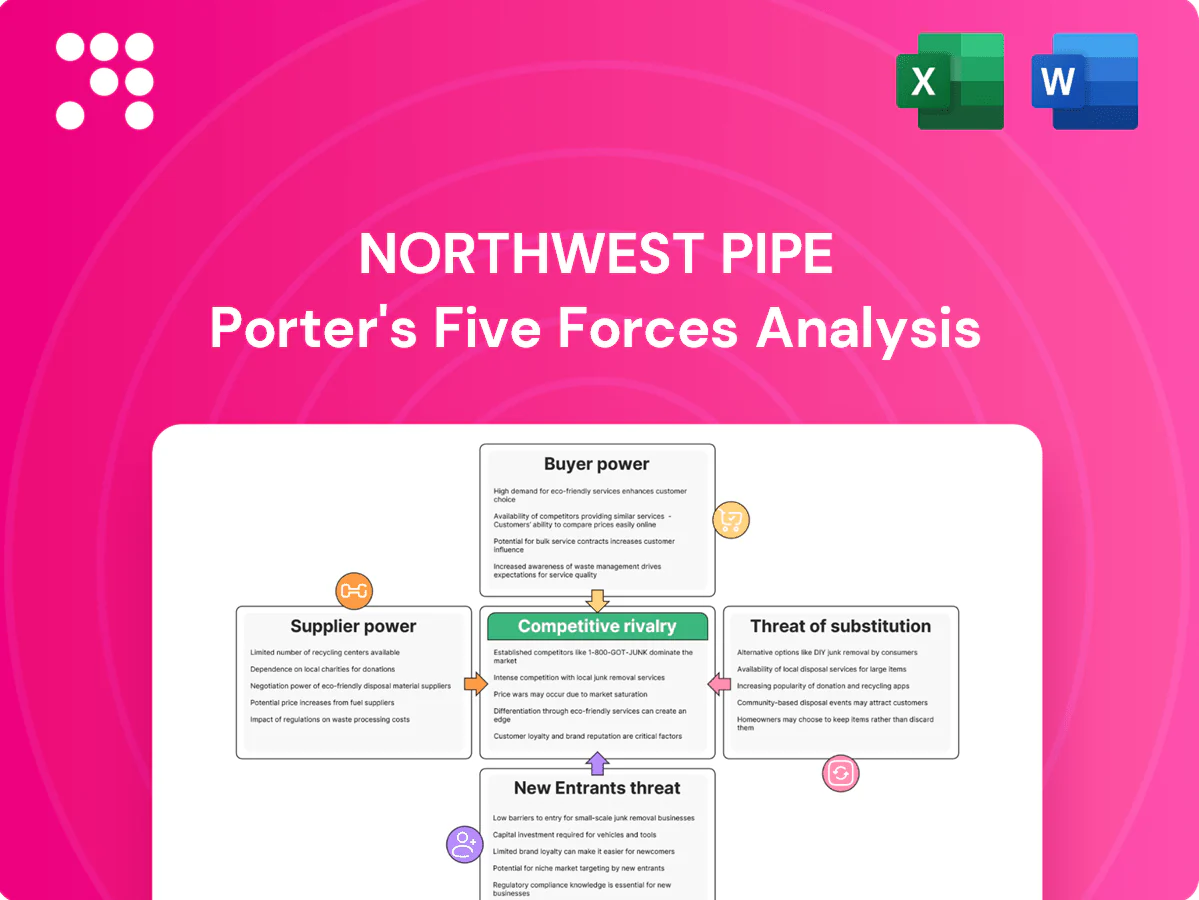

Northwest Pipe Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Northwest Pipe faces moderate supplier power and high rivalry as infrastructure demand and cyclicality shape margins; buyers pressure pricing through large contracts while substitutes remain limited. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, strategic implications, and scenario sensitivities. Purchase the full report for visuals, actionable insights, and ready-to-use slides.

Suppliers Bargaining Power

Concentrated steel plate/coil mills

Northwest Pipe depends on a narrow set of domestic steel plate and coil mills, concentrating supplier power and creating vulnerability when those mills tighten allocations or extend lead times, as seen through 2024 market allocation patterns.

