Universal Display Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

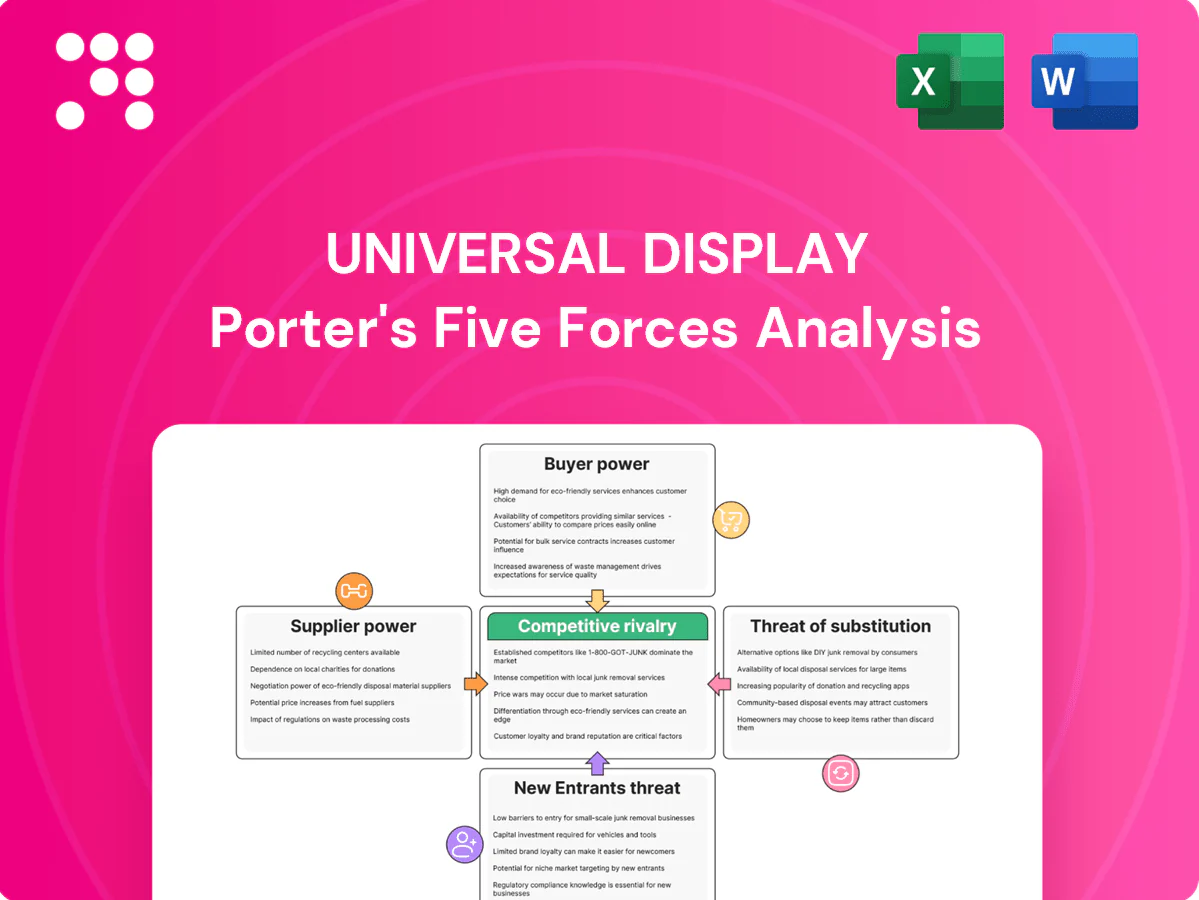

Universal Display's position in OLED materials faces distinct forces: concentrated suppliers, specialized buyers, high-tech rivalry and moderate threat from substitutes and entrants. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Scarce iridium and specialty precursors

Universal Display depends on scarce iridium and niche organic intermediates; global iridium mine supply is roughly 7–8 tonnes/year (2023–24) with most output concentrated in South Africa, creating supplier concentration risk. Scarcity and geopolitical stress can tighten availability and raise input costs. Long lead times (months) and >99.9% purity specs amplify supplier leverage. Hedging, strategic inventory and dual-sourcing mitigate but do not eliminate the risk.

