NW Natural SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

NW Natural’s stable utility footprint and regulated revenue offer resilient cash flows, but rising gas transition pressures and regulatory shifts pose notable risks; our snapshot highlights key competitive and operational signals. Want the full story—strengths, weaknesses, opportunities, and threats—mapped to financial context and strategy? Purchase the complete SWOT analysis for a professionally formatted Word report and editable Excel model to plan, pitch, or invest with confidence.

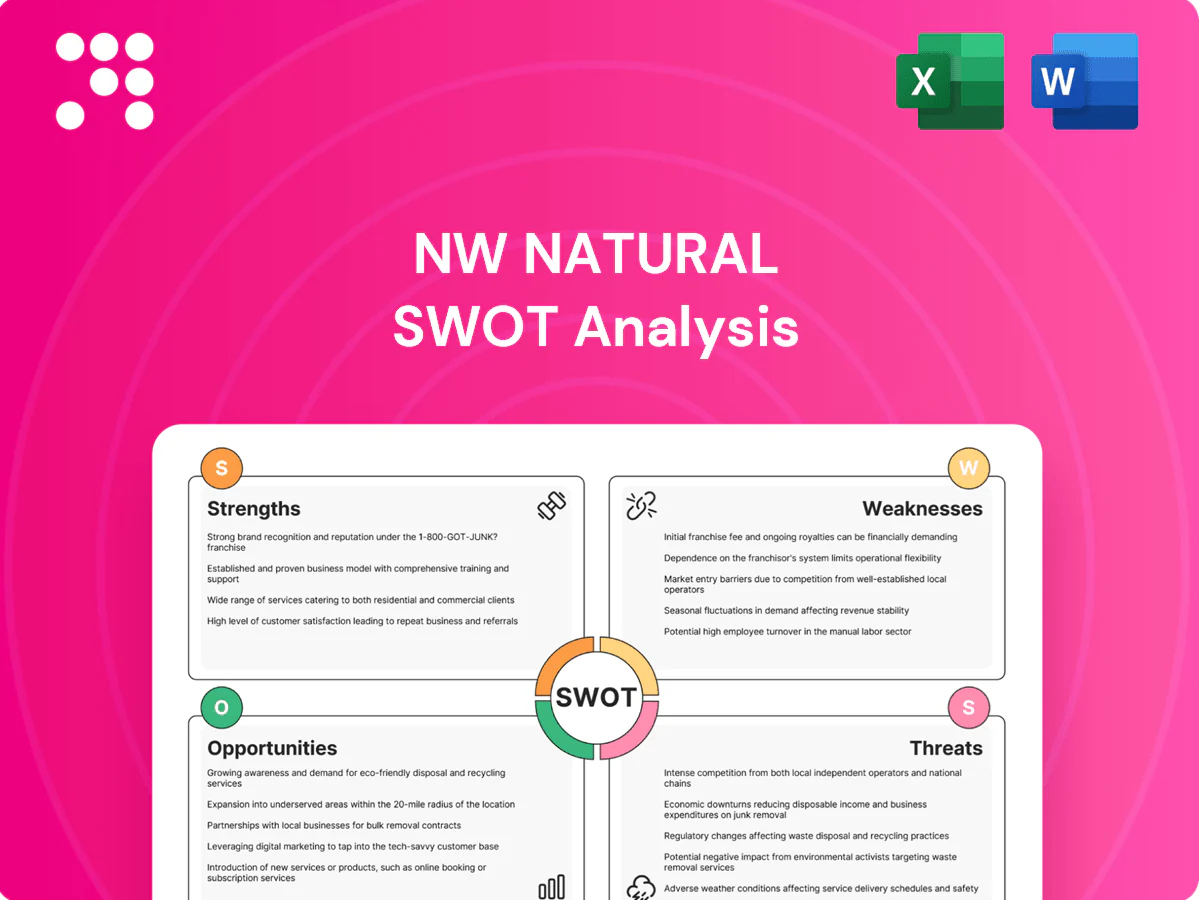

Strengths

Stable regulated cash flows

NW Natural operates as a primarily regulated utility serving roughly 760,000 customers, with state-authorized cost recovery and returns that stabilize earnings across cycles. Predictable rate mechanisms and decoupling reduce volume risk from weather and efficiency, supporting consistent cash flow. This regulatory stability underpins strong access to capital for its multiyear infrastructure plan of about $1B per year and aligns long-term planning with public policy.

