Olam Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

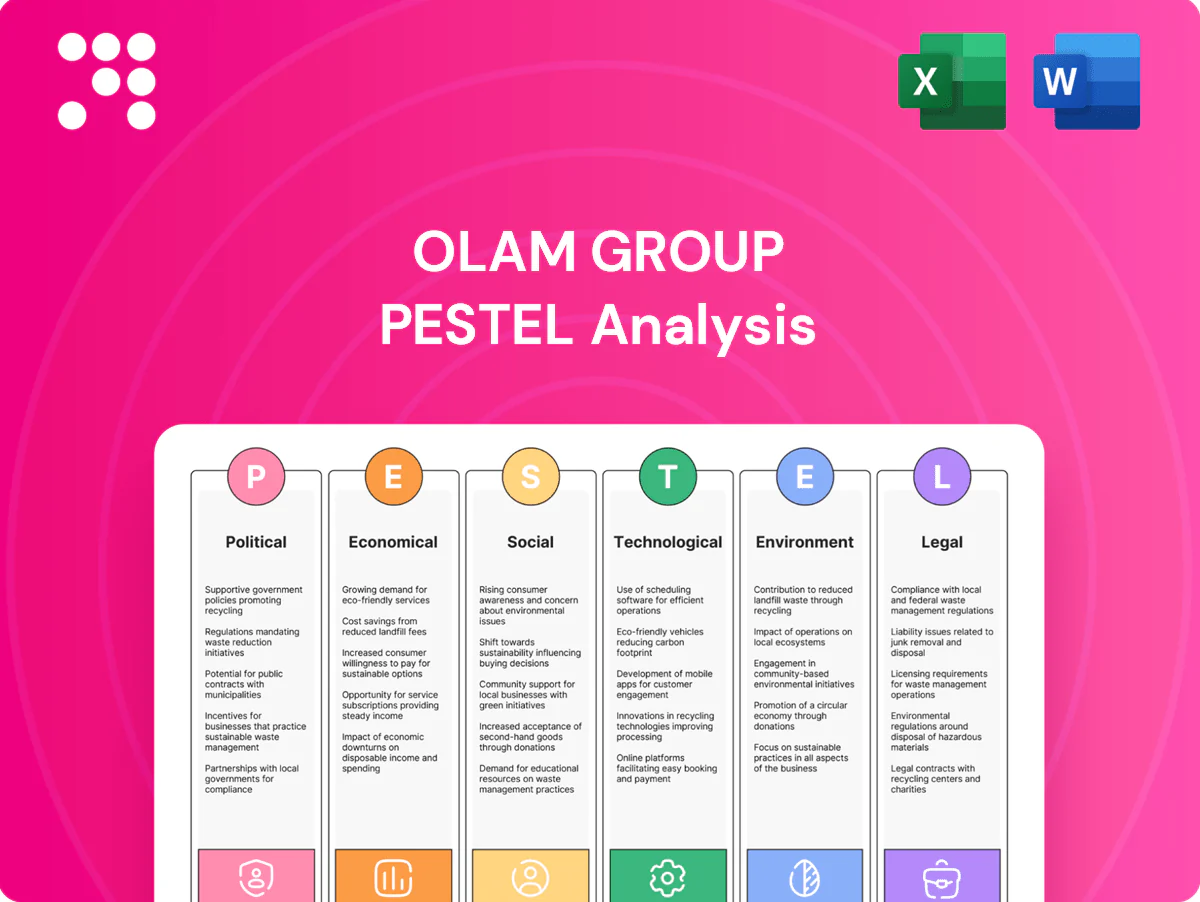

Gain strategic clarity with our PESTLE analysis of Olam Group—three to five concise insights on political, economic, social, technological, legal and environmental drivers shaping its future. Ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access the complete, editable breakdown and data-driven recommendations.

Political factors

Trade policy and tariffs

Shifts in tariffs and quotas directly affect cross-border flows of cocoa, coffee, grains, rice and edible oils central to Olam; protectionist measures can raise landed costs and logistics by roughly 10–15% while preferential trade agreements can cut costs materially. Continuous tariff monitoring and tariff-hedging strategies are vital for margin stability, and localizing processing reduces tariff exposure by keeping value-added within low-duty jurisdictions.

Geopolitical tensions

Geopolitical tensions can disrupt origination in key producing regions and reroute logistics, causing route closures, port congestion and insurance spikes that elevate working capital needs for Olam, which operates in over 60 countries; diversified sourcing and contingency routing reduce dependency on any single corridor, while scenario planning helps protect service levels to global customers.