Concentrated qualified toll manufacturers

Only a few contract manufacturers meet OLED emitter GMP-like quality and yield requirements, with qualification typically taking 6–24 months and creating switching frictions that favor suppliers; any disruption can ripple through deliveries and panel-maker ramps, delaying multi-month production ramps and inventory turns; long-term partnerships stabilize terms but embed supplier dependence for Universal Display’s materials and royalty-revenue growth.

Process IP and equipment lock-ins

Upstream synthesis routes and proprietary reactors/tooling for phosphorescent OLED emitters are highly specialized and not easily portable, and Universal Display’s process stickiness—backed by over 2,000 patents as of 2024—lets suppliers with unique know-how command higher pricing and tighter terms. Tech transfer often costs millions and carries yield and performance risk, raising supplier bargaining power during renegotiations.

Volume visibility yet batch complexity

While Universal Display offers multi-year demand visibility, emitter batches require tight spec adherence and carry rework/scrap risk; UDC reported 2024 revenue of $476.6M, underscoring scale but limited margin for defects. Suppliers often price complexity and scrap exposure into quotes, and UDC’s low defect tolerance weakens pure price-based leverage; incentives therefore tie to quality KPIs over blunt cost-downs.

- Supplier pricing: complexity & scrap built-in

- Leverage limited: low tolerance for defects

- Incentives: quality KPIs, not just cost-reductions

Counterweights via co-development

Universal Display uses joint R&D, shared QA systems, and multi-region capacity in 2024 to balance supplier power, with co-investment and selective exclusivity trading margin for supply security.

As blue emitter scale-ups progress in 2024, supplier leverage can re-emerge around novel precursor ecosystems, so strategic sourcing and diversified supplier pools remain mission-critical.

- Joint R&D

- Shared QA

- Multi-region capacity

- Co-investment vs margin

- New-emitter precursor risk

- Strategic sourcing

Scarce iridium 7–8 t/yr keeps suppliers' pricing power

Suppliers hold elevated leverage: global iridium supply ~7–8 t/yr (2023–24), purity >99.9% and niche intermediates create scarcity and switching frictions; CM qualification 6–24 months. UDC scale (2024 revenue $476.6M) and >2,000 patents reduce but do not remove supplier pricing power. Mitigants: joint R&D, multi-region capacity, KPIs over price.

| Metric | 2024 |

|---|---|

| Iridium supply | 7–8 t/yr |

| UDC revenue | $476.6M |

| Patents | >2,000 |

What is included in the product

Tailored Porter’s Five Forces analysis for Universal Display uncovering competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and strategic levers that affect its pricing, profitability, and market defensibility.

One-sheet Porter’s Five Forces for Universal Display simplifies competitive analysis—instantly visualize supplier, buyer, rivalry and entry pressures with a spider chart and customizable sliders for fast strategic decisions. Clean layout, no macros, and easy deck export make it a plug-and-play relief for busy analysts and executives.

Customers Bargaining Power

Highly concentrated panel customers

Samsung Display, LG Display, BOE and a few others account for a large share of Universal Display’s revenue, creating concentrated panel-customer risk and giving buyers leverage on price and contract terms. Loss of any major account would materially reduce UDC volumes and royalties. UDC mitigates this through differentiated IP, extensive patents and performance gains from PHOLED materials, which support longer-term bargaining power parity.

High switching costs and long qualifications

Emitter swaps demand extensive reliability testing and product requalification, often taking 6–12 months, with line tuning that can add 3–6 months of time-to-market delay. The tangible fail risk and launch penalties reduce buyer willingness to switch suppliers and temper aggressive price demands. Tightly coupled performance roadmaps aligned to device launches further anchor long-term OEM relationships.

License plus materials bundling

UDC blends IP licensing with phosphorescent OLED materials, intertwining legal and technical dependencies that give licensees limited optionality to source cheaper inputs; as of 2024 UDC holds over 6,000 issued and pending patents that underpin this leverage. Large manufacturers regularly demand carve-outs, rebates or tiered pricing, and contract renewals—often tied to volume thresholds and royalty terms—are frequent bargaining flashpoints.