Diverse customer mix

Serving roughly 760,000 residential, commercial and industrial customers across Oregon and southwest Washington spreads demand and credit risk and smooths consumption and revenue variability. Load diversity dampens seasonal swings and supports multiple program channels — from energy-efficiency offerings to RNG pilots disclosed in recent filings. The breadth of the customer base sustains resilient utilization of NW Natural’s distribution network.

RNG and decarbonization capabilities

Active investment in renewable natural gas positions NW Natural to supply low-carbon fuel blends and access compliance markets like California and Oregon LCFS; RNG can cut lifecycle GHGs by up to 90% versus fossil gas. Experience with interconnections and supply contracting creates first-mover advantages in sourcing and delivering RNG. Decarbonization offerings help maintain pipeline relevance as emissions rules tighten, strengthening stakeholder alignment and long-term license to operate.

Adjacency in water and wastewater

NW Natural Water extends the utility platform into regulated water and wastewater services, leveraging similar rate-setting frameworks and customer protections to accelerate utility-style returns.

Strategic water M&A creates a runway for rate-base growth and geographic diversification while reducing exposure to single-fuel demand cycles.

Shared customer service, billing and regulatory processes drive operational efficiencies and lower incremental costs per account.

- Adjacency: regulated water/wastewater services

- Growth: water M&A supports rate-base expansion

- Efficiency: billing and customer-service overlap

- Risk mitigation: reduces single-fuel exposure

Strong regional brand and safety culture

NW Natural’s over 160-year presence in Oregon and Southwest Washington fosters strong trust with regulators and communities, aiding constructive rate cases and permitting; its safety-first culture has contributed to consistently low incident rates and fewer regulatory penalties, supporting operational reliability and customer confidence.

- Regional trust: entrenched presence >160 years

- Safety: low incident profile, reduced penalties

- Community engagement: aids rate outcomes

- Permitting: reputation speeds approvals

Regulated utility with ~760,000 customers and ~$1B/yr capex

NW Natural serves ~760,000 customers in Oregon and SW Washington with regulated rate mechanisms and decoupling, enabling stable earnings and multiyear capex of ~$1B/year. Its RNG initiatives can cut lifecycle GHGs up to 90% and support LCFS/compliance revenue. NW Natural Water diversifies rate base, while a >160-year regional presence aids permitting and regulatory trust.

| Metric | Value |

|---|---|

| Customers | ~760,000 |

| Annual capex | ~$1B/yr |

| RNG GHG reduction | up to 90% |

| Operating region | Oregon, SW Washington |

| Years in region | >160 |

What is included in the product

Delivers a strategic overview of NW Natural’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix for NW Natural to quickly surface regulatory, infrastructure and market risks, enabling fast alignment of mitigation strategies and investment priorities.

Weaknesses

Geographic concentration

Operations are concentrated in Oregon and southwest Washington, exposing NW Natural to localized policy shifts and seismic risk from the Cascadia Subduction Zone. The utility serves roughly 750,000 customers, limiting scale economies versus national peers. A regional economic slowdown would disproportionately hit demand and growth. Local regulatory decisions (state PUC rate cases) can drive outsized earnings volatility.

