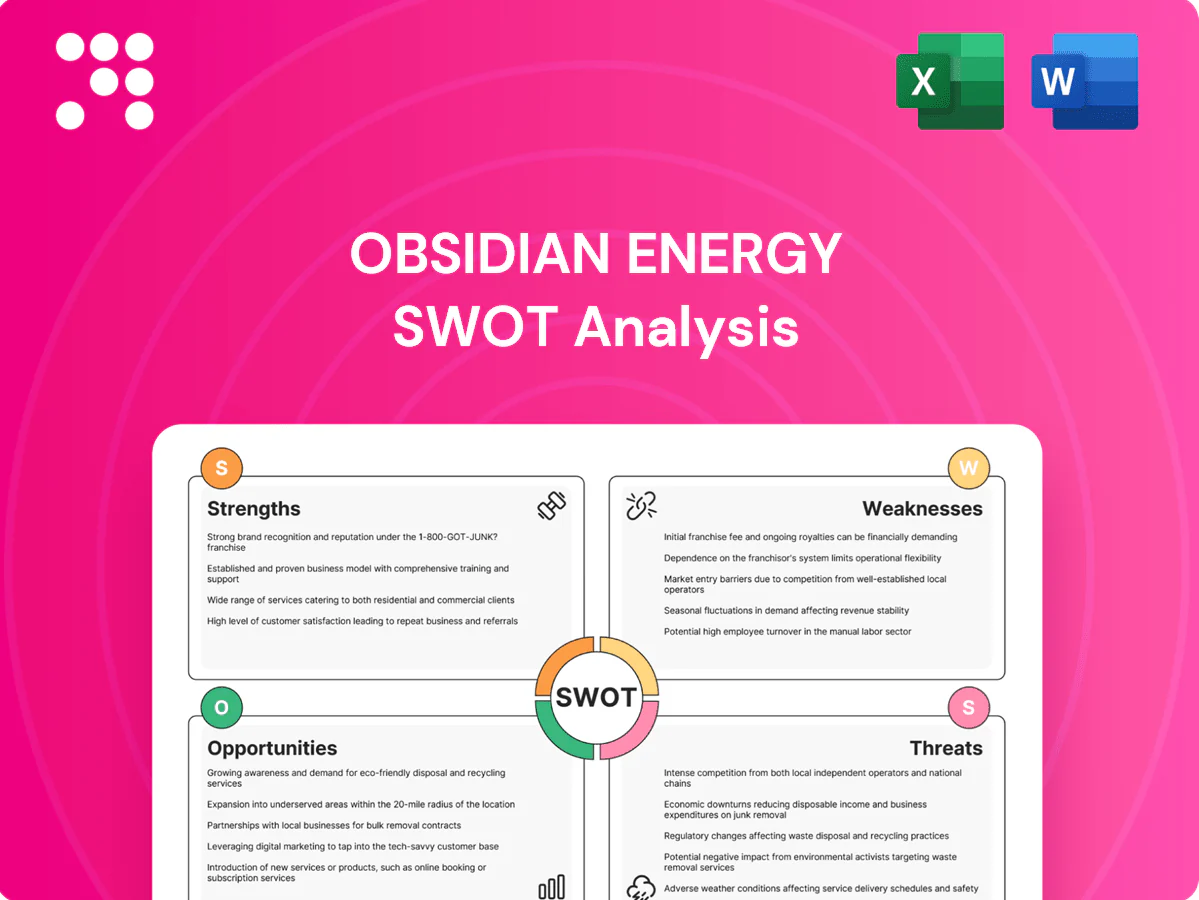

Obsidian Energy SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Obsidian Energy’s SWOT highlights resilient cash flow, asset optimization opportunities, regulatory exposure, and commodity-price sensitivity, offering a clear lens on operational strengths and strategic risks. Our full SWOT analysis unpacks competitive positioning, financial implications, and growth levers in actionable detail. Purchase the complete report to receive a professionally formatted, editable Word and Excel package to support investment or strategic decisions.

Strengths

Focused Western Canada footprint

Concentrated operations in Cardium, Viking and Peace River drive scale efficiencies and operational expertise, supporting Obsidian’s ~40,000 boe/d Western Canada production base. A tight geographic footprint cuts logistics complexity and downtime, lowering unit operating costs. Deep local knowledge improves well targeting and decline management, enabling consistent execution and capital efficiency.

