Odontoprev SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Odontoprev’s SWOT snapshot highlights robust market share, integration synergies, and regulatory exposures shaping near-term performance. Explore competitive strengths, operational risks, and growth levers across segments. Purchase the full SWOT to get a research-backed, editable Word report plus Excel matrix—ready for investor presentations and strategic planning.

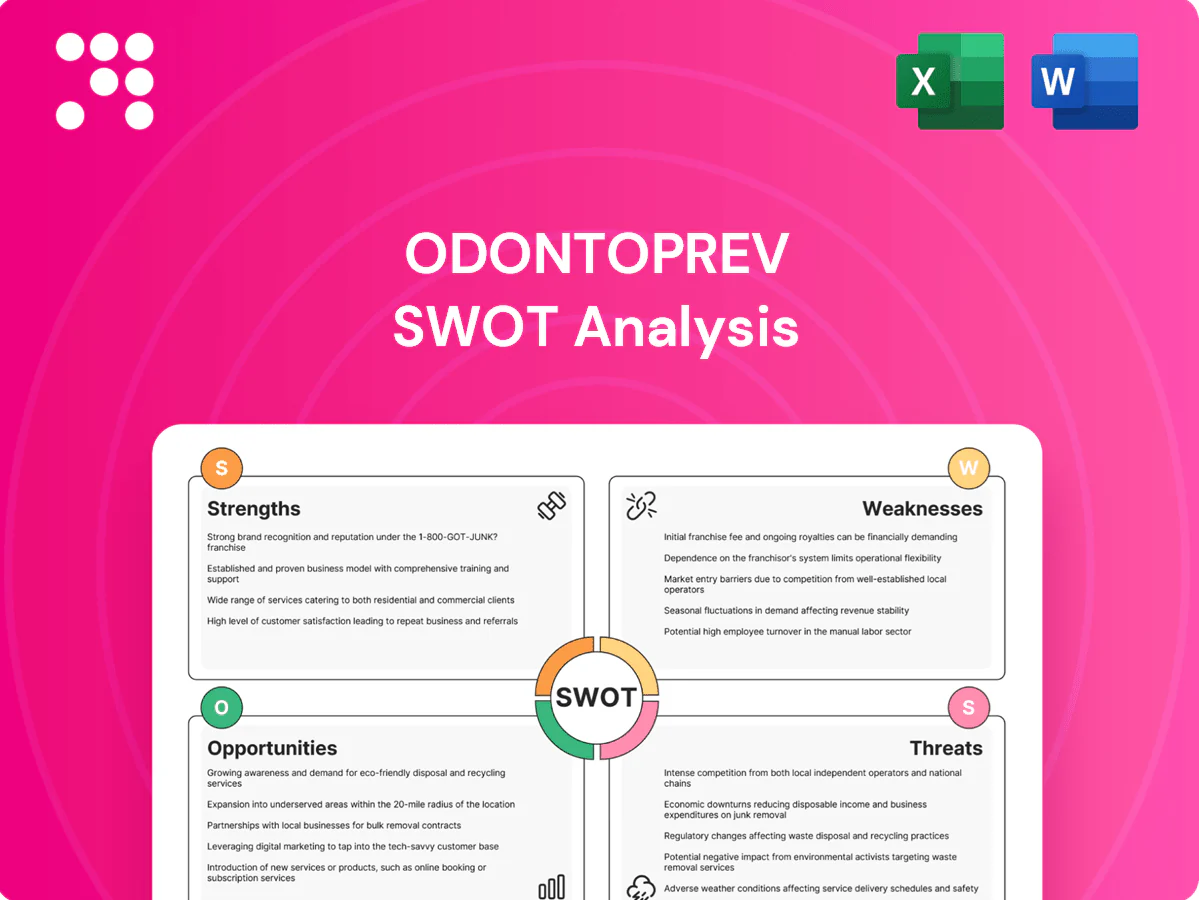

Strengths

Market leader in Brazilian dental benefits

OdontoPrev holds a leading share in Brazil's dental benefits market, with roughly 40% market share and over 7 million beneficiaries per ANS 2024, giving scale advantages in distribution, brand recognition and negotiating power. Leadership fosters trust among corporate buyers and brokers, improving tender win rates and retention. Scale also spreads risk across diverse groups and helps stabilize margins through economic cycles.

