OCBC Bank Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

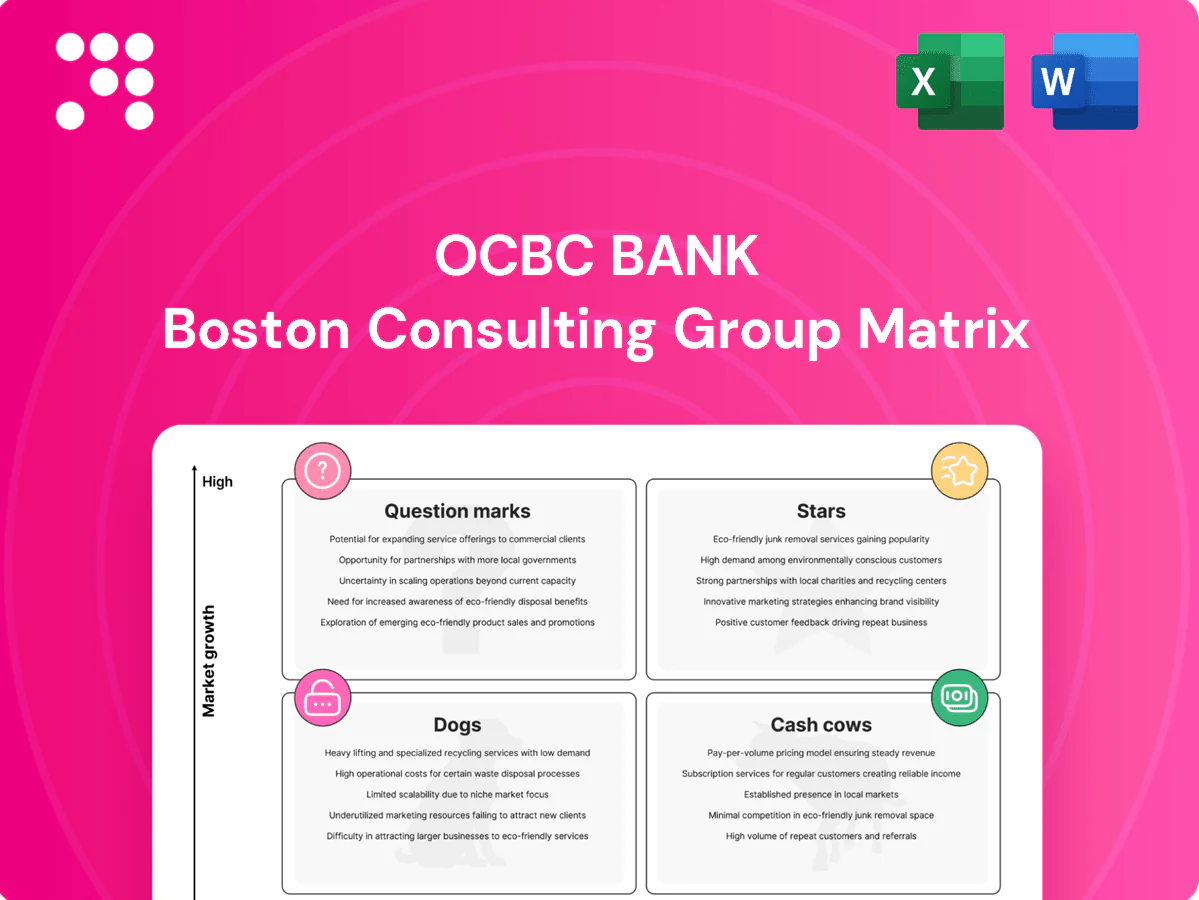

Curious where OCBC’s products and services sit—Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full OCBC BCG Matrix maps each offering to market share and growth, with clear strategic moves you can act on. Buy the complete report for quadrant-by-quadrant insights, data-backed recommendations, and ready-to-use Word and Excel files to steer investment and product decisions fast.

