OCBC Bank Business Model Canvas

Bank Business Model Canvas: customer value, distribution, and revenue for retail & corporate

Explore OCBC Bank’s Business Model Canvas to uncover how it creates customer value, scales distribution, and secures revenue across retail and corporate banking. This concise yet insightful snapshot highlights partnerships, channels, and cost drivers. Purchase the full Canvas for the complete nine-block analysis, editable templates, and strategic takeaways to inform investments or planning.

Partnerships

Regulators and central banks

OCBC collaborates closely with regulators such as MAS to maintain compliance and systemic stability; as one of Singapore's three domestic banks in 2024 it engages in MAS-led prudential supervision, resolution planning and licensing. These relationships enable access to payment rails and clearing systems including FAST, PayNow and MAS RTGS. Regular engagement builds credibility and customer trust.

Payment networks and processors

Partnerships with Visa, Mastercard, UnionPay and local schemes enable OCBC’s card issuance, merchant acquiring and cross-border rails, with global schemes covering over 90% of card acceptance worldwide. These partners supply advanced fraud detection and tokenization, boosting card security and digital wallet onboarding. Co-branding and interchange arrangements improve card economics and merchant margins, while joint initiatives accelerate contactless and wallet innovation across SEA markets.

Fintech and technology providers

Alliances with core banking vendors, cloud providers and fintechs—notably OCBC’s strategic Google Cloud partnership announced in 2020—accelerate digital feature delivery and API-led integration. They enable AI, analytics, KYC and cybersecurity capabilities and leverage sandboxes such as MAS’s 2016 framework and co-creation programs to cut time-to-market. Integration improves customer experience and reduces operating friction.

Insurance and asset management affiliates

OCBC’s insurance and asset-management affiliates, Great Eastern and Lion Global Investors, anchor bancassurance and investment offerings with integrated product design tailored to customer risk profiles and life-stage needs; Lion Global reported over S$85bn AUM in 2024 and Great Eastern remains a top regional insurer in market share.

- Joint product design → aligned to life-stage risk

- Distribution synergies → cross-sell uplift

- Shared consented data → better personalization

Correspondent and clearing banks

Global correspondent and clearing banks enable OCBC’s cross-border payments, trade finance and FX settlement, extending the bank’s reach into new markets and currencies and underpinning corporate treasury and trade corridors; OCBC operates in 18 markets as of 2024.

- Presence: 18 markets (2024)

- Function: reciprocal lines for liquidity and client servicing across major trade corridors

Bank partners with MAS, card networks and cloud allies to scale payments, digital AUM growth

OCBC partners with MAS for prudential supervision, payment rails (FAST, PayNow, RTGS) and resolution planning, supporting operations across 18 markets (2024).

Card networks (Visa, Mastercard, UnionPay) enable issuance and acceptance >90% globally; co-branding and fraud tech improve economics and security.

Tech alliances (Google Cloud since 2020), fintechs and bancassurance (Lion Global AUM S$85bn, 2024) accelerate digital products, analytics and cross-sell.

| Partner Type | Key Metric (2024) |

|---|---|

| Regulators | 18 markets |

| Card Networks | >90% global acceptance |

| Asset Mgmt | Lion Global S$85bn AUM |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to OCBC Bank, covering the nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—with real-world operations, competitive advantages, SWOT-linked insights and a polished format ideal for presentations, funding discussions, and strategic validation.

High-level view of OCBC Bank’s business model with editable cells, saving hours of formatting while condensing strategy into a digestible one-page snapshot for boardrooms, teams, and fast deliverables.

Activities

Deposit gathering and lending

OCBC mobilizes deposits and extends credit to retail, SME and corporate clients, pricing risk, structuring loans and managing collateral. Portfolio monitoring and credit governance maintain asset quality; OCBC reported a CET1 ratio of about 13% in 2024. Balance-sheet optimisation sustains margins and liquidity through funding diversification and active loan‑deposit management.

