NW Natural Porter's Five Forces Analysis

From Overview to Strategy Blueprint

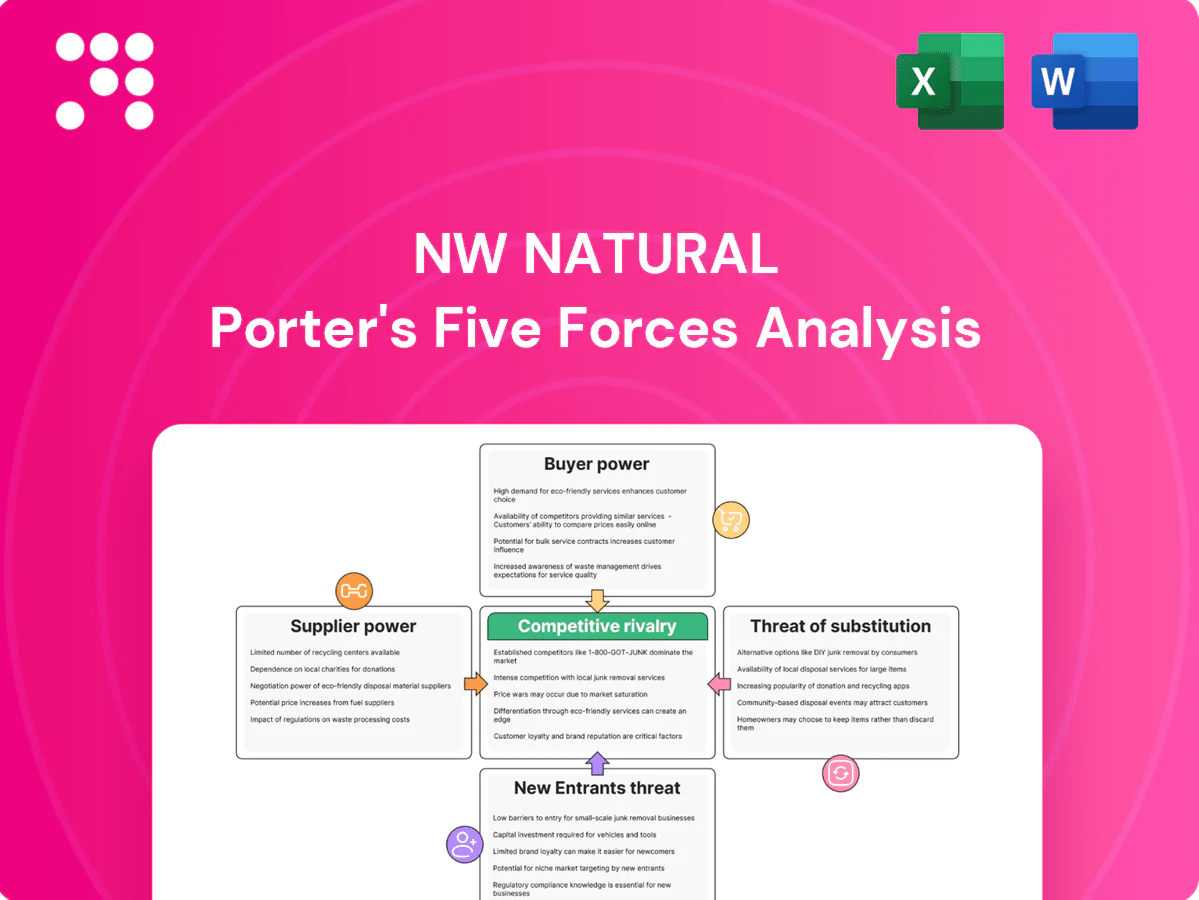

NW Natural faces moderate buyer power, steady supplier leverage, limited threat of new entrants, and growing substitute pressures from electrification—each shaping margins and strategic choices. Regulatory risk and infrastructure costs heighten competitive intensity. This snapshot teases key dynamics. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Interstate pipeline dependence

NW Natural depends on a small set of interstate pipeline operators to feed its distribution network, giving pipeline owners leverage over capacity terms and reservation rates. Long-tenor, take-or-pay contracts (commonly multi-year) lock in commitments and shift volume risk to NW Natural. Seasonal congestion and curtailments—with peak winter flows rising as much as 30–50%—can sharply increase supplier bargaining power.

