Old Mutual Ltd. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

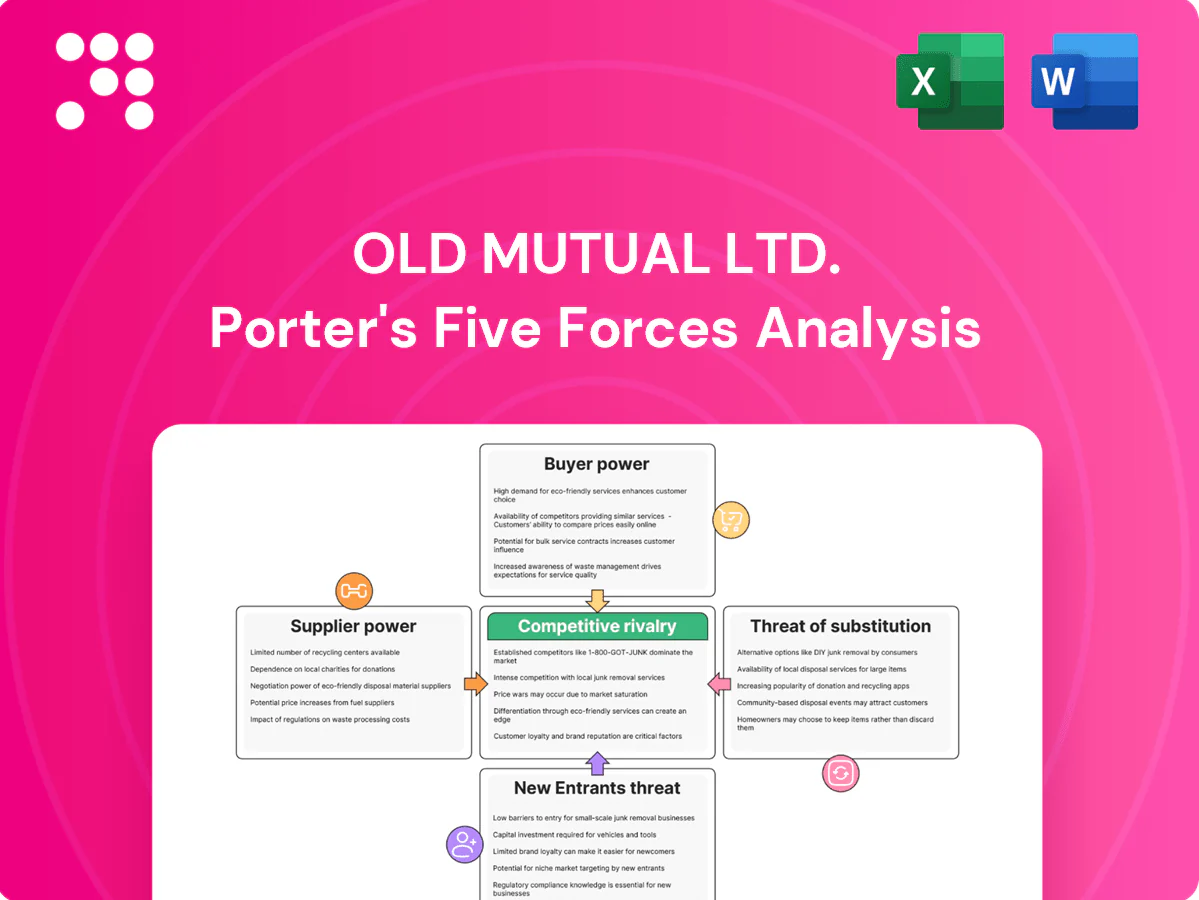

Old Mutual Ltd. faces intense competitive rivalry in South Africa and across Africa, with scale, diversification and regulatory capital requirements shaping its defenses; buyer power is moderate as distribution channels and brand loyalty matter. Emerging insurtechs and low-cost substitutes increase threat levels while supplier power remains constrained. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and strategic implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Reinsurers and capital providers

Old Mutual relies on global reinsurers for risk transfer and solvency optimisation, concentrating bargaining power with a few A‑rated firms such as Munich Re, Swiss Re and Hannover Re. Repricing and capacity tightening in hard markets have historically lifted reinsurance costs and can constrain product growth. Long-term relationships and diversified reinsurance panels mitigate but do not eliminate supplier leverage. Depth in Southern African capital markets, including the JSE, partly offsets dependency.

