faces mixed competitive pressures—moderate supplier leverage, concentrated buyer segments, and evolving substitute threats that reshape margins and growth prospects. This snapshot highlights key tensions but omits force-by-force ratings and tactical implications. Unlock the full Porter's Five Forces Analysis for detailed visuals, ratings, and strategic recommendations to inform investment or corporate decisions.

Suppliers Bargaining Power

Input concentration

Many textiles, trims and packaging come from concentrated supplier bases in Asia and Europe, with China supplying roughly one-third of global textile exports as of 2024 and key European hubs in Turkey and Italy; specialty or certified sustainable materials narrow options and raise supplier leverage. New Wave can mitigate via multi-sourcing, but certification and quality consistency limit switching; long-term contracts and volume commitments temper pricing power.

Commodity volatility

Commodity volatility is high: ICE cotton averaged about $0.85/lb in 2024 and Brent crude averaged roughly $84/bbl, while container freight and polyester feedstock prices remained sensitive to global demand spikes, forcing suppliers to pass surcharges that squeeze margins on fixed-price B2B contracts. Hedging and dynamic-pricing clauses reduce but do not eliminate exposure, and active inventory planning is critical to smoothing cost volatility.

Customization capacity

Embroidery, screen print, heat-transfer and on-demand personalization depend on specialized equipment and skilled operators, with typical lead times ranging from 3–14 days depending on technique and order size. Capacity bottlenecks during peak seasons can push order backlogs up by 20–40%, giving decorators greater bargaining power. Vertical integration or preferred supplier networks reduce constraints and can cut lead times by weeks. Lead-time agility remains a key bargaining chip in negotiations.

Compliance and ESG

Audited, compliant factories command premiums as ESG and traceability requirements rise; 2024 industry surveys report supplier premiums of 5–20% in apparel and promotional goods. Limited availability of certified suppliers increases their pricing power and risks lost tenders in Europe and North America. Partnership programs can align incentives and stabilize terms.

- Audited suppliers: price premium 5–20%

- Certified capacity: scarce, upsupplier leverage

- Risk: lost EU/NA tenders if noncompliant

- Mitigation: partnership programs to stabilize terms

Logistics dependencies

Transcontinental shipping lanes and regional warehousing drive landed cost and service levels: seaborne trade still accounts for over 80% of global trade by volume in 2024 and Asia–Europe sailings typically take 30–40 days, making routing and inventory placement critical to cost. Disruptions shift bargaining power to carriers and freight forwarders during tight markets as capacity becomes the chokepoint; nearshoring and diversified routings reduce that exposure. Better forecast accuracy strengthens negotiation on space and rates by reducing emergency air/freight spend and improving contract leverage.

- Seaborne share 2024: >80% global trade by volume

- Asia–Europe transit: 30–40 days

- Nearshoring: cuts transit risk via shorter lanes

- Forecasting: reduces premium expedited spend and improves rate leverage

Rising supplier leverage: China share, ESG premiums, commodities and shipping constraints

Suppliers hold moderate to high power: China supplies ~1/3 of textile exports (2024) and certified materials are scarce, creating 5–20% ESG premiums and switching limits. Commodity moves (ICE cotton ~$0.85/lb, Brent ~$84/bbl in 2024) and peak-season bottlenecks (order backlogs +20–40%) amplify supplier leverage. Shipping (>80% seaborne; Asia–Europe 30–40 days) further shifts power to carriers during tight markets.

| Metric | 2024 Value |

|---|---|

| China share | ~33% |

| ICE cotton | $0.85/lb |

| Brent | $84/bbl |

| ESG premium | 5–20% |

| Seaborne trade | >80% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to New Wave Group; evaluates supplier and buyer power, rivalry, substitutes and entry barriers, highlights disruptive threats and strategic levers to protect margins and inform investor or management decision‑making.

Clear one-sheet Porter's Five Forces for New Wave Group—instantly visualize strategic pressure with a spider chart, customize force levels with your data, and drop the clean layout straight into pitch decks or dashboards without macros.

Customers Bargaining Power

Corporate bulk buyers

Large B2B clients buy promo goods via tenders and frame agreements, exerting strong price pressure and representing a large share of the roughly USD 24 billion global promotional-products market in 2024. They can switch among many suppliers, but offering integrated branding, service SLAs and data-driven replenishment raises switching costs. Multi-year frame agreements commonly span 3–5 years, locking in volume and margins.

Retail consumers

Retail consumers face high price transparency as B2C shoppers compare apparel and gifts across countless online brands, with online apparel penetration around 30% globally in 2024. Rapid fashion cycles and frequent discounting make demand highly promotion-sensitive. Strong brand identity and perceived quality help defend price points, while direct-to-consumer experiences and loyalty programs reduce pure price-driven switching.

Customization stickiness

Artwork libraries, brand guidelines, and approved colorways create process lock-in by embedding assets and standards into procurement workflows, raising switching costs for buyers. Buyers prioritize consistency and speed for repeat orders, lowering churn when fulfillment is reliable. Self-service portals and API ordering deepen integration and drive higher lifetime value. If SLAs slip, however, buyers can pivot to alternatives with lower switching friction.

Channel intermediaries

Channel intermediaries aggregate demand and push hard on margins, shaping New Wave Groups product mix and retail placement; New Wave reported net sales of SEK 7,037 million in 2023, highlighting distributor-driven scale in promotional goods. They steer end-customer choices through curated assortments, while co-op marketing and exclusive ranges secure shelf space and visibility. Tiered pricing tied to volume and sell-through aligns incentives and improves sell-rate predictability.

- Distributors negotiate margins, compressing unit profit

- Influence brand mix and shelf placement

- Co-op marketing/exclusives secure visibility

- Tiered pricing links discounts to volume & sell-through

E-procurement pressure

Promo buyers squeeze margins 3-7%; bundles capture 5-12%

Customers wield strong price leverage in the ~USD 24bn promo-products market (2024) and via e-procurement (65% of large buyers, 2024), compressing commoditized SKU margins ~3–7%. Frame agreements (3–5 years) and integrated services raise switching costs; bundled/sustainability offers win premiums of 5–12%.

| Metric | Value | Impact |

|---|---|---|

| Market size (2024) | USD 24bn | High buyer leverage |

| E-procurement | 65% | Price transparency |

| Margin compression | 3–7% | On commoditized SKUs |

| Premiums | 5–12% | For bundles/sustainability |

What You See Is What You Get

New Wave Group Porter's Five Forces Analysis

This preview shows the exact New Wave Group Porter's Five Forces analysis you'll receive—no mockups, no placeholders. The document is fully formatted and ready for immediate download and use upon purchase. You're viewing the final deliverable, identical to the file you'll get.