During demand spikes mill lead times and allocations have constrained availability, enabling suppliers to enforce surcharges and pass-through pricing that pressure NWPX margins in 2024.

Concentration also limits Northwest Pipe’s ability to rapidly switch sources because alternative mills require time-consuming quality requalification, reducing short-term procurement flexibility.

Raw material price volatility

Steel, energy and coating-chemical costs showed pronounced volatility in 2024, with commodity swings exceeding 30% at points for scrap, iron ore and Brent crude (2024 average ~$86/bbl), tightening input margins for Northwest Pipe. Indexed supplier contracts have shifted price risk downstream, and pass-through lags often outpace spikes, compressing margins on fixed-price orders. Hedging reduces exposure but cannot fully protect multi-year fixed-bid projects from sudden commodity jumps.

Specialized coatings and consumables

Epoxy, polyurethane, cement mortar lining and specialty fittings for Northwest Pipe come from niche vendors certified to AWWA standards (eg AWWA C210 for cement-mortar) and NSF/ANSI 61; as of 2024 those certifications remain required for potable-water projects. Lengthy qualification cycles—measured in months to years—raise switching costs and lock specifications. That lock-in lets specialty suppliers command premium pricing and tighter terms. Suppliers' bargaining power is therefore high.

Logistics and freight constraints

Large-diameter steel and finished pipe segments often weigh 20–80 tons, requiring heavy-haul, rail, or barge capacity. Tight US trucking markets in 2024 and elevated fuel costs increase carrier leverage, while oversized loads typically need route permits and escorts (commonly for widths over 12 ft), adding cost. Logistics bottlenecks and limited rail/barge slots can delay projects, amplifying supplier bargaining power.

- Typical joint weight: 20–80 tons

- Oversize escorts often required for widths >12 ft

- 2024 trucking tightness and higher fuel costs boost carrier leverage

Trade policy and Buy America dynamics

Tariffs (Section 232 25% on steel) and Buy America rules tied to the $1.2 trillion Bipartisan Infrastructure Law materially constrain access to plate/coil and boost pricing power for domestic mills; import quotas and certification burdens raise dependence on qualified suppliers and documentation for federal projects. Policy shifts can rapidly reprice supply and alter negotiation leverage for Northwest Pipe.

- Tariff: 25% steel Section 232

- Bipartisan Infrastructure Law: $1.2 trillion

- Higher reliance on certified domestic mills

- Policy shifts quickly affect prices and leverage

Domestic pipe makers squeezed by steel tariffs, commodity swings and Buy America demand

Northwest Pipe faces high supplier bargaining power in 2024 due to concentrated domestic steel plate/coil mills (Section 232 tariff 25%) and limited alternative sources. 2024 commodity volatility (scrap/iron ore swings >30%, Brent ~$86/bbl) plus tighter trucking and extended mill lead times compressed margins. Buy America, AWWA/NSF certifications and the $1.2T Bipartisan Infrastructure Law raise switching costs and supplier leverage.

| Metric | 2024 value | Implication |

|---|---|---|

| Section 232 tariff | 25% | Boosts domestic mill pricing power |

| Brent crude | $86/bbl (avg) | Higher fuel/logistics costs |

| Commodity swings | >30% | Input-cost volatility |

| Bipartisan Infrastructure Law | $1.2T | Increases Buy America demand |

What is included in the product

Porter's Five Forces analysis tailored to Northwest Pipe uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry—highlighting industry-specific risks, pricing pressure, and strategic defenses to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for Northwest Pipe—clean, slide-ready layout that lets you customize pressure levels, swap in your own data, and instantly communicate strategic risk to stakeholders.

Customers Bargaining Power

Large, sophisticated municipal/EPC buyers

Utilities, water districts and EPCs run competitive tenders with strict specs and often pursue contracts exceeding $1 million, using lifecycle cost and service metrics to compare bids. Professional procurement teams benchmark total cost of ownership and service levels, increasing price sensitivity. Their scale and multi-year planning horizons and prequalification processes narrow vendor pools, amplifying negotiation leverage and driving tighter margins.

Project-based, lumpy demand

Orders are tied to discrete capital projects with sizable dollar values; buyers can time awards to market conditions and press for discounts, especially given lingering demand lumpiness across 2024 after the Bipartisan Infrastructure Law’s $55 billion water allocation. Schedule flexibility is routinely traded for price concessions, and at low mill utilization buyers gain disproportionate leverage.