Extensive accredited dentist network

Odontoprev's extensive, accredited network—22,000+ dentists across more than 2,700 municipalities—boosts plan attractiveness by offering convenient access and vetted quality. Dense coverage lowers member travel time and supports higher preventive-care utilization, reflected in company-reported increases in routine visits after network expansion. Strong provider relationships enable competitive fee schedules and serve as a key differentiator versus smaller rivals.

Asset-light, scalable plan-management model

Managing plans rather than owning clinics keeps Odontoprev capital intensity low, supporting strong cash conversion and operating margins; the company serves over 10 million beneficiaries, enabling scale without proportional fixed costs. This asset-light model boosts return on invested capital versus asset-heavy peers and lowers incremental unit economics as membership grows. It also enables rapid, low-cost product rollout across segments, accelerating market penetration.

Deep corporate and channel partnerships

Deep corporate and channel partnerships anchor steady group membership through established ties with employers, brokers and bancassurance partners, while payroll deduction materially improves collection efficiency and retention. These relationships lower customer acquisition cost versus purely direct channels and co-branded offerings enable targeted expansion into new demographics.

- Employer & broker distribution

- Payroll deduction = higher retention

- Lower CAC vs direct

- Co-branded reach expansion

Data-driven underwriting and cost control

Claims analytics enable pricing by segment and plan design, improving margin capture and mix management. Utilization monitoring curtails fraud, waste and abuse, tightening short-term claims volatility. Preventive-care programs reduce long-term claims ratios by lowering incidence of high-cost procedures. Actuarial discipline sustains stable loss ratios and more predictable cash flows.

- Claims analytics: segment pricing

- Utilization monitoring: fraud control

- Preventive care: lower long-term claims

- Actuarial discipline: stable loss ratios

Dental plan leader: ~40% market share, 7.0M+ beneficiaries

OdontoPrev holds ~40% market share with 7.0+ million beneficiaries (ANS 2024), giving distribution scale, brand strength and negotiating leverage. A 22,000+ dentist network across 2,700+ municipalities and asset-light plan management drive low capital intensity and high cash conversion. Strong employer, broker and payroll channels lower CAC and boost retention, while claims analytics and preventive programs sustain stable loss ratios.

| Metric | Value (2024) |

|---|---|

| Market share | ~40% |

| Beneficiaries (ANS) | 7.0M+ |

| Network dentists | 22,000+ |

| Municipalities | 2,700+ |

What is included in the product

Provides a clear SWOT framework that maps Odontoprev’s internal capabilities, operational weaknesses, market opportunities, and external threats to its strategic growth and competitive position.

Provides a concise SWOT matrix for Odontoprev that quickly identifies strengths, weaknesses, opportunities and threats to relieve strategic uncertainty and align stakeholders.

Weaknesses

High exposure to Brazil-only market

Odontoprev derives over 95% of revenue from the Brazil market, tying growth and risk to Brazil’s macro and regulatory backdrop. Brazil’s IPCA inflation ran about 4.4% in 2024, and BRL volatility can erode margins and pricing power. Limited geographic diversification reduces resilience to country shocks, and meaningful expansion beyond Brazil would demand new distribution, compliance and clinical capabilities.

Dependence on employer-sponsored demand

Odontoprev reported about 10.6 million beneficiaries at end-2024, with employer-sponsored corporate plans comprising roughly two-thirds of that base, concentrating demand risk.

Employment cycles and headcount reductions—heightened during the 2023–24 slowdown—have driven episodic spikes in churn, compressing lifetime value.

