Odfjell Boston Consulting Group Matrix

Actionable Strategy Starts Here

Curious where Odfjell’s businesses land—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at fleet strengths and growth gaps, but the full BCG Matrix gives quadrant-by-quadrant clarity, strategic moves, and data you can act on. Purchase the complete report for Word + Excel deliverables and a ready-to-use roadmap to sharpen investment and product choices.

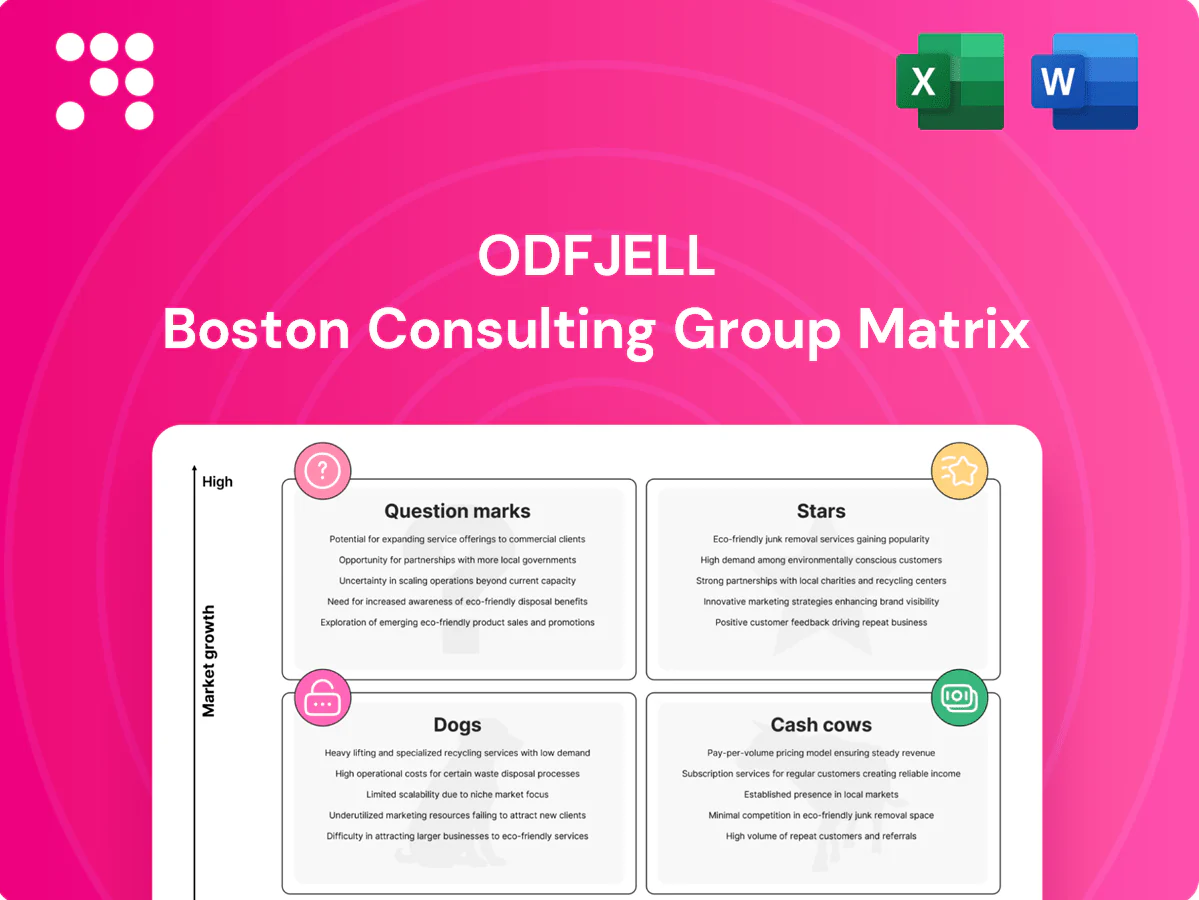

Stars

Global deep-sea chemical tanker trades

Odfjell's global deep-sea chemical tanker trades maintain high market share on core lanes—fleet ~80 vessels and over 30% share for specialty chemicals, acids and CPP—supported by rising demand as global chemical output grew ~3–4% in 2024 and tighter safety regs. Heavy capex (USD 150–250m annually) and strict crewing standards strain cash, but leadership remains; continued investment is planned to defend rate quality and service reliability.