Standardized specifications

AWWA maintains over 200 standards widely used across roughly 54,000 US community water systems, making base pipe offerings highly comparable across vendors. This standardization compresses product differentiation, enabling buyers to press for lower prices while still specifying minimum compliance. Northwest Pipe must therefore prioritize engineering services, coatings, delivery reliability and warranty enhancements to capture premiums and avoid pure commodity pricing.

Long lead times and penalties

Delivery schedules are critical for construction sequencing, and buyers frequently impose liquidated damages plus strict QA/QC, shifting execution risk to suppliers and pressuring Northwest Pipe to prioritize timeline certainty over margin. Vendors often concede tougher payment and warranty terms to secure projects, increasing working-capital strains and compressing gross margins.

- Buyers enforce LDs and QA/QC

- Execution risk shifts to suppliers

- Vendors concede terms for timelines

- Margin and cash-flow pressure

Access to alternative materials

Owners routinely benchmark steel against PCCP, ductile iron, HDPE/PVC and FRP; in 2024 VE and constructability reviews shifted an estimated 5–15% of project pipe spend between materials, giving buyers credible walk-away options and raising price sensitivity.

- materials considered: PCCP, ductile iron, HDPE/PVC, FRP

- 2024 VE pivot rate: 5–15% of pipe spend

- buyer optionality: increases bargaining leverage

Scale buyers squeeze margins across ~54,000 systems as $55B funds flow

Large utilities, water districts and EPCs run competitive tenders (> $1M) and benchmark TCO/service, boosting price sensitivity. Scale, multi-year planning and prequalification narrow suppliers and increase negotiation leverage across ~54,000 US systems. 2024 VE shifts of 5–15% of pipe spend and $55B water funding enhance buyer optionality and compress margins.

| Metric | Value |

|---|---|

| US water systems | ~54,000 |

| Typical contract size | > $1M |

| 2024 VE pivot | 5–15% |

| BIL water funding | $55B |

Preview Before You Purchase

Northwest Pipe Porter's Five Forces Analysis

This preview is the complete Porter’s Five Forces analysis for Northwest Pipe and is the exact document you’ll receive after purchase—no placeholders or excerpts. It’s fully formatted, ready to download, and immediately usable for decision-making or presentation.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Northwest Pipe faces moderate supplier power and high rivalry as infrastructure demand and cyclicality shape margins; buyers pressure pricing through large contracts while substitutes remain limited. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, strategic implications, and scenario sensitivities. Purchase the full report for visuals, actionable insights, and ready-to-use slides.

Suppliers Bargaining Power

Concentrated steel plate/coil mills

Northwest Pipe depends on a narrow set of domestic steel plate and coil mills, concentrating supplier power and creating vulnerability when those mills tighten allocations or extend lead times, as seen through 2024 market allocation patterns.

During demand spikes mill lead times and allocations have constrained availability, enabling suppliers to enforce surcharges and pass-through pricing that pressure NWPX margins in 2024.

Concentration also limits Northwest Pipe’s ability to rapidly switch sources because alternative mills require time-consuming quality requalification, reducing short-term procurement flexibility.

Raw material price volatility

Steel, energy and coating-chemical costs showed pronounced volatility in 2024, with commodity swings exceeding 30% at points for scrap, iron ore and Brent crude (2024 average ~$86/bbl), tightening input margins for Northwest Pipe. Indexed supplier contracts have shifted price risk downstream, and pass-through lags often outpace spikes, compressing margins on fixed-price orders. Hedging reduces exposure but cannot fully protect multi-year fixed-bid projects from sudden commodity jumps.

Specialized coatings and consumables

Epoxy, polyurethane, cement mortar lining and specialty fittings for Northwest Pipe come from niche vendors certified to AWWA standards (eg AWWA C210 for cement-mortar) and NSF/ANSI 61; as of 2024 those certifications remain required for potable-water projects. Lengthy qualification cycles—measured in months to years—raise switching costs and lock specifications. That lock-in lets specialty suppliers command premium pricing and tighter terms. Suppliers' bargaining power is therefore high.

