OGE Energy Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

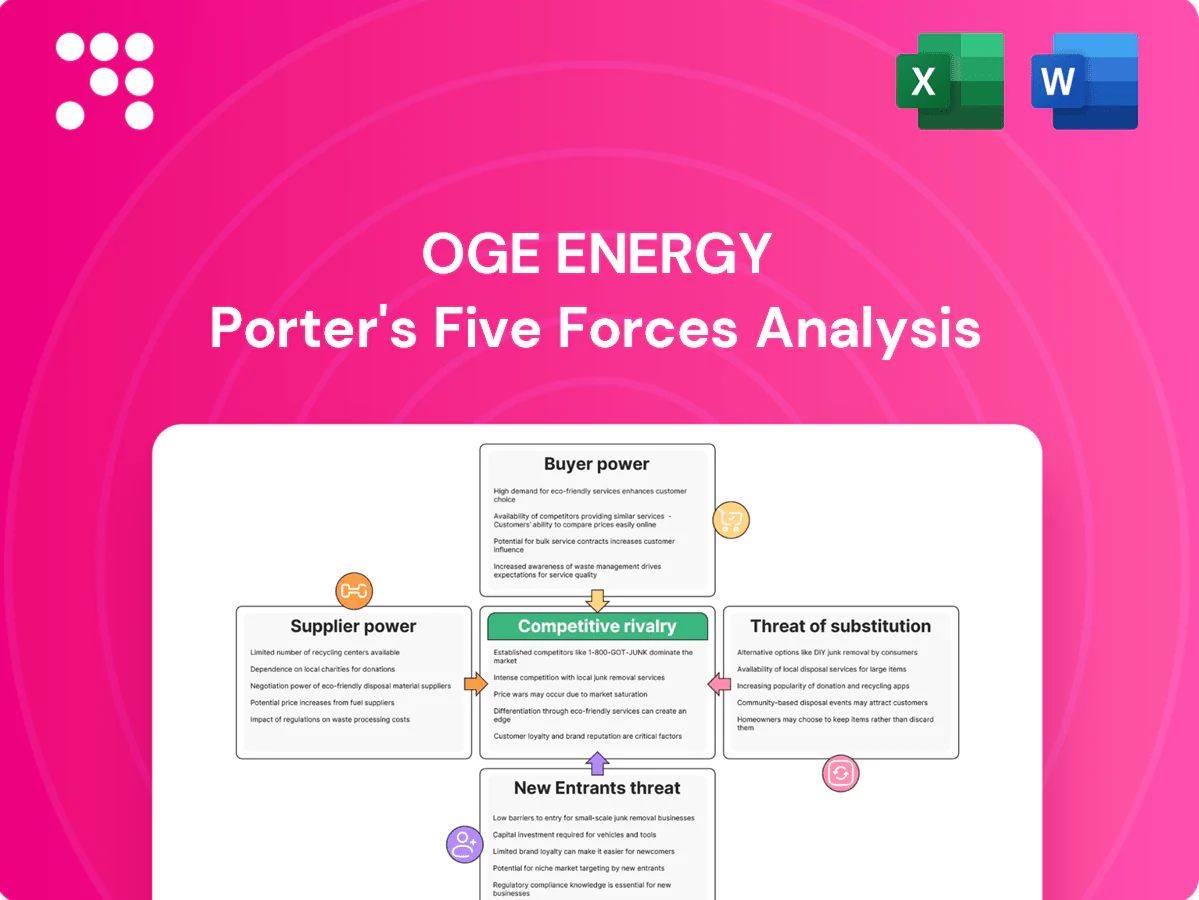

OGE Energy faces moderate buyer power, constrained supplier leverage, regulated barriers limiting new entrants, and evolving substitute threats from distributed generation; competitive rivalry is steady but innovation and regulation shift the balance. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore OGE Energy’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical equipment vendors

Large power transformers, breakers and advanced meters are sourced from a concentrated set of OEMs such as Siemens, ABB and GE, giving vendors pricing and 12–24 month lead-time leverage; extended deliveries have delayed utility reliability projects and increased carrying costs. OG&E reduces exposure with multi-year contracts, equipment standardization and strategic inventory build, while 2024 supply shocks or tariffs can still shift terms toward suppliers.