Light oil–weighted production

Obsidian’s light oil–weighted production yields higher netbacks versus heavier grades, capturing 2024 WTI strength (roughly US$85/bbl) versus Canadian heavy differentials (~US$25/bbl), producing clear pricing uplift. Lower diluent requirements shrink operating and transport costs, improving cash margins and shortening payout periods. This mix enhances resilience across price cycles and helps fund self‑financed development.

Optimization culture and cost discipline

Management prioritizes high-IRR drilling, pad development, and decline mitigation, driving continuous improvements in drilling and completion designs that have materially lowered partner breakevens. Operating and sustaining capital efficiencies have expanded free cash flow potential, enabling higher returns and steady balance-sheet strengthening. This optimization culture underpins resilient capital allocation and shareholder value creation.

Established infrastructure and takeaway

Owned and accessible infrastructure in core Alberta areas reduces transport bottlenecks and lowers unit operating costs, while robust facility and water-handling capacity supports multi-year development and repeatable well designs. Midstream optionality improves uptime and realized differentials, enabling faster cycle times and smoother production ramps.

- Lower lift & transport costs

- Multi-year development support

- Midstream optionality → better differentials

- Faster cycle times, smoother ramps

Inventory depth in proven plays

Inventory depth across Cardium and Viking provides multi-year drilling visibility, reducing execution risk and underpinning predictable volume growth.

Repeatable geology and established type curves enhance capital allocation efficiency and improve well-level returns predictability.

Optional Peace River development offers portfolio flexibility, supporting sustained production and cash-flow longevity.

- Multi-year drilling visibility

- Repeatable geology and known type curves

- Portfolio flexibility via Peace River

- Supports sustainable production and cash flow

Light-oil assets (Cardium/Viking/Peace River): ~40,000 boe/d, WTI upside boosts netbacks

Concentrated Cardium, Viking and Peace River operations support ~40,000 boe/d, lowering unit costs through scale and local expertise. Light‑oil weighting captured 2024 WTI strength (~US$85/bbl) vs Canadian heavy differential (~US$25/bbl), boosting netbacks. Repeatable geology, owned infrastructure and midstream optionality enable multi‑year drilling visibility, faster ramps and improved free‑cash‑flow potential.

| Metric | Value |

|---|---|

| 2024 avg production | ~40,000 boe/d |

| WTI (2024 avg) | ~US$85/bbl |

| Can heavy differential (2024) | ~US$25/bbl |

What is included in the product

Delivers a strategic overview of Obsidian Energy’s internal and external business factors, highlighting strengths, weaknesses, opportunities, and threats shaping its operational performance and future growth prospects.

Delivers a concise, visual SWOT matrix tailored to Obsidian Energy for rapid strategic alignment and clear stakeholder briefings. Editable format lets teams update risks and opportunities quickly to reflect market shifts and operational priorities.

Weaknesses

Smaller scale vs. peers

Smaller corporate scale versus peers raises Obsidian Energy’s cost of capital and reduces pricing power; market cap ~C$1.1bn (mid‑2025) and exclusion from the S&P/TSX 60 limit institutional demand and index-driven flows. Limited budgets restrict concurrent project execution, slowing growth versus larger producers. Lower investor liquidity and index inclusion can cap valuation multiples in down cycles.

Commodity concentration

Obsidian remains oil‑weighted—roughly 70% of 2024 cash flow tied to crude—so WTI swings directly drive results and planning risk. Limited downstream integration offers little margin insulation, leaving realized prices near Brent/WTI benchmarks. Gas and NGL byproducts provide partial offset but did not fully stabilize 2024 cash flow. The result is amplified earnings variability and forecasting difficulty.

Decline and maintenance capital needs

Obsidian’s Montney and tight-oil exposures face natural decline rates typical of tight plays, roughly 25–40% in year one, requiring steady reinvestment to sustain volumes. High-grading can boost per-well returns but sustaining capital remains material, often representing the majority of annual capex. Any capital lapse quickly pressures volumes and lifts unit costs, compressing free cash flow in weak-price environments (Brent averaged about US$86/bbl in 2024).