Logistics and freight constraints

Large-diameter steel and finished pipe segments often weigh 20–80 tons, requiring heavy-haul, rail, or barge capacity. Tight US trucking markets in 2024 and elevated fuel costs increase carrier leverage, while oversized loads typically need route permits and escorts (commonly for widths over 12 ft), adding cost. Logistics bottlenecks and limited rail/barge slots can delay projects, amplifying supplier bargaining power.

- Typical joint weight: 20–80 tons

- Oversize escorts often required for widths >12 ft

- 2024 trucking tightness and higher fuel costs boost carrier leverage

Trade policy and Buy America dynamics

Tariffs (Section 232 25% on steel) and Buy America rules tied to the $1.2 trillion Bipartisan Infrastructure Law materially constrain access to plate/coil and boost pricing power for domestic mills; import quotas and certification burdens raise dependence on qualified suppliers and documentation for federal projects. Policy shifts can rapidly reprice supply and alter negotiation leverage for Northwest Pipe.

- Tariff: 25% steel Section 232

- Bipartisan Infrastructure Law: $1.2 trillion

- Higher reliance on certified domestic mills

- Policy shifts quickly affect prices and leverage

Domestic pipe makers squeezed by steel tariffs, commodity swings and Buy America demand

Northwest Pipe faces high supplier bargaining power in 2024 due to concentrated domestic steel plate/coil mills (Section 232 tariff 25%) and limited alternative sources. 2024 commodity volatility (scrap/iron ore swings >30%, Brent ~$86/bbl) plus tighter trucking and extended mill lead times compressed margins. Buy America, AWWA/NSF certifications and the $1.2T Bipartisan Infrastructure Law raise switching costs and supplier leverage.

| Metric | 2024 value | Implication |

|---|---|---|

| Section 232 tariff | 25% | Boosts domestic mill pricing power |

| Brent crude | $86/bbl (avg) | Higher fuel/logistics costs |

| Commodity swings | >30% | Input-cost volatility |

| Bipartisan Infrastructure Law | $1.2T | Increases Buy America demand |

What is included in the product

Porter's Five Forces analysis tailored to Northwest Pipe uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry—highlighting industry-specific risks, pricing pressure, and strategic defenses to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for Northwest Pipe—clean, slide-ready layout that lets you customize pressure levels, swap in your own data, and instantly communicate strategic risk to stakeholders.

Customers Bargaining Power

Large, sophisticated municipal/EPC buyers

Utilities, water districts and EPCs run competitive tenders with strict specs and often pursue contracts exceeding $1 million, using lifecycle cost and service metrics to compare bids. Professional procurement teams benchmark total cost of ownership and service levels, increasing price sensitivity. Their scale and multi-year planning horizons and prequalification processes narrow vendor pools, amplifying negotiation leverage and driving tighter margins.

Project-based, lumpy demand

Orders are tied to discrete capital projects with sizable dollar values; buyers can time awards to market conditions and press for discounts, especially given lingering demand lumpiness across 2024 after the Bipartisan Infrastructure Law’s $55 billion water allocation. Schedule flexibility is routinely traded for price concessions, and at low mill utilization buyers gain disproportionate leverage.

Standardized specifications

AWWA maintains over 200 standards widely used across roughly 54,000 US community water systems, making base pipe offerings highly comparable across vendors. This standardization compresses product differentiation, enabling buyers to press for lower prices while still specifying minimum compliance. Northwest Pipe must therefore prioritize engineering services, coatings, delivery reliability and warranty enhancements to capture premiums and avoid pure commodity pricing.

Long lead times and penalties

Delivery schedules are critical for construction sequencing, and buyers frequently impose liquidated damages plus strict QA/QC, shifting execution risk to suppliers and pressuring Northwest Pipe to prioritize timeline certainty over margin. Vendors often concede tougher payment and warranty terms to secure projects, increasing working-capital strains and compressing gross margins.

- Buyers enforce LDs and QA/QC

- Execution risk shifts to suppliers

- Vendors concede terms for timelines

- Margin and cash-flow pressure

Access to alternative materials

Owners routinely benchmark steel against PCCP, ductile iron, HDPE/PVC and FRP; in 2024 VE and constructability reviews shifted an estimated 5–15% of project pipe spend between materials, giving buyers credible walk-away options and raising price sensitivity.