Specialist talent and actuarial skills

Experienced actuaries, data scientists and risk specialists remain scarce across African markets in 2024, increasing supplier power for Old Mutual as firms compete for limited talent pools. Wage inflation and poaching by competitors and Big Tech have pushed compensation premiums, while training pipelines (often 12–24 months) reduce vulnerability but require significant time and investment. Immigration and remote work offer limited relief given regulatory, licensing and data residency constraints.

Technology, core systems, and cloud vendors

Core policy admin, cloud, cybersecurity and analytics platforms carry high switching costs, with the global public cloud services market at about $597 billion in 2024, amplifying supplier leverage. Vendor lock-in and complex integrations increase pressure on pricing and service terms. Multi-vendor strategies and open architectures improve negotiating power. Regulatory data-localization in key African and EU markets further narrows vendor choice.

Distribution partners and intermediaries

Brokers, bancassurance partners and mobile network operators control customer access across key retail segments, pushing commission structures and exclusivity clauses that can tilt value toward these intermediaries.

Old Mutual’s owned tied-agent networks, including its OMFA channels, mitigate this dependence by retaining direct customer relationships and cross-selling capabilities.

Performance-based contracts, incentive-aligned commissions and structured data-sharing agreements have been deployed to reduce partner bargaining power and improve customer retention.

- Distribution concentration: partners control access

- Commissions/exclusivity shift value to intermediaries

- Owned tied-agent networks balance dependence

- Performance contracts and data-sharing lower partner power

Data providers and credit bureaus

Pricing and underwriting at Old Mutual rely on reliable credit, health and alternative data; globally the big three credit bureaus—Experian, Equifax, TransUnion—dominate supply. In several African and European markets a small number of bureaus or telcos are primary suppliers, concentrating bargaining power. Data privacy regimes such as GDPR and South Africa's POPIA increase compliance costs. Investing in proprietary data and telematics reduces this exposure over time.

- Dependence on bureaus: big three dominate global consumer credit data

- Market concentration: few suppliers in several markets increase supplier power

- Regulation: GDPR and POPIA raise effective costs

- Mitigation: proprietary data and telematics lower supplier risk

Concentrated reinsurers and scarce talent push insurer supplier power higher in 2024

Supplier power for Old Mutual is elevated in 2024 due to concentrated reinsurance (major players Munich Re, Swiss Re, Hannover Re), scarce actuarial/tech talent across African markets and high-switching-cost platform vendors.

Distribution partners and credit bureaus (Experian, Equifax, TransUnion) further tighten leverage; GDPR and POPIA raise compliance costs.

| Factor | 2024 datapoint |

|---|---|

| Global public cloud | $597B market |

| Credit bureaus | Dominated by big three |

What is included in the product

Tailored Porter's Five Forces analysis for Old Mutual Ltd., uncovering competitive intensity, buyer and supplier power, threat of substitutes and entrants, plus disruptive forces and strategic implications for market positioning.

One-sheet Porter's Five Forces for Old Mutual Ltd.—clear, customizable pressure levels and an instant spider chart that simplifies competitive complexity for quick decision-making and slide-ready use.

Customers Bargaining Power

Corporate buyers and group schemes

Large employers and pension funds run competitive tenders that extract volume discounts and service guarantees, pressuring margins for insurers like Old Mutual. Switching costs are moderate because benefits are standardized and brokers mediate procurement, keeping churn manageable. Multi-year contracts (commonly 2–5 years) temper short-term churn but intensify price competition at renewal. Value-add wellness programmes and analytics shift negotiations away from pure price.

Retail customers’ price sensitivity

Household budgets in key African markets remain constrained, with inflation averaging about 7% in 2023–24 in several economies, increasing sensitivity to premiums and fees. Simplified products are easily comparable online and via agents, boosting buyer power. Flexible premiums and micro-insurance features (penetration still under 10% regionally) help retain customers. Loyalty benefits and embedded services raise perceived value and reduce churn.

