NWLGI Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

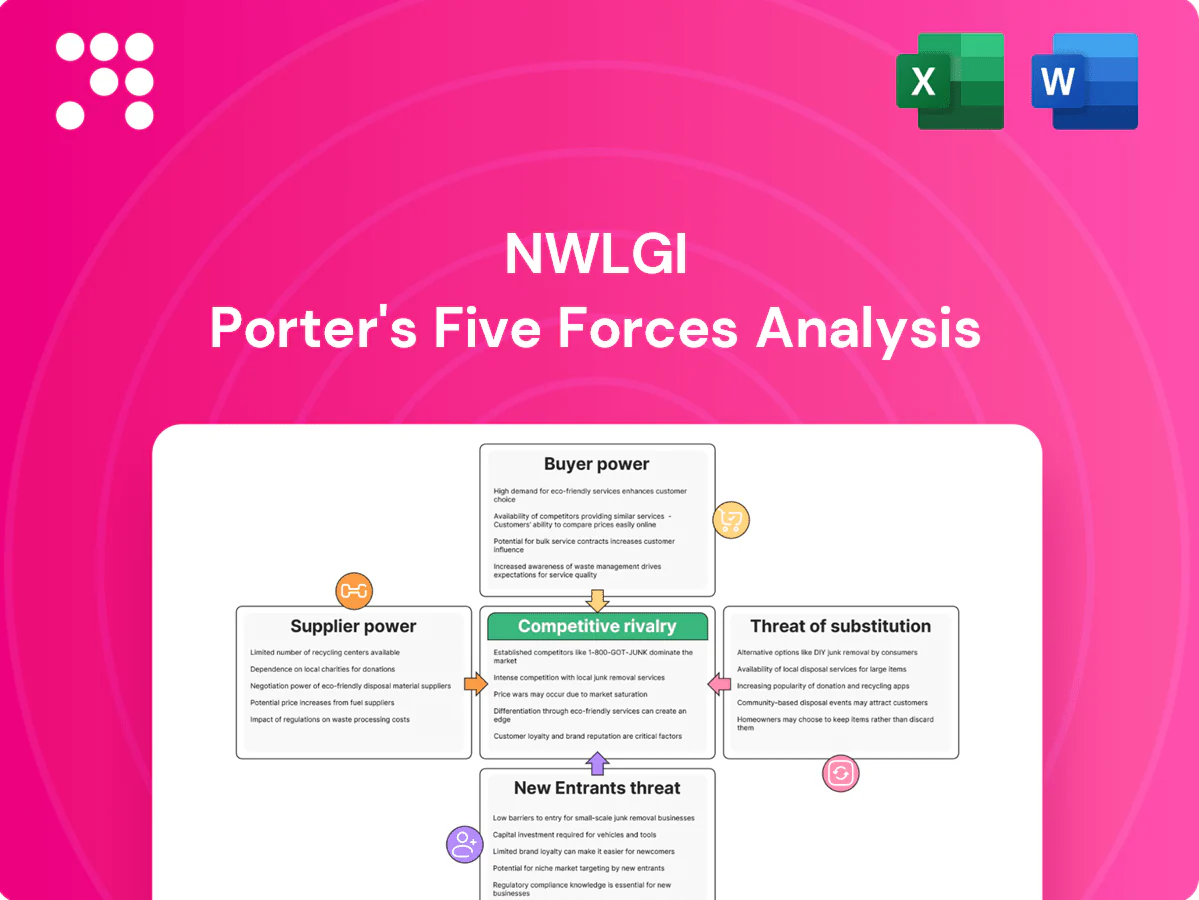

This brief Porter's Five Forces snapshot highlights NWLGI's competitive dynamics—supplier leverage, buyer power, rivalry, and threats from entrants and substitutes. The summary pinpoints immediate strategic pressures and implications. Unlock the full analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurer dependence and pricing

Reinsurance is a critical input for life and annuity risk transfer and is concentrated among a limited set of global reinsurers, giving suppliers significant bargaining power over pricing and capacity.