Upstream gas producers

Gas is a widely produced commodity—US dry gas output was about 101 Bcf/d in 2024—limiting individual upstream bargaining power, though basin-specific sourcing and NW Natural quality specs can narrow supplier choice. Price volatility tied to hubs such as AECO and Rockies (Henry Hub averaged roughly $2.78/MMBtu in 2024) can flow into purchase costs. NW Natural uses hedging and regulatory cost recovery mechanisms to mitigate exposure, but basis risk and pass-through timing leave residual risk.

RNG and decarbonization feedstock

RNG supply remains nascent and concentrated in landfills, dairies and wastewater projects; RNG made up under 1% of U.S. gas supply in 2024. Limited project pipeline and volatile environmental-attribute markets (RINs, LCFS) increase supplier leverage. Long-term offtake contracts with premiums are common, and competing buyers from transport and utilities intensify price and term pressure.

Critical equipment and contractors

Specialized pipes, meters, compressors and AMI systems are concentrated among a few OEMs, reducing substitutability as regulatory specs and multi-month lead times create supplier leverage. Skilled contractors command premium rates in tight markets, and 2023–24 supply disruptions amplified vendor power on delivery timing and price.

- Supplier concentration: few OEMs

- Lead times: multi-months

- Contractor premiums: higher rates in tight markets

Water sector assets and operators

The company’s water platform often sources assets via M&A from municipalities or private owners; scarcity of high-quality systems among roughly 151,000 US public water systems increases seller leverage. Competitive auctions have pushed buyer bids higher, while regulatory approval timelines (permits, local consent) add months of delay, giving sellers timing leverage.

- M&A sourcing: municipal and private owners

- Scarcity: ~151,000 US public water systems

- Auctions: upward pressure on bids/multiples

- Regulatory timelines: seller timing leverage

Interstate pipeline capacity and take-or-pay terms concentrate leverage on regional gas utilities

NW Natural relies on a few interstate pipelines, giving pipeline owners leverage via capacity and take-or-pay terms. Commodity liquidity caps upstream power (US dry gas ~101 Bcf/d in 2024; Henry Hub ~$2.78/MMBtu) but basis and seasonal congestion raise supplier risk. RNG is nascent (<1% of US gas in 2024) and OEMs/contractors remain concentrated, boosting vendor leverage.

| Metric | 2024 |

|---|---|

| US dry gas output | ~101 Bcf/d |

| Henry Hub | ~$2.78/MMBtu |

| RNG share | <1% |

| Public water systems | ~151,000 |

What is included in the product

Tailored Porter's Five Forces analysis for NW Natural that examines supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and regulatory barriers to identify key pressures on pricing, margins, and strategic positioning.

A concise one-sheet Porter's Five Forces for NW Natural—clely rates supplier power, buyer leverage, substitutes, new entrants, and industry rivalry for rapid strategic decisions, customizable for regulatory or market scenarios and ready to drop into decks or reports.

Customers Bargaining Power

Regulated captive customers

Regulated captive customers, roughly 725,000 retail accounts in 2024, have limited switching power inside NW Natural franchise areas, which dampens direct buyer leverage. Regulators weigh affordability—Oregon and Washington rate decisions in 2024 emphasized low-income protections and constrained allowed returns, limiting price flexibility. Demand elasticity stays low but is rising as heat pump installations grew in 2024, nudging long-term gas demand down.

Large C&I customers

Large industrial and C&I users—the industrial sector consumed 31% of US natural gas in 2023 (EIA)—can fuel-switch to electricity, propane, or fuel oil for many processes, giving them leverage. Their high-volume concentration strengthens negotiation power over rates and service terms. Utilities like NW Natural deploy interruptible tariffs and discounts to retain them. Economic downturns increase their propensity to switch fuels or suppliers.