Brokers as buying agents

Brokers aggregate client demand and steer carrier selection in commercial and high-net-worth segments, giving them leverage to negotiate higher commissions or lower client pricing. Deep relationships and service differentiation—claims support, tailored solutions—often determine broker recommendations. Digital portals and straight-through processing enhance broker stickiness by speeding placements and reporting. This concentrated broker influence elevates customer bargaining power versus carriers like Old Mutual Ltd.

Digital transparency and comparison tools

Digital transparency via comparison sites and fintech marketplaces raises customer bargaining power by making prices and cover features instantly comparable, compressing margins in commoditized lines such as motor and term life; Old Mutual counters this by developing bundled offerings and unique riders that reduce pure price shopping. Strong NPS and high claims-service ratings help retain customers and mitigate race-to-the-bottom pricing pressure.

- Comparison sites: increase transparency, compress margins

- Bundled products & riders: defend against price-only switching

- NPS/claims service: key retention levers

Regulatory and consumer protection leverage

Regulatory and consumer protection regimes, including treating customers fairly and fee-cap policies, shift leverage to Old Mutual customers by raising risks of remediation and mandated product redesigns that compress margins; clear disclosures and robust conduct-risk controls reduce dispute frequency and litigation exposure; proactive regulator engagement helps shape pragmatic enforcement expectations.

- Treating customers fairly increases buyer leverage

- Remediation and redesigns pressure profitability

- Disclosures and conduct controls mitigate disputes

- Proactive regulatory engagement shapes rules

2-5yr contracts, digital compression and ~7% inflation squeeze premiums

Large corporate tenders and broker-driven placements keep pricing pressure high; multi-year contracts (commonly 2–5 years) lock renewals into intense negotiation. Household premium sensitivity rose as inflation averaged ~7% in 2023–24; micro-insurance penetration remains below 10%, limiting premium elasticity. Digital comparison sites compress margins, while bundles, riders and claims service mitigate churn.

| Metric | Value |

|---|---|

| Inflation (selected African markets, 2023–24) | ~7% |

| Micro-insurance penetration | <10% |

| Contract length (commercial) | 2–5 yrs |

Full Version Awaits

Old Mutual Ltd. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Old Mutual Ltd. evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry dynamics to inform strategic and investment decisions. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is complete, professionally formatted, and ready for immediate download and use.

Don't Miss the Bigger Picture

Old Mutual Ltd. faces intense competitive rivalry in South Africa and across Africa, with scale, diversification and regulatory capital requirements shaping its defenses; buyer power is moderate as distribution channels and brand loyalty matter. Emerging insurtechs and low-cost substitutes increase threat levels while supplier power remains constrained. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and strategic implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Reinsurers and capital providers

Old Mutual relies on global reinsurers for risk transfer and solvency optimisation, concentrating bargaining power with a few A‑rated firms such as Munich Re, Swiss Re and Hannover Re. Repricing and capacity tightening in hard markets have historically lifted reinsurance costs and can constrain product growth. Long-term relationships and diversified reinsurance panels mitigate but do not eliminate supplier leverage. Depth in Southern African capital markets, including the JSE, partly offsets dependency.

Specialist talent and actuarial skills

Experienced actuaries, data scientists and risk specialists remain scarce across African markets in 2024, increasing supplier power for Old Mutual as firms compete for limited talent pools. Wage inflation and poaching by competitors and Big Tech have pushed compensation premiums, while training pipelines (often 12–24 months) reduce vulnerability but require significant time and investment. Immigration and remote work offer limited relief given regulatory, licensing and data residency constraints.

Technology, core systems, and cloud vendors

Core policy admin, cloud, cybersecurity and analytics platforms carry high switching costs, with the global public cloud services market at about $597 billion in 2024, amplifying supplier leverage. Vendor lock-in and complex integrations increase pressure on pricing and service terms. Multi-vendor strategies and open architectures improve negotiating power. Regulatory data-localization in key African and EU markets further narrows vendor choice.

Distribution partners and intermediaries

Brokers, bancassurance partners and mobile network operators control customer access across key retail segments, pushing commission structures and exclusivity clauses that can tilt value toward these intermediaries.