Fuel suppliers with pass-through dynamics

Natural gas and remaining coal suppliers retain some leverage, but Oklahoma’s competitive gas basin and extensive pipeline access limit single-supplier risk and OGE’s exposure; U.S. gas fueled roughly 39% of power generation in 2024, tempering supplier power. Regulated fuel-cost recovery mechanisms largely pass through price swings, muting margin impact. Long-term contracts and hedging programs stabilize cost and volume. Stricter environmental rules have pushed coal’s share down to about 15% in 2024, narrowing coal options while reducing overall coal exposure.

Renewable IPPs and PPA terms

Independent power producers gained leverage in 2024 as SPP's interconnection queue exceeded 200 GW and IRA tax-credit windows concentrated project timelines, tightening supply for new capacity bids.

PPA pricing, curtailment clauses, and annual escalation terms during constrained periods have shifted risk toward buyers, allowing IPPs to secure higher effective revenues.

Competitive solicitations and rapid technology cost deflation, plus localized transmission availability and SPP upgrades, partially counterbalance supplier bargaining power.

Transmission and construction contractors

Specialized EPC firms and scarce skilled labor raise contractor leverage during build cycles, with OGE's 2024 capital plan of approximately $1.1 billion concentrating spend on transmission and distribution and increasing demand for crews. Prevailing wage rules and peak 2024 workloads pushed mobilization rates higher, while multi-award frameworks and local workforce development moderated pricing; schedule risk clauses still shift contingencies to the utility.

- Finite EPC supply elevates bid premiums

- Prevailing wages and peak demand raise mobilization costs

- Multi-award contracts and local hires temper bargaining power

- Schedule risk provisions transfer contingency to OGE

Regulatory and compliance service providers

Regulatory and compliance vendors (environmental monitors, cybersecurity, grid software) exert strong leverage: 2024 grid modernization budgets exceeded $100B across North America, making regulatory must-haves and switching costs material; proprietary platforms lock in integration and training spend. OG&E pushes competitive RFPs and phased deployments to reduce exposure, but evolving NERC/FERC standards in 2024 can force vendor-driven upgrades on utility timelines.

- Vendor lock-in: high integration and training costs

- OGE mitigation: competitive RFPs, phased rollouts

- Risk: 2024 regulatory updates can mandate vendor upgrades

12–24m OEM leads, $1.1B capex strain; gas pass-throughs curb margins

OGE faces concentrated OEM leverage for transformers/meters (12–24 month lead times) and EPC labor pressure amid a $1.1B 2024 capex plan; fuel pass-throughs and Oklahoma gas access (U.S. gas ~39% of generation in 2024) limit supplier margins. IPP/PPA dynamics tightened with SPP queue >200GW, raising short-term procurement costs.

| Supplier | 2024 Metric | Impact |

|---|---|---|

| OEMs | 12–24m lead | Price/lead leverage |

| Fuel | Gas 39% / Coal 15% | Pass-through limits margin |

| EPC | $1.1B capex | Higher mobilization costs |

What is included in the product

Tailored Porter’s Five Forces analysis for OGE Energy uncovering key competition drivers, buyer and supplier power, substitutes and disruptive threats, and the barriers that protect incumbents—delivering strategic insights to assess pricing pressure, market entry risks, and long-term profitability.

Clear one-sheet Porter's Five Forces for OGE Energy—instantly visualize competitive pressure with a spider chart, customize force levels for regulatory shifts or new entrants, and drop into decks or Excel dashboards without macros for fast boardroom decision-making.