Government farm support

Government subsidies, minimum price schemes and input support directly shape farmer planting choices and supply stability, affecting OFI and Olam Agri volumes and quality; policy shifts can rapidly change exportable tonnages. Olam sources from roughly 4.8 million farmers across 60+ countries, so partnership programs aligned with national priorities and co-investment in smallholder resilience reinforce access and political license to operate.

Food security agendas

Many governments prioritize staple affordability and supply reliability, evidenced by India’s food subsidy ~INR 3.3 trillion (2023–24) and the global fortified-food market ≈$20bn (2024). Participation in fortified foods and staple distribution aligns Olam with public goals. Policy-driven tenders can be large but price-sensitive and compliance-heavy; transparent traceability supports procurement eligibility.

- Public spending: India subsidy INR 3.3T (2023–24)

- Market size: fortified foods ≈$20bn (2024)

- Risk: tenders large, low margin, high compliance

- Advantage: traceability = eligibility for public procurement

Localization and industrial policy

Rules promoting local processing, employment and value‑add drive Olam's siting decisions; targeted incentives in priority markets have improved project economics, while local‑content rules increase compliance complexity and capex needs.

- Incentives can boost IRRs and de-risk investments

- Regional processing hubs expand market access, lower political exposure

- Stakeholder engagement aligns projects with national development plans

- Olam Group revenue ~USD 28.6bn (FY2023) underpins investment capacity

Tariff shocks, geopolitics and subsidies reshaping agri supply chains and landed costs

Tariff shifts and protectionism can change landed costs by ~10–15%, so tariff monitoring, hedging and localized processing are critical. Geopolitical disruption raises insurance and working capital; diversified sourcing across 60+ countries and scenario planning mitigate this. Subsidies, price supports and tenders (e.g., India subsidy INR 3.3T 2023–24) shape farmer decisions across Olam’s ~4.8M farmers and product mix.

| Metric | Value |

|---|---|

| Revenue (FY2023) | USD 28.6bn |

| Farmers sourced | ~4.8M |

| Countries | 60+ |

| Fortified foods market | ~USD 20bn (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Olam Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and trends tailored to its agri-commodity and supply-chain operations. Designed for executives and investors, the analysis pinpoints risks, opportunities and forward-looking scenarios to inform strategy, financing and resilience.

A concise, visually segmented PESTLE summary of Olam Group that relieves meeting prep pain—easy to drop into decks, annotate for local context, and share for quick alignment.

Economic factors

Commodity price volatility

Large swings in soft-commodity prices drive revenue variability and margin risk for Olam Group, making robust hedging programs, origination optionality and flexible contract structures essential to preserve margins. Active basis risk management and inventory optimization are used to stabilize cash flows across cycles. Transparency with customers enables pass-through mechanisms and reduces credit friction during price shocks.

FX and interest rates

Operating across 60+ countries exposes Olam to material translation and transaction FX risk; rising policy rates—US Fed funds around 5.25–5.50% mid‑2025—raise financing costs for inventory‑heavy operations. Olam cites active FX hedging and tenor diversification in its FY2024 report to stabilise earnings, and notes that local‑currency financing can better align assets and liabilities.

Global growth and demand

Growth in emerging markets—IMF projects about 4.3% GDP expansion in 2024—boosts demand for staples, ingredients and animal feed, while global slowdowns compress discretionary and premium ingredient segments. Olam’s balanced exposure across OFI and Olam Agri cushions revenue cyclicality. Data-driven forecasting via platforms like AtSource aligns procurement and capacity, improving inventory turns and fill rates.

Logistics and energy costs

- Freight shock: >10,000 USD/FEU (2021) → ~2,000 USD/FEU (2023–24)

- Bunker fuel: ~600 USD/ton (2024)

- Mitigants: route optimization, near‑market processing, long‑term contracts, multimodal

- Focus: efficiency programs to preserve margins

Labor and productivity

Tight labor markets have increased processing and logistics wage costs, squeezing margins; global average wage growth reached about 4% in 2024, pressuring Olam’s cost base. Automation and focused training programs are reducing labor intensity, while partnerships with local institutions secure talent pipelines. Productivity analytics pilots have delivered up to 10% OEE and throughput uplifts.