Tight retrocession markets and evolving mortality/longevity assumptions have pushed cession costs higher, forcing NWLGI to factor reinsurer credit ratings and renegotiation cycles into product pricing and capital relief models.

Hedging longevity, lapse, and market risks via reinsurance increases NWLGIs exposure to supplier terms and counterparty concentration risk.

Capital markets and interest-rate hedging

Yields on investment-grade bonds, such as the ICE BofA US Corporate Index near 4.5% in 2024, plus access to derivatives and ALM instruments, constitute the supplies that cap achievable annuity crediting rates.

Rate volatility widens spreads and elevates hedging costs and collateral demands, while dealers and asset managers as suppliers shape execution quality and liquidity.

NWLGI’s annuity pricing hinges on reliable, cost-efficient market access and competitive dealer execution.

Data, underwriting, and medical services

Third-party data providers, mortality tables, exam labs, and Rx/credit data materially shape underwriting precision; industry reports show the market is concentrated with a handful of vendors dominating high-quality inputs, raising switching costs and allowing pricing power. Tight consent and data-use rules (HIPAA, GDPR) in 2024 restrict portability, while accurate inputs are essential to prevent anti-selection and protect margins.

Technology platforms and administration vendors

Rating agencies and compliance services

Rating agencies and compliance frameworks act as de facto licenses to operate; the Big Three still control roughly 95% of the global ratings market, so methodology shifts can force capital reallocation and product repricing. Third-party model-validation and regulatory-reporting vendors — a market exceeding $10B in 2024 — can charge premium fees, and NWLGI’s distribution traction is highly sensitive to rating outcomes.

- 95% market share — Big Three agencies

- $10B+ regulatory services market (2024)

- Methodology changes -> capital shifts/product repricing

- Premium fees for validation/reporting vendors

- Distribution sensitive to rating outcomes

Reinsurance concentration, ratings duopoly and rising yields squeeze insurer margins

Reinsurance concentration among a few global reinsurers gives suppliers pricing and capacity leverage; cession costs and retrocession tightenings raised reinsurance premiums in 2024.

Market yields (ICE BofA corp ~4.5% in 2024), dealer execution and collateral needs cap annuity crediting and raise hedging costs.

Vendor lock‑in (policy admin, data, ratings) and regulatory services (>10B) plus Big Three ~95% market share amplify supplier power.

| Metric | 2024 |

|---|---|

| ICE BofA US Corp Yield | ~4.5% |

| Big Three ratings share | ~95% |

| Cybersecurity market | >200B |

| Regulatory services market | >10B |

What is included in the product

Tailored Porter's Five Forces analysis for NWLGI uncovering competitive drivers, supplier and buyer power, threats from substitutes and entrants, and disruptive forces—supported by industry data and strategic commentary to inform investor decks, business plans, and internal strategy.

NWLGI's Porter's Five Forces one-sheet maps competitive pressures into a clean, customizable radar so teams instantly spot and relieve strategic pain points; ready to copy into decks, tweak for scenarios, and use without macros.

Customers Bargaining Power

Price-sensitive retail policyholders

Price-sensitive retail policyholders compare premiums, crediting rates and surrender charges across carriers; 2024 industry surveys show roughly 56% using online comparison tools and broker quotes, raising buyer leverage. Small average ticket sizes (typically under $5,000 annual premium) dilute individual power, but aggregated churn enforces pricing discipline; persistency programs are critical to counter rate-shopping.

Independent agents and brokers as channel gatekeepers

Independent agents and brokers—accounting for roughly two-thirds of U.S. retail distribution in 2024—act as gatekeepers, with producers controlling shelf space and steering client recommendations, creating indirect buyer power. They demand competitive commissions (personal lines ~10–15% in 2024), responsive underwriting and fast service; multi-carrier appointments make switching easy. NWLGI must offer compelling compensation, robust training and clear product differentiation to win mindshare.