Negotiated group pricing for large employers pressures average revenue per user, so management is expanding into SMEs and retail to diversify—a strategy that increases customer acquisition costs and margin pressure.

Price-sensitive, commoditized product perception

Odontoprev (ODPV3) competes in a market where buyers often compare dental benefits mainly by price and network size, intensifying tender competition and margin compression. Limited product differentiation contributes to higher churn at renewal, with Brazil's dental beneficiary base near 24 million (ANS 2024) increasing buyer leverage. Communicating value beyond basic coverage remains a persistent challenge.

Reliance on third-party distribution

Dependence on banks, brokers and partners gives intermediaries strong bargaining power over commissions and product placement, risking margin pressure; Odontoprev serves about 10.5 million beneficiaries (2024), intensifying reliance on these channels. Channel conflict can undermine direct-to-consumer initiatives, partners may deprioritize dental and delay access to niche segments, and end-customer insights are often filtered through intermediaries.

- Intermediary bargaining power

- Channel conflict vs D2C

- Slowed niche access

- Filtered customer visibility

Limited brand engagement with end users

Members mainly interact with dentists rather than Odontoprev, meaning low-touch engagement limits cross-sell and loyalty; perceived value often appears only at claim moments. With roughly 10.5 million beneficiaries in 2024, missed digital touchpoints constrain lifetime value and require sustained capex to build effective omni-channel engagement.

- Low direct brand contact

- Reduced cross-sell/loyalty

- Value visible at claims

- Needs sustained digital investment

Brazil dental risk: 10.6m members, employer-dependent and macro-sensitive

Odontoprev is highly Brazil-concentrated (>95% revenues) exposing it to local macro, regulatory and BRL volatility (IPCA 2024 ~4.4%).

Beneficiaries ~10.6m end-2024, ~66% employer-sponsored, increasing churn sensitivity to employment cycles.

High intermediary power and low direct member contact compress ARPU and raise digital investment needs.

| Metric | Value (2024) |

|---|---|

| Beneficiaries | 10.6m |

| Brazil revenue share | >95% |

| Employer share | ~66% |

| Brazil dental base (ANS) | ~24m |

| IPCA | 4.4% |

Preview Before You Purchase

Odontoprev SWOT Analysis

This preview is a direct excerpt from the Odontoprev SWOT analysis you’ll receive upon purchase—no placeholders or samples. The full document is professional, editable and structured for immediate use. Buy to unlock the complete, detailed report.

Dive Deeper Into the Company’s Strategic Blueprint

Odontoprev’s SWOT snapshot highlights robust market share, integration synergies, and regulatory exposures shaping near-term performance. Explore competitive strengths, operational risks, and growth levers across segments. Purchase the full SWOT to get a research-backed, editable Word report plus Excel matrix—ready for investor presentations and strategic planning.

Strengths

Market leader in Brazilian dental benefits

OdontoPrev holds a leading share in Brazil's dental benefits market, with roughly 40% market share and over 7 million beneficiaries per ANS 2024, giving scale advantages in distribution, brand recognition and negotiating power. Leadership fosters trust among corporate buyers and brokers, improving tender win rates and retention. Scale also spreads risk across diverse groups and helps stabilize margins through economic cycles.

Extensive accredited dentist network

Odontoprev's extensive, accredited network—22,000+ dentists across more than 2,700 municipalities—boosts plan attractiveness by offering convenient access and vetted quality. Dense coverage lowers member travel time and supports higher preventive-care utilization, reflected in company-reported increases in routine visits after network expansion. Strong provider relationships enable competitive fee schedules and serve as a key differentiator versus smaller rivals.

Asset-light, scalable plan-management model

Managing plans rather than owning clinics keeps Odontoprev capital intensity low, supporting strong cash conversion and operating margins; the company serves over 10 million beneficiaries, enabling scale without proportional fixed costs. This asset-light model boosts return on invested capital versus asset-heavy peers and lowers incremental unit economics as membership grows. It also enables rapid, low-cost product rollout across segments, accelerating market penetration.

