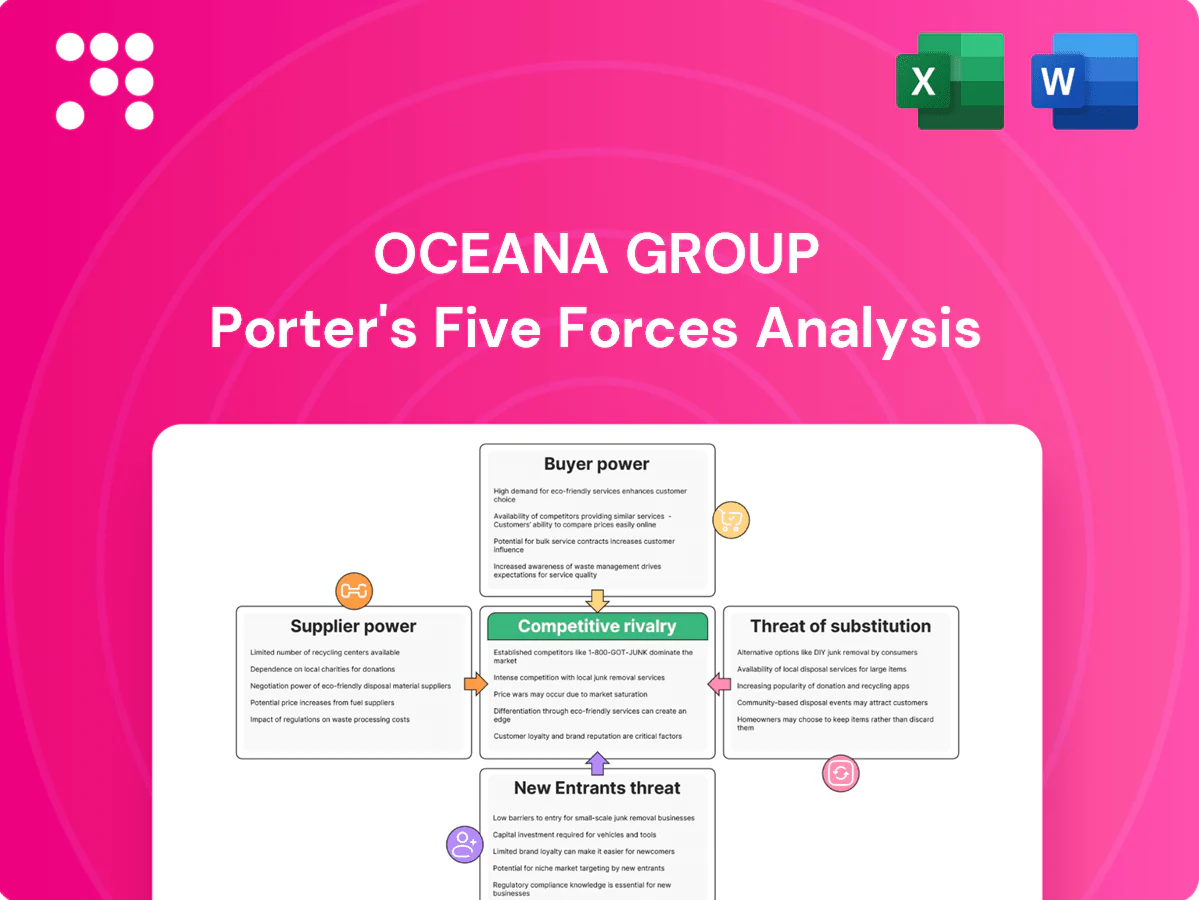

Oceana Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Oceana Group faces moderate supplier power, intense rivalry across seafood markets, and mounting substitute threats from alternative proteins, while regulatory barriers temper new entrants and buyers exert selective pressure on margins. This snapshot highlights critical competitive dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Oceana Group.

Suppliers Bargaining Power

Quota and license gatekeepers

Access to wild-catch is tightly controlled by government quota and license gatekeepers, concentrating supplier power and making availability sensitive to TAC decisions and renewals. Renewal risk and policy shifts can rapidly tighten supply and lift prices, while Oceana’s long-term rights reduce but do not remove regulatory leverage. Oceana’s strong compliance record and active stakeholder engagement mitigate dependency on quota holders.

Fuel and energy volatility

Fuel is a major cost input for Oceana, with Brent crude averaging about 85 USD/barrel in 2024, giving global suppliers pricing power; fuel can account for roughly 20–35% of vessel operating costs, so price spikes quickly compress margins and are hard to pass through in contracts. Hedging and fuel-efficient vessels soften shocks but do not eliminate exposure, while 2024 rises in energy tariffs and port fees increased localized supplier leverage.