Buyers’ internal R&D alternatives

Leading OLED makers including Samsung Display and LG Display have accelerated in-house emitter/host R&D, leveraging parent R&D budgets (Samsung Electronics R&D >$20B in 2024) to create credible walk-away options; visible progress on blue emitters strengthens buyer negotiating leverage, and even non-adoption forces pricing pressure, so UDC must outpace competitors on lifetime and EQE to defend royalties and ASPs.

- Buyers investing in internal emitters raise switching threat

- 2024 Samsung R&D scale (> $20B) deepens credibility

- Blue-emitter advances amplify bargaining power

- UDC needs superior lifetime and efficiency to retain pricing

Spec-driven performance premiums

Flagship phones, TVs and wearables prize OLED efficiency and lifetime, supporting spec-driven premiums; OLED accounted for about 60% of smartphone displays in 2024, so step-change UDC materials can temper buyer leverage. If incremental gains plateau, procurement pushes aggressive cost-downs; handset softness in 2024 (global smartphone shipments down ~3%) amplifies buyer power.

- Spec premiums justify price: OLED 60% smartphone share (2024)

- UDC breakthroughs reduce buyer leverage

- Plateau → intensified procurement

- Market cycles (shipments -3% 2024) favor buyers

Concentrated OEM demand boosts buyer pricing leverage amid patent moat and long qualification

Major customers (Samsung Display, LG Display, BOE) concentrate revenue, giving buyers pricing leverage; loss of an account would materially cut UDC volumes and royalties. Long qualification (6–18 months) plus UDC’s >6,000 patents and PHOLED performance limit switching, yet OEM in‑house R&D (Samsung R&D >20B in 2024) and blue‑emitter gains raise buyer leverage. OLED ~60% smartphone share (2024); shipments -3% in 2024 intensify procurement pressure.

| Metric | Value |

|---|---|

| UDC patents | >6,000 |

| Qualification time | 6–18 months |

| Samsung R&D (2024) | >$20B |

| OLED smartphone share (2024) | ~60% |

| Smartphone shipments 2024 | -3% |

Preview Before You Purchase

Universal Display Porter's Five Forces Analysis

This preview shows the exact Universal Display Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable.

A Must-Have Tool for Decision-Makers

Universal Display's position in OLED materials faces distinct forces: concentrated suppliers, specialized buyers, high-tech rivalry and moderate threat from substitutes and entrants. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Scarce iridium and specialty precursors

Universal Display depends on scarce iridium and niche organic intermediates; global iridium mine supply is roughly 7–8 tonnes/year (2023–24) with most output concentrated in South Africa, creating supplier concentration risk. Scarcity and geopolitical stress can tighten availability and raise input costs. Long lead times (months) and >99.9% purity specs amplify supplier leverage. Hedging, strategic inventory and dual-sourcing mitigate but do not eliminate the risk.

Concentrated qualified toll manufacturers

Only a few contract manufacturers meet OLED emitter GMP-like quality and yield requirements, with qualification typically taking 6–24 months and creating switching frictions that favor suppliers; any disruption can ripple through deliveries and panel-maker ramps, delaying multi-month production ramps and inventory turns; long-term partnerships stabilize terms but embed supplier dependence for Universal Display’s materials and royalty-revenue growth.

Process IP and equipment lock-ins

Upstream synthesis routes and proprietary reactors/tooling for phosphorescent OLED emitters are highly specialized and not easily portable, and Universal Display’s process stickiness—backed by over 2,000 patents as of 2024—lets suppliers with unique know-how command higher pricing and tighter terms. Tech transfer often costs millions and carries yield and performance risk, raising supplier bargaining power during renegotiations.

Volume visibility yet batch complexity

While Universal Display offers multi-year demand visibility, emitter batches require tight spec adherence and carry rework/scrap risk; UDC reported 2024 revenue of $476.6M, underscoring scale but limited margin for defects. Suppliers often price complexity and scrap exposure into quotes, and UDC’s low defect tolerance weakens pure price-based leverage; incentives therefore tie to quality KPIs over blunt cost-downs.

