O-I Glass Porter's Five Forces Analysis

Don't Miss the Bigger Picture

O-I Glass faces moderate supplier power, intense rivalry from global container makers, and rising substitute/packaging innovations that pressure margins; buyer consolidation raises negotiation leverage while capital intensity limits new entrants. This snapshot highlights key pressures shaping profitability and strategic choices. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

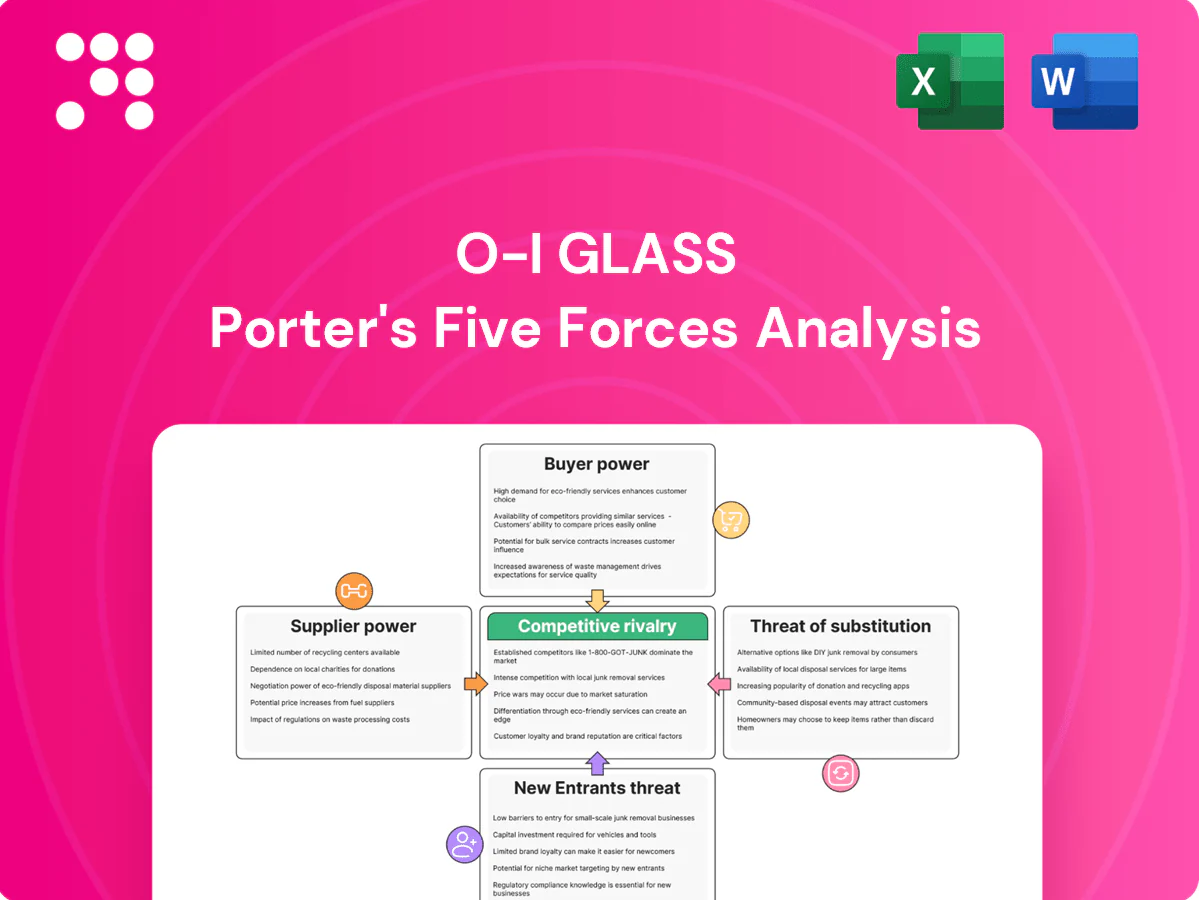

Suppliers Bargaining Power

Concentrated critical raw materials

Glass production relies on soda ash, limestone, silica sand and high-quality cullet, with soda ash and specialty refractories remaining highly concentrated suppliers as of 2024, increasing their pricing power. Regional cullet shortages and uneven collection systems tighten input markets and raise costs. O-I reduces exposure via multi-sourcing and higher recycled content targets but cannot fully remove supplier concentration risk.