Packaging and can supply

Packaging and can supply for Oceana is concentrated: the top three tinplate and can makers account for over 60% of regional supply, raising switching costs due to tight quality specs and limited alternatives. Concentration plus logistics bottlenecks tighten commercial terms, while long-term contracts and dual-sourcing—often covering 30–50% of annual volume—mitigate risk but lock in commitments. Inflation and 2024 freight volatility further amplify supplier bargaining power.

Skilled crews and processing labor

Specialized maritime and processing labor is scarce, giving crews and plant workers wage bargaining power; labor regulations and unions in South Africa and key markets further constrain cost flexibility. Training pipelines and retention programs reduce turnover risk but require capital and time. Automation lowers unit costs in high-volume lines but is limited across varied species and catch methods.

- Scarcity => higher wages

- Unions/regulations => reduced flexibility

- Training/retention => mitigates turnover

- Automation => partial cost relief

Cold chain and port infrastructure

Berths, cold storage and reefer logistics in key hubs are capacity-constrained, and congestion or outages shift pricing power to port and logistics suppliers through surcharges and priority fees; vertical integration into storage and logistics reduces dependency and exposure.

- Capacity constraints raise supplier leverage

- Surcharges/priorities boost operator margins

- Vertical integration lowers supplier risk

- Multiple ports improve negotiating leverage

Supplier power high: quota risk; fuel ~85 USD/bbl, OPEX 20–35%

Supplier power is high: quota/licence risk concentrates wild-catch; Oceana’s long-term rights mitigate but don’t eliminate regulatory leverage. Fuel (Brent ~85 USD/bbl in 2024) is 20–35% of vessel OPEX, increasing cost exposure. Packaging top‑3 >60% share; port/reefer constraints and scarce skilled labor sustain supplier bargaining power.

| Metric | 2024 |

|---|---|

| Brent | ~85 USD/bbl |

| Fuel % of OPEX | 20–35% |

| Top‑3 canmakers | >60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Oceana Group, evaluating supplier and buyer power, substitutes, and competitive rivalry; identifies disruptive threats and barriers protecting incumbency for use in investor materials, strategy decks, or academic projects.

Clear one-sheet summary of Oceana Group's Five Forces—instantly reveal supplier, buyer, and regulatory pressures to relieve strategic pain points and speed boardroom decisions.

Customers Bargaining Power

Concentrated retail chains

Concentrated retail chains consolidate volumes and extract price, promotion and payment concessions from suppliers, with South Africa’s top four grocers accounting for roughly 80% of grocery sales in 2024.

Rising private‑label penetration in canned fish intensifies price competition, but Oceana’s national brands and prominent shelf presence in core markets offer negotiating leverage.

Consistently high service levels and fill rates remain decisive to retain and expand listings with large chains.

Industrial feed customers

Industrial feed customers—large, price‑savvy aquafeed producers—buy fishmeal and fish oil on global markets and commonly benchmark to commodity indices, which erodes sellers pricing latitude. Aquaculture now accounts for roughly 50% of global seafood supply, concentrating buyer power. Quality specs and sustainability claims can fetch premia but are easily replicated; long‑term offtake contracts stabilize volumes while capping upside.

Low switching costs across species

Foodservice and distributors can swap among species and suppliers based on price and availability, keeping customer bargaining power high; frozen commodity differentiation is largely limited to grade and cut. Certifications like MSC—which has certified over 400 fisheries covering roughly 14% of global wild capture—narrow supplier pools but still permit switching within certified options. Value-added processing and traceability services increase stickiness by creating higher margins and operational dependency.

Certification and ESG demands

Buyers demand sustainability, traceability and social compliance, forcing Oceana to accept take-it-or-leave-it contract terms; retailer and foodservice audits shift certification and monitoring costs onto suppliers and raise Oceana’s fixed-cost base. Compliance unlocks access to premium channels but non-compliance risks delistings and margin compression for core product lines.

- Buyers: strong bargaining power

- Audit costs: shifted to suppliers

- Compliance: access + premiums

- Non-compliance: delisting, margin pressure

Currency and contract dynamics

Export buyers push for USD pricing and volume flexibility, shifting FX risk upstream; short-dated contracts limit pass-through of input spikes. Oceana used hedges and staggered pricing in 2024 to manage volatility and preserved a strategic customer mix to balance margin and volume stability.