Stainless-steel, high-spec tanker fleet

Modern coated and stainless-steel tonnage (around 80 vessels in Odfjell's fleet) secures premium chemical cargoes and higher spreads. Regulatory tailwinds (IMO rules, VOC/clean-fuel standards) favor compliant high-spec ships, supporting stronger charter rates. Utilization stayed above 90% in 2023–24, so cash-in closely matches reinvestment during growth. Scale and specs position these units to shift from Stars toward Cash Cow margins.

Integrated tank terminals in strategic hubs

Odfjell Terminals' integrated tank network centered on Houston, Rotterdam, Antwerp and Singapore creates strong route density and cross-hub synergies that attract multilocation customers. The company operates 16 terminals with about 1.2 million cbm of storage capacity, supporting sticky long-term contracts, rigorous safety standards and value-added services that drive market share. Expanding specialty and bio-based chemical flows increase margin potential; doubling down on capex and commercial incentives to lock in throughput and pricing secures the stars position.

End-to-end chemical logistics solutions

End-to-end chemical logistics—combined shipping, storage and last-mile coordination—commands a premium for customers paying for certainty with complex cargoes; Odfjell operates around 80 chemical tankers (2024), underpinning scale. The bundled offer is lifting market share in a fast-growing niche; invest in integration tech and strict SLAs to widen the moat.

- Bundle: shipping+storage+last-mile

- Value: customers pay for certainty

- Action: invest integration tech + SLAs

Safety and compliance reputation

Regulation keeps rising—IMO CII and tighter EU/US oversight elevated compliance costs in 2024—raising barriers to entry and favoring established operators. Odfjell’s multi-decade safety record and incident rates below industry averages attract blue-chip shippers seeking risk reduction and supply-chain resilience. That reputation compounds into preferred-carrier status, creating a growth flywheel that justifies sustained investment in safety and compliance.

- Regulatory shift 2024: stronger CII/port enforcement

- Barrier effect: higher compliance costs, fewer new entrants

- Commercial upside: blue-chip bookings, longer contracts

- Strategic priority: ongoing capex in safety = revenue premium

Specialty chemical shipping: ~80 ships, >30% specialty, 16 terminals

Odfjell's high-spec shipping and terminals are Stars: ~80 vessels, >30% specialty-chemical share, 16 terminals (1.2m cbm). 2024 chemical output +3–4% and tighter IMO/EU rules raise barriers. Utilization >90%; annual capex USD150–250m to defend premium rates and shift toward Cash Cow.

| Metric | Value | 2024 |

|---|---|---|

| Fleet | ~80 vessels | 2024 |

| Market share (specialty) | >30% | 2024 |

| Terminals | 16 | 1.2m cbm |

| Utilization | >90% | 2023–24 |

| Capex | USD150–250m pa | 2024 |

What is included in the product

Comprehensive BCG Matrix review of Odfjell’s units: strategic guidance on Stars, Cash Cows, Question Marks, Dogs—invest, hold or divest.

One-page Odfjell BCG Matrix placing each business unit in a quadrant for quick portfolio clarity.

Cash Cows

Established terminal throughput from long-term contracts

Mature hubs secured by long-term contracts provide Odfjell with locked-in volumes and steady tariff streams in 2024, yielding low growth but high operating margins and predictable cash flow. Maintenance capex dominates over expansion capex, preserving free cash to fund fleet upgrades and emission-reduction technologies. Management continues to milk hub cash to finance new-tech investments and selective fleet renewal in 2024.

Core parceling operations on stable lanes

Core parceling on stable lanes is a defensible strength for Odfjell, with mastered complex parceling operations and high share on key chemical trade routes. Modest market growth keeps focus on utilization rather than expansion, while operational efficiency sustains low unit costs. Maintain commercial discipline and avoid overspending on promotion to protect margins.