Dependence on fossil gas demand

NW Natural's core revenues remain tied to natural gas throughput while electrification accelerates; the utility serves roughly 700,000–750,000 customers. Declining per-customer usage driven by efficiency and heat-pump adoption has eroded volumetric growth. State building-decarbonization policies in Oregon and Washington heighten downside to long-term demand. Rapid transition risks outpacing cost recovery on legacy gas infrastructure.

Aging infrastructure capital needs

Aging infrastructure modernization, leak reduction and resilience upgrades force sustained capex—NW Natural projects roughly $300 million of system investment in 2024. Regulatory lag between spending and rate recovery can pressure cash flow during multi-year build cycles. Execution risks include supply-chain, labor and permitting delays, and a higher rate base may raise customer bills and affordability concerns in Oregon and Washington.

Smaller scale versus peers

Compared with larger multi-state utilities, NW Natural serves approximately 720,000 customers and has lower purchasing power and geographic diversification, which raises per-customer O&M costs and limits overhead absorption; limited scale also constrains access to lower-cost capital during market volatility and reduces optionality for large-scale technology deployment.

- ~720,000 customers

- Smaller purchasing power

- Higher per-customer O&M

- Constrained low-cost capital access

- Limited tech deployment optionality

RNG supply and cost constraints

RNG feedstock availability is constrained and often commands premium prices, limiting scale-up for NW Natural; the company serves about 760,000 customers (2024), so procurement must be robust to meet demand. Long-term RNG contracts can expose NW Natural to price and counterparty credit risk, while interconnection and upgrading to pipeline quality can add multi-million-dollar costs per project. Regulators may scrutinize cost pass-through if customer bills rise materially.

- Feedstock scarcity and premium pricing

- Contract price and credit exposure

- High interconnection/upgrading capex

- Regulatory risk on bill pass-through

Pacific NW gas utility: ~760k customers, $300M capex strains cash flow

Operations concentrated in Oregon/southwest Washington increase seismic and policy exposure; NW Natural serves ~760,000 customers (2024) with limited geographic scale. Declining gas volumes, electrification and RNG feedstock scarcity pressure revenue and raise transition/cost-recovery risk. 2024 system investment needs and regulatory lag can compress cash flow during multi-year capex cycles.

| Metric | 2024 |

|---|---|

| Customers | ~760,000 |

| System investment | $300 million |

| RNG availability | Constrained/premium |

Same Document Delivered

NW Natural SWOT Analysis

This is the actual NW Natural SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure, findings, and recommendations. Purchase unlocks the editable, full version for immediate download.

Elevate Your Analysis with the Complete SWOT Report

NW Natural’s stable utility footprint and regulated revenue offer resilient cash flows, but rising gas transition pressures and regulatory shifts pose notable risks; our snapshot highlights key competitive and operational signals. Want the full story—strengths, weaknesses, opportunities, and threats—mapped to financial context and strategy? Purchase the complete SWOT analysis for a professionally formatted Word report and editable Excel model to plan, pitch, or invest with confidence.

Strengths

Stable regulated cash flows

NW Natural operates as a primarily regulated utility serving roughly 760,000 customers, with state-authorized cost recovery and returns that stabilize earnings across cycles. Predictable rate mechanisms and decoupling reduce volume risk from weather and efficiency, supporting consistent cash flow. This regulatory stability underpins strong access to capital for its multiyear infrastructure plan of about $1B per year and aligns long-term planning with public policy.

Diverse customer mix

Serving roughly 760,000 residential, commercial and industrial customers across Oregon and southwest Washington spreads demand and credit risk and smooths consumption and revenue variability. Load diversity dampens seasonal swings and supports multiple program channels — from energy-efficiency offerings to RNG pilots disclosed in recent filings. The breadth of the customer base sustains resilient utilization of NW Natural’s distribution network.

RNG and decarbonization capabilities

Active investment in renewable natural gas positions NW Natural to supply low-carbon fuel blends and access compliance markets like California and Oregon LCFS; RNG can cut lifecycle GHGs by up to 90% versus fossil gas. Experience with interconnections and supply contracting creates first-mover advantages in sourcing and delivering RNG. Decarbonization offerings help maintain pipeline relevance as emissions rules tighten, strengthening stakeholder alignment and long-term license to operate.