Geographic and regulatory exposure

Operations concentrated in Alberta and Saskatchewan expose Obsidian Energy to provincial and federal policy shifts; Canada’s federal carbon price rose to CAD 70/t in 2024, raising operating costs and royalty sensitivity. Tightening methane regulations and stricter permitting increase compliance and capex needs, while cyclical regional labour and service constraints can spike service costs and delay projects, concentrating single-region operational and price risk.

- Geographic concentration: Western Canada only

- Carbon price: CAD 70/t (2024) raises costs

- Regulatory: methane/permitting compliance increases capex

- Operational: cyclical labour/service shortages amplify project risk

Balance sheet sensitivity

Balance sheet sensitivity: Obsidian’s leverage and covenant headroom tighten in downcycles — reported net debt of CAD 249m (Q4 2024) leaves limited buffer if prices drop and cash flow falls. Rising interest costs and upcoming refinancing windows through 2025 reduce financial flexibility, while hedging gaps can expose cash flows in prolonged downturns, constraining opportunistic M&A or buybacks.

- Net debt: CAD 249m (Q4 2024)

- Refinancing window: 2025

- Hedging gaps: exposes cash flow in downturns

- Limits: reduced capacity for M&A/buybacks

C$1.1bn cap, oil‑heavy (~70%), CAD 249m debt, CAD 70/t carbon risk

Smaller scale (market cap ~C$1.1bn mid‑2025) limits institutional demand and pricing power; oil‑weighted (~70% of 2024 cash flow) ties results to Brent/WTI volatility (Brent ~US$86/bbl in 2024). Net debt CAD 249m (Q4 2024) and 2025 refinancing windows tighten financial flexibility; operations concentrated in Western Canada face CAD 70/t carbon costs (2024) and regulatory/labour risks.

| Metric | Value | Implication |

|---|---|---|

| Market cap | C$1.1bn (mid‑2025) | Low institutional demand |

| Oil exposure | ~70% cash flow (2024) | Price sensitivity |

| Net debt | CAD 249m (Q4 2024) | Refinancing risk |

| Carbon price | CAD 70/t (2024) | Higher operating costs |

Full Version Awaits

Obsidian Energy SWOT Analysis

This is the actual SWOT analysis document for Obsidian Energy you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structure, findings, and editable content included in the download. Buy now to unlock the complete, detailed version immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Obsidian Energy’s SWOT highlights resilient cash flow, asset optimization opportunities, regulatory exposure, and commodity-price sensitivity, offering a clear lens on operational strengths and strategic risks. Our full SWOT analysis unpacks competitive positioning, financial implications, and growth levers in actionable detail. Purchase the complete report to receive a professionally formatted, editable Word and Excel package to support investment or strategic decisions.

Strengths

Focused Western Canada footprint

Concentrated operations in Cardium, Viking and Peace River drive scale efficiencies and operational expertise, supporting Obsidian’s ~40,000 boe/d Western Canada production base. A tight geographic footprint cuts logistics complexity and downtime, lowering unit operating costs. Deep local knowledge improves well targeting and decline management, enabling consistent execution and capital efficiency.

Light oil–weighted production

Obsidian’s light oil–weighted production yields higher netbacks versus heavier grades, capturing 2024 WTI strength (roughly US$85/bbl) versus Canadian heavy differentials (~US$25/bbl), producing clear pricing uplift. Lower diluent requirements shrink operating and transport costs, improving cash margins and shortening payout periods. This mix enhances resilience across price cycles and helps fund self‑financed development.

Optimization culture and cost discipline

Management prioritizes high-IRR drilling, pad development, and decline mitigation, driving continuous improvements in drilling and completion designs that have materially lowered partner breakevens. Operating and sustaining capital efficiencies have expanded free cash flow potential, enabling higher returns and steady balance-sheet strengthening. This optimization culture underpins resilient capital allocation and shareholder value creation.

Established infrastructure and takeaway

Owned and accessible infrastructure in core Alberta areas reduces transport bottlenecks and lowers unit operating costs, while robust facility and water-handling capacity supports multi-year development and repeatable well designs. Midstream optionality improves uptime and realized differentials, enabling faster cycle times and smoother production ramps.