Switching costs and surrender features

Surrender charges commonly range 5–10% in early years and combined tax consequences (including the 10% IRS early-distribution penalty for under‑59½ where applicable) create material friction that tempers buyer power. Aggressive bonus credits and single‑premium step‑up rates at competitors can neutralize that pain, especially in annuities, driving observable churn. Regulatory replacement scrutiny reduces but does not eliminate replacements; product design (bonus vesting, roll‑out of credits) can tune persistency without deterring initial sales.

Demand for simplicity and speed

Buyers increasingly prioritize accelerated underwriting, digital issuance, and transparent illustrations, and carriers that cut cycle times secure leverage against price concessions; friction in underwriting elevates walk-away risk and strengthens customer negotiation power. NWLGI’s digital enablement in 2024 materially influences perceived value and retention.

- Accelerated underwriting reduces concession leverage

- Digital issuance raises perceived value

- Underwriting friction increases walk-away risk

Financial literacy and advice influence

Customer understanding of guarantees, fees and riders varies widely; in 2024 surveys 58% relied on advisors to interpret terms, so price sensitivity is often traded for feature value and protection. Advisors frame value and offset pure price pressure, while educated segments increasingly negotiate better terms and custom riders.

- 58% reliance on advisors 2024

- Educated buyers push custom riders

- Clear disclosures shape expectations

56% shop online; brokers ≈66% control sales; fees 10–15%

Retail buyers use online tools (56% in 2024) and price-shop, raising leverage, though small ticket sizes limit individual bargaining; aggregated churn enforces discipline. Brokers (≈66% distribution) steer sales, demanding 10–15% commissions and easy switching. Surrender charges (5–10%) and tax penalties dampen churn, but digital issuance and accelerated underwriting cut concession needs.

| Metric | 2024 Value |

|---|---|

| Online comparison use | 56% |

| Broker distribution | ≈66% |

| Typical commissions | 10–15% |

| Surrender charges | 5–10% |

| Advisor reliance | 58% |

Preview Before You Purchase

NWLGI Porter's Five Forces Analysis

This preview shows the exact NWLGI Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the final, professionally formatted analysis, ready for download and use the moment you buy. You’re viewing the complete deliverable and will gain instant access to this identical document upon payment.

A Must-Have Tool for Decision-Makers

This brief Porter's Five Forces snapshot highlights NWLGI's competitive dynamics—supplier leverage, buyer power, rivalry, and threats from entrants and substitutes. The summary pinpoints immediate strategic pressures and implications. Unlock the full analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurer dependence and pricing

Reinsurance is a critical input for life and annuity risk transfer and is concentrated among a limited set of global reinsurers, giving suppliers significant bargaining power over pricing and capacity.

Tight retrocession markets and evolving mortality/longevity assumptions have pushed cession costs higher, forcing NWLGI to factor reinsurer credit ratings and renegotiation cycles into product pricing and capital relief models.

Hedging longevity, lapse, and market risks via reinsurance increases NWLGIs exposure to supplier terms and counterparty concentration risk.

Capital markets and interest-rate hedging

Yields on investment-grade bonds, such as the ICE BofA US Corporate Index near 4.5% in 2024, plus access to derivatives and ALM instruments, constitute the supplies that cap achievable annuity crediting rates.

Rate volatility widens spreads and elevates hedging costs and collateral demands, while dealers and asset managers as suppliers shape execution quality and liquidity.

NWLGI’s annuity pricing hinges on reliable, cost-efficient market access and competitive dealer execution.

Data, underwriting, and medical services

Third-party data providers, mortality tables, exam labs, and Rx/credit data materially shape underwriting precision; industry reports show the market is concentrated with a handful of vendors dominating high-quality inputs, raising switching costs and allowing pricing power. Tight consent and data-use rules (HIPAA, GDPR) in 2024 restrict portability, while accurate inputs are essential to prevent anti-selection and protect margins.