Deep corporate and channel partnerships

Deep corporate and channel partnerships anchor steady group membership through established ties with employers, brokers and bancassurance partners, while payroll deduction materially improves collection efficiency and retention. These relationships lower customer acquisition cost versus purely direct channels and co-branded offerings enable targeted expansion into new demographics.

- Employer & broker distribution

- Payroll deduction = higher retention

- Lower CAC vs direct

- Co-branded reach expansion

Data-driven underwriting and cost control

Claims analytics enable pricing by segment and plan design, improving margin capture and mix management. Utilization monitoring curtails fraud, waste and abuse, tightening short-term claims volatility. Preventive-care programs reduce long-term claims ratios by lowering incidence of high-cost procedures. Actuarial discipline sustains stable loss ratios and more predictable cash flows.

- Claims analytics: segment pricing

- Utilization monitoring: fraud control

- Preventive care: lower long-term claims

- Actuarial discipline: stable loss ratios

Dental plan leader: ~40% market share, 7.0M+ beneficiaries

OdontoPrev holds ~40% market share with 7.0+ million beneficiaries (ANS 2024), giving distribution scale, brand strength and negotiating leverage. A 22,000+ dentist network across 2,700+ municipalities and asset-light plan management drive low capital intensity and high cash conversion. Strong employer, broker and payroll channels lower CAC and boost retention, while claims analytics and preventive programs sustain stable loss ratios.

| Metric | Value (2024) |

|---|---|

| Market share | ~40% |

| Beneficiaries (ANS) | 7.0M+ |

| Network dentists | 22,000+ |

| Municipalities | 2,700+ |

What is included in the product

Provides a clear SWOT framework that maps Odontoprev’s internal capabilities, operational weaknesses, market opportunities, and external threats to its strategic growth and competitive position.

Provides a concise SWOT matrix for Odontoprev that quickly identifies strengths, weaknesses, opportunities and threats to relieve strategic uncertainty and align stakeholders.

Weaknesses

High exposure to Brazil-only market

Odontoprev derives over 95% of revenue from the Brazil market, tying growth and risk to Brazil’s macro and regulatory backdrop. Brazil’s IPCA inflation ran about 4.4% in 2024, and BRL volatility can erode margins and pricing power. Limited geographic diversification reduces resilience to country shocks, and meaningful expansion beyond Brazil would demand new distribution, compliance and clinical capabilities.

Dependence on employer-sponsored demand

Odontoprev reported about 10.6 million beneficiaries at end-2024, with employer-sponsored corporate plans comprising roughly two-thirds of that base, concentrating demand risk.

Employment cycles and headcount reductions—heightened during the 2023–24 slowdown—have driven episodic spikes in churn, compressing lifetime value.

Negotiated group pricing for large employers pressures average revenue per user, so management is expanding into SMEs and retail to diversify—a strategy that increases customer acquisition costs and margin pressure.

Price-sensitive, commoditized product perception

Odontoprev (ODPV3) competes in a market where buyers often compare dental benefits mainly by price and network size, intensifying tender competition and margin compression. Limited product differentiation contributes to higher churn at renewal, with Brazil's dental beneficiary base near 24 million (ANS 2024) increasing buyer leverage. Communicating value beyond basic coverage remains a persistent challenge.

Reliance on third-party distribution

Dependence on banks, brokers and partners gives intermediaries strong bargaining power over commissions and product placement, risking margin pressure; Odontoprev serves about 10.5 million beneficiaries (2024), intensifying reliance on these channels. Channel conflict can undermine direct-to-consumer initiatives, partners may deprioritize dental and delay access to niche segments, and end-customer insights are often filtered through intermediaries.

- Intermediary bargaining power

- Channel conflict vs D2C

- Slowed niche access

- Filtered customer visibility

Limited brand engagement with end users

Members mainly interact with dentists rather than Odontoprev, meaning low-touch engagement limits cross-sell and loyalty; perceived value often appears only at claim moments. With roughly 10.5 million beneficiaries in 2024, missed digital touchpoints constrain lifetime value and require sustained capex to build effective omni-channel engagement.

