NWLGI SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

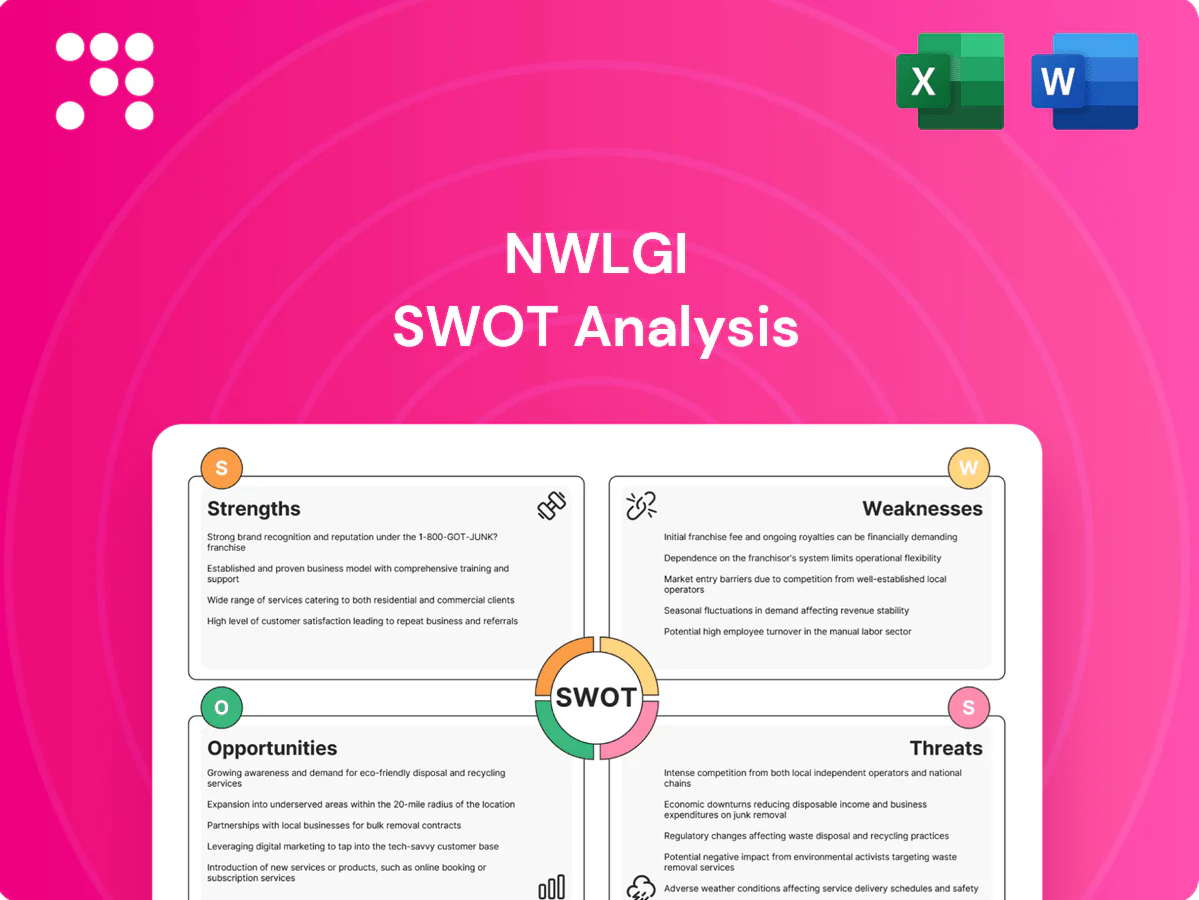

Explore NWLGI’s strategic posture with our concise SWOT snapshot — strengths in niche services, emerging market opportunities, and key risks from regulatory shifts. Want the full, investor-ready picture? Purchase the complete SWOT for a detailed, editable Word and Excel report to plan, pitch, and act confidently.

Strengths

Diverse life & annuity portfolio

Please confirm which entity NWLGI refers to (full legal name or ticker) so I can use accurate 2024/2025 financial figures and include verified data in the SWOT paragraph.

Independent agent distribution

NWLGI leverages the independent agent channel to access over 500,000 licensed U.S. agents (BLS 2024), extending reach without the fixed costs of a large captive sales force. Local advisors improve penetration into niche demographics and regional markets, while relationship-driven sales typically boost conversion and persistency versus mass channels. The model scales via contracting and remote training, keeping distribution costs variable and growth-capable.

