OKI Electric Industry Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

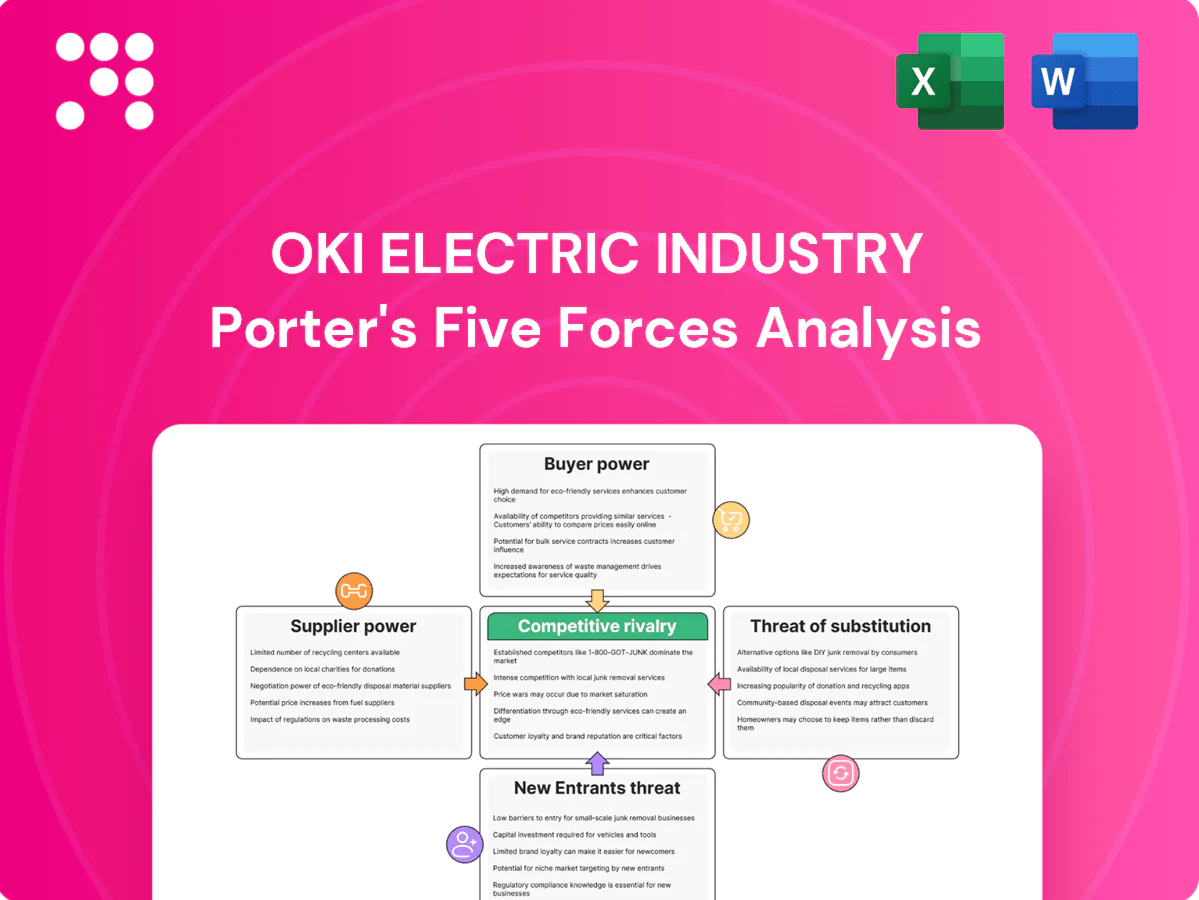

OKI Electric Industry faces moderate supplier power, evolving buyer expectations, and rising substitute risks from digital communication solutions, creating a competitive landscape that rewards innovation and cost discipline. This snapshot outlines key pressure points but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to get detailed ratings, visuals, and actionable recommendations tailored to OKI Electric.