- materials considered: PCCP, ductile iron, HDPE/PVC, FRP

- 2024 VE pivot rate: 5–15% of pipe spend

- buyer optionality: increases bargaining leverage

Scale buyers squeeze margins across ~54,000 systems as $55B funds flow

Large utilities, water districts and EPCs run competitive tenders (> $1M) and benchmark TCO/service, boosting price sensitivity. Scale, multi-year planning and prequalification narrow suppliers and increase negotiation leverage across ~54,000 US systems. 2024 VE shifts of 5–15% of pipe spend and $55B water funding enhance buyer optionality and compress margins.

| Metric | Value |

|---|---|

| US water systems | ~54,000 |

| Typical contract size | > $1M |

| 2024 VE pivot | 5–15% |

| BIL water funding | $55B |

Preview Before You Purchase

Northwest Pipe Porter's Five Forces Analysis

This preview is the complete Porter’s Five Forces analysis for Northwest Pipe and is the exact document you’ll receive after purchase—no placeholders or excerpts. It’s fully formatted, ready to download, and immediately usable for decision-making or presentation.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Northwest Pipe faces moderate supplier power and high rivalry as infrastructure demand and cyclicality shape margins; buyers pressure pricing through large contracts while substitutes remain limited. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for detailed force ratings, strategic implications, and scenario sensitivities. Purchase the full report for visuals, actionable insights, and ready-to-use slides.

Suppliers Bargaining Power

Concentrated steel plate/coil mills

Northwest Pipe depends on a narrow set of domestic steel plate and coil mills, concentrating supplier power and creating vulnerability when those mills tighten allocations or extend lead times, as seen through 2024 market allocation patterns.

During demand spikes mill lead times and allocations have constrained availability, enabling suppliers to enforce surcharges and pass-through pricing that pressure NWPX margins in 2024.

Concentration also limits Northwest Pipe’s ability to rapidly switch sources because alternative mills require time-consuming quality requalification, reducing short-term procurement flexibility.

Raw material price volatility

Steel, energy and coating-chemical costs showed pronounced volatility in 2024, with commodity swings exceeding 30% at points for scrap, iron ore and Brent crude (2024 average ~$86/bbl), tightening input margins for Northwest Pipe. Indexed supplier contracts have shifted price risk downstream, and pass-through lags often outpace spikes, compressing margins on fixed-price orders. Hedging reduces exposure but cannot fully protect multi-year fixed-bid projects from sudden commodity jumps.

Specialized coatings and consumables

Epoxy, polyurethane, cement mortar lining and specialty fittings for Northwest Pipe come from niche vendors certified to AWWA standards (eg AWWA C210 for cement-mortar) and NSF/ANSI 61; as of 2024 those certifications remain required for potable-water projects. Lengthy qualification cycles—measured in months to years—raise switching costs and lock specifications. That lock-in lets specialty suppliers command premium pricing and tighter terms. Suppliers' bargaining power is therefore high.

Logistics and freight constraints

Large-diameter steel and finished pipe segments often weigh 20–80 tons, requiring heavy-haul, rail, or barge capacity. Tight US trucking markets in 2024 and elevated fuel costs increase carrier leverage, while oversized loads typically need route permits and escorts (commonly for widths over 12 ft), adding cost. Logistics bottlenecks and limited rail/barge slots can delay projects, amplifying supplier bargaining power.

- Typical joint weight: 20–80 tons

- Oversize escorts often required for widths >12 ft

- 2024 trucking tightness and higher fuel costs boost carrier leverage

Trade policy and Buy America dynamics

Tariffs (Section 232 25% on steel) and Buy America rules tied to the $1.2 trillion Bipartisan Infrastructure Law materially constrain access to plate/coil and boost pricing power for domestic mills; import quotas and certification burdens raise dependence on qualified suppliers and documentation for federal projects. Policy shifts can rapidly reprice supply and alter negotiation leverage for Northwest Pipe.