- USD pricing shifts FX risk

- Short-dated contracts restrict pass-through

- Hedges + staggered pricing mitigate shocks

- Customer mix = margin vs volume trade-off

Concentrated buyers squeeze margins; exports, private labels and sustainability shift risk

Concentrated retailers (top four grocers ~80% of SA grocery sales in 2024) and industrial feed buyers (aquaculture ~50% of global supply) exert strong bargaining power, compressing prices and payment terms. Private‑label growth and USD export contracts shift FX and margin risk to Oceana, while sustainability audits raise fixed costs but enable premium channels.

| Metric | 2024 |

|---|---|

| Top‑4 grocer share (SA) | ~80% |

| Aquaculture share (global) | ~50% |

| MSC certified wild catch | ~14% |

Same Document Delivered

Oceana Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Oceana Group you'll receive immediately after purchase—no surprises, no placeholders. The report provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes and entry barriers, and clear strategic implications. It's professionally formatted and ready for immediate download and use. Purchase grants instant access to this same file.

Go Beyond the Preview—Access the Full Strategic Report

Oceana Group faces moderate supplier power, intense rivalry across seafood markets, and mounting substitute threats from alternative proteins, while regulatory barriers temper new entrants and buyers exert selective pressure on margins. This snapshot highlights critical competitive dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Oceana Group.

Suppliers Bargaining Power

Quota and license gatekeepers

Access to wild-catch is tightly controlled by government quota and license gatekeepers, concentrating supplier power and making availability sensitive to TAC decisions and renewals. Renewal risk and policy shifts can rapidly tighten supply and lift prices, while Oceana’s long-term rights reduce but do not remove regulatory leverage. Oceana’s strong compliance record and active stakeholder engagement mitigate dependency on quota holders.

Fuel and energy volatility

Fuel is a major cost input for Oceana, with Brent crude averaging about 85 USD/barrel in 2024, giving global suppliers pricing power; fuel can account for roughly 20–35% of vessel operating costs, so price spikes quickly compress margins and are hard to pass through in contracts. Hedging and fuel-efficient vessels soften shocks but do not eliminate exposure, while 2024 rises in energy tariffs and port fees increased localized supplier leverage.

Packaging and can supply

Packaging and can supply for Oceana is concentrated: the top three tinplate and can makers account for over 60% of regional supply, raising switching costs due to tight quality specs and limited alternatives. Concentration plus logistics bottlenecks tighten commercial terms, while long-term contracts and dual-sourcing—often covering 30–50% of annual volume—mitigate risk but lock in commitments. Inflation and 2024 freight volatility further amplify supplier bargaining power.

Skilled crews and processing labor

Specialized maritime and processing labor is scarce, giving crews and plant workers wage bargaining power; labor regulations and unions in South Africa and key markets further constrain cost flexibility. Training pipelines and retention programs reduce turnover risk but require capital and time. Automation lowers unit costs in high-volume lines but is limited across varied species and catch methods.

- Scarcity => higher wages

- Unions/regulations => reduced flexibility

- Training/retention => mitigates turnover

- Automation => partial cost relief

Cold chain and port infrastructure

Berths, cold storage and reefer logistics in key hubs are capacity-constrained, and congestion or outages shift pricing power to port and logistics suppliers through surcharges and priority fees; vertical integration into storage and logistics reduces dependency and exposure.

- Capacity constraints raise supplier leverage

- Surcharges/priorities boost operator margins

- Vertical integration lowers supplier risk

- Multiple ports improve negotiating leverage

Supplier power high: quota risk; fuel ~85 USD/bbl, OPEX 20–35%

Supplier power is high: quota/licence risk concentrates wild-catch; Oceana’s long-term rights mitigate but don’t eliminate regulatory leverage. Fuel (Brent ~85 USD/bbl in 2024) is 20–35% of vessel OPEX, increasing cost exposure. Packaging top‑3 >60% share; port/reefer constraints and scarce skilled labor sustain supplier bargaining power.

| Metric | 2024 |

|---|---|

| Brent | ~85 USD/bbl |

| Fuel % of OPEX | 20–35% |

| Top‑3 canmakers | >60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Oceana Group, evaluating supplier and buyer power, substitutes, and competitive rivalry; identifies disruptive threats and barriers protecting incumbency for use in investor materials, strategy decks, or academic projects.

Clear one-sheet summary of Oceana Group's Five Forces—instantly reveal supplier, buyer, and regulatory pressures to relieve strategic pain points and speed boardroom decisions.

Customers Bargaining Power

Concentrated retail chains

Concentrated retail chains consolidate volumes and extract price, promotion and payment concessions from suppliers, with South Africa’s top four grocers accounting for roughly 80% of grocery sales in 2024.

Rising private‑label penetration in canned fish intensifies price competition, but Oceana’s national brands and prominent shelf presence in core markets offer negotiating leverage.