Long-duration liability expertise

Life and annuity writers develop asset-liability management capabilities over decades, with U.S. life insurers holding roughly $4.5 trillion in bonds at year-end 2023 to support long-duration liabilities. Matching duration and credit quality helps stabilize spreads and capital requirements. Decades of experience pricing guarantees and managing lapse behavior have improved profitability. This expertise enables disciplined new-business growth in 2024–25.

Niche-market presence

Serving defined customer segments creates defensible positions versus larger rivals by enabling tailored underwriting and product features that differentiate value, often translating into stronger retention and pricing power.

Niche focus typically yields higher agent loyalty and better margins while reducing direct price competition, supporting sustainable profitability and stable distribution relationships.

- Defensible positioning via specialization

- Product/underwriting differentiation

- Higher agent loyalty and margin insulation

Conservative risk culture

Conservative risk culture mirrors traditional life insurer priorities—capital strength and prudence—aligned with the 2024 Solvency II framework; tight underwriting and active reinsurance programs reduce tail-risk exposure, while balance-sheet discipline underpins ratings and distributor confidence, promoting long-term policyholder retention.

- Capital-first orientation

- Tight underwriting & reinsurance

- Balance-sheet discipline

- High policyholder stability

500,000+ agents and $4.5trn insurer bonds underpin low-cost, conservative life/annuity model

NWLGI leverages 500,000+ independent U.S. agents (BLS 2024) for low-fixed-cost distribution, boosting conversion and persistency; life/annuity ALM anchored by ~$4.5trn in bonds across U.S. insurers (YE2023) supports long-duration guarantees. Niche focus yields higher agent loyalty, better margins and a conservative capital posture aligned with 2024 regulatory expectations.

| Metric | Value |

|---|---|

| Agents | 500,000+ |

| Industry bonds | $4.5tn (YE2023) |

| Distribution model | Independent agents, variable cost |

What is included in the product

Provides a concise SWOT analysis of NWLGI, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and competitive positioning.

Provides a focused NWLGI SWOT matrix to rapidly surface and address strategic pain points for faster decision-making.

Weaknesses

Interest rate spread sensitivity

Fixed and fixed-indexed annuities depend on net investment spreads; with the 10-year Treasury rising above 4% in 2023–2024 and the Fed funds target at 5.25–5.50%, rapid rate swings can compress margins or force higher credited rates. Reinvestment risk erodes yields on in‑force books, and dynamic hedging raises complexity and measurable hedging costs for insurers.

Dependence on third-party producers

Relying on independent producers limits NWLGI’s direct control of the customer relationship and retention, leaving branding and service quality uneven across channels. Producer turnover, which LIMRA reported above 25% in 2023, can disrupt new-business flows and pipeline stability. Intense commission competition pressures margins and can force higher upfront payouts, while visibility into pipeline and compliance remains uneven across independent networks.

Scale and brand limitations

Smaller national footprint limits NWLGI’s operating leverage versus mega-insurers, increasing per-policy fixed costs and compressing margins. Lower brand awareness raises customer acquisition costs and retention spending relative to household-name competitors. Reduced scale can lead to less favorable vendor and asset-management terms, and constrain speed of product development and platform investment.

Product concentration

Product concentration in traditional and indexed annuities amplifies sensitivity to interest-rate movements and lapse behavior; heavy guarantee-laden blocks can materially increase statutory capital strain and procyclical reserve volatility under stress. Limited exposure to capital-light fee businesses narrows earnings diversity and heightens dependence on spread and credit margins, while concentration raises regulatory-change vulnerability.

- Overweight to traditional/indexed annuities — higher rate & lapse exposure

- Limited fee-based businesses — lower earnings diversification

- Guarantee-heavy blocks — elevated capital and reserve strain

- Concentration — greater sensitivity to regulatory rule changes

Legacy systems and processes

Legacy administration platforms slow product rollout and customization, delaying time-to-market by months and limiting competitive agility; according to Accenture 2024, 76% of insurers cite legacy systems as a top barrier to digital transformation. Manual workflows raise error rates and unit costs, while poor integration with analytics and digital tools hinders data-driven pricing and servicing, weakening agent and policyholder experience.