Customers Bargaining Power

Captive retail customers

Residential and small commercial customers have minimal switching ability within OGE Energys monopoly service territory, so direct buyer leverage is limited. Low price elasticity reduces threat of demand-side pressure. State utility commissions act as the practical counterparty, overseeing rates and returns. Customer satisfaction and outage performance remain important inputs in 2024 regulatory reviews and rate case outcomes.

Large C&I tariff negotiations

Industrial C&I customers can lobby OG&E for special rates, riders, or economic development tariffs; their load concentration—roughly 20% of OG&E’s energy sales across about 870,000 served customers—gives them strong standing in rate cases and resource plans. Threats to relocate or self-generate further enhance leverage, and OG&E routinely balances retention incentives against regulatory fairness tests in tariff and rider negotiations.

Regulatory proxy for customer interests

The Oklahoma Corporation Commission and Arkansas PSC set allowed returns, cost recovery and rate design for OGE, with regulators nationwide in 2024 generally authorizing utility ROEs in the 9–11% range. Stakeholders and consumer advocates routinely constrain pricing power through rate case interventions and settlements. Performance metrics, prudence reviews and formal dockets anchor decisions, aggregating dispersed buyer power into institutional proceedings.

Distributed energy and demand response options

Rooftop solar, batteries and demand response give customers real alternatives to manage bills, increasing bargaining power even at modest uptake; in 2024 OG&E serves about 800,000 customers so small shifts can affect load patterns and rate debates. Netting rules, standby charges and interconnection ease materially influence adoption rates and the salience of rate-design negotiations. Well-designed OG&E programs can align interests, reduce churn and lower system costs.

Service quality expectations

- Reliability over price

- Outage restoration metrics matter

- Customer care influences regulatory pressure

- Storm visibility affects filing leverage

Low residential switching boosts regulator pricing power; C&I and distributed techs shift leverage

Residential switching limited in OG&E’s monopoly (≈900,000 customers in 2024), so direct buyer leverage is low; regulators hold pricing power. Large C&I account for ~20% of sales, giving negotiation leverage via tariffs or self-generation. Distributed techs (solar+battery, demand response) rising, shifting bargaining dynamics.

| Metric | 2024 |

|---|---|

| Customers | 900,000 |

| C&I share | ~20% |

| Regulatory ROE | 9–11% |

Full Version Awaits

OGE Energy Porter's Five Forces Analysis

This preview shows the exact OGE Energy Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the complete, professionally formatted document ready for download and use the moment you buy. You'll get this same file instantly with no further setup required.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

OGE Energy faces moderate buyer power, constrained supplier leverage, regulated barriers limiting new entrants, and evolving substitute threats from distributed generation; competitive rivalry is steady but innovation and regulation shift the balance. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore OGE Energy’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical equipment vendors

Large power transformers, breakers and advanced meters are sourced from a concentrated set of OEMs such as Siemens, ABB and GE, giving vendors pricing and 12–24 month lead-time leverage; extended deliveries have delayed utility reliability projects and increased carrying costs. OG&E reduces exposure with multi-year contracts, equipment standardization and strategic inventory build, while 2024 supply shocks or tariffs can still shift terms toward suppliers.

Fuel suppliers with pass-through dynamics

Natural gas and remaining coal suppliers retain some leverage, but Oklahoma’s competitive gas basin and extensive pipeline access limit single-supplier risk and OGE’s exposure; U.S. gas fueled roughly 39% of power generation in 2024, tempering supplier power. Regulated fuel-cost recovery mechanisms largely pass through price swings, muting margin impact. Long-term contracts and hedging programs stabilize cost and volume. Stricter environmental rules have pushed coal’s share down to about 15% in 2024, narrowing coal options while reducing overall coal exposure.

Renewable IPPs and PPA terms

Independent power producers gained leverage in 2024 as SPP's interconnection queue exceeded 200 GW and IRA tax-credit windows concentrated project timelines, tightening supply for new capacity bids.

PPA pricing, curtailment clauses, and annual escalation terms during constrained periods have shifted risk toward buyers, allowing IPPs to secure higher effective revenues.