Regulators as proxy buyers

OPUC and WUTC act as proxy buyers for NW Natural, steering allowable rates and service standards through rate cases that dictate revenue recovery. Prudence reviews and cost-of-service frameworks limit the company’s ability to expand margins by scrutinizing capital and expense allocation. Performance metrics and decarbonization mandates now determine which costs are recoverable, tying financial outcomes to regulatory compliance. This institutional oversight concentrates buyer power well above that of individual customers.

Community and municipal stakeholders

Local governments control franchise renewals, permitting and climate rules, and by 2024 major cities such as Berkeley, San Francisco and Seattle had enacted limits on new gas hookups, shifting bargaining power toward municipalities. Electrification building codes and public safety/emissions concerns push for tougher service terms; stakeholder engagement can reduce but not remove regulatory risk.

- Regulatory leverage: municipal franchise & permitting

- Market shift: electrification codes reduce gas demand

- Mitigation: engagement lowers, not eliminates, downside

Water utility customers

Water utility customers are captive and highly sensitive to rate affordability and reliability; as of 2024 US public water systems serve about 286 million people, which raises political scrutiny of rate hikes. State regulators closely vet acquisition premiums and investment plans, while consolidated billing and visible service quality shape perceived value. Drought and water-quality events increase oversight on pricing and capital approvals.

- Customer captivity vs affordability pressure

- Regulatory scrutiny on acquisitions/investments

- Consolidated billing influences perceived value

- Drought/quality events heighten pricing oversight

Regulated captive base and OR/WA limits curb buyer leverage as electrification raises elasticity

Regulated captive base (~725,000 retail accounts in 2024) limits switching, reducing direct buyer leverage; regulators in OR/WA constrained allowed returns in 2024. Large C&I users (industrial = 31% US gas use, 2023) hold negotiating power via fuel-switch options. Electrification and rising heat pump adoption in 2024 gradually increase elasticity.

| Metric | Value |

|---|---|

| Retail accounts (2024) | ~725,000 |

| Industrial gas share (2023) | 31% |

| US water served (2024) | ~286M people |

Preview the Actual Deliverable

NW Natural Porter's Five Forces Analysis

This NW Natural Porter’s Five Forces analysis delivers a professional assessment of competitive dynamics, supplier and buyer power, threat of substitutes, and industry rivalry. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or mockups. Downloadable and ready to use for decision-making and reporting.

From Overview to Strategy Blueprint

NW Natural faces moderate buyer power, steady supplier leverage, limited threat of new entrants, and growing substitute pressures from electrification—each shaping margins and strategic choices. Regulatory risk and infrastructure costs heighten competitive intensity. This snapshot teases key dynamics. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Interstate pipeline dependence

NW Natural depends on a small set of interstate pipeline operators to feed its distribution network, giving pipeline owners leverage over capacity terms and reservation rates. Long-tenor, take-or-pay contracts (commonly multi-year) lock in commitments and shift volume risk to NW Natural. Seasonal congestion and curtailments—with peak winter flows rising as much as 30–50%—can sharply increase supplier bargaining power.

Upstream gas producers

Gas is a widely produced commodity—US dry gas output was about 101 Bcf/d in 2024—limiting individual upstream bargaining power, though basin-specific sourcing and NW Natural quality specs can narrow supplier choice. Price volatility tied to hubs such as AECO and Rockies (Henry Hub averaged roughly $2.78/MMBtu in 2024) can flow into purchase costs. NW Natural uses hedging and regulatory cost recovery mechanisms to mitigate exposure, but basis risk and pass-through timing leave residual risk.

RNG and decarbonization feedstock

RNG supply remains nascent and concentrated in landfills, dairies and wastewater projects; RNG made up under 1% of U.S. gas supply in 2024. Limited project pipeline and volatile environmental-attribute markets (RINs, LCFS) increase supplier leverage. Long-term offtake contracts with premiums are common, and competing buyers from transport and utilities intensify price and term pressure.