Old Mutual’s owned tied-agent networks, including its OMFA channels, mitigate this dependence by retaining direct customer relationships and cross-selling capabilities.

Performance-based contracts, incentive-aligned commissions and structured data-sharing agreements have been deployed to reduce partner bargaining power and improve customer retention.

- Distribution concentration: partners control access

- Commissions/exclusivity shift value to intermediaries

- Owned tied-agent networks balance dependence

- Performance contracts and data-sharing lower partner power

Data providers and credit bureaus

Pricing and underwriting at Old Mutual rely on reliable credit, health and alternative data; globally the big three credit bureaus—Experian, Equifax, TransUnion—dominate supply. In several African and European markets a small number of bureaus or telcos are primary suppliers, concentrating bargaining power. Data privacy regimes such as GDPR and South Africa's POPIA increase compliance costs. Investing in proprietary data and telematics reduces this exposure over time.

- Dependence on bureaus: big three dominate global consumer credit data

- Market concentration: few suppliers in several markets increase supplier power

- Regulation: GDPR and POPIA raise effective costs

- Mitigation: proprietary data and telematics lower supplier risk

Concentrated reinsurers and scarce talent push insurer supplier power higher in 2024

Supplier power for Old Mutual is elevated in 2024 due to concentrated reinsurance (major players Munich Re, Swiss Re, Hannover Re), scarce actuarial/tech talent across African markets and high-switching-cost platform vendors.

Distribution partners and credit bureaus (Experian, Equifax, TransUnion) further tighten leverage; GDPR and POPIA raise compliance costs.

| Factor | 2024 datapoint |

|---|---|

| Global public cloud | $597B market |

| Credit bureaus | Dominated by big three |

What is included in the product

Tailored Porter's Five Forces analysis for Old Mutual Ltd., uncovering competitive intensity, buyer and supplier power, threat of substitutes and entrants, plus disruptive forces and strategic implications for market positioning.

One-sheet Porter's Five Forces for Old Mutual Ltd.—clear, customizable pressure levels and an instant spider chart that simplifies competitive complexity for quick decision-making and slide-ready use.

Customers Bargaining Power

Corporate buyers and group schemes

Large employers and pension funds run competitive tenders that extract volume discounts and service guarantees, pressuring margins for insurers like Old Mutual. Switching costs are moderate because benefits are standardized and brokers mediate procurement, keeping churn manageable. Multi-year contracts (commonly 2–5 years) temper short-term churn but intensify price competition at renewal. Value-add wellness programmes and analytics shift negotiations away from pure price.

Retail customers’ price sensitivity

Household budgets in key African markets remain constrained, with inflation averaging about 7% in 2023–24 in several economies, increasing sensitivity to premiums and fees. Simplified products are easily comparable online and via agents, boosting buyer power. Flexible premiums and micro-insurance features (penetration still under 10% regionally) help retain customers. Loyalty benefits and embedded services raise perceived value and reduce churn.

Brokers as buying agents

Brokers aggregate client demand and steer carrier selection in commercial and high-net-worth segments, giving them leverage to negotiate higher commissions or lower client pricing. Deep relationships and service differentiation—claims support, tailored solutions—often determine broker recommendations. Digital portals and straight-through processing enhance broker stickiness by speeding placements and reporting. This concentrated broker influence elevates customer bargaining power versus carriers like Old Mutual Ltd.

Digital transparency and comparison tools

Digital transparency via comparison sites and fintech marketplaces raises customer bargaining power by making prices and cover features instantly comparable, compressing margins in commoditized lines such as motor and term life; Old Mutual counters this by developing bundled offerings and unique riders that reduce pure price shopping. Strong NPS and high claims-service ratings help retain customers and mitigate race-to-the-bottom pricing pressure.

- Comparison sites: increase transparency, compress margins

- Bundled products & riders: defend against price-only switching

- NPS/claims service: key retention levers

Regulatory and consumer protection leverage

Regulatory and consumer protection regimes, including treating customers fairly and fee-cap policies, shift leverage to Old Mutual customers by raising risks of remediation and mandated product redesigns that compress margins; clear disclosures and robust conduct-risk controls reduce dispute frequency and litigation exposure; proactive regulator engagement helps shape pragmatic enforcement expectations.