Energy intensity and volatility

Melting furnaces are highly energy intensive, often making energy 20–30% of glass production costs, and exposure to volatile gas and power markets (EU ETS average ~€77/t CO2 in 2024) heightens supplier power. In regions with few utilities or constrained grids, suppliers can extract premiums; hedging and long‑term contracts mitigate but do not fully offset short-term spikes. Decarbonization mandates and rising carbon costs further increase energy‑supplier influence.

Specialized equipment and maintenance

Furnace refractories, forming machines, molds and control systems come from niche OEMs with high switching costs; 2024 industry lead times run about 6–12 months for furnace rebuilds and 12–24 weeks for molds. Qualification, integration needs and downtime risk give suppliers bargaining power, with unplanned outages costing glass plants roughly $100,000–$500,000 per day. Service contracts and spare-part constraints embed lock-in and dictate resilience.

Logistics and proximity constraints

Bulk raw materials for glass are heavy and low value-to-weight, making transport distance and cost critical; local quarry or soda ash suppliers near plants can exert leverage because economical alternatives are limited. Port congestion and trucking constraints spike supplier power during 2023–24 global supply disruptions. O-I’s ~70 plants across 20+ countries partly offset risk but dependence on nearby suppliers remains.

- Local suppliers: concentrated leverage

- Transport: high cost sensitivity

- Port/truck bottlenecks: amplify power

- O-I footprint: ~70 plants, partial mitigation

ESG and regulatory pressures on inputs

Environmental standards, recycled-content mandates and tightening emissions rules are shrinking the pool of compliant inputs, pushing glassmakers to source higher-quality cullet and low-carbon additives. Suppliers that meet elevated ESG thresholds capture pricing power and can charge premiums, while certification and traceability requirements create switching frictions and raise onboarding costs. This dynamic strengthens qualified suppliers’ bargaining positions relative to commoditized vendors and raises input cost predictability risks for O-I.

- ESG-compliant suppliers — higher premiums, less price elasticity

- Certification/traceability — increased switching costs and lead times

- Compliant-input scarcity — tightens supply, elevates supplier leverage

Energy 20–30% of costs; EU ETS €77/t raise supplier leverage

Supplier power is high due to concentrated soda ash and specialty refractory suppliers, regional cullet shortages and ESG-compliant input scarcity. Energy is 20–30% of production costs with EU ETS ≈€77/t CO2 in 2024, raising utility leverage. OEM lead times 6–12 months (furnace) and outages cost ~$100k–$500k/day; O-I has ~70 plants in 20+ countries.

| Metric | 2024 Value |

|---|---|

| Plants | ~70 |

| Energy share | 20–30% |

| EU ETS price | €77/t CO2 |

| Furnace lead time | 6–12 months |

| Outage cost/day | $100k–$500k |

What is included in the product

Tailored Porter's Five Forces analysis for O-I Glass highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for O-I Glass that instantly highlights competitive pressures with an interactive spider chart and customizable scores—perfect for fast boardroom decisions or slide-ready summaries. Swap in your own data, scenarios, or labels to model regulation shifts, new entrants, or supply-chain shocks without any complex code.

Customers Bargaining Power

Highly concentrated beverage customers

Global brewers, wine/spirits majors and soft‑drink giants buy huge glass volumes and negotiate aggressively, raising buyer power for O‑I Glass. Their professional procurement and scale increase price sensitivity and contract rigor, enabling demands on service levels, cost pass‑through caps and co‑funded innovation. In the US carbonated soft drink market Coca‑Cola and PepsiCo hold roughly 70% share (2024), concentrating leverage in core segments.

Switching options and dual sourcing

Large buyers use multi-supplier strategies and dual sourcing across regions to secure continuity and pricing; custom molds add stickiness but customers routinely requalify SKUs with rivals. The rise of alternatives — global aluminum can output surpassing 350 billion units by 2024 and widespread PET availability — strengthens buyer leverage. O-I must win on total cost, quality and sustainability to retain volume.