- Lower lift & transport costs

- Multi-year development support

- Midstream optionality → better differentials

- Faster cycle times, smoother ramps

Inventory depth in proven plays

Inventory depth across Cardium and Viking provides multi-year drilling visibility, reducing execution risk and underpinning predictable volume growth.

Repeatable geology and established type curves enhance capital allocation efficiency and improve well-level returns predictability.

Optional Peace River development offers portfolio flexibility, supporting sustained production and cash-flow longevity.

- Multi-year drilling visibility

- Repeatable geology and known type curves

- Portfolio flexibility via Peace River

- Supports sustainable production and cash flow

Light-oil assets (Cardium/Viking/Peace River): ~40,000 boe/d, WTI upside boosts netbacks

Concentrated Cardium, Viking and Peace River operations support ~40,000 boe/d, lowering unit costs through scale and local expertise. Light‑oil weighting captured 2024 WTI strength (~US$85/bbl) vs Canadian heavy differential (~US$25/bbl), boosting netbacks. Repeatable geology, owned infrastructure and midstream optionality enable multi‑year drilling visibility, faster ramps and improved free‑cash‑flow potential.

| Metric | Value |

|---|---|

| 2024 avg production | ~40,000 boe/d |

| WTI (2024 avg) | ~US$85/bbl |

| Can heavy differential (2024) | ~US$25/bbl |

What is included in the product

Delivers a strategic overview of Obsidian Energy’s internal and external business factors, highlighting strengths, weaknesses, opportunities, and threats shaping its operational performance and future growth prospects.

Delivers a concise, visual SWOT matrix tailored to Obsidian Energy for rapid strategic alignment and clear stakeholder briefings. Editable format lets teams update risks and opportunities quickly to reflect market shifts and operational priorities.

Weaknesses

Smaller scale vs. peers

Smaller corporate scale versus peers raises Obsidian Energy’s cost of capital and reduces pricing power; market cap ~C$1.1bn (mid‑2025) and exclusion from the S&P/TSX 60 limit institutional demand and index-driven flows. Limited budgets restrict concurrent project execution, slowing growth versus larger producers. Lower investor liquidity and index inclusion can cap valuation multiples in down cycles.

Commodity concentration

Obsidian remains oil‑weighted—roughly 70% of 2024 cash flow tied to crude—so WTI swings directly drive results and planning risk. Limited downstream integration offers little margin insulation, leaving realized prices near Brent/WTI benchmarks. Gas and NGL byproducts provide partial offset but did not fully stabilize 2024 cash flow. The result is amplified earnings variability and forecasting difficulty.

Decline and maintenance capital needs

Obsidian’s Montney and tight-oil exposures face natural decline rates typical of tight plays, roughly 25–40% in year one, requiring steady reinvestment to sustain volumes. High-grading can boost per-well returns but sustaining capital remains material, often representing the majority of annual capex. Any capital lapse quickly pressures volumes and lifts unit costs, compressing free cash flow in weak-price environments (Brent averaged about US$86/bbl in 2024).

Geographic and regulatory exposure

Operations concentrated in Alberta and Saskatchewan expose Obsidian Energy to provincial and federal policy shifts; Canada’s federal carbon price rose to CAD 70/t in 2024, raising operating costs and royalty sensitivity. Tightening methane regulations and stricter permitting increase compliance and capex needs, while cyclical regional labour and service constraints can spike service costs and delay projects, concentrating single-region operational and price risk.

- Geographic concentration: Western Canada only

- Carbon price: CAD 70/t (2024) raises costs

- Regulatory: methane/permitting compliance increases capex

- Operational: cyclical labour/service shortages amplify project risk

Balance sheet sensitivity

Balance sheet sensitivity: Obsidian’s leverage and covenant headroom tighten in downcycles — reported net debt of CAD 249m (Q4 2024) leaves limited buffer if prices drop and cash flow falls. Rising interest costs and upcoming refinancing windows through 2025 reduce financial flexibility, while hedging gaps can expose cash flows in prolonged downturns, constraining opportunistic M&A or buybacks.