Suppliers Bargaining Power

Concentrated semiconductor and component vendors

OKI depends on specialized chips, print heads and network ICs supplied by a few global vendors, with leading foundry TSMC holding about 56% of the pure-play foundry market in 2023, concentrating bargaining power. This raises switching costs and historically extended lead times to 20–26 weeks during shortages. Suppliers have passed price hikes amid constrained supply; OKI reduces leverage via long-term contracts and strategic inventories.

Special materials and compliance requirements

ATM/security modules, telecom-grade parts and stringent durability standards narrow OKI Electric Industry’s qualified supplier pool, concentrating leverage among compliant vendors. Certification and reliability testing—often requiring 99.999% availability design targets and 6–12 month qualification cycles—limit rapid supplier substitution. This elevates supplier bargaining power on compliant components, while approved-vendor expansion programs can progressively reduce single-supplier exposure.

Logistics and currency exposure

Global supply chains expose OKI to FX and freight volatility: container rates fell roughly 70% from 2021 peaks into 2024, but episodic spikes persist and can be passed by suppliers. Yen swings (around a 15% range versus the dollar in recent years) amplify component cost swings for OKI. Contract clauses and FX hedging blunt but do not remove supplier pricing power. Nearshoring and multi-node sourcing have reduced lead-time risk and supplier leverage.

ODM/OEM dependency in commoditized gear

ODM partners often retain design knowledge and tooling for printers and POS hardware, creating lock-in that raises transition costs and timing risks for redesigns; in 2024 ODMs still produce a majority of commoditized devices, keeping supplier leverage high. Dual-sourcing reference designs lowers dependence, while co-development with IP-sharing rebalances power.

- Dual-sourcing lowers lock-in

- Co-development + IP-sharing rebalance leverage

- Design/tooling ownership drives transition cost and timing risk

Supplier power tempered by OKI’s scale and forecasting

Aggregate demand across OKI’s printers, ATMs and telecom lines raises its supplier leverage, enabling large-volume contracts and better pricing; VMI and accurate forecasts cut stockouts ~20–30% and lower buffer inventory 10–30%, improving supplier utilization. Volume commitments have secured allocation in recent chip-constrained windows, though specialized niche parts still grant suppliers bargaining clout.

- Scale: cross-divisional demand

- VMI: −20–30% stockouts

- Volume commits: priority allocation

- Risk: niche-part supplier power

Concentrated chip supply (TSMC 56%) and 20–26 week lead times raise procurement, FX risk

OKI faces concentrated supplier power for chips/print heads (TSMC ~56% foundry share in 2023) and telecom-grade parts, causing 20–26 week lead times in shortages; long-term contracts, VMI and nearshoring cut risks. FX swings (~15% yen vs USD) and freight volatility (container rates down ~70% from 2021 peaks into 2024) sustain supplier pricing leverage despite volume commitments.

| Metric | 2023–24 |

|---|---|

| TSMC foundry share | 56% |

| Lead times (shortage) | 20–26 wks |

| Container rates change | −70% |

| Yen volatility | ~15% |

| VMI stockout reduction | 20–30% |

What is included in the product

Concise Porter's Five Forces analysis for OKI Electric Industry, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market position.

A concise one-sheet Porter's Five Forces analysis for OKI Electric Industry that visualizes supplier/customer power, rivalry, threats and substitutes—perfect for quick strategic decisions, board slides, and customizing pressure levels as market conditions evolve.

Customers Bargaining Power

Large enterprise and government procurement

Banks, retailers and public agencies procure office and printing solutions via formal RFPs with strict specs, with OECD estimates showing public procurement around 12% of GDP (2024), concentrating large-ticket deals. Their scale drives price pressure, extended payment terms often up to 60–90 days, and demanding SLAs (enterprise uptime targets commonly 99.9–99.99%). Multi-year frameworks intensify renewal competition with typical price erosion of 5–15%, while value-added services and uptime guarantees can protect 5–10% of margin.

High switching costs in ATMs and networks

Integration, certification, and field-service ecosystems for ATMs and telecom gear create material switching costs; ATM lifespans are typically 7–10 years and field-service contracts commonly run 3–7 years, raising operational disruption risk. Buyers therefore weigh operational continuity alongside price, which dampens post-deployment bargaining power. Lifecycle support and compatibility drive stickiness and favor incumbent vendors like OKI.