Critical equipment and contractors

Specialized pipes, meters, compressors and AMI systems are concentrated among a few OEMs, reducing substitutability as regulatory specs and multi-month lead times create supplier leverage. Skilled contractors command premium rates in tight markets, and 2023–24 supply disruptions amplified vendor power on delivery timing and price.

- Supplier concentration: few OEMs

- Lead times: multi-months

- Contractor premiums: higher rates in tight markets

Water sector assets and operators

The company’s water platform often sources assets via M&A from municipalities or private owners; scarcity of high-quality systems among roughly 151,000 US public water systems increases seller leverage. Competitive auctions have pushed buyer bids higher, while regulatory approval timelines (permits, local consent) add months of delay, giving sellers timing leverage.

- M&A sourcing: municipal and private owners

- Scarcity: ~151,000 US public water systems

- Auctions: upward pressure on bids/multiples

- Regulatory timelines: seller timing leverage

Interstate pipeline capacity and take-or-pay terms concentrate leverage on regional gas utilities

NW Natural relies on a few interstate pipelines, giving pipeline owners leverage via capacity and take-or-pay terms. Commodity liquidity caps upstream power (US dry gas ~101 Bcf/d in 2024; Henry Hub ~$2.78/MMBtu) but basis and seasonal congestion raise supplier risk. RNG is nascent (<1% of US gas in 2024) and OEMs/contractors remain concentrated, boosting vendor leverage.

| Metric | 2024 |

|---|---|

| US dry gas output | ~101 Bcf/d |

| Henry Hub | ~$2.78/MMBtu |

| RNG share | <1% |

| Public water systems | ~151,000 |

What is included in the product

Tailored Porter's Five Forces analysis for NW Natural that examines supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and regulatory barriers to identify key pressures on pricing, margins, and strategic positioning.

A concise one-sheet Porter's Five Forces for NW Natural—clely rates supplier power, buyer leverage, substitutes, new entrants, and industry rivalry for rapid strategic decisions, customizable for regulatory or market scenarios and ready to drop into decks or reports.

Customers Bargaining Power

Regulated captive customers

Regulated captive customers, roughly 725,000 retail accounts in 2024, have limited switching power inside NW Natural franchise areas, which dampens direct buyer leverage. Regulators weigh affordability—Oregon and Washington rate decisions in 2024 emphasized low-income protections and constrained allowed returns, limiting price flexibility. Demand elasticity stays low but is rising as heat pump installations grew in 2024, nudging long-term gas demand down.

Large C&I customers

Large industrial and C&I users—the industrial sector consumed 31% of US natural gas in 2023 (EIA)—can fuel-switch to electricity, propane, or fuel oil for many processes, giving them leverage. Their high-volume concentration strengthens negotiation power over rates and service terms. Utilities like NW Natural deploy interruptible tariffs and discounts to retain them. Economic downturns increase their propensity to switch fuels or suppliers.

Regulators as proxy buyers

OPUC and WUTC act as proxy buyers for NW Natural, steering allowable rates and service standards through rate cases that dictate revenue recovery. Prudence reviews and cost-of-service frameworks limit the company’s ability to expand margins by scrutinizing capital and expense allocation. Performance metrics and decarbonization mandates now determine which costs are recoverable, tying financial outcomes to regulatory compliance. This institutional oversight concentrates buyer power well above that of individual customers.

Community and municipal stakeholders

Local governments control franchise renewals, permitting and climate rules, and by 2024 major cities such as Berkeley, San Francisco and Seattle had enacted limits on new gas hookups, shifting bargaining power toward municipalities. Electrification building codes and public safety/emissions concerns push for tougher service terms; stakeholder engagement can reduce but not remove regulatory risk.

- Regulatory leverage: municipal franchise & permitting

- Market shift: electrification codes reduce gas demand

- Mitigation: engagement lowers, not eliminates, downside

Water utility customers

Water utility customers are captive and highly sensitive to rate affordability and reliability; as of 2024 US public water systems serve about 286 million people, which raises political scrutiny of rate hikes. State regulators closely vet acquisition premiums and investment plans, while consolidated billing and visible service quality shape perceived value. Drought and water-quality events increase oversight on pricing and capital approvals.