- Labor cost rise ~4% (2024)

- Automation + training = lower labor intensity

- Local partnerships → talent pipelines

- Analytics → up to 10% OEE/throughput gain

Tariff shocks, geopolitics and subsidies reshaping agri supply chains and landed costs

Soft‑commodity price volatility drives revenue and margin risk, requiring hedging, origination optionality and pass‑through contracts. Operating in 60+ countries creates FX and translation exposure as US Fed funds near 5.25–5.50% mid‑2025, raising working‑capital costs. Freight/container and labor shocks (container ~2,000 USD/FEU, bunker ~600 USD/ton, wage growth ~4% in 2024) compress margins.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Emerging market GDP (2024) | ~4.3% |

| Container rate (2023–24) | ~2,000 USD/FEU |

| Bunker fuel (2024) | ~600 USD/ton |

| Wage growth (2024) | ~4% |

What You See Is What You Get

Olam Group PESTLE Analysis

The preview of the Olam Group PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product with no placeholders or teasers. After payment you’ll instantly download the same final file displayed here.

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE analysis of Olam Group—three to five concise insights on political, economic, social, technological, legal and environmental drivers shaping its future. Ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access the complete, editable breakdown and data-driven recommendations.

Political factors

Trade policy and tariffs

Shifts in tariffs and quotas directly affect cross-border flows of cocoa, coffee, grains, rice and edible oils central to Olam; protectionist measures can raise landed costs and logistics by roughly 10–15% while preferential trade agreements can cut costs materially. Continuous tariff monitoring and tariff-hedging strategies are vital for margin stability, and localizing processing reduces tariff exposure by keeping value-added within low-duty jurisdictions.

Geopolitical tensions

Geopolitical tensions can disrupt origination in key producing regions and reroute logistics, causing route closures, port congestion and insurance spikes that elevate working capital needs for Olam, which operates in over 60 countries; diversified sourcing and contingency routing reduce dependency on any single corridor, while scenario planning helps protect service levels to global customers.

Government farm support

Government subsidies, minimum price schemes and input support directly shape farmer planting choices and supply stability, affecting OFI and Olam Agri volumes and quality; policy shifts can rapidly change exportable tonnages. Olam sources from roughly 4.8 million farmers across 60+ countries, so partnership programs aligned with national priorities and co-investment in smallholder resilience reinforce access and political license to operate.

Food security agendas

Many governments prioritize staple affordability and supply reliability, evidenced by India’s food subsidy ~INR 3.3 trillion (2023–24) and the global fortified-food market ≈$20bn (2024). Participation in fortified foods and staple distribution aligns Olam with public goals. Policy-driven tenders can be large but price-sensitive and compliance-heavy; transparent traceability supports procurement eligibility.

- Public spending: India subsidy INR 3.3T (2023–24)

- Market size: fortified foods ≈$20bn (2024)

- Risk: tenders large, low margin, high compliance

- Advantage: traceability = eligibility for public procurement

Localization and industrial policy

Rules promoting local processing, employment and value‑add drive Olam's siting decisions; targeted incentives in priority markets have improved project economics, while local‑content rules increase compliance complexity and capex needs.

- Incentives can boost IRRs and de-risk investments

- Regional processing hubs expand market access, lower political exposure

- Stakeholder engagement aligns projects with national development plans

- Olam Group revenue ~USD 28.6bn (FY2023) underpins investment capacity

Tariff shocks, geopolitics and subsidies reshaping agri supply chains and landed costs

Tariff shifts and protectionism can change landed costs by ~10–15%, so tariff monitoring, hedging and localized processing are critical. Geopolitical disruption raises insurance and working capital; diversified sourcing across 60+ countries and scenario planning mitigate this. Subsidies, price supports and tenders (e.g., India subsidy INR 3.3T 2023–24) shape farmer decisions across Olam’s ~4.8M farmers and product mix.

| Metric | Value |

|---|---|

| Revenue (FY2023) | USD 28.6bn |

| Farmers sourced | ~4.8M |

| Countries | 60+ |

| Fortified foods market | ~USD 20bn (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Olam Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and trends tailored to its agri-commodity and supply-chain operations. Designed for executives and investors, the analysis pinpoints risks, opportunities and forward-looking scenarios to inform strategy, financing and resilience.

A concise, visually segmented PESTLE summary of Olam Group that relieves meeting prep pain—easy to drop into decks, annotate for local context, and share for quick alignment.

Economic factors

Commodity price volatility

Large swings in soft-commodity prices drive revenue variability and margin risk for Olam Group, making robust hedging programs, origination optionality and flexible contract structures essential to preserve margins. Active basis risk management and inventory optimization are used to stabilize cash flows across cycles. Transparency with customers enables pass-through mechanisms and reduces credit friction during price shocks.