- Supplier pricing: complexity & scrap built-in

- Leverage limited: low tolerance for defects

- Incentives: quality KPIs, not just cost-reductions

Counterweights via co-development

Universal Display uses joint R&D, shared QA systems, and multi-region capacity in 2024 to balance supplier power, with co-investment and selective exclusivity trading margin for supply security.

As blue emitter scale-ups progress in 2024, supplier leverage can re-emerge around novel precursor ecosystems, so strategic sourcing and diversified supplier pools remain mission-critical.

- Joint R&D

- Shared QA

- Multi-region capacity

- Co-investment vs margin

- New-emitter precursor risk

- Strategic sourcing

Scarce iridium 7–8 t/yr keeps suppliers' pricing power

Suppliers hold elevated leverage: global iridium supply ~7–8 t/yr (2023–24), purity >99.9% and niche intermediates create scarcity and switching frictions; CM qualification 6–24 months. UDC scale (2024 revenue $476.6M) and >2,000 patents reduce but do not remove supplier pricing power. Mitigants: joint R&D, multi-region capacity, KPIs over price.

| Metric | 2024 |

|---|---|

| Iridium supply | 7–8 t/yr |

| UDC revenue | $476.6M |

| Patents | >2,000 |

What is included in the product

Tailored Porter’s Five Forces analysis for Universal Display uncovering competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and strategic levers that affect its pricing, profitability, and market defensibility.

One-sheet Porter’s Five Forces for Universal Display simplifies competitive analysis—instantly visualize supplier, buyer, rivalry and entry pressures with a spider chart and customizable sliders for fast strategic decisions. Clean layout, no macros, and easy deck export make it a plug-and-play relief for busy analysts and executives.

Customers Bargaining Power

Highly concentrated panel customers

Samsung Display, LG Display, BOE and a few others account for a large share of Universal Display’s revenue, creating concentrated panel-customer risk and giving buyers leverage on price and contract terms. Loss of any major account would materially reduce UDC volumes and royalties. UDC mitigates this through differentiated IP, extensive patents and performance gains from PHOLED materials, which support longer-term bargaining power parity.

High switching costs and long qualifications

Emitter swaps demand extensive reliability testing and product requalification, often taking 6–12 months, with line tuning that can add 3–6 months of time-to-market delay. The tangible fail risk and launch penalties reduce buyer willingness to switch suppliers and temper aggressive price demands. Tightly coupled performance roadmaps aligned to device launches further anchor long-term OEM relationships.

License plus materials bundling

UDC blends IP licensing with phosphorescent OLED materials, intertwining legal and technical dependencies that give licensees limited optionality to source cheaper inputs; as of 2024 UDC holds over 6,000 issued and pending patents that underpin this leverage. Large manufacturers regularly demand carve-outs, rebates or tiered pricing, and contract renewals—often tied to volume thresholds and royalty terms—are frequent bargaining flashpoints.

Buyers’ internal R&D alternatives

Leading OLED makers including Samsung Display and LG Display have accelerated in-house emitter/host R&D, leveraging parent R&D budgets (Samsung Electronics R&D >$20B in 2024) to create credible walk-away options; visible progress on blue emitters strengthens buyer negotiating leverage, and even non-adoption forces pricing pressure, so UDC must outpace competitors on lifetime and EQE to defend royalties and ASPs.

- Buyers investing in internal emitters raise switching threat

- 2024 Samsung R&D scale (> $20B) deepens credibility

- Blue-emitter advances amplify bargaining power

- UDC needs superior lifetime and efficiency to retain pricing

Spec-driven performance premiums

Flagship phones, TVs and wearables prize OLED efficiency and lifetime, supporting spec-driven premiums; OLED accounted for about 60% of smartphone displays in 2024, so step-change UDC materials can temper buyer leverage. If incremental gains plateau, procurement pushes aggressive cost-downs; handset softness in 2024 (global smartphone shipments down ~3%) amplifies buyer power.