- Low direct brand contact

- Reduced cross-sell/loyalty

- Value visible at claims

- Needs sustained digital investment

Brazil dental risk: 10.6m members, employer-dependent and macro-sensitive

Odontoprev is highly Brazil-concentrated (>95% revenues) exposing it to local macro, regulatory and BRL volatility (IPCA 2024 ~4.4%).

Beneficiaries ~10.6m end-2024, ~66% employer-sponsored, increasing churn sensitivity to employment cycles.

High intermediary power and low direct member contact compress ARPU and raise digital investment needs.

| Metric | Value (2024) |

|---|---|

| Beneficiaries | 10.6m |

| Brazil revenue share | >95% |

| Employer share | ~66% |

| Brazil dental base (ANS) | ~24m |

| IPCA | 4.4% |

Preview Before You Purchase

Odontoprev SWOT Analysis

This preview is a direct excerpt from the Odontoprev SWOT analysis you’ll receive upon purchase—no placeholders or samples. The full document is professional, editable and structured for immediate use. Buy to unlock the complete, detailed report.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Odontoprev’s SWOT snapshot highlights robust market share, integration synergies, and regulatory exposures shaping near-term performance. Explore competitive strengths, operational risks, and growth levers across segments. Purchase the full SWOT to get a research-backed, editable Word report plus Excel matrix—ready for investor presentations and strategic planning.

Strengths

Market leader in Brazilian dental benefits

OdontoPrev holds a leading share in Brazil's dental benefits market, with roughly 40% market share and over 7 million beneficiaries per ANS 2024, giving scale advantages in distribution, brand recognition and negotiating power. Leadership fosters trust among corporate buyers and brokers, improving tender win rates and retention. Scale also spreads risk across diverse groups and helps stabilize margins through economic cycles.

Extensive accredited dentist network

Odontoprev's extensive, accredited network—22,000+ dentists across more than 2,700 municipalities—boosts plan attractiveness by offering convenient access and vetted quality. Dense coverage lowers member travel time and supports higher preventive-care utilization, reflected in company-reported increases in routine visits after network expansion. Strong provider relationships enable competitive fee schedules and serve as a key differentiator versus smaller rivals.

Asset-light, scalable plan-management model

Managing plans rather than owning clinics keeps Odontoprev capital intensity low, supporting strong cash conversion and operating margins; the company serves over 10 million beneficiaries, enabling scale without proportional fixed costs. This asset-light model boosts return on invested capital versus asset-heavy peers and lowers incremental unit economics as membership grows. It also enables rapid, low-cost product rollout across segments, accelerating market penetration.

Deep corporate and channel partnerships

Deep corporate and channel partnerships anchor steady group membership through established ties with employers, brokers and bancassurance partners, while payroll deduction materially improves collection efficiency and retention. These relationships lower customer acquisition cost versus purely direct channels and co-branded offerings enable targeted expansion into new demographics.

- Employer & broker distribution

- Payroll deduction = higher retention

- Lower CAC vs direct

- Co-branded reach expansion

Data-driven underwriting and cost control

Claims analytics enable pricing by segment and plan design, improving margin capture and mix management. Utilization monitoring curtails fraud, waste and abuse, tightening short-term claims volatility. Preventive-care programs reduce long-term claims ratios by lowering incidence of high-cost procedures. Actuarial discipline sustains stable loss ratios and more predictable cash flows.