Third-party ship management services

Odfjell third-party ship management is a cash cow: reputation secures repeat contracts and the market shows near-flat growth (~0–1% annually in 2024), keeping demand steady. The business is asset-light, charging management fees with strong process control and operating margins around 12–15%. Low selling costs (single-digit % of revenues) sustain profitability. Excess cash is deployed to underwrite R&D and pay down debt.

Repeat business with multinational chemical majors

Repeat business with multinational chemical majors drives Odfjells cash-cow segment: sticky contracts and predictable vessel rotations yield low churn and high wallet share despite low market growth. Fleet scale of about 70 chemical tankers underpins negotiating leverage, sustaining margins and contract renewal rates. Focus remains on keeping service levels high and costs tight to protect EBITDA.

- Sticky contracts

- Predictable rotations

- Low churn

- High wallet share

- Negotiating leverage sustains margins

- Maintain service levels and tight costs

Value-added terminal services (heating, nitrogen, blending lite)

Value-added terminal services (heating, nitrogen, blending lite) are cash cows for Odfjell with mature, inelastic demand and clear pricing power, delivering high incremental margin because opex rises minimally while throughput and yield add outsized cash flow. Low promotion needs and frequent upsell within existing accounts reduce acquisition cost, so optimizing terminal utilization and turnaround times directly squeezes more free cash from existing assets. 2024 operational focus prioritized utilization gains and margin capture across terminals.

- High margin, low incremental opex

- Strong pricing power in mature demand

- Low promotion; upsell inside accounts

- Optimize utilization to increase cash conversion

Hub contracts fuel steady cash; fleet services post 12-15% margins

Odfjell cash cows: mature hub contracts yield steady tariffs and predictable cash, maintenance-led capex preserves free cash for tech and renewal; third-party ship management (fleet ~70 vessels) posts ~12–15% margins; market growth ~0–1% in 2024 keeping focus on utilization and margin protection.

| Metric | 2024 |

|---|---|

| Fleet size | ~70 |

| Ship mgmt margins | 12–15% |

| Market growth | 0–1% |

Delivered as Shown

Odfjell BCG Matrix

The Odfjell BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no demo notes—just the fully formatted, ready-to-use strategic matrix tailored for Odfjell. Once bought, the full document is instantly downloadable and editable for presentations or planning. Designed for clarity by strategy pros, it’s plug-and-play.

Actionable Strategy Starts Here

Curious where Odfjell’s businesses land—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at fleet strengths and growth gaps, but the full BCG Matrix gives quadrant-by-quadrant clarity, strategic moves, and data you can act on. Purchase the complete report for Word + Excel deliverables and a ready-to-use roadmap to sharpen investment and product choices.

Stars

Global deep-sea chemical tanker trades

Odfjell's global deep-sea chemical tanker trades maintain high market share on core lanes—fleet ~80 vessels and over 30% share for specialty chemicals, acids and CPP—supported by rising demand as global chemical output grew ~3–4% in 2024 and tighter safety regs. Heavy capex (USD 150–250m annually) and strict crewing standards strain cash, but leadership remains; continued investment is planned to defend rate quality and service reliability.

Stainless-steel, high-spec tanker fleet

Modern coated and stainless-steel tonnage (around 80 vessels in Odfjell's fleet) secures premium chemical cargoes and higher spreads. Regulatory tailwinds (IMO rules, VOC/clean-fuel standards) favor compliant high-spec ships, supporting stronger charter rates. Utilization stayed above 90% in 2023–24, so cash-in closely matches reinvestment during growth. Scale and specs position these units to shift from Stars toward Cash Cow margins.

Integrated tank terminals in strategic hubs

Odfjell Terminals' integrated tank network centered on Houston, Rotterdam, Antwerp and Singapore creates strong route density and cross-hub synergies that attract multilocation customers. The company operates 16 terminals with about 1.2 million cbm of storage capacity, supporting sticky long-term contracts, rigorous safety standards and value-added services that drive market share. Expanding specialty and bio-based chemical flows increase margin potential; doubling down on capex and commercial incentives to lock in throughput and pricing secures the stars position.