- Spec premiums justify price: OLED 60% smartphone share (2024)

- UDC breakthroughs reduce buyer leverage

- Plateau → intensified procurement

- Market cycles (shipments -3% 2024) favor buyers

Concentrated OEM demand boosts buyer pricing leverage amid patent moat and long qualification

Major customers (Samsung Display, LG Display, BOE) concentrate revenue, giving buyers pricing leverage; loss of an account would materially cut UDC volumes and royalties. Long qualification (6–18 months) plus UDC’s >6,000 patents and PHOLED performance limit switching, yet OEM in‑house R&D (Samsung R&D >20B in 2024) and blue‑emitter gains raise buyer leverage. OLED ~60% smartphone share (2024); shipments -3% in 2024 intensify procurement pressure.

| Metric | Value |

|---|---|

| UDC patents | >6,000 |

| Qualification time | 6–18 months |

| Samsung R&D (2024) | >$20B |

| OLED smartphone share (2024) | ~60% |

| Smartphone shipments 2024 | -3% |

Preview Before You Purchase

Universal Display Porter's Five Forces Analysis

This preview shows the exact Universal Display Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable.

Description

A Must-Have Tool for Decision-Makers

Universal Display's position in OLED materials faces distinct forces: concentrated suppliers, specialized buyers, high-tech rivalry and moderate threat from substitutes and entrants. This snapshot highlights key pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Scarce iridium and specialty precursors

Universal Display depends on scarce iridium and niche organic intermediates; global iridium mine supply is roughly 7–8 tonnes/year (2023–24) with most output concentrated in South Africa, creating supplier concentration risk. Scarcity and geopolitical stress can tighten availability and raise input costs. Long lead times (months) and >99.9% purity specs amplify supplier leverage. Hedging, strategic inventory and dual-sourcing mitigate but do not eliminate the risk.

Concentrated qualified toll manufacturers

Only a few contract manufacturers meet OLED emitter GMP-like quality and yield requirements, with qualification typically taking 6–24 months and creating switching frictions that favor suppliers; any disruption can ripple through deliveries and panel-maker ramps, delaying multi-month production ramps and inventory turns; long-term partnerships stabilize terms but embed supplier dependence for Universal Display’s materials and royalty-revenue growth.

Process IP and equipment lock-ins

Upstream synthesis routes and proprietary reactors/tooling for phosphorescent OLED emitters are highly specialized and not easily portable, and Universal Display’s process stickiness—backed by over 2,000 patents as of 2024—lets suppliers with unique know-how command higher pricing and tighter terms. Tech transfer often costs millions and carries yield and performance risk, raising supplier bargaining power during renegotiations.

Volume visibility yet batch complexity

While Universal Display offers multi-year demand visibility, emitter batches require tight spec adherence and carry rework/scrap risk; UDC reported 2024 revenue of $476.6M, underscoring scale but limited margin for defects. Suppliers often price complexity and scrap exposure into quotes, and UDC’s low defect tolerance weakens pure price-based leverage; incentives therefore tie to quality KPIs over blunt cost-downs.

- Supplier pricing: complexity & scrap built-in

- Leverage limited: low tolerance for defects

- Incentives: quality KPIs, not just cost-reductions

Counterweights via co-development

Universal Display uses joint R&D, shared QA systems, and multi-region capacity in 2024 to balance supplier power, with co-investment and selective exclusivity trading margin for supply security.

As blue emitter scale-ups progress in 2024, supplier leverage can re-emerge around novel precursor ecosystems, so strategic sourcing and diversified supplier pools remain mission-critical.

- Joint R&D

- Shared QA

- Multi-region capacity

- Co-investment vs margin

- New-emitter precursor risk

- Strategic sourcing

Scarce iridium 7–8 t/yr keeps suppliers' pricing power

Suppliers hold elevated leverage: global iridium supply ~7–8 t/yr (2023–24), purity >99.9% and niche intermediates create scarcity and switching frictions; CM qualification 6–24 months. UDC scale (2024 revenue $476.6M) and >2,000 patents reduce but do not remove supplier pricing power. Mitigants: joint R&D, multi-region capacity, KPIs over price.

| Metric | 2024 |

|---|---|

| Iridium supply | 7–8 t/yr |

| UDC revenue | $476.6M |

| Patents | >2,000 |

What is included in the product

Tailored Porter’s Five Forces analysis for Universal Display uncovering competitive intensity, supplier and buyer bargaining power, threat of substitutes and new entrants, and strategic levers that affect its pricing, profitability, and market defensibility.