Competitive solicitations and rapid technology cost deflation, plus localized transmission availability and SPP upgrades, partially counterbalance supplier bargaining power.

Transmission and construction contractors

Specialized EPC firms and scarce skilled labor raise contractor leverage during build cycles, with OGE's 2024 capital plan of approximately $1.1 billion concentrating spend on transmission and distribution and increasing demand for crews. Prevailing wage rules and peak 2024 workloads pushed mobilization rates higher, while multi-award frameworks and local workforce development moderated pricing; schedule risk clauses still shift contingencies to the utility.

- Finite EPC supply elevates bid premiums

- Prevailing wages and peak demand raise mobilization costs

- Multi-award contracts and local hires temper bargaining power

- Schedule risk provisions transfer contingency to OGE

Regulatory and compliance service providers

Regulatory and compliance vendors (environmental monitors, cybersecurity, grid software) exert strong leverage: 2024 grid modernization budgets exceeded $100B across North America, making regulatory must-haves and switching costs material; proprietary platforms lock in integration and training spend. OG&E pushes competitive RFPs and phased deployments to reduce exposure, but evolving NERC/FERC standards in 2024 can force vendor-driven upgrades on utility timelines.

- Vendor lock-in: high integration and training costs

- OGE mitigation: competitive RFPs, phased rollouts

- Risk: 2024 regulatory updates can mandate vendor upgrades

12–24m OEM leads, $1.1B capex strain; gas pass-throughs curb margins

OGE faces concentrated OEM leverage for transformers/meters (12–24 month lead times) and EPC labor pressure amid a $1.1B 2024 capex plan; fuel pass-throughs and Oklahoma gas access (U.S. gas ~39% of generation in 2024) limit supplier margins. IPP/PPA dynamics tightened with SPP queue >200GW, raising short-term procurement costs.

| Supplier | 2024 Metric | Impact |

|---|---|---|

| OEMs | 12–24m lead | Price/lead leverage |

| Fuel | Gas 39% / Coal 15% | Pass-through limits margin |

| EPC | $1.1B capex | Higher mobilization costs |

What is included in the product

Tailored Porter’s Five Forces analysis for OGE Energy uncovering key competition drivers, buyer and supplier power, substitutes and disruptive threats, and the barriers that protect incumbents—delivering strategic insights to assess pricing pressure, market entry risks, and long-term profitability.

Clear one-sheet Porter's Five Forces for OGE Energy—instantly visualize competitive pressure with a spider chart, customize force levels for regulatory shifts or new entrants, and drop into decks or Excel dashboards without macros for fast boardroom decision-making.

Customers Bargaining Power

Captive retail customers

Residential and small commercial customers have minimal switching ability within OGE Energys monopoly service territory, so direct buyer leverage is limited. Low price elasticity reduces threat of demand-side pressure. State utility commissions act as the practical counterparty, overseeing rates and returns. Customer satisfaction and outage performance remain important inputs in 2024 regulatory reviews and rate case outcomes.

Large C&I tariff negotiations

Industrial C&I customers can lobby OG&E for special rates, riders, or economic development tariffs; their load concentration—roughly 20% of OG&E’s energy sales across about 870,000 served customers—gives them strong standing in rate cases and resource plans. Threats to relocate or self-generate further enhance leverage, and OG&E routinely balances retention incentives against regulatory fairness tests in tariff and rider negotiations.

Regulatory proxy for customer interests

The Oklahoma Corporation Commission and Arkansas PSC set allowed returns, cost recovery and rate design for OGE, with regulators nationwide in 2024 generally authorizing utility ROEs in the 9–11% range. Stakeholders and consumer advocates routinely constrain pricing power through rate case interventions and settlements. Performance metrics, prudence reviews and formal dockets anchor decisions, aggregating dispersed buyer power into institutional proceedings.