- Tariff: 25% steel Section 232

- Bipartisan Infrastructure Law: $1.2 trillion

- Higher reliance on certified domestic mills

- Policy shifts quickly affect prices and leverage

Domestic pipe makers squeezed by steel tariffs, commodity swings and Buy America demand

Northwest Pipe faces high supplier bargaining power in 2024 due to concentrated domestic steel plate/coil mills (Section 232 tariff 25%) and limited alternative sources. 2024 commodity volatility (scrap/iron ore swings >30%, Brent ~$86/bbl) plus tighter trucking and extended mill lead times compressed margins. Buy America, AWWA/NSF certifications and the $1.2T Bipartisan Infrastructure Law raise switching costs and supplier leverage.

| Metric | 2024 value | Implication |

|---|---|---|

| Section 232 tariff | 25% | Boosts domestic mill pricing power |

| Brent crude | $86/bbl (avg) | Higher fuel/logistics costs |

| Commodity swings | >30% | Input-cost volatility |

| Bipartisan Infrastructure Law | $1.2T | Increases Buy America demand |

What is included in the product

Porter's Five Forces analysis tailored to Northwest Pipe uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and intensity of rivalry—highlighting industry-specific risks, pricing pressure, and strategic defenses to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for Northwest Pipe—clean, slide-ready layout that lets you customize pressure levels, swap in your own data, and instantly communicate strategic risk to stakeholders.

Customers Bargaining Power

Large, sophisticated municipal/EPC buyers

Utilities, water districts and EPCs run competitive tenders with strict specs and often pursue contracts exceeding $1 million, using lifecycle cost and service metrics to compare bids. Professional procurement teams benchmark total cost of ownership and service levels, increasing price sensitivity. Their scale and multi-year planning horizons and prequalification processes narrow vendor pools, amplifying negotiation leverage and driving tighter margins.

Project-based, lumpy demand

Orders are tied to discrete capital projects with sizable dollar values; buyers can time awards to market conditions and press for discounts, especially given lingering demand lumpiness across 2024 after the Bipartisan Infrastructure Law’s $55 billion water allocation. Schedule flexibility is routinely traded for price concessions, and at low mill utilization buyers gain disproportionate leverage.

Standardized specifications

AWWA maintains over 200 standards widely used across roughly 54,000 US community water systems, making base pipe offerings highly comparable across vendors. This standardization compresses product differentiation, enabling buyers to press for lower prices while still specifying minimum compliance. Northwest Pipe must therefore prioritize engineering services, coatings, delivery reliability and warranty enhancements to capture premiums and avoid pure commodity pricing.

Long lead times and penalties

Delivery schedules are critical for construction sequencing, and buyers frequently impose liquidated damages plus strict QA/QC, shifting execution risk to suppliers and pressuring Northwest Pipe to prioritize timeline certainty over margin. Vendors often concede tougher payment and warranty terms to secure projects, increasing working-capital strains and compressing gross margins.

- Buyers enforce LDs and QA/QC

- Execution risk shifts to suppliers

- Vendors concede terms for timelines

- Margin and cash-flow pressure

Access to alternative materials

Owners routinely benchmark steel against PCCP, ductile iron, HDPE/PVC and FRP; in 2024 VE and constructability reviews shifted an estimated 5–15% of project pipe spend between materials, giving buyers credible walk-away options and raising price sensitivity.

- materials considered: PCCP, ductile iron, HDPE/PVC, FRP

- 2024 VE pivot rate: 5–15% of pipe spend

- buyer optionality: increases bargaining leverage

Scale buyers squeeze margins across ~54,000 systems as $55B funds flow

Large utilities, water districts and EPCs run competitive tenders (> $1M) and benchmark TCO/service, boosting price sensitivity. Scale, multi-year planning and prequalification narrow suppliers and increase negotiation leverage across ~54,000 US systems. 2024 VE shifts of 5–15% of pipe spend and $55B water funding enhance buyer optionality and compress margins.

| Metric | Value |

|---|---|

| US water systems | ~54,000 |

| Typical contract size | > $1M |

| 2024 VE pivot | 5–15% |

| BIL water funding | $55B |

Preview Before You Purchase

Northwest Pipe Porter's Five Forces Analysis

This preview is the complete Porter’s Five Forces analysis for Northwest Pipe and is the exact document you’ll receive after purchase—no placeholders or excerpts. It’s fully formatted, ready to download, and immediately usable for decision-making or presentation.