Customization versus lock-in

Proprietary molds, embossing and unique bottle designs create significant switching costs for premium brands, reinforcing customer dependence even as O-I reported 2024 net sales of about $6.8 billion; standard SKUs remain easily shifted between suppliers by volume buyers. Contractual tooling-ownership terms determine which party bears retooling costs, so customization tempers but does not eliminate buyer bargaining power.

Service reliability and proximity expectations

Beverage fillers demand on-time, in-full (OTIF) deliveries—often targeting 98%—and nearby plants to cut freight and breakage; missed KPIs trigger penalties or rapid shifts to rivals, increasing buyer bargaining power. Buyers leverage service metrics to press pricing and terms; O-I’s global footprint of about 70 plants helps proximity but must sustain tight OTIF and damage rates to retain contracts.

- OTIF target: 98%

- ~70 plants boosts proximity

- Misses → penalties or customer loss

Sustainability and price trade-offs

Buyers increasingly demand recycled content, lightweighting, and lower carbon footprints, and meeting these specs can win market share but raises production complexity and capital intensity for O-I Glass. Customers often resist full price premiums for eco-attributes, compressing margins and enhancing buyer negotiating leverage. This dynamic strengthens customer bargaining power and pressures O-I to balance sustainability investment with cost control.

- Demand: recycled content and low-carbon packaging

- Cost: higher CAPEX and process complexity

- Pricing: limited willingness to pay premiums

- Impact: margin pressure and stronger buyer leverage

Brewers, CSD duopoly ~70% and aluminum >350B units squeeze glass margins

Global brewers, wine/spirits majors and CSD giants (Coke/Pepsi ~70% US CSD share 2024) exert strong price and service pressure on O-I Glass (2024 net sales ~$6.8B). Alternatives (aluminum cans >350B units 2024, PET) and multi‑sourcing raise buyer leverage; OTIF targets ~98% and O-I’s ~70 plants partially mitigate proximity risks. Sustainability demands (recycled content, low‑carbon) add CAPEX and margin squeeze.

| Metric | Value (2024) |

|---|---|

| O-I net sales | $6.8B |

| US CSD share (Coke+Pepsi) | ~70% |

| Aluminum cans output | >350B units |

| Plants | ~70 |

| OTIF target | 98% |

Preview the Actual Deliverable

O-I Glass Porter's Five Forces Analysis

This preview of the O-I Glass Porter's Five Forces Analysis is the exact document you'll receive upon purchase—fully formatted and ready to use. No mockups or placeholders are shown; the file available for download is identical to this preview. Instant access follows payment, with professional analysis tailored for decision-makers.

Don't Miss the Bigger Picture

O-I Glass faces moderate supplier power, intense rivalry from global container makers, and rising substitute/packaging innovations that pressure margins; buyer consolidation raises negotiation leverage while capital intensity limits new entrants. This snapshot highlights key pressures shaping profitability and strategic choices. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated critical raw materials

Glass production relies on soda ash, limestone, silica sand and high-quality cullet, with soda ash and specialty refractories remaining highly concentrated suppliers as of 2024, increasing their pricing power. Regional cullet shortages and uneven collection systems tighten input markets and raise costs. O-I reduces exposure via multi-sourcing and higher recycled content targets but cannot fully remove supplier concentration risk.

Energy intensity and volatility

Melting furnaces are highly energy intensive, often making energy 20–30% of glass production costs, and exposure to volatile gas and power markets (EU ETS average ~€77/t CO2 in 2024) heightens supplier power. In regions with few utilities or constrained grids, suppliers can extract premiums; hedging and long‑term contracts mitigate but do not fully offset short-term spikes. Decarbonization mandates and rising carbon costs further increase energy‑supplier influence.

Specialized equipment and maintenance

Furnace refractories, forming machines, molds and control systems come from niche OEMs with high switching costs; 2024 industry lead times run about 6–12 months for furnace rebuilds and 12–24 weeks for molds. Qualification, integration needs and downtime risk give suppliers bargaining power, with unplanned outages costing glass plants roughly $100,000–$500,000 per day. Service contracts and spare-part constraints embed lock-in and dictate resilience.

Logistics and proximity constraints

Bulk raw materials for glass are heavy and low value-to-weight, making transport distance and cost critical; local quarry or soda ash suppliers near plants can exert leverage because economical alternatives are limited. Port congestion and trucking constraints spike supplier power during 2023–24 global supply disruptions. O-I’s ~70 plants across 20+ countries partly offset risk but dependence on nearby suppliers remains.