Technology platforms and administration vendors

Rating agencies and compliance services

Rating agencies and compliance frameworks act as de facto licenses to operate; the Big Three still control roughly 95% of the global ratings market, so methodology shifts can force capital reallocation and product repricing. Third-party model-validation and regulatory-reporting vendors — a market exceeding $10B in 2024 — can charge premium fees, and NWLGI’s distribution traction is highly sensitive to rating outcomes.

- 95% market share — Big Three agencies

- $10B+ regulatory services market (2024)

- Methodology changes -> capital shifts/product repricing

- Premium fees for validation/reporting vendors

- Distribution sensitive to rating outcomes

Reinsurance concentration, ratings duopoly and rising yields squeeze insurer margins

Reinsurance concentration among a few global reinsurers gives suppliers pricing and capacity leverage; cession costs and retrocession tightenings raised reinsurance premiums in 2024.

Market yields (ICE BofA corp ~4.5% in 2024), dealer execution and collateral needs cap annuity crediting and raise hedging costs.

Vendor lock‑in (policy admin, data, ratings) and regulatory services (>10B) plus Big Three ~95% market share amplify supplier power.

| Metric | 2024 |

|---|---|

| ICE BofA US Corp Yield | ~4.5% |

| Big Three ratings share | ~95% |

| Cybersecurity market | >200B |

| Regulatory services market | >10B |

What is included in the product

Tailored Porter's Five Forces analysis for NWLGI uncovering competitive drivers, supplier and buyer power, threats from substitutes and entrants, and disruptive forces—supported by industry data and strategic commentary to inform investor decks, business plans, and internal strategy.

NWLGI's Porter's Five Forces one-sheet maps competitive pressures into a clean, customizable radar so teams instantly spot and relieve strategic pain points; ready to copy into decks, tweak for scenarios, and use without macros.

Customers Bargaining Power

Price-sensitive retail policyholders

Price-sensitive retail policyholders compare premiums, crediting rates and surrender charges across carriers; 2024 industry surveys show roughly 56% using online comparison tools and broker quotes, raising buyer leverage. Small average ticket sizes (typically under $5,000 annual premium) dilute individual power, but aggregated churn enforces pricing discipline; persistency programs are critical to counter rate-shopping.

Independent agents and brokers as channel gatekeepers

Independent agents and brokers—accounting for roughly two-thirds of U.S. retail distribution in 2024—act as gatekeepers, with producers controlling shelf space and steering client recommendations, creating indirect buyer power. They demand competitive commissions (personal lines ~10–15% in 2024), responsive underwriting and fast service; multi-carrier appointments make switching easy. NWLGI must offer compelling compensation, robust training and clear product differentiation to win mindshare.

Switching costs and surrender features

Surrender charges commonly range 5–10% in early years and combined tax consequences (including the 10% IRS early-distribution penalty for under‑59½ where applicable) create material friction that tempers buyer power. Aggressive bonus credits and single‑premium step‑up rates at competitors can neutralize that pain, especially in annuities, driving observable churn. Regulatory replacement scrutiny reduces but does not eliminate replacements; product design (bonus vesting, roll‑out of credits) can tune persistency without deterring initial sales.

Demand for simplicity and speed

Buyers increasingly prioritize accelerated underwriting, digital issuance, and transparent illustrations, and carriers that cut cycle times secure leverage against price concessions; friction in underwriting elevates walk-away risk and strengthens customer negotiation power. NWLGI’s digital enablement in 2024 materially influences perceived value and retention.

- Accelerated underwriting reduces concession leverage

- Digital issuance raises perceived value

- Underwriting friction increases walk-away risk

Financial literacy and advice influence

Customer understanding of guarantees, fees and riders varies widely; in 2024 surveys 58% relied on advisors to interpret terms, so price sensitivity is often traded for feature value and protection. Advisors frame value and offset pure price pressure, while educated segments increasingly negotiate better terms and custom riders.