Risk, compliance, and governance

OCBC manages credit, market, liquidity and operational risk via centralized frameworks and limits; AML/CFT, sanctions screening and regulatory reporting are run group-wide to meet MAS and international standards. Internal audit and control functions safeguard financial integrity, while stress testing and ICAAP underpin capital planning in line with MAS 2024 supervisory expectations.

Digital platform development

OCBC continuously enhances mobile, web and API platforms to boost engagement across its over 9 million customers, focusing on secure, scalable microservices and frictionless user journeys. Robust data pipelines enable personalization and real-time insights, supporting targeted product offers and risk controls. Cyber defense and resilience—backed by continuous monitoring and incident response—remain core to platform strategy.

Wealth and advisory services

Advisors deliver portfolio construction, discretionary mandates and comprehensive financial planning across client segments; suitability and advisory frameworks govern recommendations and risk profiling. Product curation spans funds, bonds, equities, insurance and alternatives to meet return, income and legacy objectives. Regular client reviews realign portfolios to changing goals and market conditions.

- Advisory: portfolio construction, discretionary mandates, financial planning

- Products: funds, bonds, equities, insurance, alternatives

- Governance: suitability and advisory frameworks

- Client care: periodic reviews to align goals

Treasury and markets operations

Treasury manages funding, liquidity buffers and interest-rate risk with ALM aligning structural risks to OCBC’s strategy; Singapore/Basel III LCR minimum is 100%. Markets teams provide FX, rates and derivatives solutions to institutional and corporate clients. Trading and sales collaborate on execution and hedging to convert risk positions into client solutions.

- Top-three Singapore bank

- LCR regulatory floor 100%

- Focus: FX, rates, derivatives

- ALM aligns funding, liquidity, interest-rate profiles

Top-three Singapore bank: CET1 ~13%, customers >9M, LCR 100%

OCBC mobilizes deposits and originates and services loans across retail, SME and corporate segments, with tight credit governance and portfolio monitoring; reported CET1 ~13% in 2024. It manages liquidity and ALM to maintain a regulatory LCR floor of 100% and diversified funding. Digital platforms serve over 9 million customers, supporting product distribution, risk analytics and cyber resilience.