- Customer captivity vs affordability pressure

- Regulatory scrutiny on acquisitions/investments

- Consolidated billing influences perceived value

- Drought/quality events heighten pricing oversight

Regulated captive base and OR/WA limits curb buyer leverage as electrification raises elasticity

Regulated captive base (~725,000 retail accounts in 2024) limits switching, reducing direct buyer leverage; regulators in OR/WA constrained allowed returns in 2024. Large C&I users (industrial = 31% US gas use, 2023) hold negotiating power via fuel-switch options. Electrification and rising heat pump adoption in 2024 gradually increase elasticity.

| Metric | Value |

|---|---|

| Retail accounts (2024) | ~725,000 |

| Industrial gas share (2023) | 31% |

| US water served (2024) | ~286M people |

Preview the Actual Deliverable

NW Natural Porter's Five Forces Analysis

This NW Natural Porter’s Five Forces analysis delivers a professional assessment of competitive dynamics, supplier and buyer power, threat of substitutes, and industry rivalry. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or mockups. Downloadable and ready to use for decision-making and reporting.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

NW Natural faces moderate buyer power, steady supplier leverage, limited threat of new entrants, and growing substitute pressures from electrification—each shaping margins and strategic choices. Regulatory risk and infrastructure costs heighten competitive intensity. This snapshot teases key dynamics. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Interstate pipeline dependence

NW Natural depends on a small set of interstate pipeline operators to feed its distribution network, giving pipeline owners leverage over capacity terms and reservation rates. Long-tenor, take-or-pay contracts (commonly multi-year) lock in commitments and shift volume risk to NW Natural. Seasonal congestion and curtailments—with peak winter flows rising as much as 30–50%—can sharply increase supplier bargaining power.

Upstream gas producers

Gas is a widely produced commodity—US dry gas output was about 101 Bcf/d in 2024—limiting individual upstream bargaining power, though basin-specific sourcing and NW Natural quality specs can narrow supplier choice. Price volatility tied to hubs such as AECO and Rockies (Henry Hub averaged roughly $2.78/MMBtu in 2024) can flow into purchase costs. NW Natural uses hedging and regulatory cost recovery mechanisms to mitigate exposure, but basis risk and pass-through timing leave residual risk.

RNG and decarbonization feedstock

RNG supply remains nascent and concentrated in landfills, dairies and wastewater projects; RNG made up under 1% of U.S. gas supply in 2024. Limited project pipeline and volatile environmental-attribute markets (RINs, LCFS) increase supplier leverage. Long-term offtake contracts with premiums are common, and competing buyers from transport and utilities intensify price and term pressure.

Critical equipment and contractors

Specialized pipes, meters, compressors and AMI systems are concentrated among a few OEMs, reducing substitutability as regulatory specs and multi-month lead times create supplier leverage. Skilled contractors command premium rates in tight markets, and 2023–24 supply disruptions amplified vendor power on delivery timing and price.

- Supplier concentration: few OEMs

- Lead times: multi-months

- Contractor premiums: higher rates in tight markets

Water sector assets and operators

The company’s water platform often sources assets via M&A from municipalities or private owners; scarcity of high-quality systems among roughly 151,000 US public water systems increases seller leverage. Competitive auctions have pushed buyer bids higher, while regulatory approval timelines (permits, local consent) add months of delay, giving sellers timing leverage.

- M&A sourcing: municipal and private owners

- Scarcity: ~151,000 US public water systems

- Auctions: upward pressure on bids/multiples

- Regulatory timelines: seller timing leverage

Interstate pipeline capacity and take-or-pay terms concentrate leverage on regional gas utilities

NW Natural relies on a few interstate pipelines, giving pipeline owners leverage via capacity and take-or-pay terms. Commodity liquidity caps upstream power (US dry gas ~101 Bcf/d in 2024; Henry Hub ~$2.78/MMBtu) but basis and seasonal congestion raise supplier risk. RNG is nascent (<1% of US gas in 2024) and OEMs/contractors remain concentrated, boosting vendor leverage.

| Metric | 2024 |

|---|---|

| US dry gas output | ~101 Bcf/d |

| Henry Hub | ~$2.78/MMBtu |

| RNG share | <1% |

| Public water systems | ~151,000 |

What is included in the product

Tailored Porter's Five Forces analysis for NW Natural that examines supplier and buyer power, competitive rivalry, threat of new entrants and substitutes, and regulatory barriers to identify key pressures on pricing, margins, and strategic positioning.