Distributed energy and demand response options

Rooftop solar, batteries and demand response give customers real alternatives to manage bills, increasing bargaining power even at modest uptake; in 2024 OG&E serves about 800,000 customers so small shifts can affect load patterns and rate debates. Netting rules, standby charges and interconnection ease materially influence adoption rates and the salience of rate-design negotiations. Well-designed OG&E programs can align interests, reduce churn and lower system costs.

Service quality expectations

- Reliability over price

- Outage restoration metrics matter

- Customer care influences regulatory pressure

- Storm visibility affects filing leverage

Low residential switching boosts regulator pricing power; C&I and distributed techs shift leverage

Residential switching limited in OG&E’s monopoly (≈900,000 customers in 2024), so direct buyer leverage is low; regulators hold pricing power. Large C&I account for ~20% of sales, giving negotiation leverage via tariffs or self-generation. Distributed techs (solar+battery, demand response) rising, shifting bargaining dynamics.

| Metric | 2024 |

|---|---|

| Customers | 900,000 |

| C&I share | ~20% |

| Regulatory ROE | 9–11% |

Full Version Awaits

OGE Energy Porter's Five Forces Analysis

This preview shows the exact OGE Energy Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the complete, professionally formatted document ready for download and use the moment you buy. You'll get this same file instantly with no further setup required.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

OGE Energy faces moderate buyer power, constrained supplier leverage, regulated barriers limiting new entrants, and evolving substitute threats from distributed generation; competitive rivalry is steady but innovation and regulation shift the balance. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore OGE Energy’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical equipment vendors

Large power transformers, breakers and advanced meters are sourced from a concentrated set of OEMs such as Siemens, ABB and GE, giving vendors pricing and 12–24 month lead-time leverage; extended deliveries have delayed utility reliability projects and increased carrying costs. OG&E reduces exposure with multi-year contracts, equipment standardization and strategic inventory build, while 2024 supply shocks or tariffs can still shift terms toward suppliers.

Fuel suppliers with pass-through dynamics

Natural gas and remaining coal suppliers retain some leverage, but Oklahoma’s competitive gas basin and extensive pipeline access limit single-supplier risk and OGE’s exposure; U.S. gas fueled roughly 39% of power generation in 2024, tempering supplier power. Regulated fuel-cost recovery mechanisms largely pass through price swings, muting margin impact. Long-term contracts and hedging programs stabilize cost and volume. Stricter environmental rules have pushed coal’s share down to about 15% in 2024, narrowing coal options while reducing overall coal exposure.

Renewable IPPs and PPA terms

Independent power producers gained leverage in 2024 as SPP's interconnection queue exceeded 200 GW and IRA tax-credit windows concentrated project timelines, tightening supply for new capacity bids.

PPA pricing, curtailment clauses, and annual escalation terms during constrained periods have shifted risk toward buyers, allowing IPPs to secure higher effective revenues.

Competitive solicitations and rapid technology cost deflation, plus localized transmission availability and SPP upgrades, partially counterbalance supplier bargaining power.

Transmission and construction contractors

Specialized EPC firms and scarce skilled labor raise contractor leverage during build cycles, with OGE's 2024 capital plan of approximately $1.1 billion concentrating spend on transmission and distribution and increasing demand for crews. Prevailing wage rules and peak 2024 workloads pushed mobilization rates higher, while multi-award frameworks and local workforce development moderated pricing; schedule risk clauses still shift contingencies to the utility.

- Finite EPC supply elevates bid premiums

- Prevailing wages and peak demand raise mobilization costs

- Multi-award contracts and local hires temper bargaining power

- Schedule risk provisions transfer contingency to OGE

Regulatory and compliance service providers

Regulatory and compliance vendors (environmental monitors, cybersecurity, grid software) exert strong leverage: 2024 grid modernization budgets exceeded $100B across North America, making regulatory must-haves and switching costs material; proprietary platforms lock in integration and training spend. OG&E pushes competitive RFPs and phased deployments to reduce exposure, but evolving NERC/FERC standards in 2024 can force vendor-driven upgrades on utility timelines.