Commoditization in printers and POS

Commoditization in printers and POS means standardized features and easy comparability, allowing buyers to pit multiple brands and drive down prices and bundling; the global POS market was valued at USD 70.5 billion in 2024, amplifying buyer leverage. Total cost of ownership and consumables pricing become decisive purchase drivers, with consumables often determining long-term margins. Consequently differentiation shifts to reliability, workflow integration, and managed print services.

Demand for holistic solutions

Customers increasingly demand integrated hardware, software and services for digital transformation; solution selling in 2024 reduces like-for-like price comparisons and shifts negotiations to outcomes and total cost of ownership. Cross-selling across sectors dilutes bargaining on single line items, but outcome-based contracts raise pressure for tightly delivered SLAs and measurable KPIs.

- Trend: integrated bundles dominate negotiations

- Effect: fewer price-only comparisons

- Risk: delivery-linked penalties increase

Global service coverage expectations

Multinational clients demand consistent global support and spare parts, raising their bargaining power when OKI shows capability gaps in certain regions. Robust service networks, field technicians and remote monitoring lower buyer churn and enable premium pricing. Transparent service KPIs (uptime, MTTR, parts availability) sustain OKI’s negotiating position with large buyers.

- global-support: consistency reduces churn

- capability-gaps: weaken pricing power

- remote-monitoring: strengthens retention

- KPIs: justify premium contracts

Buyer leverage: procurement ~12% GDP, terms 60-90 days

Banks, retailers and public agencies (public procurement ~12% of GDP in 2024) push price and payment-term pressure (60–90 days), driving typical price erosion of 5–15% while services/uptime defend ~5–10% margin. Commodity printers/POS (global POS market $70.5B in 2024) increase buyer leverage; lifecycle contracts (ATM 7–10 yrs) create switching costs that favor incumbents.

| Buyer type | Metric | 2024 value | Impact |

|---|---|---|---|

| Public | Procurement | ~12% GDP | Concentrated large deals |

| POS | Market size | $70.5B | Price competition |

| Enterprise | Payment terms | 60–90 days | Cashflow pressure |

Preview the Actual Deliverable

OKI Electric Industry Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of OKI Electric Industry you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download the moment you buy. Use it for strategic insight and decision-making.

Go Beyond the Preview—Access the Full Strategic Report

OKI Electric Industry faces moderate supplier power, evolving buyer expectations, and rising substitute risks from digital communication solutions, creating a competitive landscape that rewards innovation and cost discipline. This snapshot outlines key pressure points but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to get detailed ratings, visuals, and actionable recommendations tailored to OKI Electric.

Suppliers Bargaining Power

Concentrated semiconductor and component vendors

OKI depends on specialized chips, print heads and network ICs supplied by a few global vendors, with leading foundry TSMC holding about 56% of the pure-play foundry market in 2023, concentrating bargaining power. This raises switching costs and historically extended lead times to 20–26 weeks during shortages. Suppliers have passed price hikes amid constrained supply; OKI reduces leverage via long-term contracts and strategic inventories.

Special materials and compliance requirements

ATM/security modules, telecom-grade parts and stringent durability standards narrow OKI Electric Industry’s qualified supplier pool, concentrating leverage among compliant vendors. Certification and reliability testing—often requiring 99.999% availability design targets and 6–12 month qualification cycles—limit rapid supplier substitution. This elevates supplier bargaining power on compliant components, while approved-vendor expansion programs can progressively reduce single-supplier exposure.

Logistics and currency exposure

Global supply chains expose OKI to FX and freight volatility: container rates fell roughly 70% from 2021 peaks into 2024, but episodic spikes persist and can be passed by suppliers. Yen swings (around a 15% range versus the dollar in recent years) amplify component cost swings for OKI. Contract clauses and FX hedging blunt but do not remove supplier pricing power. Nearshoring and multi-node sourcing have reduced lead-time risk and supplier leverage.