| Metric | 2024 |

|---|---|

| CET1 ratio | ~13% |

| Customers | >9 million |

| LCR | 100% regulatory floor |

| Market position | Top-three Singapore bank |

Full Document Unlocks After Purchase

Business Model Canvas

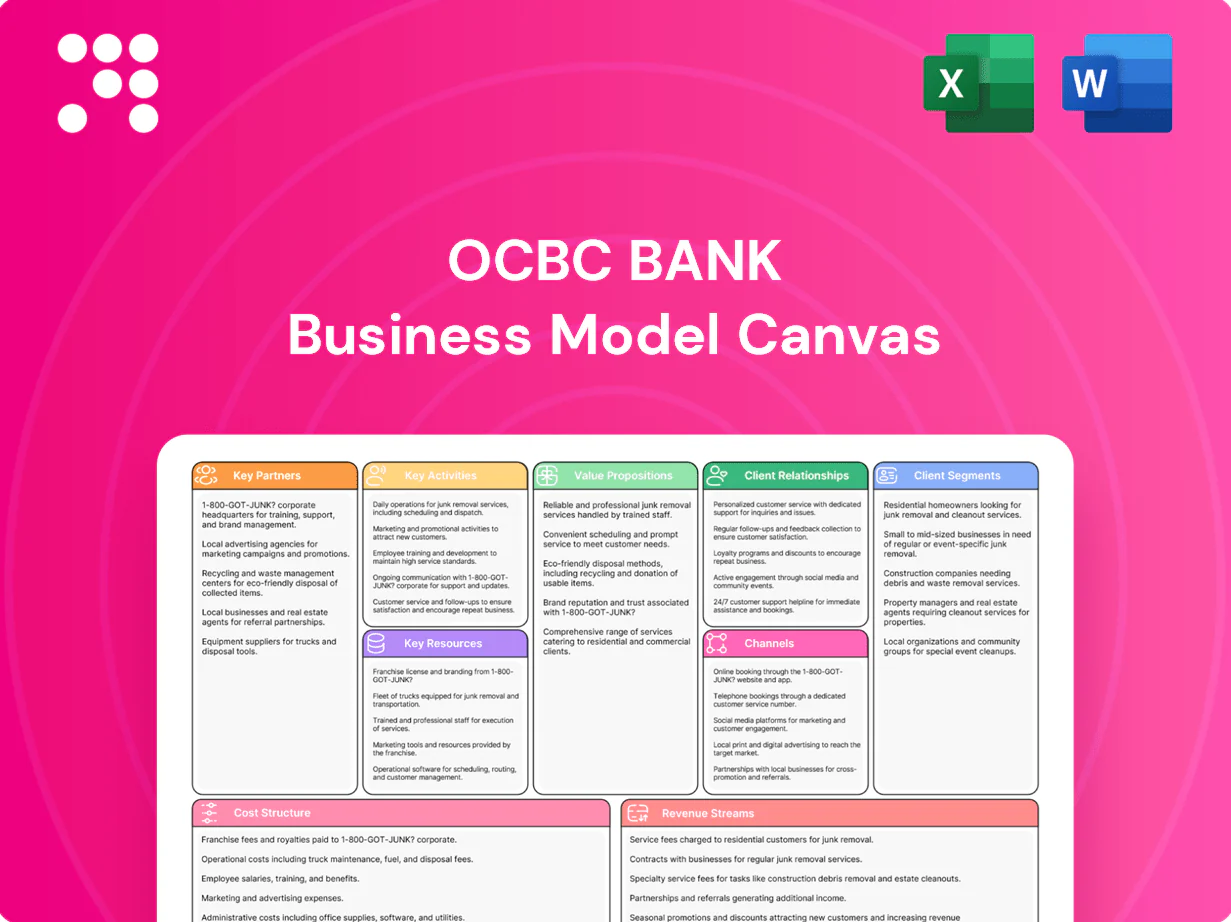

The OCBC Bank Business Model Canvas you’re previewing is the actual deliverable—not a mockup—and shows the same content and layout you’ll receive after purchase. Upon completion of your order you’ll get the full, ready-to-edit document in Word and Excel formats. No hidden pages, no fillers—what you see is what you’ll download and use.

Bank Business Model Canvas: customer value, distribution, and revenue for retail & corporate

Explore OCBC Bank’s Business Model Canvas to uncover how it creates customer value, scales distribution, and secures revenue across retail and corporate banking. This concise yet insightful snapshot highlights partnerships, channels, and cost drivers. Purchase the full Canvas for the complete nine-block analysis, editable templates, and strategic takeaways to inform investments or planning.

Partnerships

Regulators and central banks

OCBC collaborates closely with regulators such as MAS to maintain compliance and systemic stability; as one of Singapore's three domestic banks in 2024 it engages in MAS-led prudential supervision, resolution planning and licensing. These relationships enable access to payment rails and clearing systems including FAST, PayNow and MAS RTGS. Regular engagement builds credibility and customer trust.

Payment networks and processors

Partnerships with Visa, Mastercard, UnionPay and local schemes enable OCBC’s card issuance, merchant acquiring and cross-border rails, with global schemes covering over 90% of card acceptance worldwide. These partners supply advanced fraud detection and tokenization, boosting card security and digital wallet onboarding. Co-branding and interchange arrangements improve card economics and merchant margins, while joint initiatives accelerate contactless and wallet innovation across SEA markets.

Fintech and technology providers

Alliances with core banking vendors, cloud providers and fintechs—notably OCBC’s strategic Google Cloud partnership announced in 2020—accelerate digital feature delivery and API-led integration. They enable AI, analytics, KYC and cybersecurity capabilities and leverage sandboxes such as MAS’s 2016 framework and co-creation programs to cut time-to-market. Integration improves customer experience and reduces operating friction.