- Vendor lock-in: high integration and training costs

- OGE mitigation: competitive RFPs, phased rollouts

- Risk: 2024 regulatory updates can mandate vendor upgrades

12–24m OEM leads, $1.1B capex strain; gas pass-throughs curb margins

OGE faces concentrated OEM leverage for transformers/meters (12–24 month lead times) and EPC labor pressure amid a $1.1B 2024 capex plan; fuel pass-throughs and Oklahoma gas access (U.S. gas ~39% of generation in 2024) limit supplier margins. IPP/PPA dynamics tightened with SPP queue >200GW, raising short-term procurement costs.

| Supplier | 2024 Metric | Impact |

|---|---|---|

| OEMs | 12–24m lead | Price/lead leverage |

| Fuel | Gas 39% / Coal 15% | Pass-through limits margin |

| EPC | $1.1B capex | Higher mobilization costs |

What is included in the product

Tailored Porter’s Five Forces analysis for OGE Energy uncovering key competition drivers, buyer and supplier power, substitutes and disruptive threats, and the barriers that protect incumbents—delivering strategic insights to assess pricing pressure, market entry risks, and long-term profitability.

Clear one-sheet Porter's Five Forces for OGE Energy—instantly visualize competitive pressure with a spider chart, customize force levels for regulatory shifts or new entrants, and drop into decks or Excel dashboards without macros for fast boardroom decision-making.

Customers Bargaining Power

Captive retail customers

Residential and small commercial customers have minimal switching ability within OGE Energys monopoly service territory, so direct buyer leverage is limited. Low price elasticity reduces threat of demand-side pressure. State utility commissions act as the practical counterparty, overseeing rates and returns. Customer satisfaction and outage performance remain important inputs in 2024 regulatory reviews and rate case outcomes.

Large C&I tariff negotiations

Industrial C&I customers can lobby OG&E for special rates, riders, or economic development tariffs; their load concentration—roughly 20% of OG&E’s energy sales across about 870,000 served customers—gives them strong standing in rate cases and resource plans. Threats to relocate or self-generate further enhance leverage, and OG&E routinely balances retention incentives against regulatory fairness tests in tariff and rider negotiations.

Regulatory proxy for customer interests

The Oklahoma Corporation Commission and Arkansas PSC set allowed returns, cost recovery and rate design for OGE, with regulators nationwide in 2024 generally authorizing utility ROEs in the 9–11% range. Stakeholders and consumer advocates routinely constrain pricing power through rate case interventions and settlements. Performance metrics, prudence reviews and formal dockets anchor decisions, aggregating dispersed buyer power into institutional proceedings.

Distributed energy and demand response options

Rooftop solar, batteries and demand response give customers real alternatives to manage bills, increasing bargaining power even at modest uptake; in 2024 OG&E serves about 800,000 customers so small shifts can affect load patterns and rate debates. Netting rules, standby charges and interconnection ease materially influence adoption rates and the salience of rate-design negotiations. Well-designed OG&E programs can align interests, reduce churn and lower system costs.

Service quality expectations

- Reliability over price

- Outage restoration metrics matter

- Customer care influences regulatory pressure

- Storm visibility affects filing leverage

Low residential switching boosts regulator pricing power; C&I and distributed techs shift leverage

Residential switching limited in OG&E’s monopoly (≈900,000 customers in 2024), so direct buyer leverage is low; regulators hold pricing power. Large C&I account for ~20% of sales, giving negotiation leverage via tariffs or self-generation. Distributed techs (solar+battery, demand response) rising, shifting bargaining dynamics.

| Metric | 2024 |

|---|---|

| Customers | 900,000 |

| C&I share | ~20% |

| Regulatory ROE | 9–11% |

Full Version Awaits

OGE Energy Porter's Five Forces Analysis

This preview shows the exact OGE Energy Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. It is the complete, professionally formatted document ready for download and use the moment you buy. You'll get this same file instantly with no further setup required.