- 58% reliance on advisors 2024

- Educated buyers push custom riders

- Clear disclosures shape expectations

56% shop online; brokers ≈66% control sales; fees 10–15%

Retail buyers use online tools (56% in 2024) and price-shop, raising leverage, though small ticket sizes limit individual bargaining; aggregated churn enforces discipline. Brokers (≈66% distribution) steer sales, demanding 10–15% commissions and easy switching. Surrender charges (5–10%) and tax penalties dampen churn, but digital issuance and accelerated underwriting cut concession needs.

| Metric | 2024 Value |

|---|---|

| Online comparison use | 56% |

| Broker distribution | ≈66% |

| Typical commissions | 10–15% |

| Surrender charges | 5–10% |

| Advisor reliance | 58% |

Preview Before You Purchase

NWLGI Porter's Five Forces Analysis

This preview shows the exact NWLGI Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the final, professionally formatted analysis, ready for download and use the moment you buy. You’re viewing the complete deliverable and will gain instant access to this identical document upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

This brief Porter's Five Forces snapshot highlights NWLGI's competitive dynamics—supplier leverage, buyer power, rivalry, and threats from entrants and substitutes. The summary pinpoints immediate strategic pressures and implications. Unlock the full analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Reinsurer dependence and pricing

Reinsurance is a critical input for life and annuity risk transfer and is concentrated among a limited set of global reinsurers, giving suppliers significant bargaining power over pricing and capacity.

Tight retrocession markets and evolving mortality/longevity assumptions have pushed cession costs higher, forcing NWLGI to factor reinsurer credit ratings and renegotiation cycles into product pricing and capital relief models.

Hedging longevity, lapse, and market risks via reinsurance increases NWLGIs exposure to supplier terms and counterparty concentration risk.

Capital markets and interest-rate hedging

Yields on investment-grade bonds, such as the ICE BofA US Corporate Index near 4.5% in 2024, plus access to derivatives and ALM instruments, constitute the supplies that cap achievable annuity crediting rates.

Rate volatility widens spreads and elevates hedging costs and collateral demands, while dealers and asset managers as suppliers shape execution quality and liquidity.

NWLGI’s annuity pricing hinges on reliable, cost-efficient market access and competitive dealer execution.

Data, underwriting, and medical services

Third-party data providers, mortality tables, exam labs, and Rx/credit data materially shape underwriting precision; industry reports show the market is concentrated with a handful of vendors dominating high-quality inputs, raising switching costs and allowing pricing power. Tight consent and data-use rules (HIPAA, GDPR) in 2024 restrict portability, while accurate inputs are essential to prevent anti-selection and protect margins.

Technology platforms and administration vendors

Rating agencies and compliance services

Rating agencies and compliance frameworks act as de facto licenses to operate; the Big Three still control roughly 95% of the global ratings market, so methodology shifts can force capital reallocation and product repricing. Third-party model-validation and regulatory-reporting vendors — a market exceeding $10B in 2024 — can charge premium fees, and NWLGI’s distribution traction is highly sensitive to rating outcomes.

- 95% market share — Big Three agencies

- $10B+ regulatory services market (2024)

- Methodology changes -> capital shifts/product repricing

- Premium fees for validation/reporting vendors

- Distribution sensitive to rating outcomes

Reinsurance concentration, ratings duopoly and rising yields squeeze insurer margins

Reinsurance concentration among a few global reinsurers gives suppliers pricing and capacity leverage; cession costs and retrocession tightenings raised reinsurance premiums in 2024.

Market yields (ICE BofA corp ~4.5% in 2024), dealer execution and collateral needs cap annuity crediting and raise hedging costs.