Insurance and asset management affiliates

OCBC’s insurance and asset-management affiliates, Great Eastern and Lion Global Investors, anchor bancassurance and investment offerings with integrated product design tailored to customer risk profiles and life-stage needs; Lion Global reported over S$85bn AUM in 2024 and Great Eastern remains a top regional insurer in market share.

- Joint product design → aligned to life-stage risk

- Distribution synergies → cross-sell uplift

- Shared consented data → better personalization

Correspondent and clearing banks

Global correspondent and clearing banks enable OCBC’s cross-border payments, trade finance and FX settlement, extending the bank’s reach into new markets and currencies and underpinning corporate treasury and trade corridors; OCBC operates in 18 markets as of 2024.

- Presence: 18 markets (2024)

- Function: reciprocal lines for liquidity and client servicing across major trade corridors

Bank partners with MAS, card networks and cloud allies to scale payments, digital AUM growth

OCBC partners with MAS for prudential supervision, payment rails (FAST, PayNow, RTGS) and resolution planning, supporting operations across 18 markets (2024).

Card networks (Visa, Mastercard, UnionPay) enable issuance and acceptance >90% globally; co-branding and fraud tech improve economics and security.

Tech alliances (Google Cloud since 2020), fintechs and bancassurance (Lion Global AUM S$85bn, 2024) accelerate digital products, analytics and cross-sell.

| Partner Type | Key Metric (2024) |

|---|---|

| Regulators | 18 markets |

| Card Networks | >90% global acceptance |

| Asset Mgmt | Lion Global S$85bn AUM |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to OCBC Bank, covering the nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—with real-world operations, competitive advantages, SWOT-linked insights and a polished format ideal for presentations, funding discussions, and strategic validation.

High-level view of OCBC Bank’s business model with editable cells, saving hours of formatting while condensing strategy into a digestible one-page snapshot for boardrooms, teams, and fast deliverables.

Activities

Deposit gathering and lending

OCBC mobilizes deposits and extends credit to retail, SME and corporate clients, pricing risk, structuring loans and managing collateral. Portfolio monitoring and credit governance maintain asset quality; OCBC reported a CET1 ratio of about 13% in 2024. Balance-sheet optimisation sustains margins and liquidity through funding diversification and active loan‑deposit management.

Risk, compliance, and governance

OCBC manages credit, market, liquidity and operational risk via centralized frameworks and limits; AML/CFT, sanctions screening and regulatory reporting are run group-wide to meet MAS and international standards. Internal audit and control functions safeguard financial integrity, while stress testing and ICAAP underpin capital planning in line with MAS 2024 supervisory expectations.

Digital platform development

OCBC continuously enhances mobile, web and API platforms to boost engagement across its over 9 million customers, focusing on secure, scalable microservices and frictionless user journeys. Robust data pipelines enable personalization and real-time insights, supporting targeted product offers and risk controls. Cyber defense and resilience—backed by continuous monitoring and incident response—remain core to platform strategy.

Wealth and advisory services

Advisors deliver portfolio construction, discretionary mandates and comprehensive financial planning across client segments; suitability and advisory frameworks govern recommendations and risk profiling. Product curation spans funds, bonds, equities, insurance and alternatives to meet return, income and legacy objectives. Regular client reviews realign portfolios to changing goals and market conditions.

- Advisory: portfolio construction, discretionary mandates, financial planning

- Products: funds, bonds, equities, insurance, alternatives

- Governance: suitability and advisory frameworks

- Client care: periodic reviews to align goals

Treasury and markets operations

Treasury manages funding, liquidity buffers and interest-rate risk with ALM aligning structural risks to OCBC’s strategy; Singapore/Basel III LCR minimum is 100%. Markets teams provide FX, rates and derivatives solutions to institutional and corporate clients. Trading and sales collaborate on execution and hedging to convert risk positions into client solutions.