ODM/OEM dependency in commoditized gear

ODM partners often retain design knowledge and tooling for printers and POS hardware, creating lock-in that raises transition costs and timing risks for redesigns; in 2024 ODMs still produce a majority of commoditized devices, keeping supplier leverage high. Dual-sourcing reference designs lowers dependence, while co-development with IP-sharing rebalances power.

- Dual-sourcing lowers lock-in

- Co-development + IP-sharing rebalance leverage

- Design/tooling ownership drives transition cost and timing risk

Supplier power tempered by OKI’s scale and forecasting

Aggregate demand across OKI’s printers, ATMs and telecom lines raises its supplier leverage, enabling large-volume contracts and better pricing; VMI and accurate forecasts cut stockouts ~20–30% and lower buffer inventory 10–30%, improving supplier utilization. Volume commitments have secured allocation in recent chip-constrained windows, though specialized niche parts still grant suppliers bargaining clout.

- Scale: cross-divisional demand

- VMI: −20–30% stockouts

- Volume commits: priority allocation

- Risk: niche-part supplier power

Concentrated chip supply (TSMC 56%) and 20–26 week lead times raise procurement, FX risk

OKI faces concentrated supplier power for chips/print heads (TSMC ~56% foundry share in 2023) and telecom-grade parts, causing 20–26 week lead times in shortages; long-term contracts, VMI and nearshoring cut risks. FX swings (~15% yen vs USD) and freight volatility (container rates down ~70% from 2021 peaks into 2024) sustain supplier pricing leverage despite volume commitments.

| Metric | 2023–24 |

|---|---|

| TSMC foundry share | 56% |

| Lead times (shortage) | 20–26 wks |

| Container rates change | −70% |

| Yen volatility | ~15% |

| VMI stockout reduction | 20–30% |

What is included in the product

Concise Porter's Five Forces analysis for OKI Electric Industry, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market position.

A concise one-sheet Porter's Five Forces analysis for OKI Electric Industry that visualizes supplier/customer power, rivalry, threats and substitutes—perfect for quick strategic decisions, board slides, and customizing pressure levels as market conditions evolve.

Customers Bargaining Power

Large enterprise and government procurement

Banks, retailers and public agencies procure office and printing solutions via formal RFPs with strict specs, with OECD estimates showing public procurement around 12% of GDP (2024), concentrating large-ticket deals. Their scale drives price pressure, extended payment terms often up to 60–90 days, and demanding SLAs (enterprise uptime targets commonly 99.9–99.99%). Multi-year frameworks intensify renewal competition with typical price erosion of 5–15%, while value-added services and uptime guarantees can protect 5–10% of margin.

High switching costs in ATMs and networks

Integration, certification, and field-service ecosystems for ATMs and telecom gear create material switching costs; ATM lifespans are typically 7–10 years and field-service contracts commonly run 3–7 years, raising operational disruption risk. Buyers therefore weigh operational continuity alongside price, which dampens post-deployment bargaining power. Lifecycle support and compatibility drive stickiness and favor incumbent vendors like OKI.

Commoditization in printers and POS

Commoditization in printers and POS means standardized features and easy comparability, allowing buyers to pit multiple brands and drive down prices and bundling; the global POS market was valued at USD 70.5 billion in 2024, amplifying buyer leverage. Total cost of ownership and consumables pricing become decisive purchase drivers, with consumables often determining long-term margins. Consequently differentiation shifts to reliability, workflow integration, and managed print services.

Demand for holistic solutions

Customers increasingly demand integrated hardware, software and services for digital transformation; solution selling in 2024 reduces like-for-like price comparisons and shifts negotiations to outcomes and total cost of ownership. Cross-selling across sectors dilutes bargaining on single line items, but outcome-based contracts raise pressure for tightly delivered SLAs and measurable KPIs.

- Trend: integrated bundles dominate negotiations

- Effect: fewer price-only comparisons

- Risk: delivery-linked penalties increase

Global service coverage expectations

Multinational clients demand consistent global support and spare parts, raising their bargaining power when OKI shows capability gaps in certain regions. Robust service networks, field technicians and remote monitoring lower buyer churn and enable premium pricing. Transparent service KPIs (uptime, MTTR, parts availability) sustain OKI’s negotiating position with large buyers.