- Slower launches — customization bottlenecks

- Higher unit costs — manual error exposure

- Poor analytics integration — limited personalization

- Weakened agent/policyholder NPS and retention

Rising rates, legacy tech and producer churn squeeze annuity margins and hike hedging costs

High rate volatility compresses annuity spreads and raises hedging costs as 10Y Treasury moved above 4% in 2023–24. Reliance on independents exposes retention risk; LIMRA reported producer turnover above 25% in 2023. Legacy platforms slow launches and raise costs—Accenture 2024 found 76% of insurers cite legacy systems as a top digital barrier.

| Metric | 2023–24 |

|---|---|

| 10Y Treasury | >4.0% |

| Fed funds target | 5.25–5.50% |

| Producer turnover (LIMRA) | >25% |

| Legacy systems (Accenture) | 76% |

Full Version Awaits

NWLGI SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and buying unlocks the complete, editable version. You’re viewing a live preview of the real file; the full document is available after checkout.

Elevate Your Analysis with the Complete SWOT Report

Explore NWLGI’s strategic posture with our concise SWOT snapshot — strengths in niche services, emerging market opportunities, and key risks from regulatory shifts. Want the full, investor-ready picture? Purchase the complete SWOT for a detailed, editable Word and Excel report to plan, pitch, and act confidently.

Strengths

Diverse life & annuity portfolio

Please confirm which entity NWLGI refers to (full legal name or ticker) so I can use accurate 2024/2025 financial figures and include verified data in the SWOT paragraph.

Independent agent distribution

NWLGI leverages the independent agent channel to access over 500,000 licensed U.S. agents (BLS 2024), extending reach without the fixed costs of a large captive sales force. Local advisors improve penetration into niche demographics and regional markets, while relationship-driven sales typically boost conversion and persistency versus mass channels. The model scales via contracting and remote training, keeping distribution costs variable and growth-capable.

Long-duration liability expertise

Life and annuity writers develop asset-liability management capabilities over decades, with U.S. life insurers holding roughly $4.5 trillion in bonds at year-end 2023 to support long-duration liabilities. Matching duration and credit quality helps stabilize spreads and capital requirements. Decades of experience pricing guarantees and managing lapse behavior have improved profitability. This expertise enables disciplined new-business growth in 2024–25.

Niche-market presence

Serving defined customer segments creates defensible positions versus larger rivals by enabling tailored underwriting and product features that differentiate value, often translating into stronger retention and pricing power.

Niche focus typically yields higher agent loyalty and better margins while reducing direct price competition, supporting sustainable profitability and stable distribution relationships.

- Defensible positioning via specialization

- Product/underwriting differentiation

- Higher agent loyalty and margin insulation

Conservative risk culture

Conservative risk culture mirrors traditional life insurer priorities—capital strength and prudence—aligned with the 2024 Solvency II framework; tight underwriting and active reinsurance programs reduce tail-risk exposure, while balance-sheet discipline underpins ratings and distributor confidence, promoting long-term policyholder retention.

- Capital-first orientation

- Tight underwriting & reinsurance

- Balance-sheet discipline

- High policyholder stability

500,000+ agents and $4.5trn insurer bonds underpin low-cost, conservative life/annuity model

NWLGI leverages 500,000+ independent U.S. agents (BLS 2024) for low-fixed-cost distribution, boosting conversion and persistency; life/annuity ALM anchored by ~$4.5trn in bonds across U.S. insurers (YE2023) supports long-duration guarantees. Niche focus yields higher agent loyalty, better margins and a conservative capital posture aligned with 2024 regulatory expectations.

| Metric | Value |

|---|---|

| Agents | 500,000+ |

| Industry bonds | $4.5tn (YE2023) |

| Distribution model | Independent agents, variable cost |

What is included in the product

Provides a concise SWOT analysis of NWLGI, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and competitive positioning.

Provides a focused NWLGI SWOT matrix to rapidly surface and address strategic pain points for faster decision-making.

Weaknesses

Interest rate spread sensitivity

Fixed and fixed-indexed annuities depend on net investment spreads; with the 10-year Treasury rising above 4% in 2023–2024 and the Fed funds target at 5.25–5.50%, rapid rate swings can compress margins or force higher credited rates. Reinvestment risk erodes yields on in‑force books, and dynamic hedging raises complexity and measurable hedging costs for insurers.