FX and interest rates

Operating across 60+ countries exposes Olam to material translation and transaction FX risk; rising policy rates—US Fed funds around 5.25–5.50% mid‑2025—raise financing costs for inventory‑heavy operations. Olam cites active FX hedging and tenor diversification in its FY2024 report to stabilise earnings, and notes that local‑currency financing can better align assets and liabilities.

Global growth and demand

Growth in emerging markets—IMF projects about 4.3% GDP expansion in 2024—boosts demand for staples, ingredients and animal feed, while global slowdowns compress discretionary and premium ingredient segments. Olam’s balanced exposure across OFI and Olam Agri cushions revenue cyclicality. Data-driven forecasting via platforms like AtSource aligns procurement and capacity, improving inventory turns and fill rates.

Logistics and energy costs

- Freight shock: >10,000 USD/FEU (2021) → ~2,000 USD/FEU (2023–24)

- Bunker fuel: ~600 USD/ton (2024)

- Mitigants: route optimization, near‑market processing, long‑term contracts, multimodal

- Focus: efficiency programs to preserve margins

Labor and productivity

Tight labor markets have increased processing and logistics wage costs, squeezing margins; global average wage growth reached about 4% in 2024, pressuring Olam’s cost base. Automation and focused training programs are reducing labor intensity, while partnerships with local institutions secure talent pipelines. Productivity analytics pilots have delivered up to 10% OEE and throughput uplifts.

- Labor cost rise ~4% (2024)

- Automation + training = lower labor intensity

- Local partnerships → talent pipelines

- Analytics → up to 10% OEE/throughput gain

Tariff shocks, geopolitics and subsidies reshaping agri supply chains and landed costs

Soft‑commodity price volatility drives revenue and margin risk, requiring hedging, origination optionality and pass‑through contracts. Operating in 60+ countries creates FX and translation exposure as US Fed funds near 5.25–5.50% mid‑2025, raising working‑capital costs. Freight/container and labor shocks (container ~2,000 USD/FEU, bunker ~600 USD/ton, wage growth ~4% in 2024) compress margins.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Emerging market GDP (2024) | ~4.3% |

| Container rate (2023–24) | ~2,000 USD/FEU |

| Bunker fuel (2024) | ~600 USD/ton |

| Wage growth (2024) | ~4% |

What You See Is What You Get

Olam Group PESTLE Analysis

The preview of the Olam Group PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product with no placeholders or teasers. After payment you’ll instantly download the same final file displayed here.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Gain strategic clarity with our PESTLE analysis of Olam Group—three to five concise insights on political, economic, social, technological, legal and environmental drivers shaping its future. Ideal for investors and strategists seeking actionable intelligence. Purchase the full report to access the complete, editable breakdown and data-driven recommendations.

Political factors

Trade policy and tariffs

Shifts in tariffs and quotas directly affect cross-border flows of cocoa, coffee, grains, rice and edible oils central to Olam; protectionist measures can raise landed costs and logistics by roughly 10–15% while preferential trade agreements can cut costs materially. Continuous tariff monitoring and tariff-hedging strategies are vital for margin stability, and localizing processing reduces tariff exposure by keeping value-added within low-duty jurisdictions.

Geopolitical tensions

Geopolitical tensions can disrupt origination in key producing regions and reroute logistics, causing route closures, port congestion and insurance spikes that elevate working capital needs for Olam, which operates in over 60 countries; diversified sourcing and contingency routing reduce dependency on any single corridor, while scenario planning helps protect service levels to global customers.

Government farm support

Government subsidies, minimum price schemes and input support directly shape farmer planting choices and supply stability, affecting OFI and Olam Agri volumes and quality; policy shifts can rapidly change exportable tonnages. Olam sources from roughly 4.8 million farmers across 60+ countries, so partnership programs aligned with national priorities and co-investment in smallholder resilience reinforce access and political license to operate.

Food security agendas

Many governments prioritize staple affordability and supply reliability, evidenced by India’s food subsidy ~INR 3.3 trillion (2023–24) and the global fortified-food market ≈$20bn (2024). Participation in fortified foods and staple distribution aligns Olam with public goals. Policy-driven tenders can be large but price-sensitive and compliance-heavy; transparent traceability supports procurement eligibility.