Adjacency in water and wastewater

NW Natural Water extends the utility platform into regulated water and wastewater services, leveraging similar rate-setting frameworks and customer protections to accelerate utility-style returns.

Strategic water M&A creates a runway for rate-base growth and geographic diversification while reducing exposure to single-fuel demand cycles.

Shared customer service, billing and regulatory processes drive operational efficiencies and lower incremental costs per account.

- Adjacency: regulated water/wastewater services

- Growth: water M&A supports rate-base expansion

- Efficiency: billing and customer-service overlap

- Risk mitigation: reduces single-fuel exposure

Strong regional brand and safety culture

NW Natural’s over 160-year presence in Oregon and Southwest Washington fosters strong trust with regulators and communities, aiding constructive rate cases and permitting; its safety-first culture has contributed to consistently low incident rates and fewer regulatory penalties, supporting operational reliability and customer confidence.

- Regional trust: entrenched presence >160 years

- Safety: low incident profile, reduced penalties

- Community engagement: aids rate outcomes

- Permitting: reputation speeds approvals

Regulated utility with ~760,000 customers and ~$1B/yr capex

NW Natural serves ~760,000 customers in Oregon and SW Washington with regulated rate mechanisms and decoupling, enabling stable earnings and multiyear capex of ~$1B/year. Its RNG initiatives can cut lifecycle GHGs up to 90% and support LCFS/compliance revenue. NW Natural Water diversifies rate base, while a >160-year regional presence aids permitting and regulatory trust.

| Metric | Value |

|---|---|

| Customers | ~760,000 |

| Annual capex | ~$1B/yr |

| RNG GHG reduction | up to 90% |

| Operating region | Oregon, SW Washington |

| Years in region | >160 |

What is included in the product

Delivers a strategic overview of NW Natural’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix for NW Natural to quickly surface regulatory, infrastructure and market risks, enabling fast alignment of mitigation strategies and investment priorities.

Weaknesses

Geographic concentration

Operations are concentrated in Oregon and southwest Washington, exposing NW Natural to localized policy shifts and seismic risk from the Cascadia Subduction Zone. The utility serves roughly 750,000 customers, limiting scale economies versus national peers. A regional economic slowdown would disproportionately hit demand and growth. Local regulatory decisions (state PUC rate cases) can drive outsized earnings volatility.

Dependence on fossil gas demand

NW Natural's core revenues remain tied to natural gas throughput while electrification accelerates; the utility serves roughly 700,000–750,000 customers. Declining per-customer usage driven by efficiency and heat-pump adoption has eroded volumetric growth. State building-decarbonization policies in Oregon and Washington heighten downside to long-term demand. Rapid transition risks outpacing cost recovery on legacy gas infrastructure.

Aging infrastructure capital needs

Aging infrastructure modernization, leak reduction and resilience upgrades force sustained capex—NW Natural projects roughly $300 million of system investment in 2024. Regulatory lag between spending and rate recovery can pressure cash flow during multi-year build cycles. Execution risks include supply-chain, labor and permitting delays, and a higher rate base may raise customer bills and affordability concerns in Oregon and Washington.

Smaller scale versus peers

Compared with larger multi-state utilities, NW Natural serves approximately 720,000 customers and has lower purchasing power and geographic diversification, which raises per-customer O&M costs and limits overhead absorption; limited scale also constrains access to lower-cost capital during market volatility and reduces optionality for large-scale technology deployment.