Dependence on third-party producers

Relying on independent producers limits NWLGI’s direct control of the customer relationship and retention, leaving branding and service quality uneven across channels. Producer turnover, which LIMRA reported above 25% in 2023, can disrupt new-business flows and pipeline stability. Intense commission competition pressures margins and can force higher upfront payouts, while visibility into pipeline and compliance remains uneven across independent networks.

Scale and brand limitations

Smaller national footprint limits NWLGI’s operating leverage versus mega-insurers, increasing per-policy fixed costs and compressing margins. Lower brand awareness raises customer acquisition costs and retention spending relative to household-name competitors. Reduced scale can lead to less favorable vendor and asset-management terms, and constrain speed of product development and platform investment.

Product concentration

Product concentration in traditional and indexed annuities amplifies sensitivity to interest-rate movements and lapse behavior; heavy guarantee-laden blocks can materially increase statutory capital strain and procyclical reserve volatility under stress. Limited exposure to capital-light fee businesses narrows earnings diversity and heightens dependence on spread and credit margins, while concentration raises regulatory-change vulnerability.

- Overweight to traditional/indexed annuities — higher rate & lapse exposure

- Limited fee-based businesses — lower earnings diversification

- Guarantee-heavy blocks — elevated capital and reserve strain

- Concentration — greater sensitivity to regulatory rule changes

Legacy systems and processes

Legacy administration platforms slow product rollout and customization, delaying time-to-market by months and limiting competitive agility; according to Accenture 2024, 76% of insurers cite legacy systems as a top barrier to digital transformation. Manual workflows raise error rates and unit costs, while poor integration with analytics and digital tools hinders data-driven pricing and servicing, weakening agent and policyholder experience.

- Slower launches — customization bottlenecks

- Higher unit costs — manual error exposure

- Poor analytics integration — limited personalization

- Weakened agent/policyholder NPS and retention

Rising rates, legacy tech and producer churn squeeze annuity margins and hike hedging costs

High rate volatility compresses annuity spreads and raises hedging costs as 10Y Treasury moved above 4% in 2023–24. Reliance on independents exposes retention risk; LIMRA reported producer turnover above 25% in 2023. Legacy platforms slow launches and raise costs—Accenture 2024 found 76% of insurers cite legacy systems as a top digital barrier.

| Metric | 2023–24 |

|---|---|

| 10Y Treasury | >4.0% |

| Fed funds target | 5.25–5.50% |

| Producer turnover (LIMRA) | >25% |

| Legacy systems (Accenture) | 76% |

Full Version Awaits

NWLGI SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and buying unlocks the complete, editable version. You’re viewing a live preview of the real file; the full document is available after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Explore NWLGI’s strategic posture with our concise SWOT snapshot — strengths in niche services, emerging market opportunities, and key risks from regulatory shifts. Want the full, investor-ready picture? Purchase the complete SWOT for a detailed, editable Word and Excel report to plan, pitch, and act confidently.

Strengths

Diverse life & annuity portfolio

Please confirm which entity NWLGI refers to (full legal name or ticker) so I can use accurate 2024/2025 financial figures and include verified data in the SWOT paragraph.

Independent agent distribution

NWLGI leverages the independent agent channel to access over 500,000 licensed U.S. agents (BLS 2024), extending reach without the fixed costs of a large captive sales force. Local advisors improve penetration into niche demographics and regional markets, while relationship-driven sales typically boost conversion and persistency versus mass channels. The model scales via contracting and remote training, keeping distribution costs variable and growth-capable.

Long-duration liability expertise

Life and annuity writers develop asset-liability management capabilities over decades, with U.S. life insurers holding roughly $4.5 trillion in bonds at year-end 2023 to support long-duration liabilities. Matching duration and credit quality helps stabilize spreads and capital requirements. Decades of experience pricing guarantees and managing lapse behavior have improved profitability. This expertise enables disciplined new-business growth in 2024–25.

Niche-market presence

Serving defined customer segments creates defensible positions versus larger rivals by enabling tailored underwriting and product features that differentiate value, often translating into stronger retention and pricing power.

Niche focus typically yields higher agent loyalty and better margins while reducing direct price competition, supporting sustainable profitability and stable distribution relationships.