- Local suppliers: concentrated leverage

- Transport: high cost sensitivity

- Port/truck bottlenecks: amplify power

- O-I footprint: ~70 plants, partial mitigation

ESG and regulatory pressures on inputs

Environmental standards, recycled-content mandates and tightening emissions rules are shrinking the pool of compliant inputs, pushing glassmakers to source higher-quality cullet and low-carbon additives. Suppliers that meet elevated ESG thresholds capture pricing power and can charge premiums, while certification and traceability requirements create switching frictions and raise onboarding costs. This dynamic strengthens qualified suppliers’ bargaining positions relative to commoditized vendors and raises input cost predictability risks for O-I.

- ESG-compliant suppliers — higher premiums, less price elasticity

- Certification/traceability — increased switching costs and lead times

- Compliant-input scarcity — tightens supply, elevates supplier leverage

Energy 20–30% of costs; EU ETS €77/t raise supplier leverage

Supplier power is high due to concentrated soda ash and specialty refractory suppliers, regional cullet shortages and ESG-compliant input scarcity. Energy is 20–30% of production costs with EU ETS ≈€77/t CO2 in 2024, raising utility leverage. OEM lead times 6–12 months (furnace) and outages cost ~$100k–$500k/day; O-I has ~70 plants in 20+ countries.

| Metric | 2024 Value |

|---|---|

| Plants | ~70 |

| Energy share | 20–30% |

| EU ETS price | €77/t CO2 |

| Furnace lead time | 6–12 months |

| Outage cost/day | $100k–$500k |

What is included in the product

Tailored Porter's Five Forces analysis for O-I Glass highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for O-I Glass that instantly highlights competitive pressures with an interactive spider chart and customizable scores—perfect for fast boardroom decisions or slide-ready summaries. Swap in your own data, scenarios, or labels to model regulation shifts, new entrants, or supply-chain shocks without any complex code.

Customers Bargaining Power

Highly concentrated beverage customers

Global brewers, wine/spirits majors and soft‑drink giants buy huge glass volumes and negotiate aggressively, raising buyer power for O‑I Glass. Their professional procurement and scale increase price sensitivity and contract rigor, enabling demands on service levels, cost pass‑through caps and co‑funded innovation. In the US carbonated soft drink market Coca‑Cola and PepsiCo hold roughly 70% share (2024), concentrating leverage in core segments.

Switching options and dual sourcing

Large buyers use multi-supplier strategies and dual sourcing across regions to secure continuity and pricing; custom molds add stickiness but customers routinely requalify SKUs with rivals. The rise of alternatives — global aluminum can output surpassing 350 billion units by 2024 and widespread PET availability — strengthens buyer leverage. O-I must win on total cost, quality and sustainability to retain volume.

Customization versus lock-in

Proprietary molds, embossing and unique bottle designs create significant switching costs for premium brands, reinforcing customer dependence even as O-I reported 2024 net sales of about $6.8 billion; standard SKUs remain easily shifted between suppliers by volume buyers. Contractual tooling-ownership terms determine which party bears retooling costs, so customization tempers but does not eliminate buyer bargaining power.

Service reliability and proximity expectations

Beverage fillers demand on-time, in-full (OTIF) deliveries—often targeting 98%—and nearby plants to cut freight and breakage; missed KPIs trigger penalties or rapid shifts to rivals, increasing buyer bargaining power. Buyers leverage service metrics to press pricing and terms; O-I’s global footprint of about 70 plants helps proximity but must sustain tight OTIF and damage rates to retain contracts.

- OTIF target: 98%

- ~70 plants boosts proximity

- Misses → penalties or customer loss

Sustainability and price trade-offs

Buyers increasingly demand recycled content, lightweighting, and lower carbon footprints, and meeting these specs can win market share but raises production complexity and capital intensity for O-I Glass. Customers often resist full price premiums for eco-attributes, compressing margins and enhancing buyer negotiating leverage. This dynamic strengthens customer bargaining power and pressures O-I to balance sustainability investment with cost control.