- Public spending: India subsidy INR 3.3T (2023–24)

- Market size: fortified foods ≈$20bn (2024)

- Risk: tenders large, low margin, high compliance

- Advantage: traceability = eligibility for public procurement

Localization and industrial policy

Rules promoting local processing, employment and value‑add drive Olam's siting decisions; targeted incentives in priority markets have improved project economics, while local‑content rules increase compliance complexity and capex needs.

- Incentives can boost IRRs and de-risk investments

- Regional processing hubs expand market access, lower political exposure

- Stakeholder engagement aligns projects with national development plans

- Olam Group revenue ~USD 28.6bn (FY2023) underpins investment capacity

Tariff shocks, geopolitics and subsidies reshaping agri supply chains and landed costs

Tariff shifts and protectionism can change landed costs by ~10–15%, so tariff monitoring, hedging and localized processing are critical. Geopolitical disruption raises insurance and working capital; diversified sourcing across 60+ countries and scenario planning mitigate this. Subsidies, price supports and tenders (e.g., India subsidy INR 3.3T 2023–24) shape farmer decisions across Olam’s ~4.8M farmers and product mix.

| Metric | Value |

|---|---|

| Revenue (FY2023) | USD 28.6bn |

| Farmers sourced | ~4.8M |

| Countries | 60+ |

| Fortified foods market | ~USD 20bn (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Olam Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and trends tailored to its agri-commodity and supply-chain operations. Designed for executives and investors, the analysis pinpoints risks, opportunities and forward-looking scenarios to inform strategy, financing and resilience.

A concise, visually segmented PESTLE summary of Olam Group that relieves meeting prep pain—easy to drop into decks, annotate for local context, and share for quick alignment.

Economic factors

Commodity price volatility

Large swings in soft-commodity prices drive revenue variability and margin risk for Olam Group, making robust hedging programs, origination optionality and flexible contract structures essential to preserve margins. Active basis risk management and inventory optimization are used to stabilize cash flows across cycles. Transparency with customers enables pass-through mechanisms and reduces credit friction during price shocks.

FX and interest rates

Operating across 60+ countries exposes Olam to material translation and transaction FX risk; rising policy rates—US Fed funds around 5.25–5.50% mid‑2025—raise financing costs for inventory‑heavy operations. Olam cites active FX hedging and tenor diversification in its FY2024 report to stabilise earnings, and notes that local‑currency financing can better align assets and liabilities.

Global growth and demand

Growth in emerging markets—IMF projects about 4.3% GDP expansion in 2024—boosts demand for staples, ingredients and animal feed, while global slowdowns compress discretionary and premium ingredient segments. Olam’s balanced exposure across OFI and Olam Agri cushions revenue cyclicality. Data-driven forecasting via platforms like AtSource aligns procurement and capacity, improving inventory turns and fill rates.

Logistics and energy costs

- Freight shock: >10,000 USD/FEU (2021) → ~2,000 USD/FEU (2023–24)

- Bunker fuel: ~600 USD/ton (2024)

- Mitigants: route optimization, near‑market processing, long‑term contracts, multimodal

- Focus: efficiency programs to preserve margins

Labor and productivity

Tight labor markets have increased processing and logistics wage costs, squeezing margins; global average wage growth reached about 4% in 2024, pressuring Olam’s cost base. Automation and focused training programs are reducing labor intensity, while partnerships with local institutions secure talent pipelines. Productivity analytics pilots have delivered up to 10% OEE and throughput uplifts.

- Labor cost rise ~4% (2024)

- Automation + training = lower labor intensity

- Local partnerships → talent pipelines

- Analytics → up to 10% OEE/throughput gain

Tariff shocks, geopolitics and subsidies reshaping agri supply chains and landed costs

Soft‑commodity price volatility drives revenue and margin risk, requiring hedging, origination optionality and pass‑through contracts. Operating in 60+ countries creates FX and translation exposure as US Fed funds near 5.25–5.50% mid‑2025, raising working‑capital costs. Freight/container and labor shocks (container ~2,000 USD/FEU, bunker ~600 USD/ton, wage growth ~4% in 2024) compress margins.

| Metric | Value |

|---|---|

| Fed funds (mid‑2025) | 5.25–5.50% |

| Emerging market GDP (2024) | ~4.3% |

| Container rate (2023–24) | ~2,000 USD/FEU |

| Bunker fuel (2024) | ~600 USD/ton |

| Wage growth (2024) | ~4% |

What You See Is What You Get

Olam Group PESTLE Analysis

The preview of the Olam Group PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product with no placeholders or teasers. After payment you’ll instantly download the same final file displayed here.