Consistently high service levels and fill rates remain decisive to retain and expand listings with large chains.

Industrial feed customers

Industrial feed customers—large, price‑savvy aquafeed producers—buy fishmeal and fish oil on global markets and commonly benchmark to commodity indices, which erodes sellers pricing latitude. Aquaculture now accounts for roughly 50% of global seafood supply, concentrating buyer power. Quality specs and sustainability claims can fetch premia but are easily replicated; long‑term offtake contracts stabilize volumes while capping upside.

Low switching costs across species

Foodservice and distributors can swap among species and suppliers based on price and availability, keeping customer bargaining power high; frozen commodity differentiation is largely limited to grade and cut. Certifications like MSC—which has certified over 400 fisheries covering roughly 14% of global wild capture—narrow supplier pools but still permit switching within certified options. Value-added processing and traceability services increase stickiness by creating higher margins and operational dependency.

Certification and ESG demands

Buyers demand sustainability, traceability and social compliance, forcing Oceana to accept take-it-or-leave-it contract terms; retailer and foodservice audits shift certification and monitoring costs onto suppliers and raise Oceana’s fixed-cost base. Compliance unlocks access to premium channels but non-compliance risks delistings and margin compression for core product lines.

- Buyers: strong bargaining power

- Audit costs: shifted to suppliers

- Compliance: access + premiums

- Non-compliance: delisting, margin pressure

Currency and contract dynamics

Export buyers push for USD pricing and volume flexibility, shifting FX risk upstream; short-dated contracts limit pass-through of input spikes. Oceana used hedges and staggered pricing in 2024 to manage volatility and preserved a strategic customer mix to balance margin and volume stability.

- USD pricing shifts FX risk

- Short-dated contracts restrict pass-through

- Hedges + staggered pricing mitigate shocks

- Customer mix = margin vs volume trade-off

Concentrated buyers squeeze margins; exports, private labels and sustainability shift risk

Concentrated retailers (top four grocers ~80% of SA grocery sales in 2024) and industrial feed buyers (aquaculture ~50% of global supply) exert strong bargaining power, compressing prices and payment terms. Private‑label growth and USD export contracts shift FX and margin risk to Oceana, while sustainability audits raise fixed costs but enable premium channels.

| Metric | 2024 |

|---|---|

| Top‑4 grocer share (SA) | ~80% |

| Aquaculture share (global) | ~50% |

| MSC certified wild catch | ~14% |

Same Document Delivered

Oceana Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Oceana Group you'll receive immediately after purchase—no surprises, no placeholders. The report provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes and entry barriers, and clear strategic implications. It's professionally formatted and ready for immediate download and use. Purchase grants instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Oceana Group faces moderate supplier power, intense rivalry across seafood markets, and mounting substitute threats from alternative proteins, while regulatory barriers temper new entrants and buyers exert selective pressure on margins. This snapshot highlights critical competitive dynamics and strategic levers. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations tailored to Oceana Group.

Suppliers Bargaining Power

Quota and license gatekeepers

Access to wild-catch is tightly controlled by government quota and license gatekeepers, concentrating supplier power and making availability sensitive to TAC decisions and renewals. Renewal risk and policy shifts can rapidly tighten supply and lift prices, while Oceana’s long-term rights reduce but do not remove regulatory leverage. Oceana’s strong compliance record and active stakeholder engagement mitigate dependency on quota holders.

Fuel and energy volatility

Fuel is a major cost input for Oceana, with Brent crude averaging about 85 USD/barrel in 2024, giving global suppliers pricing power; fuel can account for roughly 20–35% of vessel operating costs, so price spikes quickly compress margins and are hard to pass through in contracts. Hedging and fuel-efficient vessels soften shocks but do not eliminate exposure, while 2024 rises in energy tariffs and port fees increased localized supplier leverage.

Packaging and can supply

Packaging and can supply for Oceana is concentrated: the top three tinplate and can makers account for over 60% of regional supply, raising switching costs due to tight quality specs and limited alternatives. Concentration plus logistics bottlenecks tighten commercial terms, while long-term contracts and dual-sourcing—often covering 30–50% of annual volume—mitigate risk but lock in commitments. Inflation and 2024 freight volatility further amplify supplier bargaining power.

Skilled crews and processing labor

Specialized maritime and processing labor is scarce, giving crews and plant workers wage bargaining power; labor regulations and unions in South Africa and key markets further constrain cost flexibility. Training pipelines and retention programs reduce turnover risk but require capital and time. Automation lowers unit costs in high-volume lines but is limited across varied species and catch methods.