- Demand: recycled content and low-carbon packaging

- Cost: higher CAPEX and process complexity

- Pricing: limited willingness to pay premiums

- Impact: margin pressure and stronger buyer leverage

Brewers, CSD duopoly ~70% and aluminum >350B units squeeze glass margins

Global brewers, wine/spirits majors and CSD giants (Coke/Pepsi ~70% US CSD share 2024) exert strong price and service pressure on O-I Glass (2024 net sales ~$6.8B). Alternatives (aluminum cans >350B units 2024, PET) and multi‑sourcing raise buyer leverage; OTIF targets ~98% and O-I’s ~70 plants partially mitigate proximity risks. Sustainability demands (recycled content, low‑carbon) add CAPEX and margin squeeze.

| Metric | Value (2024) |

|---|---|

| O-I net sales | $6.8B |

| US CSD share (Coke+Pepsi) | ~70% |

| Aluminum cans output | >350B units |

| Plants | ~70 |

| OTIF target | 98% |

Preview the Actual Deliverable

O-I Glass Porter's Five Forces Analysis

This preview of the O-I Glass Porter's Five Forces Analysis is the exact document you'll receive upon purchase—fully formatted and ready to use. No mockups or placeholders are shown; the file available for download is identical to this preview. Instant access follows payment, with professional analysis tailored for decision-makers.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

O-I Glass faces moderate supplier power, intense rivalry from global container makers, and rising substitute/packaging innovations that pressure margins; buyer consolidation raises negotiation leverage while capital intensity limits new entrants. This snapshot highlights key pressures shaping profitability and strategic choices. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated critical raw materials

Glass production relies on soda ash, limestone, silica sand and high-quality cullet, with soda ash and specialty refractories remaining highly concentrated suppliers as of 2024, increasing their pricing power. Regional cullet shortages and uneven collection systems tighten input markets and raise costs. O-I reduces exposure via multi-sourcing and higher recycled content targets but cannot fully remove supplier concentration risk.

Energy intensity and volatility

Melting furnaces are highly energy intensive, often making energy 20–30% of glass production costs, and exposure to volatile gas and power markets (EU ETS average ~€77/t CO2 in 2024) heightens supplier power. In regions with few utilities or constrained grids, suppliers can extract premiums; hedging and long‑term contracts mitigate but do not fully offset short-term spikes. Decarbonization mandates and rising carbon costs further increase energy‑supplier influence.

Specialized equipment and maintenance

Furnace refractories, forming machines, molds and control systems come from niche OEMs with high switching costs; 2024 industry lead times run about 6–12 months for furnace rebuilds and 12–24 weeks for molds. Qualification, integration needs and downtime risk give suppliers bargaining power, with unplanned outages costing glass plants roughly $100,000–$500,000 per day. Service contracts and spare-part constraints embed lock-in and dictate resilience.

Logistics and proximity constraints

Bulk raw materials for glass are heavy and low value-to-weight, making transport distance and cost critical; local quarry or soda ash suppliers near plants can exert leverage because economical alternatives are limited. Port congestion and trucking constraints spike supplier power during 2023–24 global supply disruptions. O-I’s ~70 plants across 20+ countries partly offset risk but dependence on nearby suppliers remains.

- Local suppliers: concentrated leverage

- Transport: high cost sensitivity

- Port/truck bottlenecks: amplify power

- O-I footprint: ~70 plants, partial mitigation

ESG and regulatory pressures on inputs

Environmental standards, recycled-content mandates and tightening emissions rules are shrinking the pool of compliant inputs, pushing glassmakers to source higher-quality cullet and low-carbon additives. Suppliers that meet elevated ESG thresholds capture pricing power and can charge premiums, while certification and traceability requirements create switching frictions and raise onboarding costs. This dynamic strengthens qualified suppliers’ bargaining positions relative to commoditized vendors and raises input cost predictability risks for O-I.

- ESG-compliant suppliers — higher premiums, less price elasticity

- Certification/traceability — increased switching costs and lead times

- Compliant-input scarcity — tightens supply, elevates supplier leverage

Energy 20–30% of costs; EU ETS €77/t raise supplier leverage

Supplier power is high due to concentrated soda ash and specialty refractory suppliers, regional cullet shortages and ESG-compliant input scarcity. Energy is 20–30% of production costs with EU ETS ≈€77/t CO2 in 2024, raising utility leverage. OEM lead times 6–12 months (furnace) and outages cost ~$100k–$500k/day; O-I has ~70 plants in 20+ countries.

| Metric | 2024 Value |

|---|---|

| Plants | ~70 |

| Energy share | 20–30% |

| EU ETS price | €77/t CO2 |

| Furnace lead time | 6–12 months |

| Outage cost/day | $100k–$500k |

What is included in the product

Tailored Porter's Five Forces analysis for O-I Glass highlighting competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive forces and strategic levers to protect margins and market share.