Stars

Wealth Management & Private Banking (Bank of Singapore)

Bank of Singapore, OCBC’s private-banking arm, sits in the Stars quadrant driven by high-growth client assets across Asia and leading positions in Singapore, Hong Kong and Dubai; it serves clients in more than 10 Asian markets and reports AUM north of USD 50 billion (2024), justifying heavy investment in bankers, platforms and product shelves. Maintain share and it will mature into a cash engine when growth cools; for now it is invest-to-win.

Digital Payments & Mobile Banking (OCBC Digital / Pay Anyone)

Mobile-first banking is expanding rapidly and OCBC Digital / Pay Anyone serves a hefty active base of over 3 million users in 2024; maintaining growth requires continuous investment in UX, security, and partner integrations. Revenue closely tracks engagement, so protecting share keeps the engagement-to-fee flywheel turning. With sustained retention and cross-sell, the channel can mature into a dependable earner for OCBC.

Life Insurance in Core Markets (Great Eastern)

Great Eastern, acquired by OCBC in 2004, is a life insurer across four core markets (Singapore, Malaysia, Indonesia, Brunei) where protection and savings demand is surging amid aging populations and rising middle-income cohorts.

Its bank-channel distribution leverages OCBC’s retail footprint to lower cost-to-serve and extend reach, supporting scale advantages in new business acquisition.

Growth requires ongoing capital and marketing investment to capture share; if momentum is sustained as markets mature, the franchise can transition from a high-investment star to a cash-generating cow.

Sustainable Finance & Green Lending

Green loans and transition financing are expanding rapidly and OCBC is a visible leader, executing complex mandates that require intensive origination and risk structuring while capturing rising deal flow and fee pools in 2024.

- Leadership in Asia-Pacific sustainable finance

- High origination and risk-work intensity

- Growing deal flow and fee pools in 2024

- Continued investment positions OCBC for long-run dominance

FX & Rates Franchise in Home Market

OCBCs FX & Rates franchise in the home market is a star: high client activity and strong share in SGD-linked flows drive recurring trading volumes and cross-sell into hedging and investment products. Maintaining deep liquidity, advanced pricing technology, and risk capacity consumes capital and management attention but secures leadership in flow generation.

- High client activity

- SGD-linked flow leadership

- Liquidity & pricing tech intensive

- Recurring flow + cross-sell

- Priority: stay liquid, stay leader

Wealth AUM USD 50bn+, 3m+ digital users, SE Asia insurance growth, green loans & FX fee capture

OCBC Stars: Bank of Singapore AUM > USD 50bn (2024); OCBC Digital Pay Anyone > 3m active users (2024); Great Eastern growth across SG/MY/ID/BN; leadership in green loans and FX/SGD flow franchise capturing rising 2024 fee pools.

| Business | 2024 Metric |

|---|---|

| Bank of Singapore | AUM > USD 50bn |

| OCBC Digital | > 3m active users |

| Great Eastern | 4 core markets |

| Sustainable finance | Growing 2024 fee pools |

What is included in the product

Comprehensive OCBC BCG Matrix overview with strategic recommendations for Stars, Cash Cows, Question Marks and Dogs.

One-page OCBC BCG Matrix mapping each unit to a quadrant—clear decisions, no guesswork.

Cash Cows

Singapore Retail Deposits & Mortgages

Singapore retail deposits and mortgages are a mature, high-share cash cow for OCBC, underpinning its position as Singapore's second-largest bank by assets in 2024. These portfolios feature low incremental acquisition costs and sticky balances that supply stable funding and margin. OCBC targeted efficiency investments rather than aggressive growth, optimizing cost-to-serve and digital onboarding in 2024. The franchise reliably funds core operations and contributes surplus earnings.

SME Lending in Core Geographies

SME lending in core geographies is a large, relationship-driven book (around SGD 55bn) with stable risk outcomes—non-performing loans below 1.5% and default experience materially better than unsecured segments. Growth is modest but yields and fee income remain reliable, contributing steady NII and fee revenue. Infrastructure upgrades have reduced processing costs and improved efficiency, enabling margin preservation while defending market share.