End-to-end chemical logistics solutions

End-to-end chemical logistics—combined shipping, storage and last-mile coordination—commands a premium for customers paying for certainty with complex cargoes; Odfjell operates around 80 chemical tankers (2024), underpinning scale. The bundled offer is lifting market share in a fast-growing niche; invest in integration tech and strict SLAs to widen the moat.

- Bundle: shipping+storage+last-mile

- Value: customers pay for certainty

- Action: invest integration tech + SLAs

Safety and compliance reputation

Regulation keeps rising—IMO CII and tighter EU/US oversight elevated compliance costs in 2024—raising barriers to entry and favoring established operators. Odfjell’s multi-decade safety record and incident rates below industry averages attract blue-chip shippers seeking risk reduction and supply-chain resilience. That reputation compounds into preferred-carrier status, creating a growth flywheel that justifies sustained investment in safety and compliance.

- Regulatory shift 2024: stronger CII/port enforcement

- Barrier effect: higher compliance costs, fewer new entrants

- Commercial upside: blue-chip bookings, longer contracts

- Strategic priority: ongoing capex in safety = revenue premium

Specialty chemical shipping: ~80 ships, >30% specialty, 16 terminals

Odfjell's high-spec shipping and terminals are Stars: ~80 vessels, >30% specialty-chemical share, 16 terminals (1.2m cbm). 2024 chemical output +3–4% and tighter IMO/EU rules raise barriers. Utilization >90%; annual capex USD150–250m to defend premium rates and shift toward Cash Cow.

| Metric | Value | 2024 |

|---|---|---|

| Fleet | ~80 vessels | 2024 |

| Market share (specialty) | >30% | 2024 |

| Terminals | 16 | 1.2m cbm |

| Utilization | >90% | 2023–24 |

| Capex | USD150–250m pa | 2024 |

What is included in the product

Comprehensive BCG Matrix review of Odfjell’s units: strategic guidance on Stars, Cash Cows, Question Marks, Dogs—invest, hold or divest.

One-page Odfjell BCG Matrix placing each business unit in a quadrant for quick portfolio clarity.

Cash Cows

Established terminal throughput from long-term contracts

Mature hubs secured by long-term contracts provide Odfjell with locked-in volumes and steady tariff streams in 2024, yielding low growth but high operating margins and predictable cash flow. Maintenance capex dominates over expansion capex, preserving free cash to fund fleet upgrades and emission-reduction technologies. Management continues to milk hub cash to finance new-tech investments and selective fleet renewal in 2024.

Core parceling operations on stable lanes

Core parceling on stable lanes is a defensible strength for Odfjell, with mastered complex parceling operations and high share on key chemical trade routes. Modest market growth keeps focus on utilization rather than expansion, while operational efficiency sustains low unit costs. Maintain commercial discipline and avoid overspending on promotion to protect margins.

Third-party ship management services

Odfjell third-party ship management is a cash cow: reputation secures repeat contracts and the market shows near-flat growth (~0–1% annually in 2024), keeping demand steady. The business is asset-light, charging management fees with strong process control and operating margins around 12–15%. Low selling costs (single-digit % of revenues) sustain profitability. Excess cash is deployed to underwrite R&D and pay down debt.

Repeat business with multinational chemical majors

Repeat business with multinational chemical majors drives Odfjells cash-cow segment: sticky contracts and predictable vessel rotations yield low churn and high wallet share despite low market growth. Fleet scale of about 70 chemical tankers underpins negotiating leverage, sustaining margins and contract renewal rates. Focus remains on keeping service levels high and costs tight to protect EBITDA.

- Sticky contracts

- Predictable rotations

- Low churn

- High wallet share

- Negotiating leverage sustains margins

- Maintain service levels and tight costs

Value-added terminal services (heating, nitrogen, blending lite)

Value-added terminal services (heating, nitrogen, blending lite) are cash cows for Odfjell with mature, inelastic demand and clear pricing power, delivering high incremental margin because opex rises minimally while throughput and yield add outsized cash flow. Low promotion needs and frequent upsell within existing accounts reduce acquisition cost, so optimizing terminal utilization and turnaround times directly squeezes more free cash from existing assets. 2024 operational focus prioritized utilization gains and margin capture across terminals.