- ~720,000 customers

- Smaller purchasing power

- Higher per-customer O&M

- Constrained low-cost capital access

- Limited tech deployment optionality

RNG supply and cost constraints

RNG feedstock availability is constrained and often commands premium prices, limiting scale-up for NW Natural; the company serves about 760,000 customers (2024), so procurement must be robust to meet demand. Long-term RNG contracts can expose NW Natural to price and counterparty credit risk, while interconnection and upgrading to pipeline quality can add multi-million-dollar costs per project. Regulators may scrutinize cost pass-through if customer bills rise materially.

- Feedstock scarcity and premium pricing

- Contract price and credit exposure

- High interconnection/upgrading capex

- Regulatory risk on bill pass-through

Pacific NW gas utility: ~760k customers, $300M capex strains cash flow

Operations concentrated in Oregon/southwest Washington increase seismic and policy exposure; NW Natural serves ~760,000 customers (2024) with limited geographic scale. Declining gas volumes, electrification and RNG feedstock scarcity pressure revenue and raise transition/cost-recovery risk. 2024 system investment needs and regulatory lag can compress cash flow during multi-year capex cycles.

| Metric | 2024 |

|---|---|

| Customers | ~760,000 |

| System investment | $300 million |

| RNG availability | Constrained/premium |

Same Document Delivered

NW Natural SWOT Analysis

This is the actual NW Natural SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure, findings, and recommendations. Purchase unlocks the editable, full version for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

NW Natural’s stable utility footprint and regulated revenue offer resilient cash flows, but rising gas transition pressures and regulatory shifts pose notable risks; our snapshot highlights key competitive and operational signals. Want the full story—strengths, weaknesses, opportunities, and threats—mapped to financial context and strategy? Purchase the complete SWOT analysis for a professionally formatted Word report and editable Excel model to plan, pitch, or invest with confidence.

Strengths

Stable regulated cash flows

NW Natural operates as a primarily regulated utility serving roughly 760,000 customers, with state-authorized cost recovery and returns that stabilize earnings across cycles. Predictable rate mechanisms and decoupling reduce volume risk from weather and efficiency, supporting consistent cash flow. This regulatory stability underpins strong access to capital for its multiyear infrastructure plan of about $1B per year and aligns long-term planning with public policy.

Diverse customer mix

Serving roughly 760,000 residential, commercial and industrial customers across Oregon and southwest Washington spreads demand and credit risk and smooths consumption and revenue variability. Load diversity dampens seasonal swings and supports multiple program channels — from energy-efficiency offerings to RNG pilots disclosed in recent filings. The breadth of the customer base sustains resilient utilization of NW Natural’s distribution network.

RNG and decarbonization capabilities

Active investment in renewable natural gas positions NW Natural to supply low-carbon fuel blends and access compliance markets like California and Oregon LCFS; RNG can cut lifecycle GHGs by up to 90% versus fossil gas. Experience with interconnections and supply contracting creates first-mover advantages in sourcing and delivering RNG. Decarbonization offerings help maintain pipeline relevance as emissions rules tighten, strengthening stakeholder alignment and long-term license to operate.

Adjacency in water and wastewater

NW Natural Water extends the utility platform into regulated water and wastewater services, leveraging similar rate-setting frameworks and customer protections to accelerate utility-style returns.

Strategic water M&A creates a runway for rate-base growth and geographic diversification while reducing exposure to single-fuel demand cycles.

Shared customer service, billing and regulatory processes drive operational efficiencies and lower incremental costs per account.

- Adjacency: regulated water/wastewater services

- Growth: water M&A supports rate-base expansion

- Efficiency: billing and customer-service overlap

- Risk mitigation: reduces single-fuel exposure

Strong regional brand and safety culture

NW Natural’s over 160-year presence in Oregon and Southwest Washington fosters strong trust with regulators and communities, aiding constructive rate cases and permitting; its safety-first culture has contributed to consistently low incident rates and fewer regulatory penalties, supporting operational reliability and customer confidence.