Corporate Cash Management & Transaction Banking

Corporate cash management and transaction banking deliver entrenched mandates with large corporates, producing recurring fee income, low growth and high customer stickiness with strong operating leverage; incremental 2024 spend is focused on APIs and service uptime to protect volumes, making the franchise a dependable cash machine for OCBC.

Trade Finance in Established Sectors

Trade Finance in established corridors shows steady volumes and OCBC’s regional network keeps the bank entrenched; margins remain moderate but utilization predictable; ongoing digitalization reduces cost-to-serve and improves processing times; classic cash cow dynamics persist.

- steady volumes

- predictable margins

- network entrenchment

- digital cost trim

Credit Cards in Mature Segments (SG/MY)

Competition is intense in SG and MY card markets, but OCBC leverages a solid cardholder base and steady interchange income to deliver predictable fee and interest revenue; acquisition costs are contained and retention tactics (rewards, partnerships) are well-established. Not high-growth—reliable, cash-generative business to milk and maintain.

- Steady interchange flows

- Controlled acquisition costs

- High retention via rewards

- Low growth, strong cash yield

Singapore deposits, mortgages & SME loans: steady funding, predictable fee income

Singapore retail deposits and mortgages underpin OCBC’s 2024 position as Singapore’s second-largest bank by assets, supplying stable funding; SME lending (~SGD 55bn) shows NPLs <1.5%; corporate cash management and trade finance deliver recurring fees and low growth; cards provide steady interchange income with controlled acquisition costs.

| Business | 2024 metric | Role |

|---|---|---|

| Retail deposits & mortgages | Major funding source | Cash cow |

| SME lending | ~SGD 55bn; NPL <1.5% | Stable yield |

| Txn banking & trade | Recurring fees | Low growth, high stickiness |

| Cards | Steady interchange | Predictable cash flow |

Full Transparency, Always

OCBC Bank BCG Matrix

The OCBC Bank BCG Matrix you’re previewing is the exact file you’ll receive after purchase—no watermarks, no demo overlays. This ready-to-use report is formatted for clarity and immediate presentation, crafted by analysts with banking-sector insight. After buying, the full, editable document is yours to download, print, or share with stakeholders—no surprises, just strategic-ready content.

Visual. Strategic. Downloadable.

Curious where OCBC’s products and services sit—Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full OCBC BCG Matrix maps each offering to market share and growth, with clear strategic moves you can act on. Buy the complete report for quadrant-by-quadrant insights, data-backed recommendations, and ready-to-use Word and Excel files to steer investment and product decisions fast.

Stars

Wealth Management & Private Banking (Bank of Singapore)

Bank of Singapore, OCBC’s private-banking arm, sits in the Stars quadrant driven by high-growth client assets across Asia and leading positions in Singapore, Hong Kong and Dubai; it serves clients in more than 10 Asian markets and reports AUM north of USD 50 billion (2024), justifying heavy investment in bankers, platforms and product shelves. Maintain share and it will mature into a cash engine when growth cools; for now it is invest-to-win.

Digital Payments & Mobile Banking (OCBC Digital / Pay Anyone)

Mobile-first banking is expanding rapidly and OCBC Digital / Pay Anyone serves a hefty active base of over 3 million users in 2024; maintaining growth requires continuous investment in UX, security, and partner integrations. Revenue closely tracks engagement, so protecting share keeps the engagement-to-fee flywheel turning. With sustained retention and cross-sell, the channel can mature into a dependable earner for OCBC.

Life Insurance in Core Markets (Great Eastern)

Great Eastern, acquired by OCBC in 2004, is a life insurer across four core markets (Singapore, Malaysia, Indonesia, Brunei) where protection and savings demand is surging amid aging populations and rising middle-income cohorts.