- High margin, low incremental opex

- Strong pricing power in mature demand

- Low promotion; upsell inside accounts

- Optimize utilization to increase cash conversion

Hub contracts fuel steady cash; fleet services post 12-15% margins

Odfjell cash cows: mature hub contracts yield steady tariffs and predictable cash, maintenance-led capex preserves free cash for tech and renewal; third-party ship management (fleet ~70 vessels) posts ~12–15% margins; market growth ~0–1% in 2024 keeping focus on utilization and margin protection.

| Metric | 2024 |

|---|---|

| Fleet size | ~70 |

| Ship mgmt margins | 12–15% |

| Market growth | 0–1% |

Delivered as Shown

Odfjell BCG Matrix

The Odfjell BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no demo notes—just the fully formatted, ready-to-use strategic matrix tailored for Odfjell. Once bought, the full document is instantly downloadable and editable for presentations or planning. Designed for clarity by strategy pros, it’s plug-and-play.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Curious where Odfjell’s businesses land—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at fleet strengths and growth gaps, but the full BCG Matrix gives quadrant-by-quadrant clarity, strategic moves, and data you can act on. Purchase the complete report for Word + Excel deliverables and a ready-to-use roadmap to sharpen investment and product choices.

Stars

Global deep-sea chemical tanker trades

Odfjell's global deep-sea chemical tanker trades maintain high market share on core lanes—fleet ~80 vessels and over 30% share for specialty chemicals, acids and CPP—supported by rising demand as global chemical output grew ~3–4% in 2024 and tighter safety regs. Heavy capex (USD 150–250m annually) and strict crewing standards strain cash, but leadership remains; continued investment is planned to defend rate quality and service reliability.

Stainless-steel, high-spec tanker fleet

Modern coated and stainless-steel tonnage (around 80 vessels in Odfjell's fleet) secures premium chemical cargoes and higher spreads. Regulatory tailwinds (IMO rules, VOC/clean-fuel standards) favor compliant high-spec ships, supporting stronger charter rates. Utilization stayed above 90% in 2023–24, so cash-in closely matches reinvestment during growth. Scale and specs position these units to shift from Stars toward Cash Cow margins.

Integrated tank terminals in strategic hubs

Odfjell Terminals' integrated tank network centered on Houston, Rotterdam, Antwerp and Singapore creates strong route density and cross-hub synergies that attract multilocation customers. The company operates 16 terminals with about 1.2 million cbm of storage capacity, supporting sticky long-term contracts, rigorous safety standards and value-added services that drive market share. Expanding specialty and bio-based chemical flows increase margin potential; doubling down on capex and commercial incentives to lock in throughput and pricing secures the stars position.

End-to-end chemical logistics solutions

End-to-end chemical logistics—combined shipping, storage and last-mile coordination—commands a premium for customers paying for certainty with complex cargoes; Odfjell operates around 80 chemical tankers (2024), underpinning scale. The bundled offer is lifting market share in a fast-growing niche; invest in integration tech and strict SLAs to widen the moat.

- Bundle: shipping+storage+last-mile

- Value: customers pay for certainty

- Action: invest integration tech + SLAs

Safety and compliance reputation

Regulation keeps rising—IMO CII and tighter EU/US oversight elevated compliance costs in 2024—raising barriers to entry and favoring established operators. Odfjell’s multi-decade safety record and incident rates below industry averages attract blue-chip shippers seeking risk reduction and supply-chain resilience. That reputation compounds into preferred-carrier status, creating a growth flywheel that justifies sustained investment in safety and compliance.