- Defensible positioning via specialization

- Product/underwriting differentiation

- Higher agent loyalty and margin insulation

Conservative risk culture

Conservative risk culture mirrors traditional life insurer priorities—capital strength and prudence—aligned with the 2024 Solvency II framework; tight underwriting and active reinsurance programs reduce tail-risk exposure, while balance-sheet discipline underpins ratings and distributor confidence, promoting long-term policyholder retention.

- Capital-first orientation

- Tight underwriting & reinsurance

- Balance-sheet discipline

- High policyholder stability

500,000+ agents and $4.5trn insurer bonds underpin low-cost, conservative life/annuity model

NWLGI leverages 500,000+ independent U.S. agents (BLS 2024) for low-fixed-cost distribution, boosting conversion and persistency; life/annuity ALM anchored by ~$4.5trn in bonds across U.S. insurers (YE2023) supports long-duration guarantees. Niche focus yields higher agent loyalty, better margins and a conservative capital posture aligned with 2024 regulatory expectations.

| Metric | Value |

|---|---|

| Agents | 500,000+ |

| Industry bonds | $4.5tn (YE2023) |

| Distribution model | Independent agents, variable cost |

What is included in the product

Provides a concise SWOT analysis of NWLGI, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic decision-making and competitive positioning.

Provides a focused NWLGI SWOT matrix to rapidly surface and address strategic pain points for faster decision-making.

Weaknesses

Interest rate spread sensitivity

Fixed and fixed-indexed annuities depend on net investment spreads; with the 10-year Treasury rising above 4% in 2023–2024 and the Fed funds target at 5.25–5.50%, rapid rate swings can compress margins or force higher credited rates. Reinvestment risk erodes yields on in‑force books, and dynamic hedging raises complexity and measurable hedging costs for insurers.

Dependence on third-party producers

Relying on independent producers limits NWLGI’s direct control of the customer relationship and retention, leaving branding and service quality uneven across channels. Producer turnover, which LIMRA reported above 25% in 2023, can disrupt new-business flows and pipeline stability. Intense commission competition pressures margins and can force higher upfront payouts, while visibility into pipeline and compliance remains uneven across independent networks.

Scale and brand limitations

Smaller national footprint limits NWLGI’s operating leverage versus mega-insurers, increasing per-policy fixed costs and compressing margins. Lower brand awareness raises customer acquisition costs and retention spending relative to household-name competitors. Reduced scale can lead to less favorable vendor and asset-management terms, and constrain speed of product development and platform investment.

Product concentration

Product concentration in traditional and indexed annuities amplifies sensitivity to interest-rate movements and lapse behavior; heavy guarantee-laden blocks can materially increase statutory capital strain and procyclical reserve volatility under stress. Limited exposure to capital-light fee businesses narrows earnings diversity and heightens dependence on spread and credit margins, while concentration raises regulatory-change vulnerability.

- Overweight to traditional/indexed annuities — higher rate & lapse exposure

- Limited fee-based businesses — lower earnings diversification

- Guarantee-heavy blocks — elevated capital and reserve strain

- Concentration — greater sensitivity to regulatory rule changes

Legacy systems and processes

Legacy administration platforms slow product rollout and customization, delaying time-to-market by months and limiting competitive agility; according to Accenture 2024, 76% of insurers cite legacy systems as a top barrier to digital transformation. Manual workflows raise error rates and unit costs, while poor integration with analytics and digital tools hinders data-driven pricing and servicing, weakening agent and policyholder experience.

- Slower launches — customization bottlenecks

- Higher unit costs — manual error exposure

- Poor analytics integration — limited personalization

- Weakened agent/policyholder NPS and retention

Rising rates, legacy tech and producer churn squeeze annuity margins and hike hedging costs

High rate volatility compresses annuity spreads and raises hedging costs as 10Y Treasury moved above 4% in 2023–24. Reliance on independents exposes retention risk; LIMRA reported producer turnover above 25% in 2023. Legacy platforms slow launches and raise costs—Accenture 2024 found 76% of insurers cite legacy systems as a top digital barrier.

| Metric | 2023–24 |

|---|---|

| 10Y Treasury | >4.0% |

| Fed funds target | 5.25–5.50% |

| Producer turnover (LIMRA) | >25% |

| Legacy systems (Accenture) | 76% |

Full Version Awaits

NWLGI SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and buying unlocks the complete, editable version. You’re viewing a live preview of the real file; the full document is available after checkout.