Its bank-channel distribution leverages OCBC’s retail footprint to lower cost-to-serve and extend reach, supporting scale advantages in new business acquisition.

Growth requires ongoing capital and marketing investment to capture share; if momentum is sustained as markets mature, the franchise can transition from a high-investment star to a cash-generating cow.

Sustainable Finance & Green Lending

Green loans and transition financing are expanding rapidly and OCBC is a visible leader, executing complex mandates that require intensive origination and risk structuring while capturing rising deal flow and fee pools in 2024.

- Leadership in Asia-Pacific sustainable finance

- High origination and risk-work intensity

- Growing deal flow and fee pools in 2024

- Continued investment positions OCBC for long-run dominance

FX & Rates Franchise in Home Market

OCBCs FX & Rates franchise in the home market is a star: high client activity and strong share in SGD-linked flows drive recurring trading volumes and cross-sell into hedging and investment products. Maintaining deep liquidity, advanced pricing technology, and risk capacity consumes capital and management attention but secures leadership in flow generation.

- High client activity

- SGD-linked flow leadership

- Liquidity & pricing tech intensive

- Recurring flow + cross-sell

- Priority: stay liquid, stay leader

Wealth AUM USD 50bn+, 3m+ digital users, SE Asia insurance growth, green loans & FX fee capture

OCBC Stars: Bank of Singapore AUM > USD 50bn (2024); OCBC Digital Pay Anyone > 3m active users (2024); Great Eastern growth across SG/MY/ID/BN; leadership in green loans and FX/SGD flow franchise capturing rising 2024 fee pools.

| Business | 2024 Metric |

|---|---|

| Bank of Singapore | AUM > USD 50bn |

| OCBC Digital | > 3m active users |

| Great Eastern | 4 core markets |

| Sustainable finance | Growing 2024 fee pools |

What is included in the product

Comprehensive OCBC BCG Matrix overview with strategic recommendations for Stars, Cash Cows, Question Marks and Dogs.

One-page OCBC BCG Matrix mapping each unit to a quadrant—clear decisions, no guesswork.

Cash Cows

Singapore Retail Deposits & Mortgages

Singapore retail deposits and mortgages are a mature, high-share cash cow for OCBC, underpinning its position as Singapore's second-largest bank by assets in 2024. These portfolios feature low incremental acquisition costs and sticky balances that supply stable funding and margin. OCBC targeted efficiency investments rather than aggressive growth, optimizing cost-to-serve and digital onboarding in 2024. The franchise reliably funds core operations and contributes surplus earnings.

SME Lending in Core Geographies

SME lending in core geographies is a large, relationship-driven book (around SGD 55bn) with stable risk outcomes—non-performing loans below 1.5% and default experience materially better than unsecured segments. Growth is modest but yields and fee income remain reliable, contributing steady NII and fee revenue. Infrastructure upgrades have reduced processing costs and improved efficiency, enabling margin preservation while defending market share.

Corporate Cash Management & Transaction Banking

Corporate cash management and transaction banking deliver entrenched mandates with large corporates, producing recurring fee income, low growth and high customer stickiness with strong operating leverage; incremental 2024 spend is focused on APIs and service uptime to protect volumes, making the franchise a dependable cash machine for OCBC.

Trade Finance in Established Sectors

Trade Finance in established corridors shows steady volumes and OCBC’s regional network keeps the bank entrenched; margins remain moderate but utilization predictable; ongoing digitalization reduces cost-to-serve and improves processing times; classic cash cow dynamics persist.

- steady volumes

- predictable margins

- network entrenchment

- digital cost trim

Credit Cards in Mature Segments (SG/MY)

Competition is intense in SG and MY card markets, but OCBC leverages a solid cardholder base and steady interchange income to deliver predictable fee and interest revenue; acquisition costs are contained and retention tactics (rewards, partnerships) are well-established. Not high-growth—reliable, cash-generative business to milk and maintain.