A concise one-sheet Porter's Five Forces for NW Natural—clely rates supplier power, buyer leverage, substitutes, new entrants, and industry rivalry for rapid strategic decisions, customizable for regulatory or market scenarios and ready to drop into decks or reports.

Customers Bargaining Power

Regulated captive customers

Regulated captive customers, roughly 725,000 retail accounts in 2024, have limited switching power inside NW Natural franchise areas, which dampens direct buyer leverage. Regulators weigh affordability—Oregon and Washington rate decisions in 2024 emphasized low-income protections and constrained allowed returns, limiting price flexibility. Demand elasticity stays low but is rising as heat pump installations grew in 2024, nudging long-term gas demand down.

Large C&I customers

Large industrial and C&I users—the industrial sector consumed 31% of US natural gas in 2023 (EIA)—can fuel-switch to electricity, propane, or fuel oil for many processes, giving them leverage. Their high-volume concentration strengthens negotiation power over rates and service terms. Utilities like NW Natural deploy interruptible tariffs and discounts to retain them. Economic downturns increase their propensity to switch fuels or suppliers.

Regulators as proxy buyers

OPUC and WUTC act as proxy buyers for NW Natural, steering allowable rates and service standards through rate cases that dictate revenue recovery. Prudence reviews and cost-of-service frameworks limit the company’s ability to expand margins by scrutinizing capital and expense allocation. Performance metrics and decarbonization mandates now determine which costs are recoverable, tying financial outcomes to regulatory compliance. This institutional oversight concentrates buyer power well above that of individual customers.

Community and municipal stakeholders

Local governments control franchise renewals, permitting and climate rules, and by 2024 major cities such as Berkeley, San Francisco and Seattle had enacted limits on new gas hookups, shifting bargaining power toward municipalities. Electrification building codes and public safety/emissions concerns push for tougher service terms; stakeholder engagement can reduce but not remove regulatory risk.

- Regulatory leverage: municipal franchise & permitting

- Market shift: electrification codes reduce gas demand

- Mitigation: engagement lowers, not eliminates, downside

Water utility customers

Water utility customers are captive and highly sensitive to rate affordability and reliability; as of 2024 US public water systems serve about 286 million people, which raises political scrutiny of rate hikes. State regulators closely vet acquisition premiums and investment plans, while consolidated billing and visible service quality shape perceived value. Drought and water-quality events increase oversight on pricing and capital approvals.

- Customer captivity vs affordability pressure

- Regulatory scrutiny on acquisitions/investments

- Consolidated billing influences perceived value

- Drought/quality events heighten pricing oversight

Regulated captive base and OR/WA limits curb buyer leverage as electrification raises elasticity

Regulated captive base (~725,000 retail accounts in 2024) limits switching, reducing direct buyer leverage; regulators in OR/WA constrained allowed returns in 2024. Large C&I users (industrial = 31% US gas use, 2023) hold negotiating power via fuel-switch options. Electrification and rising heat pump adoption in 2024 gradually increase elasticity.

| Metric | Value |

|---|---|

| Retail accounts (2024) | ~725,000 |

| Industrial gas share (2023) | 31% |

| US water served (2024) | ~286M people |

Preview the Actual Deliverable

NW Natural Porter's Five Forces Analysis

This NW Natural Porter’s Five Forces analysis delivers a professional assessment of competitive dynamics, supplier and buyer power, threat of substitutes, and industry rivalry. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders or mockups. Downloadable and ready to use for decision-making and reporting.