- Net debt: CAD 249m (Q4 2024)

- Refinancing window: 2025

- Hedging gaps: exposes cash flow in downturns

- Limits: reduced capacity for M&A/buybacks

C$1.1bn cap, oil‑heavy (~70%), CAD 249m debt, CAD 70/t carbon risk

Smaller scale (market cap ~C$1.1bn mid‑2025) limits institutional demand and pricing power; oil‑weighted (~70% of 2024 cash flow) ties results to Brent/WTI volatility (Brent ~US$86/bbl in 2024). Net debt CAD 249m (Q4 2024) and 2025 refinancing windows tighten financial flexibility; operations concentrated in Western Canada face CAD 70/t carbon costs (2024) and regulatory/labour risks.

| Metric | Value | Implication |

|---|---|---|

| Market cap | C$1.1bn (mid‑2025) | Low institutional demand |

| Oil exposure | ~70% cash flow (2024) | Price sensitivity |

| Net debt | CAD 249m (Q4 2024) | Refinancing risk |

| Carbon price | CAD 70/t (2024) | Higher operating costs |

Full Version Awaits

Obsidian Energy SWOT Analysis

This is the actual SWOT analysis document for Obsidian Energy you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structure, findings, and editable content included in the download. Buy now to unlock the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Obsidian Energy’s SWOT highlights resilient cash flow, asset optimization opportunities, regulatory exposure, and commodity-price sensitivity, offering a clear lens on operational strengths and strategic risks. Our full SWOT analysis unpacks competitive positioning, financial implications, and growth levers in actionable detail. Purchase the complete report to receive a professionally formatted, editable Word and Excel package to support investment or strategic decisions.

Strengths

Focused Western Canada footprint

Concentrated operations in Cardium, Viking and Peace River drive scale efficiencies and operational expertise, supporting Obsidian’s ~40,000 boe/d Western Canada production base. A tight geographic footprint cuts logistics complexity and downtime, lowering unit operating costs. Deep local knowledge improves well targeting and decline management, enabling consistent execution and capital efficiency.

Light oil–weighted production

Obsidian’s light oil–weighted production yields higher netbacks versus heavier grades, capturing 2024 WTI strength (roughly US$85/bbl) versus Canadian heavy differentials (~US$25/bbl), producing clear pricing uplift. Lower diluent requirements shrink operating and transport costs, improving cash margins and shortening payout periods. This mix enhances resilience across price cycles and helps fund self‑financed development.

Optimization culture and cost discipline

Management prioritizes high-IRR drilling, pad development, and decline mitigation, driving continuous improvements in drilling and completion designs that have materially lowered partner breakevens. Operating and sustaining capital efficiencies have expanded free cash flow potential, enabling higher returns and steady balance-sheet strengthening. This optimization culture underpins resilient capital allocation and shareholder value creation.

Established infrastructure and takeaway

Owned and accessible infrastructure in core Alberta areas reduces transport bottlenecks and lowers unit operating costs, while robust facility and water-handling capacity supports multi-year development and repeatable well designs. Midstream optionality improves uptime and realized differentials, enabling faster cycle times and smoother production ramps.

- Lower lift & transport costs

- Multi-year development support

- Midstream optionality → better differentials

- Faster cycle times, smoother ramps

Inventory depth in proven plays

Inventory depth across Cardium and Viking provides multi-year drilling visibility, reducing execution risk and underpinning predictable volume growth.

Repeatable geology and established type curves enhance capital allocation efficiency and improve well-level returns predictability.

Optional Peace River development offers portfolio flexibility, supporting sustained production and cash-flow longevity.

- Multi-year drilling visibility

- Repeatable geology and known type curves

- Portfolio flexibility via Peace River

- Supports sustainable production and cash flow

Light-oil assets (Cardium/Viking/Peace River): ~40,000 boe/d, WTI upside boosts netbacks

Concentrated Cardium, Viking and Peace River operations support ~40,000 boe/d, lowering unit costs through scale and local expertise. Light‑oil weighting captured 2024 WTI strength (~US$85/bbl) vs Canadian heavy differential (~US$25/bbl), boosting netbacks. Repeatable geology, owned infrastructure and midstream optionality enable multi‑year drilling visibility, faster ramps and improved free‑cash‑flow potential.

| Metric | Value |

|---|---|

| 2024 avg production | ~40,000 boe/d |

| WTI (2024 avg) | ~US$85/bbl |

| Can heavy differential (2024) | ~US$25/bbl |

What is included in the product

Delivers a strategic overview of Obsidian Energy’s internal and external business factors, highlighting strengths, weaknesses, opportunities, and threats shaping its operational performance and future growth prospects.