- Steady interchange flows

- Controlled acquisition costs

- High retention via rewards

- Low growth, strong cash yield

Singapore deposits, mortgages & SME loans: steady funding, predictable fee income

Singapore retail deposits and mortgages underpin OCBC’s 2024 position as Singapore’s second-largest bank by assets, supplying stable funding; SME lending (~SGD 55bn) shows NPLs <1.5%; corporate cash management and trade finance deliver recurring fees and low growth; cards provide steady interchange income with controlled acquisition costs.

| Business | 2024 metric | Role |

|---|---|---|

| Retail deposits & mortgages | Major funding source | Cash cow |

| SME lending | ~SGD 55bn; NPL <1.5% | Stable yield |

| Txn banking & trade | Recurring fees | Low growth, high stickiness |

| Cards | Steady interchange | Predictable cash flow |

Full Transparency, Always

OCBC Bank BCG Matrix

The OCBC Bank BCG Matrix you’re previewing is the exact file you’ll receive after purchase—no watermarks, no demo overlays. This ready-to-use report is formatted for clarity and immediate presentation, crafted by analysts with banking-sector insight. After buying, the full, editable document is yours to download, print, or share with stakeholders—no surprises, just strategic-ready content.

Description

Visual. Strategic. Downloadable.

Curious where OCBC’s products and services sit—Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full OCBC BCG Matrix maps each offering to market share and growth, with clear strategic moves you can act on. Buy the complete report for quadrant-by-quadrant insights, data-backed recommendations, and ready-to-use Word and Excel files to steer investment and product decisions fast.

Stars

Wealth Management & Private Banking (Bank of Singapore)

Bank of Singapore, OCBC’s private-banking arm, sits in the Stars quadrant driven by high-growth client assets across Asia and leading positions in Singapore, Hong Kong and Dubai; it serves clients in more than 10 Asian markets and reports AUM north of USD 50 billion (2024), justifying heavy investment in bankers, platforms and product shelves. Maintain share and it will mature into a cash engine when growth cools; for now it is invest-to-win.

Digital Payments & Mobile Banking (OCBC Digital / Pay Anyone)

Mobile-first banking is expanding rapidly and OCBC Digital / Pay Anyone serves a hefty active base of over 3 million users in 2024; maintaining growth requires continuous investment in UX, security, and partner integrations. Revenue closely tracks engagement, so protecting share keeps the engagement-to-fee flywheel turning. With sustained retention and cross-sell, the channel can mature into a dependable earner for OCBC.

Life Insurance in Core Markets (Great Eastern)

Great Eastern, acquired by OCBC in 2004, is a life insurer across four core markets (Singapore, Malaysia, Indonesia, Brunei) where protection and savings demand is surging amid aging populations and rising middle-income cohorts.

Its bank-channel distribution leverages OCBC’s retail footprint to lower cost-to-serve and extend reach, supporting scale advantages in new business acquisition.

Growth requires ongoing capital and marketing investment to capture share; if momentum is sustained as markets mature, the franchise can transition from a high-investment star to a cash-generating cow.

Sustainable Finance & Green Lending

Green loans and transition financing are expanding rapidly and OCBC is a visible leader, executing complex mandates that require intensive origination and risk structuring while capturing rising deal flow and fee pools in 2024.

- Leadership in Asia-Pacific sustainable finance

- High origination and risk-work intensity

- Growing deal flow and fee pools in 2024

- Continued investment positions OCBC for long-run dominance

FX & Rates Franchise in Home Market

OCBCs FX & Rates franchise in the home market is a star: high client activity and strong share in SGD-linked flows drive recurring trading volumes and cross-sell into hedging and investment products. Maintaining deep liquidity, advanced pricing technology, and risk capacity consumes capital and management attention but secures leadership in flow generation.