- Treating customers fairly increases buyer leverage

- Remediation and redesigns pressure profitability

- Disclosures and conduct controls mitigate disputes

- Proactive regulatory engagement shapes rules

2-5yr contracts, digital compression and ~7% inflation squeeze premiums

Large corporate tenders and broker-driven placements keep pricing pressure high; multi-year contracts (commonly 2–5 years) lock renewals into intense negotiation. Household premium sensitivity rose as inflation averaged ~7% in 2023–24; micro-insurance penetration remains below 10%, limiting premium elasticity. Digital comparison sites compress margins, while bundles, riders and claims service mitigate churn.

| Metric | Value |

|---|---|

| Inflation (selected African markets, 2023–24) | ~7% |

| Micro-insurance penetration | <10% |

| Contract length (commercial) | 2–5 yrs |

Full Version Awaits

Old Mutual Ltd. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Old Mutual Ltd. evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry dynamics to inform strategic and investment decisions. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is complete, professionally formatted, and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Old Mutual Ltd. faces intense competitive rivalry in South Africa and across Africa, with scale, diversification and regulatory capital requirements shaping its defenses; buyer power is moderate as distribution channels and brand loyalty matter. Emerging insurtechs and low-cost substitutes increase threat levels while supplier power remains constrained. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals and strategic implications to inform investment or strategy decisions.

Suppliers Bargaining Power

Reinsurers and capital providers

Old Mutual relies on global reinsurers for risk transfer and solvency optimisation, concentrating bargaining power with a few A‑rated firms such as Munich Re, Swiss Re and Hannover Re. Repricing and capacity tightening in hard markets have historically lifted reinsurance costs and can constrain product growth. Long-term relationships and diversified reinsurance panels mitigate but do not eliminate supplier leverage. Depth in Southern African capital markets, including the JSE, partly offsets dependency.

Specialist talent and actuarial skills

Experienced actuaries, data scientists and risk specialists remain scarce across African markets in 2024, increasing supplier power for Old Mutual as firms compete for limited talent pools. Wage inflation and poaching by competitors and Big Tech have pushed compensation premiums, while training pipelines (often 12–24 months) reduce vulnerability but require significant time and investment. Immigration and remote work offer limited relief given regulatory, licensing and data residency constraints.

Technology, core systems, and cloud vendors

Core policy admin, cloud, cybersecurity and analytics platforms carry high switching costs, with the global public cloud services market at about $597 billion in 2024, amplifying supplier leverage. Vendor lock-in and complex integrations increase pressure on pricing and service terms. Multi-vendor strategies and open architectures improve negotiating power. Regulatory data-localization in key African and EU markets further narrows vendor choice.

Distribution partners and intermediaries

Brokers, bancassurance partners and mobile network operators control customer access across key retail segments, pushing commission structures and exclusivity clauses that can tilt value toward these intermediaries.

Old Mutual’s owned tied-agent networks, including its OMFA channels, mitigate this dependence by retaining direct customer relationships and cross-selling capabilities.

Performance-based contracts, incentive-aligned commissions and structured data-sharing agreements have been deployed to reduce partner bargaining power and improve customer retention.

- Distribution concentration: partners control access

- Commissions/exclusivity shift value to intermediaries

- Owned tied-agent networks balance dependence

- Performance contracts and data-sharing lower partner power

Data providers and credit bureaus

Pricing and underwriting at Old Mutual rely on reliable credit, health and alternative data; globally the big three credit bureaus—Experian, Equifax, TransUnion—dominate supply. In several African and European markets a small number of bureaus or telcos are primary suppliers, concentrating bargaining power. Data privacy regimes such as GDPR and South Africa's POPIA increase compliance costs. Investing in proprietary data and telematics reduces this exposure over time.

- Dependence on bureaus: big three dominate global consumer credit data

- Market concentration: few suppliers in several markets increase supplier power

- Regulation: GDPR and POPIA raise effective costs

- Mitigation: proprietary data and telematics lower supplier risk

Concentrated reinsurers and scarce talent push insurer supplier power higher in 2024

Supplier power for Old Mutual is elevated in 2024 due to concentrated reinsurance (major players Munich Re, Swiss Re, Hannover Re), scarce actuarial/tech talent across African markets and high-switching-cost platform vendors.