- Regional trust: entrenched presence >160 years

- Safety: low incident profile, reduced penalties

- Community engagement: aids rate outcomes

- Permitting: reputation speeds approvals

Regulated utility with ~760,000 customers and ~$1B/yr capex

NW Natural serves ~760,000 customers in Oregon and SW Washington with regulated rate mechanisms and decoupling, enabling stable earnings and multiyear capex of ~$1B/year. Its RNG initiatives can cut lifecycle GHGs up to 90% and support LCFS/compliance revenue. NW Natural Water diversifies rate base, while a >160-year regional presence aids permitting and regulatory trust.

| Metric | Value |

|---|---|

| Customers | ~760,000 |

| Annual capex | ~$1B/yr |

| RNG GHG reduction | up to 90% |

| Operating region | Oregon, SW Washington |

| Years in region | >160 |

What is included in the product

Delivers a strategic overview of NW Natural’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix for NW Natural to quickly surface regulatory, infrastructure and market risks, enabling fast alignment of mitigation strategies and investment priorities.

Weaknesses

Geographic concentration

Operations are concentrated in Oregon and southwest Washington, exposing NW Natural to localized policy shifts and seismic risk from the Cascadia Subduction Zone. The utility serves roughly 750,000 customers, limiting scale economies versus national peers. A regional economic slowdown would disproportionately hit demand and growth. Local regulatory decisions (state PUC rate cases) can drive outsized earnings volatility.

Dependence on fossil gas demand

NW Natural's core revenues remain tied to natural gas throughput while electrification accelerates; the utility serves roughly 700,000–750,000 customers. Declining per-customer usage driven by efficiency and heat-pump adoption has eroded volumetric growth. State building-decarbonization policies in Oregon and Washington heighten downside to long-term demand. Rapid transition risks outpacing cost recovery on legacy gas infrastructure.

Aging infrastructure capital needs

Aging infrastructure modernization, leak reduction and resilience upgrades force sustained capex—NW Natural projects roughly $300 million of system investment in 2024. Regulatory lag between spending and rate recovery can pressure cash flow during multi-year build cycles. Execution risks include supply-chain, labor and permitting delays, and a higher rate base may raise customer bills and affordability concerns in Oregon and Washington.

Smaller scale versus peers

Compared with larger multi-state utilities, NW Natural serves approximately 720,000 customers and has lower purchasing power and geographic diversification, which raises per-customer O&M costs and limits overhead absorption; limited scale also constrains access to lower-cost capital during market volatility and reduces optionality for large-scale technology deployment.

- ~720,000 customers

- Smaller purchasing power

- Higher per-customer O&M

- Constrained low-cost capital access

- Limited tech deployment optionality

RNG supply and cost constraints

RNG feedstock availability is constrained and often commands premium prices, limiting scale-up for NW Natural; the company serves about 760,000 customers (2024), so procurement must be robust to meet demand. Long-term RNG contracts can expose NW Natural to price and counterparty credit risk, while interconnection and upgrading to pipeline quality can add multi-million-dollar costs per project. Regulators may scrutinize cost pass-through if customer bills rise materially.

- Feedstock scarcity and premium pricing

- Contract price and credit exposure

- High interconnection/upgrading capex

- Regulatory risk on bill pass-through

Pacific NW gas utility: ~760k customers, $300M capex strains cash flow

Operations concentrated in Oregon/southwest Washington increase seismic and policy exposure; NW Natural serves ~760,000 customers (2024) with limited geographic scale. Declining gas volumes, electrification and RNG feedstock scarcity pressure revenue and raise transition/cost-recovery risk. 2024 system investment needs and regulatory lag can compress cash flow during multi-year capex cycles.

| Metric | 2024 |

|---|---|

| Customers | ~760,000 |

| System investment | $300 million |

| RNG availability | Constrained/premium |

Same Document Delivered

NW Natural SWOT Analysis

This is the actual NW Natural SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete structure, findings, and recommendations. Purchase unlocks the editable, full version for immediate download.