- global-support: consistency reduces churn

- capability-gaps: weaken pricing power

- remote-monitoring: strengthens retention

- KPIs: justify premium contracts

Buyer leverage: procurement ~12% GDP, terms 60-90 days

Banks, retailers and public agencies (public procurement ~12% of GDP in 2024) push price and payment-term pressure (60–90 days), driving typical price erosion of 5–15% while services/uptime defend ~5–10% margin. Commodity printers/POS (global POS market $70.5B in 2024) increase buyer leverage; lifecycle contracts (ATM 7–10 yrs) create switching costs that favor incumbents.

| Buyer type | Metric | 2024 value | Impact |

|---|---|---|---|

| Public | Procurement | ~12% GDP | Concentrated large deals |

| POS | Market size | $70.5B | Price competition |

| Enterprise | Payment terms | 60–90 days | Cashflow pressure |

Preview the Actual Deliverable

OKI Electric Industry Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of OKI Electric Industry you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download the moment you buy. Use it for strategic insight and decision-making.

Description

Go Beyond the Preview—Access the Full Strategic Report

OKI Electric Industry faces moderate supplier power, evolving buyer expectations, and rising substitute risks from digital communication solutions, creating a competitive landscape that rewards innovation and cost discipline. This snapshot outlines key pressure points but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to get detailed ratings, visuals, and actionable recommendations tailored to OKI Electric.

Suppliers Bargaining Power

Concentrated semiconductor and component vendors

OKI depends on specialized chips, print heads and network ICs supplied by a few global vendors, with leading foundry TSMC holding about 56% of the pure-play foundry market in 2023, concentrating bargaining power. This raises switching costs and historically extended lead times to 20–26 weeks during shortages. Suppliers have passed price hikes amid constrained supply; OKI reduces leverage via long-term contracts and strategic inventories.

Special materials and compliance requirements

ATM/security modules, telecom-grade parts and stringent durability standards narrow OKI Electric Industry’s qualified supplier pool, concentrating leverage among compliant vendors. Certification and reliability testing—often requiring 99.999% availability design targets and 6–12 month qualification cycles—limit rapid supplier substitution. This elevates supplier bargaining power on compliant components, while approved-vendor expansion programs can progressively reduce single-supplier exposure.

Logistics and currency exposure

Global supply chains expose OKI to FX and freight volatility: container rates fell roughly 70% from 2021 peaks into 2024, but episodic spikes persist and can be passed by suppliers. Yen swings (around a 15% range versus the dollar in recent years) amplify component cost swings for OKI. Contract clauses and FX hedging blunt but do not remove supplier pricing power. Nearshoring and multi-node sourcing have reduced lead-time risk and supplier leverage.

ODM/OEM dependency in commoditized gear

ODM partners often retain design knowledge and tooling for printers and POS hardware, creating lock-in that raises transition costs and timing risks for redesigns; in 2024 ODMs still produce a majority of commoditized devices, keeping supplier leverage high. Dual-sourcing reference designs lowers dependence, while co-development with IP-sharing rebalances power.

- Dual-sourcing lowers lock-in

- Co-development + IP-sharing rebalance leverage

- Design/tooling ownership drives transition cost and timing risk

Supplier power tempered by OKI’s scale and forecasting

Aggregate demand across OKI’s printers, ATMs and telecom lines raises its supplier leverage, enabling large-volume contracts and better pricing; VMI and accurate forecasts cut stockouts ~20–30% and lower buffer inventory 10–30%, improving supplier utilization. Volume commitments have secured allocation in recent chip-constrained windows, though specialized niche parts still grant suppliers bargaining clout.