- Scarcity => higher wages

- Unions/regulations => reduced flexibility

- Training/retention => mitigates turnover

- Automation => partial cost relief

Cold chain and port infrastructure

Berths, cold storage and reefer logistics in key hubs are capacity-constrained, and congestion or outages shift pricing power to port and logistics suppliers through surcharges and priority fees; vertical integration into storage and logistics reduces dependency and exposure.

- Capacity constraints raise supplier leverage

- Surcharges/priorities boost operator margins

- Vertical integration lowers supplier risk

- Multiple ports improve negotiating leverage

Supplier power high: quota risk; fuel ~85 USD/bbl, OPEX 20–35%

Supplier power is high: quota/licence risk concentrates wild-catch; Oceana’s long-term rights mitigate but don’t eliminate regulatory leverage. Fuel (Brent ~85 USD/bbl in 2024) is 20–35% of vessel OPEX, increasing cost exposure. Packaging top‑3 >60% share; port/reefer constraints and scarce skilled labor sustain supplier bargaining power.

| Metric | 2024 |

|---|---|

| Brent | ~85 USD/bbl |

| Fuel % of OPEX | 20–35% |

| Top‑3 canmakers | >60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Oceana Group, evaluating supplier and buyer power, substitutes, and competitive rivalry; identifies disruptive threats and barriers protecting incumbency for use in investor materials, strategy decks, or academic projects.

Clear one-sheet summary of Oceana Group's Five Forces—instantly reveal supplier, buyer, and regulatory pressures to relieve strategic pain points and speed boardroom decisions.

Customers Bargaining Power

Concentrated retail chains

Concentrated retail chains consolidate volumes and extract price, promotion and payment concessions from suppliers, with South Africa’s top four grocers accounting for roughly 80% of grocery sales in 2024.

Rising private‑label penetration in canned fish intensifies price competition, but Oceana’s national brands and prominent shelf presence in core markets offer negotiating leverage.

Consistently high service levels and fill rates remain decisive to retain and expand listings with large chains.

Industrial feed customers

Industrial feed customers—large, price‑savvy aquafeed producers—buy fishmeal and fish oil on global markets and commonly benchmark to commodity indices, which erodes sellers pricing latitude. Aquaculture now accounts for roughly 50% of global seafood supply, concentrating buyer power. Quality specs and sustainability claims can fetch premia but are easily replicated; long‑term offtake contracts stabilize volumes while capping upside.

Low switching costs across species

Foodservice and distributors can swap among species and suppliers based on price and availability, keeping customer bargaining power high; frozen commodity differentiation is largely limited to grade and cut. Certifications like MSC—which has certified over 400 fisheries covering roughly 14% of global wild capture—narrow supplier pools but still permit switching within certified options. Value-added processing and traceability services increase stickiness by creating higher margins and operational dependency.

Certification and ESG demands

Buyers demand sustainability, traceability and social compliance, forcing Oceana to accept take-it-or-leave-it contract terms; retailer and foodservice audits shift certification and monitoring costs onto suppliers and raise Oceana’s fixed-cost base. Compliance unlocks access to premium channels but non-compliance risks delistings and margin compression for core product lines.

- Buyers: strong bargaining power

- Audit costs: shifted to suppliers

- Compliance: access + premiums

- Non-compliance: delisting, margin pressure

Currency and contract dynamics

Export buyers push for USD pricing and volume flexibility, shifting FX risk upstream; short-dated contracts limit pass-through of input spikes. Oceana used hedges and staggered pricing in 2024 to manage volatility and preserved a strategic customer mix to balance margin and volume stability.

- USD pricing shifts FX risk

- Short-dated contracts restrict pass-through

- Hedges + staggered pricing mitigate shocks

- Customer mix = margin vs volume trade-off

Concentrated buyers squeeze margins; exports, private labels and sustainability shift risk

Concentrated retailers (top four grocers ~80% of SA grocery sales in 2024) and industrial feed buyers (aquaculture ~50% of global supply) exert strong bargaining power, compressing prices and payment terms. Private‑label growth and USD export contracts shift FX and margin risk to Oceana, while sustainability audits raise fixed costs but enable premium channels.

| Metric | 2024 |

|---|---|

| Top‑4 grocer share (SA) | ~80% |

| Aquaculture share (global) | ~50% |

| MSC certified wild catch | ~14% |

Same Document Delivered

Oceana Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Oceana Group you'll receive immediately after purchase—no surprises, no placeholders. The report provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of substitutes and entry barriers, and clear strategic implications. It's professionally formatted and ready for immediate download and use. Purchase grants instant access to this same file.