Delivers a concise, visual SWOT matrix tailored to Obsidian Energy for rapid strategic alignment and clear stakeholder briefings. Editable format lets teams update risks and opportunities quickly to reflect market shifts and operational priorities.

Weaknesses

Smaller scale vs. peers

Smaller corporate scale versus peers raises Obsidian Energy’s cost of capital and reduces pricing power; market cap ~C$1.1bn (mid‑2025) and exclusion from the S&P/TSX 60 limit institutional demand and index-driven flows. Limited budgets restrict concurrent project execution, slowing growth versus larger producers. Lower investor liquidity and index inclusion can cap valuation multiples in down cycles.

Commodity concentration

Obsidian remains oil‑weighted—roughly 70% of 2024 cash flow tied to crude—so WTI swings directly drive results and planning risk. Limited downstream integration offers little margin insulation, leaving realized prices near Brent/WTI benchmarks. Gas and NGL byproducts provide partial offset but did not fully stabilize 2024 cash flow. The result is amplified earnings variability and forecasting difficulty.

Decline and maintenance capital needs

Obsidian’s Montney and tight-oil exposures face natural decline rates typical of tight plays, roughly 25–40% in year one, requiring steady reinvestment to sustain volumes. High-grading can boost per-well returns but sustaining capital remains material, often representing the majority of annual capex. Any capital lapse quickly pressures volumes and lifts unit costs, compressing free cash flow in weak-price environments (Brent averaged about US$86/bbl in 2024).

Geographic and regulatory exposure

Operations concentrated in Alberta and Saskatchewan expose Obsidian Energy to provincial and federal policy shifts; Canada’s federal carbon price rose to CAD 70/t in 2024, raising operating costs and royalty sensitivity. Tightening methane regulations and stricter permitting increase compliance and capex needs, while cyclical regional labour and service constraints can spike service costs and delay projects, concentrating single-region operational and price risk.

- Geographic concentration: Western Canada only

- Carbon price: CAD 70/t (2024) raises costs

- Regulatory: methane/permitting compliance increases capex

- Operational: cyclical labour/service shortages amplify project risk

Balance sheet sensitivity

Balance sheet sensitivity: Obsidian’s leverage and covenant headroom tighten in downcycles — reported net debt of CAD 249m (Q4 2024) leaves limited buffer if prices drop and cash flow falls. Rising interest costs and upcoming refinancing windows through 2025 reduce financial flexibility, while hedging gaps can expose cash flows in prolonged downturns, constraining opportunistic M&A or buybacks.

- Net debt: CAD 249m (Q4 2024)

- Refinancing window: 2025

- Hedging gaps: exposes cash flow in downturns

- Limits: reduced capacity for M&A/buybacks

C$1.1bn cap, oil‑heavy (~70%), CAD 249m debt, CAD 70/t carbon risk

Smaller scale (market cap ~C$1.1bn mid‑2025) limits institutional demand and pricing power; oil‑weighted (~70% of 2024 cash flow) ties results to Brent/WTI volatility (Brent ~US$86/bbl in 2024). Net debt CAD 249m (Q4 2024) and 2025 refinancing windows tighten financial flexibility; operations concentrated in Western Canada face CAD 70/t carbon costs (2024) and regulatory/labour risks.

| Metric | Value | Implication |

|---|---|---|

| Market cap | C$1.1bn (mid‑2025) | Low institutional demand |

| Oil exposure | ~70% cash flow (2024) | Price sensitivity |

| Net debt | CAD 249m (Q4 2024) | Refinancing risk |

| Carbon price | CAD 70/t (2024) | Higher operating costs |

Full Version Awaits

Obsidian Energy SWOT Analysis

This is the actual SWOT analysis document for Obsidian Energy you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structure, findings, and editable content included in the download. Buy now to unlock the complete, detailed version immediately after checkout.