- Top-three Singapore bank

- LCR regulatory floor 100%

- Focus: FX, rates, derivatives

- ALM aligns funding, liquidity, interest-rate profiles

Top-three Singapore bank: CET1 ~13%, customers >9M, LCR 100%

OCBC mobilizes deposits and originates and services loans across retail, SME and corporate segments, with tight credit governance and portfolio monitoring; reported CET1 ~13% in 2024. It manages liquidity and ALM to maintain a regulatory LCR floor of 100% and diversified funding. Digital platforms serve over 9 million customers, supporting product distribution, risk analytics and cyber resilience.

| Metric | 2024 |

|---|---|

| CET1 ratio | ~13% |

| Customers | >9 million |

| LCR | 100% regulatory floor |

| Market position | Top-three Singapore bank |

Full Document Unlocks After Purchase

Business Model Canvas

The OCBC Bank Business Model Canvas you’re previewing is the actual deliverable—not a mockup—and shows the same content and layout you’ll receive after purchase. Upon completion of your order you’ll get the full, ready-to-edit document in Word and Excel formats. No hidden pages, no fillers—what you see is what you’ll download and use.

Original: $10.00

-65%$10.00

$3.50Description

Bank Business Model Canvas: customer value, distribution, and revenue for retail & corporate

Explore OCBC Bank’s Business Model Canvas to uncover how it creates customer value, scales distribution, and secures revenue across retail and corporate banking. This concise yet insightful snapshot highlights partnerships, channels, and cost drivers. Purchase the full Canvas for the complete nine-block analysis, editable templates, and strategic takeaways to inform investments or planning.

Partnerships

Regulators and central banks

OCBC collaborates closely with regulators such as MAS to maintain compliance and systemic stability; as one of Singapore's three domestic banks in 2024 it engages in MAS-led prudential supervision, resolution planning and licensing. These relationships enable access to payment rails and clearing systems including FAST, PayNow and MAS RTGS. Regular engagement builds credibility and customer trust.

Payment networks and processors

Partnerships with Visa, Mastercard, UnionPay and local schemes enable OCBC’s card issuance, merchant acquiring and cross-border rails, with global schemes covering over 90% of card acceptance worldwide. These partners supply advanced fraud detection and tokenization, boosting card security and digital wallet onboarding. Co-branding and interchange arrangements improve card economics and merchant margins, while joint initiatives accelerate contactless and wallet innovation across SEA markets.

Fintech and technology providers

Alliances with core banking vendors, cloud providers and fintechs—notably OCBC’s strategic Google Cloud partnership announced in 2020—accelerate digital feature delivery and API-led integration. They enable AI, analytics, KYC and cybersecurity capabilities and leverage sandboxes such as MAS’s 2016 framework and co-creation programs to cut time-to-market. Integration improves customer experience and reduces operating friction.

Insurance and asset management affiliates

OCBC’s insurance and asset-management affiliates, Great Eastern and Lion Global Investors, anchor bancassurance and investment offerings with integrated product design tailored to customer risk profiles and life-stage needs; Lion Global reported over S$85bn AUM in 2024 and Great Eastern remains a top regional insurer in market share.

- Joint product design → aligned to life-stage risk

- Distribution synergies → cross-sell uplift

- Shared consented data → better personalization

Correspondent and clearing banks

Global correspondent and clearing banks enable OCBC’s cross-border payments, trade finance and FX settlement, extending the bank’s reach into new markets and currencies and underpinning corporate treasury and trade corridors; OCBC operates in 18 markets as of 2024.

- Presence: 18 markets (2024)

- Function: reciprocal lines for liquidity and client servicing across major trade corridors

Bank partners with MAS, card networks and cloud allies to scale payments, digital AUM growth

OCBC partners with MAS for prudential supervision, payment rails (FAST, PayNow, RTGS) and resolution planning, supporting operations across 18 markets (2024).