Distribution partners and credit bureaus (Experian, Equifax, TransUnion) further tighten leverage; GDPR and POPIA raise compliance costs.

| Factor | 2024 datapoint |

|---|---|

| Global public cloud | $597B market |

| Credit bureaus | Dominated by big three |

What is included in the product

Tailored Porter's Five Forces analysis for Old Mutual Ltd., uncovering competitive intensity, buyer and supplier power, threat of substitutes and entrants, plus disruptive forces and strategic implications for market positioning.

One-sheet Porter's Five Forces for Old Mutual Ltd.—clear, customizable pressure levels and an instant spider chart that simplifies competitive complexity for quick decision-making and slide-ready use.

Customers Bargaining Power

Corporate buyers and group schemes

Large employers and pension funds run competitive tenders that extract volume discounts and service guarantees, pressuring margins for insurers like Old Mutual. Switching costs are moderate because benefits are standardized and brokers mediate procurement, keeping churn manageable. Multi-year contracts (commonly 2–5 years) temper short-term churn but intensify price competition at renewal. Value-add wellness programmes and analytics shift negotiations away from pure price.

Retail customers’ price sensitivity

Household budgets in key African markets remain constrained, with inflation averaging about 7% in 2023–24 in several economies, increasing sensitivity to premiums and fees. Simplified products are easily comparable online and via agents, boosting buyer power. Flexible premiums and micro-insurance features (penetration still under 10% regionally) help retain customers. Loyalty benefits and embedded services raise perceived value and reduce churn.

Brokers as buying agents

Brokers aggregate client demand and steer carrier selection in commercial and high-net-worth segments, giving them leverage to negotiate higher commissions or lower client pricing. Deep relationships and service differentiation—claims support, tailored solutions—often determine broker recommendations. Digital portals and straight-through processing enhance broker stickiness by speeding placements and reporting. This concentrated broker influence elevates customer bargaining power versus carriers like Old Mutual Ltd.

Digital transparency and comparison tools

Digital transparency via comparison sites and fintech marketplaces raises customer bargaining power by making prices and cover features instantly comparable, compressing margins in commoditized lines such as motor and term life; Old Mutual counters this by developing bundled offerings and unique riders that reduce pure price shopping. Strong NPS and high claims-service ratings help retain customers and mitigate race-to-the-bottom pricing pressure.

- Comparison sites: increase transparency, compress margins

- Bundled products & riders: defend against price-only switching

- NPS/claims service: key retention levers

Regulatory and consumer protection leverage

Regulatory and consumer protection regimes, including treating customers fairly and fee-cap policies, shift leverage to Old Mutual customers by raising risks of remediation and mandated product redesigns that compress margins; clear disclosures and robust conduct-risk controls reduce dispute frequency and litigation exposure; proactive regulator engagement helps shape pragmatic enforcement expectations.

- Treating customers fairly increases buyer leverage

- Remediation and redesigns pressure profitability

- Disclosures and conduct controls mitigate disputes

- Proactive regulatory engagement shapes rules

2-5yr contracts, digital compression and ~7% inflation squeeze premiums

Large corporate tenders and broker-driven placements keep pricing pressure high; multi-year contracts (commonly 2–5 years) lock renewals into intense negotiation. Household premium sensitivity rose as inflation averaged ~7% in 2023–24; micro-insurance penetration remains below 10%, limiting premium elasticity. Digital comparison sites compress margins, while bundles, riders and claims service mitigate churn.

| Metric | Value |

|---|---|

| Inflation (selected African markets, 2023–24) | ~7% |

| Micro-insurance penetration | <10% |

| Contract length (commercial) | 2–5 yrs |

Full Version Awaits

Old Mutual Ltd. Porter's Five Forces Analysis

This Porter's Five Forces analysis of Old Mutual Ltd. evaluates competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and industry dynamics to inform strategic and investment decisions. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. The file is complete, professionally formatted, and ready for immediate download and use.