A concise, one-sheet Porter’s Five Forces for O-I Glass that instantly highlights competitive pressures with an interactive spider chart and customizable scores—perfect for fast boardroom decisions or slide-ready summaries. Swap in your own data, scenarios, or labels to model regulation shifts, new entrants, or supply-chain shocks without any complex code.

Customers Bargaining Power

Highly concentrated beverage customers

Global brewers, wine/spirits majors and soft‑drink giants buy huge glass volumes and negotiate aggressively, raising buyer power for O‑I Glass. Their professional procurement and scale increase price sensitivity and contract rigor, enabling demands on service levels, cost pass‑through caps and co‑funded innovation. In the US carbonated soft drink market Coca‑Cola and PepsiCo hold roughly 70% share (2024), concentrating leverage in core segments.

Switching options and dual sourcing

Large buyers use multi-supplier strategies and dual sourcing across regions to secure continuity and pricing; custom molds add stickiness but customers routinely requalify SKUs with rivals. The rise of alternatives — global aluminum can output surpassing 350 billion units by 2024 and widespread PET availability — strengthens buyer leverage. O-I must win on total cost, quality and sustainability to retain volume.

Customization versus lock-in

Proprietary molds, embossing and unique bottle designs create significant switching costs for premium brands, reinforcing customer dependence even as O-I reported 2024 net sales of about $6.8 billion; standard SKUs remain easily shifted between suppliers by volume buyers. Contractual tooling-ownership terms determine which party bears retooling costs, so customization tempers but does not eliminate buyer bargaining power.

Service reliability and proximity expectations

Beverage fillers demand on-time, in-full (OTIF) deliveries—often targeting 98%—and nearby plants to cut freight and breakage; missed KPIs trigger penalties or rapid shifts to rivals, increasing buyer bargaining power. Buyers leverage service metrics to press pricing and terms; O-I’s global footprint of about 70 plants helps proximity but must sustain tight OTIF and damage rates to retain contracts.

- OTIF target: 98%

- ~70 plants boosts proximity

- Misses → penalties or customer loss

Sustainability and price trade-offs

Buyers increasingly demand recycled content, lightweighting, and lower carbon footprints, and meeting these specs can win market share but raises production complexity and capital intensity for O-I Glass. Customers often resist full price premiums for eco-attributes, compressing margins and enhancing buyer negotiating leverage. This dynamic strengthens customer bargaining power and pressures O-I to balance sustainability investment with cost control.

- Demand: recycled content and low-carbon packaging

- Cost: higher CAPEX and process complexity

- Pricing: limited willingness to pay premiums

- Impact: margin pressure and stronger buyer leverage

Brewers, CSD duopoly ~70% and aluminum >350B units squeeze glass margins

Global brewers, wine/spirits majors and CSD giants (Coke/Pepsi ~70% US CSD share 2024) exert strong price and service pressure on O-I Glass (2024 net sales ~$6.8B). Alternatives (aluminum cans >350B units 2024, PET) and multi‑sourcing raise buyer leverage; OTIF targets ~98% and O-I’s ~70 plants partially mitigate proximity risks. Sustainability demands (recycled content, low‑carbon) add CAPEX and margin squeeze.

| Metric | Value (2024) |

|---|---|

| O-I net sales | $6.8B |

| US CSD share (Coke+Pepsi) | ~70% |

| Aluminum cans output | >350B units |

| Plants | ~70 |

| OTIF target | 98% |

Preview the Actual Deliverable

O-I Glass Porter's Five Forces Analysis

This preview of the O-I Glass Porter's Five Forces Analysis is the exact document you'll receive upon purchase—fully formatted and ready to use. No mockups or placeholders are shown; the file available for download is identical to this preview. Instant access follows payment, with professional analysis tailored for decision-makers.