Card networks (Visa, Mastercard, UnionPay) enable issuance and acceptance >90% globally; co-branding and fraud tech improve economics and security.

Tech alliances (Google Cloud since 2020), fintechs and bancassurance (Lion Global AUM S$85bn, 2024) accelerate digital products, analytics and cross-sell.

| Partner Type | Key Metric (2024) |

|---|---|

| Regulators | 18 markets |

| Card Networks | >90% global acceptance |

| Asset Mgmt | Lion Global S$85bn AUM |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to OCBC Bank, covering the nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partnerships, and cost structure—with real-world operations, competitive advantages, SWOT-linked insights and a polished format ideal for presentations, funding discussions, and strategic validation.

High-level view of OCBC Bank’s business model with editable cells, saving hours of formatting while condensing strategy into a digestible one-page snapshot for boardrooms, teams, and fast deliverables.

Activities

Deposit gathering and lending

OCBC mobilizes deposits and extends credit to retail, SME and corporate clients, pricing risk, structuring loans and managing collateral. Portfolio monitoring and credit governance maintain asset quality; OCBC reported a CET1 ratio of about 13% in 2024. Balance-sheet optimisation sustains margins and liquidity through funding diversification and active loan‑deposit management.

Risk, compliance, and governance

OCBC manages credit, market, liquidity and operational risk via centralized frameworks and limits; AML/CFT, sanctions screening and regulatory reporting are run group-wide to meet MAS and international standards. Internal audit and control functions safeguard financial integrity, while stress testing and ICAAP underpin capital planning in line with MAS 2024 supervisory expectations.

Digital platform development

OCBC continuously enhances mobile, web and API platforms to boost engagement across its over 9 million customers, focusing on secure, scalable microservices and frictionless user journeys. Robust data pipelines enable personalization and real-time insights, supporting targeted product offers and risk controls. Cyber defense and resilience—backed by continuous monitoring and incident response—remain core to platform strategy.

Wealth and advisory services

Advisors deliver portfolio construction, discretionary mandates and comprehensive financial planning across client segments; suitability and advisory frameworks govern recommendations and risk profiling. Product curation spans funds, bonds, equities, insurance and alternatives to meet return, income and legacy objectives. Regular client reviews realign portfolios to changing goals and market conditions.

- Advisory: portfolio construction, discretionary mandates, financial planning

- Products: funds, bonds, equities, insurance, alternatives

- Governance: suitability and advisory frameworks

- Client care: periodic reviews to align goals

Treasury and markets operations

Treasury manages funding, liquidity buffers and interest-rate risk with ALM aligning structural risks to OCBC’s strategy; Singapore/Basel III LCR minimum is 100%. Markets teams provide FX, rates and derivatives solutions to institutional and corporate clients. Trading and sales collaborate on execution and hedging to convert risk positions into client solutions.

- Top-three Singapore bank

- LCR regulatory floor 100%

- Focus: FX, rates, derivatives

- ALM aligns funding, liquidity, interest-rate profiles

Top-three Singapore bank: CET1 ~13%, customers >9M, LCR 100%

OCBC mobilizes deposits and originates and services loans across retail, SME and corporate segments, with tight credit governance and portfolio monitoring; reported CET1 ~13% in 2024. It manages liquidity and ALM to maintain a regulatory LCR floor of 100% and diversified funding. Digital platforms serve over 9 million customers, supporting product distribution, risk analytics and cyber resilience.

| Metric | 2024 |

|---|---|

| CET1 ratio | ~13% |

| Customers | >9 million |

| LCR | 100% regulatory floor |

| Market position | Top-three Singapore bank |

Full Document Unlocks After Purchase

Business Model Canvas

The OCBC Bank Business Model Canvas you’re previewing is the actual deliverable—not a mockup—and shows the same content and layout you’ll receive after purchase. Upon completion of your order you’ll get the full, ready-to-edit document in Word and Excel formats. No hidden pages, no fillers—what you see is what you’ll download and use.