One-sheet Porter’s Five Forces for Universal Display simplifies competitive analysis—instantly visualize supplier, buyer, rivalry and entry pressures with a spider chart and customizable sliders for fast strategic decisions. Clean layout, no macros, and easy deck export make it a plug-and-play relief for busy analysts and executives.

Customers Bargaining Power

Highly concentrated panel customers

Samsung Display, LG Display, BOE and a few others account for a large share of Universal Display’s revenue, creating concentrated panel-customer risk and giving buyers leverage on price and contract terms. Loss of any major account would materially reduce UDC volumes and royalties. UDC mitigates this through differentiated IP, extensive patents and performance gains from PHOLED materials, which support longer-term bargaining power parity.

High switching costs and long qualifications

Emitter swaps demand extensive reliability testing and product requalification, often taking 6–12 months, with line tuning that can add 3–6 months of time-to-market delay. The tangible fail risk and launch penalties reduce buyer willingness to switch suppliers and temper aggressive price demands. Tightly coupled performance roadmaps aligned to device launches further anchor long-term OEM relationships.

License plus materials bundling

UDC blends IP licensing with phosphorescent OLED materials, intertwining legal and technical dependencies that give licensees limited optionality to source cheaper inputs; as of 2024 UDC holds over 6,000 issued and pending patents that underpin this leverage. Large manufacturers regularly demand carve-outs, rebates or tiered pricing, and contract renewals—often tied to volume thresholds and royalty terms—are frequent bargaining flashpoints.

Buyers’ internal R&D alternatives

Leading OLED makers including Samsung Display and LG Display have accelerated in-house emitter/host R&D, leveraging parent R&D budgets (Samsung Electronics R&D >$20B in 2024) to create credible walk-away options; visible progress on blue emitters strengthens buyer negotiating leverage, and even non-adoption forces pricing pressure, so UDC must outpace competitors on lifetime and EQE to defend royalties and ASPs.

- Buyers investing in internal emitters raise switching threat

- 2024 Samsung R&D scale (> $20B) deepens credibility

- Blue-emitter advances amplify bargaining power

- UDC needs superior lifetime and efficiency to retain pricing

Spec-driven performance premiums

Flagship phones, TVs and wearables prize OLED efficiency and lifetime, supporting spec-driven premiums; OLED accounted for about 60% of smartphone displays in 2024, so step-change UDC materials can temper buyer leverage. If incremental gains plateau, procurement pushes aggressive cost-downs; handset softness in 2024 (global smartphone shipments down ~3%) amplifies buyer power.

- Spec premiums justify price: OLED 60% smartphone share (2024)

- UDC breakthroughs reduce buyer leverage

- Plateau → intensified procurement

- Market cycles (shipments -3% 2024) favor buyers

Concentrated OEM demand boosts buyer pricing leverage amid patent moat and long qualification

Major customers (Samsung Display, LG Display, BOE) concentrate revenue, giving buyers pricing leverage; loss of an account would materially cut UDC volumes and royalties. Long qualification (6–18 months) plus UDC’s >6,000 patents and PHOLED performance limit switching, yet OEM in‑house R&D (Samsung R&D >20B in 2024) and blue‑emitter gains raise buyer leverage. OLED ~60% smartphone share (2024); shipments -3% in 2024 intensify procurement pressure.

| Metric | Value |

|---|---|

| UDC patents | >6,000 |

| Qualification time | 6–18 months |

| Samsung R&D (2024) | >$20B |

| OLED smartphone share (2024) | ~60% |

| Smartphone shipments 2024 | -3% |

Preview Before You Purchase

Universal Display Porter's Five Forces Analysis

This preview shows the exact Universal Display Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is fully formatted, professionally written, and ready for download and use the moment you buy. You're looking at the actual deliverable.