Vendor lock‑in (policy admin, data, ratings) and regulatory services (>10B) plus Big Three ~95% market share amplify supplier power.

| Metric | 2024 |

|---|---|

| ICE BofA US Corp Yield | ~4.5% |

| Big Three ratings share | ~95% |

| Cybersecurity market | >200B |

| Regulatory services market | >10B |

What is included in the product

Tailored Porter's Five Forces analysis for NWLGI uncovering competitive drivers, supplier and buyer power, threats from substitutes and entrants, and disruptive forces—supported by industry data and strategic commentary to inform investor decks, business plans, and internal strategy.

NWLGI's Porter's Five Forces one-sheet maps competitive pressures into a clean, customizable radar so teams instantly spot and relieve strategic pain points; ready to copy into decks, tweak for scenarios, and use without macros.

Customers Bargaining Power

Price-sensitive retail policyholders

Price-sensitive retail policyholders compare premiums, crediting rates and surrender charges across carriers; 2024 industry surveys show roughly 56% using online comparison tools and broker quotes, raising buyer leverage. Small average ticket sizes (typically under $5,000 annual premium) dilute individual power, but aggregated churn enforces pricing discipline; persistency programs are critical to counter rate-shopping.

Independent agents and brokers as channel gatekeepers

Independent agents and brokers—accounting for roughly two-thirds of U.S. retail distribution in 2024—act as gatekeepers, with producers controlling shelf space and steering client recommendations, creating indirect buyer power. They demand competitive commissions (personal lines ~10–15% in 2024), responsive underwriting and fast service; multi-carrier appointments make switching easy. NWLGI must offer compelling compensation, robust training and clear product differentiation to win mindshare.

Switching costs and surrender features

Surrender charges commonly range 5–10% in early years and combined tax consequences (including the 10% IRS early-distribution penalty for under‑59½ where applicable) create material friction that tempers buyer power. Aggressive bonus credits and single‑premium step‑up rates at competitors can neutralize that pain, especially in annuities, driving observable churn. Regulatory replacement scrutiny reduces but does not eliminate replacements; product design (bonus vesting, roll‑out of credits) can tune persistency without deterring initial sales.

Demand for simplicity and speed

Buyers increasingly prioritize accelerated underwriting, digital issuance, and transparent illustrations, and carriers that cut cycle times secure leverage against price concessions; friction in underwriting elevates walk-away risk and strengthens customer negotiation power. NWLGI’s digital enablement in 2024 materially influences perceived value and retention.

- Accelerated underwriting reduces concession leverage

- Digital issuance raises perceived value

- Underwriting friction increases walk-away risk

Financial literacy and advice influence

Customer understanding of guarantees, fees and riders varies widely; in 2024 surveys 58% relied on advisors to interpret terms, so price sensitivity is often traded for feature value and protection. Advisors frame value and offset pure price pressure, while educated segments increasingly negotiate better terms and custom riders.

- 58% reliance on advisors 2024

- Educated buyers push custom riders

- Clear disclosures shape expectations

56% shop online; brokers ≈66% control sales; fees 10–15%

Retail buyers use online tools (56% in 2024) and price-shop, raising leverage, though small ticket sizes limit individual bargaining; aggregated churn enforces discipline. Brokers (≈66% distribution) steer sales, demanding 10–15% commissions and easy switching. Surrender charges (5–10%) and tax penalties dampen churn, but digital issuance and accelerated underwriting cut concession needs.

| Metric | 2024 Value |

|---|---|

| Online comparison use | 56% |

| Broker distribution | ≈66% |

| Typical commissions | 10–15% |

| Surrender charges | 5–10% |

| Advisor reliance | 58% |

Preview Before You Purchase

NWLGI Porter's Five Forces Analysis

This preview shows the exact NWLGI Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is the final, professionally formatted analysis, ready for download and use the moment you buy. You’re viewing the complete deliverable and will gain instant access to this identical document upon payment.