- Scale: cross-divisional demand

- VMI: −20–30% stockouts

- Volume commits: priority allocation

- Risk: niche-part supplier power

Concentrated chip supply (TSMC 56%) and 20–26 week lead times raise procurement, FX risk

OKI faces concentrated supplier power for chips/print heads (TSMC ~56% foundry share in 2023) and telecom-grade parts, causing 20–26 week lead times in shortages; long-term contracts, VMI and nearshoring cut risks. FX swings (~15% yen vs USD) and freight volatility (container rates down ~70% from 2021 peaks into 2024) sustain supplier pricing leverage despite volume commitments.

| Metric | 2023–24 |

|---|---|

| TSMC foundry share | 56% |

| Lead times (shortage) | 20–26 wks |

| Container rates change | −70% |

| Yen volatility | ~15% |

| VMI stockout reduction | 20–30% |

What is included in the product

Concise Porter's Five Forces analysis for OKI Electric Industry, uncovering competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect margins and market position.

A concise one-sheet Porter's Five Forces analysis for OKI Electric Industry that visualizes supplier/customer power, rivalry, threats and substitutes—perfect for quick strategic decisions, board slides, and customizing pressure levels as market conditions evolve.

Customers Bargaining Power

Large enterprise and government procurement

Banks, retailers and public agencies procure office and printing solutions via formal RFPs with strict specs, with OECD estimates showing public procurement around 12% of GDP (2024), concentrating large-ticket deals. Their scale drives price pressure, extended payment terms often up to 60–90 days, and demanding SLAs (enterprise uptime targets commonly 99.9–99.99%). Multi-year frameworks intensify renewal competition with typical price erosion of 5–15%, while value-added services and uptime guarantees can protect 5–10% of margin.

High switching costs in ATMs and networks

Integration, certification, and field-service ecosystems for ATMs and telecom gear create material switching costs; ATM lifespans are typically 7–10 years and field-service contracts commonly run 3–7 years, raising operational disruption risk. Buyers therefore weigh operational continuity alongside price, which dampens post-deployment bargaining power. Lifecycle support and compatibility drive stickiness and favor incumbent vendors like OKI.

Commoditization in printers and POS

Commoditization in printers and POS means standardized features and easy comparability, allowing buyers to pit multiple brands and drive down prices and bundling; the global POS market was valued at USD 70.5 billion in 2024, amplifying buyer leverage. Total cost of ownership and consumables pricing become decisive purchase drivers, with consumables often determining long-term margins. Consequently differentiation shifts to reliability, workflow integration, and managed print services.

Demand for holistic solutions

Customers increasingly demand integrated hardware, software and services for digital transformation; solution selling in 2024 reduces like-for-like price comparisons and shifts negotiations to outcomes and total cost of ownership. Cross-selling across sectors dilutes bargaining on single line items, but outcome-based contracts raise pressure for tightly delivered SLAs and measurable KPIs.

- Trend: integrated bundles dominate negotiations

- Effect: fewer price-only comparisons

- Risk: delivery-linked penalties increase

Global service coverage expectations

Multinational clients demand consistent global support and spare parts, raising their bargaining power when OKI shows capability gaps in certain regions. Robust service networks, field technicians and remote monitoring lower buyer churn and enable premium pricing. Transparent service KPIs (uptime, MTTR, parts availability) sustain OKI’s negotiating position with large buyers.

- global-support: consistency reduces churn

- capability-gaps: weaken pricing power

- remote-monitoring: strengthens retention

- KPIs: justify premium contracts

Buyer leverage: procurement ~12% GDP, terms 60-90 days

Banks, retailers and public agencies (public procurement ~12% of GDP in 2024) push price and payment-term pressure (60–90 days), driving typical price erosion of 5–15% while services/uptime defend ~5–10% margin. Commodity printers/POS (global POS market $70.5B in 2024) increase buyer leverage; lifecycle contracts (ATM 7–10 yrs) create switching costs that favor incumbents.

| Buyer type | Metric | 2024 value | Impact |

|---|---|---|---|

| Public | Procurement | ~12% GDP | Concentrated large deals |

| POS | Market size | $70.5B | Price competition |

| Enterprise | Payment terms | 60–90 days | Cashflow pressure |

Preview the Actual Deliverable

OKI Electric Industry Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of OKI Electric Industry you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is fully formatted and ready for download the moment you buy. Use it for strategic insight and decision-making.