- Claims analytics: segment pricing

- Utilization monitoring: fraud control

- Preventive care: lower long-term claims

- Actuarial discipline: stable loss ratios

Dental plan leader: ~40% market share, 7.0M+ beneficiaries

OdontoPrev holds ~40% market share with 7.0+ million beneficiaries (ANS 2024), giving distribution scale, brand strength and negotiating leverage. A 22,000+ dentist network across 2,700+ municipalities and asset-light plan management drive low capital intensity and high cash conversion. Strong employer, broker and payroll channels lower CAC and boost retention, while claims analytics and preventive programs sustain stable loss ratios.

| Metric | Value (2024) |

|---|---|

| Market share | ~40% |

| Beneficiaries (ANS) | 7.0M+ |

| Network dentists | 22,000+ |

| Municipalities | 2,700+ |

What is included in the product

Provides a clear SWOT framework that maps Odontoprev’s internal capabilities, operational weaknesses, market opportunities, and external threats to its strategic growth and competitive position.

Provides a concise SWOT matrix for Odontoprev that quickly identifies strengths, weaknesses, opportunities and threats to relieve strategic uncertainty and align stakeholders.

Weaknesses

High exposure to Brazil-only market

Odontoprev derives over 95% of revenue from the Brazil market, tying growth and risk to Brazil’s macro and regulatory backdrop. Brazil’s IPCA inflation ran about 4.4% in 2024, and BRL volatility can erode margins and pricing power. Limited geographic diversification reduces resilience to country shocks, and meaningful expansion beyond Brazil would demand new distribution, compliance and clinical capabilities.

Dependence on employer-sponsored demand

Odontoprev reported about 10.6 million beneficiaries at end-2024, with employer-sponsored corporate plans comprising roughly two-thirds of that base, concentrating demand risk.

Employment cycles and headcount reductions—heightened during the 2023–24 slowdown—have driven episodic spikes in churn, compressing lifetime value.

Negotiated group pricing for large employers pressures average revenue per user, so management is expanding into SMEs and retail to diversify—a strategy that increases customer acquisition costs and margin pressure.

Price-sensitive, commoditized product perception

Odontoprev (ODPV3) competes in a market where buyers often compare dental benefits mainly by price and network size, intensifying tender competition and margin compression. Limited product differentiation contributes to higher churn at renewal, with Brazil's dental beneficiary base near 24 million (ANS 2024) increasing buyer leverage. Communicating value beyond basic coverage remains a persistent challenge.

Reliance on third-party distribution

Dependence on banks, brokers and partners gives intermediaries strong bargaining power over commissions and product placement, risking margin pressure; Odontoprev serves about 10.5 million beneficiaries (2024), intensifying reliance on these channels. Channel conflict can undermine direct-to-consumer initiatives, partners may deprioritize dental and delay access to niche segments, and end-customer insights are often filtered through intermediaries.

- Intermediary bargaining power

- Channel conflict vs D2C

- Slowed niche access

- Filtered customer visibility

Limited brand engagement with end users

Members mainly interact with dentists rather than Odontoprev, meaning low-touch engagement limits cross-sell and loyalty; perceived value often appears only at claim moments. With roughly 10.5 million beneficiaries in 2024, missed digital touchpoints constrain lifetime value and require sustained capex to build effective omni-channel engagement.

- Low direct brand contact

- Reduced cross-sell/loyalty

- Value visible at claims

- Needs sustained digital investment

Brazil dental risk: 10.6m members, employer-dependent and macro-sensitive

Odontoprev is highly Brazil-concentrated (>95% revenues) exposing it to local macro, regulatory and BRL volatility (IPCA 2024 ~4.4%).

Beneficiaries ~10.6m end-2024, ~66% employer-sponsored, increasing churn sensitivity to employment cycles.

High intermediary power and low direct member contact compress ARPU and raise digital investment needs.

| Metric | Value (2024) |

|---|---|

| Beneficiaries | 10.6m |

| Brazil revenue share | >95% |

| Employer share | ~66% |

| Brazil dental base (ANS) | ~24m |

| IPCA | 4.4% |

Preview Before You Purchase

Odontoprev SWOT Analysis

This preview is a direct excerpt from the Odontoprev SWOT analysis you’ll receive upon purchase—no placeholders or samples. The full document is professional, editable and structured for immediate use. Buy to unlock the complete, detailed report.