- High client activity

- SGD-linked flow leadership

- Liquidity & pricing tech intensive

- Recurring flow + cross-sell

- Priority: stay liquid, stay leader

Wealth AUM USD 50bn+, 3m+ digital users, SE Asia insurance growth, green loans & FX fee capture

OCBC Stars: Bank of Singapore AUM > USD 50bn (2024); OCBC Digital Pay Anyone > 3m active users (2024); Great Eastern growth across SG/MY/ID/BN; leadership in green loans and FX/SGD flow franchise capturing rising 2024 fee pools.

| Business | 2024 Metric |

|---|---|

| Bank of Singapore | AUM > USD 50bn |

| OCBC Digital | > 3m active users |

| Great Eastern | 4 core markets |

| Sustainable finance | Growing 2024 fee pools |

What is included in the product

Comprehensive OCBC BCG Matrix overview with strategic recommendations for Stars, Cash Cows, Question Marks and Dogs.

One-page OCBC BCG Matrix mapping each unit to a quadrant—clear decisions, no guesswork.

Cash Cows

Singapore Retail Deposits & Mortgages

Singapore retail deposits and mortgages are a mature, high-share cash cow for OCBC, underpinning its position as Singapore's second-largest bank by assets in 2024. These portfolios feature low incremental acquisition costs and sticky balances that supply stable funding and margin. OCBC targeted efficiency investments rather than aggressive growth, optimizing cost-to-serve and digital onboarding in 2024. The franchise reliably funds core operations and contributes surplus earnings.

SME Lending in Core Geographies

SME lending in core geographies is a large, relationship-driven book (around SGD 55bn) with stable risk outcomes—non-performing loans below 1.5% and default experience materially better than unsecured segments. Growth is modest but yields and fee income remain reliable, contributing steady NII and fee revenue. Infrastructure upgrades have reduced processing costs and improved efficiency, enabling margin preservation while defending market share.

Corporate Cash Management & Transaction Banking

Corporate cash management and transaction banking deliver entrenched mandates with large corporates, producing recurring fee income, low growth and high customer stickiness with strong operating leverage; incremental 2024 spend is focused on APIs and service uptime to protect volumes, making the franchise a dependable cash machine for OCBC.

Trade Finance in Established Sectors

Trade Finance in established corridors shows steady volumes and OCBC’s regional network keeps the bank entrenched; margins remain moderate but utilization predictable; ongoing digitalization reduces cost-to-serve and improves processing times; classic cash cow dynamics persist.

- steady volumes

- predictable margins

- network entrenchment

- digital cost trim

Credit Cards in Mature Segments (SG/MY)

Competition is intense in SG and MY card markets, but OCBC leverages a solid cardholder base and steady interchange income to deliver predictable fee and interest revenue; acquisition costs are contained and retention tactics (rewards, partnerships) are well-established. Not high-growth—reliable, cash-generative business to milk and maintain.

- Steady interchange flows

- Controlled acquisition costs

- High retention via rewards

- Low growth, strong cash yield

Singapore deposits, mortgages & SME loans: steady funding, predictable fee income

Singapore retail deposits and mortgages underpin OCBC’s 2024 position as Singapore’s second-largest bank by assets, supplying stable funding; SME lending (~SGD 55bn) shows NPLs <1.5%; corporate cash management and trade finance deliver recurring fees and low growth; cards provide steady interchange income with controlled acquisition costs.

| Business | 2024 metric | Role |

|---|---|---|

| Retail deposits & mortgages | Major funding source | Cash cow |

| SME lending | ~SGD 55bn; NPL <1.5% | Stable yield |

| Txn banking & trade | Recurring fees | Low growth, high stickiness |

| Cards | Steady interchange | Predictable cash flow |

Full Transparency, Always

OCBC Bank BCG Matrix

The OCBC Bank BCG Matrix you’re previewing is the exact file you’ll receive after purchase—no watermarks, no demo overlays. This ready-to-use report is formatted for clarity and immediate presentation, crafted by analysts with banking-sector insight. After buying, the full, editable document is yours to download, print, or share with stakeholders—no surprises, just strategic-ready content.