- Regulatory shift 2024: stronger CII/port enforcement

- Barrier effect: higher compliance costs, fewer new entrants

- Commercial upside: blue-chip bookings, longer contracts

- Strategic priority: ongoing capex in safety = revenue premium

Specialty chemical shipping: ~80 ships, >30% specialty, 16 terminals

Odfjell's high-spec shipping and terminals are Stars: ~80 vessels, >30% specialty-chemical share, 16 terminals (1.2m cbm). 2024 chemical output +3–4% and tighter IMO/EU rules raise barriers. Utilization >90%; annual capex USD150–250m to defend premium rates and shift toward Cash Cow.

| Metric | Value | 2024 |

|---|---|---|

| Fleet | ~80 vessels | 2024 |

| Market share (specialty) | >30% | 2024 |

| Terminals | 16 | 1.2m cbm |

| Utilization | >90% | 2023–24 |

| Capex | USD150–250m pa | 2024 |

What is included in the product

Comprehensive BCG Matrix review of Odfjell’s units: strategic guidance on Stars, Cash Cows, Question Marks, Dogs—invest, hold or divest.

One-page Odfjell BCG Matrix placing each business unit in a quadrant for quick portfolio clarity.

Cash Cows

Established terminal throughput from long-term contracts

Mature hubs secured by long-term contracts provide Odfjell with locked-in volumes and steady tariff streams in 2024, yielding low growth but high operating margins and predictable cash flow. Maintenance capex dominates over expansion capex, preserving free cash to fund fleet upgrades and emission-reduction technologies. Management continues to milk hub cash to finance new-tech investments and selective fleet renewal in 2024.

Core parceling operations on stable lanes

Core parceling on stable lanes is a defensible strength for Odfjell, with mastered complex parceling operations and high share on key chemical trade routes. Modest market growth keeps focus on utilization rather than expansion, while operational efficiency sustains low unit costs. Maintain commercial discipline and avoid overspending on promotion to protect margins.

Third-party ship management services

Odfjell third-party ship management is a cash cow: reputation secures repeat contracts and the market shows near-flat growth (~0–1% annually in 2024), keeping demand steady. The business is asset-light, charging management fees with strong process control and operating margins around 12–15%. Low selling costs (single-digit % of revenues) sustain profitability. Excess cash is deployed to underwrite R&D and pay down debt.

Repeat business with multinational chemical majors

Repeat business with multinational chemical majors drives Odfjells cash-cow segment: sticky contracts and predictable vessel rotations yield low churn and high wallet share despite low market growth. Fleet scale of about 70 chemical tankers underpins negotiating leverage, sustaining margins and contract renewal rates. Focus remains on keeping service levels high and costs tight to protect EBITDA.

- Sticky contracts

- Predictable rotations

- Low churn

- High wallet share

- Negotiating leverage sustains margins

- Maintain service levels and tight costs

Value-added terminal services (heating, nitrogen, blending lite)

Value-added terminal services (heating, nitrogen, blending lite) are cash cows for Odfjell with mature, inelastic demand and clear pricing power, delivering high incremental margin because opex rises minimally while throughput and yield add outsized cash flow. Low promotion needs and frequent upsell within existing accounts reduce acquisition cost, so optimizing terminal utilization and turnaround times directly squeezes more free cash from existing assets. 2024 operational focus prioritized utilization gains and margin capture across terminals.

- High margin, low incremental opex

- Strong pricing power in mature demand

- Low promotion; upsell inside accounts

- Optimize utilization to increase cash conversion

Hub contracts fuel steady cash; fleet services post 12-15% margins

Odfjell cash cows: mature hub contracts yield steady tariffs and predictable cash, maintenance-led capex preserves free cash for tech and renewal; third-party ship management (fleet ~70 vessels) posts ~12–15% margins; market growth ~0–1% in 2024 keeping focus on utilization and margin protection.

| Metric | 2024 |

|---|---|

| Fleet size | ~70 |

| Ship mgmt margins | 12–15% |

| Market growth | 0–1% |

Delivered as Shown

Odfjell BCG Matrix

The Odfjell BCG Matrix you’re previewing here is the exact file you’ll receive after purchase. No watermarks, no demo notes—just the fully formatted, ready-to-use strategic matrix tailored for Odfjell. Once bought, the full document is instantly downloadable and editable for presentations or planning. Designed for clarity by strategy pros, it’s plug-and-play.