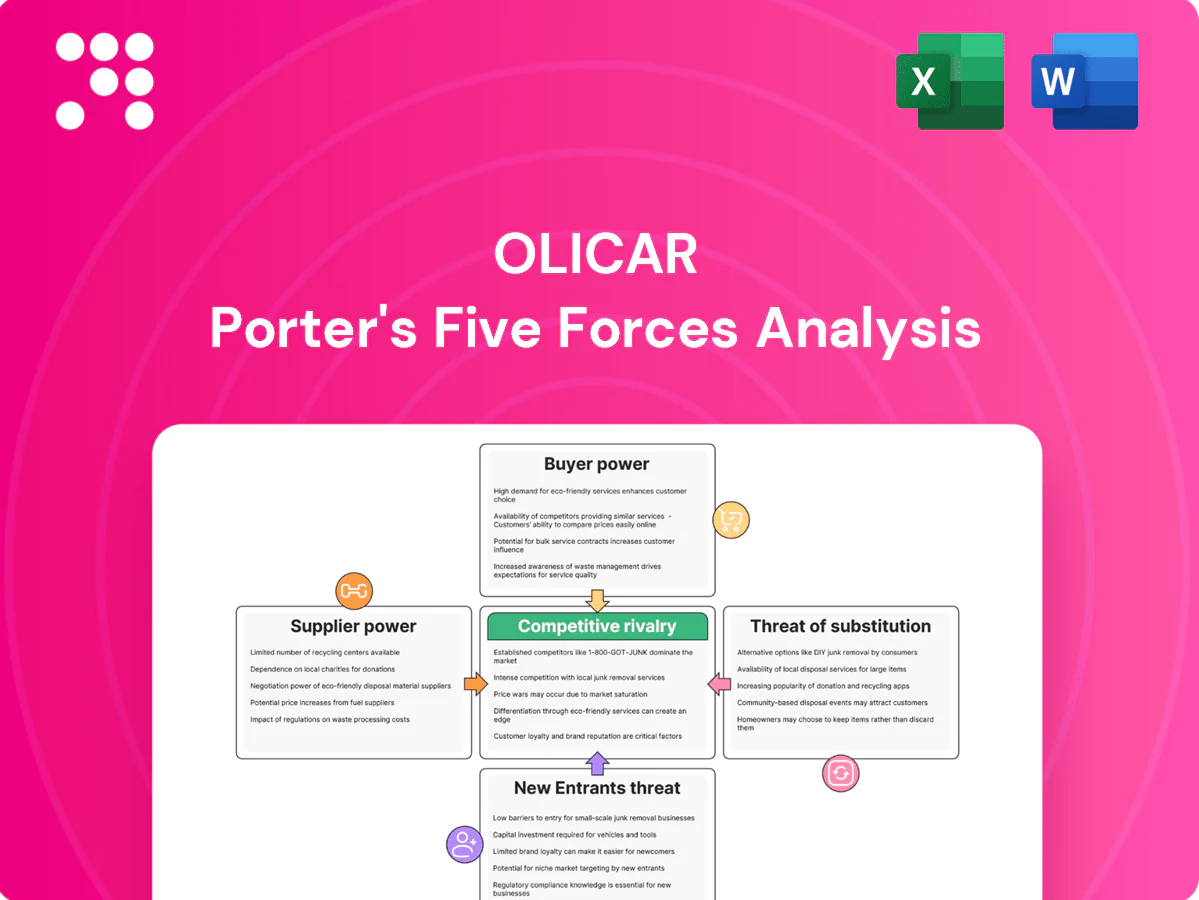

Olicar Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Olicar faces varied competitive pressures—from supplier leverage and buyer demands to substitution risks and potential new entrants—shaping margins and growth prospects. Our snapshot highlights key tensions and strategic levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to access detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

OEM concentration in compressors & chillers

Core equipment for compressed air, nitrogen generation, chillers and vacuum is dominated by a few global OEMs that together hold over 50% of respective equipment markets, increasing supplier leverage. Preferred access to spare parts, firmware and warranty servicing is often gated through authorized channels, constraining aftermarket margins. This raises pressure on equipment resale and lifecycle service contract profitability; diversifying approved vendors and building multi-brand capability mitigates concentration risk.

Specialized parts and consumables

Filters, valves, desiccants, membranes, oils and refrigerants are often proprietary, creating supplier leverage; lead times commonly run 4–12 weeks in 2024 and minimum order quantities drive higher working capital. Dependency rises because price pass-through is limited in fixed-price maintenance contracts, squeezing margins. Standardizing SKUs and strategic inventory builds have reduced stockouts and cut SKU counts in pilot programs by around 30%, lowering exposure.

Technical lock-in and software controls

Modern Olicar systems embed vendor-licensed controls and diagnostics that 68% of operators reported in 2024 restrict third-party access, constraining optimization and remote monitoring. These access limits materially raise switching costs by locking in service, parts and recurring license fees. Negotiating open-protocol access and API connectivity reduces supplier leverage and can cut integration costs and downtime by a material margin.

Energy and refrigerant regulatory shifts

Refrigerant phase-downs under the Kigali Amendment (up to 85% reduction for HFCs by 2047) and tighter 2023–24 efficiency rules have reshaped supplier portfolios and pricing, concentrating power among certified low-GWP refrigerant and high-efficiency equipment suppliers. Compliance-driven retrofits raise supplier leverage during transition cycles, while supply volatility has disrupted project costing and maintenance schedules. Early procurement alignment on future-proof refrigerants and efficiency classes reduces renegotiation risk and cost overruns.

- Phase-down: Kigali up to 85% by 2047

- Efficiency: 2023–24 rules raised minimums ~10%

- Supplier leverage rises during transition/refit waves

- Early alignment cuts renegotiation and schedule risk

Service partnerships and certification requirements

Service partnerships for food and beverage standards demand certified components and documentation; suppliers with ISO or EHEDG certification commanded premiums of about 5–15% in 2023–24 industry reports. Auditable traceability increases reliance on those certified supply chains, while dual-sourcing certified lines preserves pricing leverage and resilience.

- ISO/EHEDG premiums 5–15% (2023–24)

- Traceability raises supplier reliance

- Dual-sourcing sustains leverage

Supply squeeze: OEMs >50% share, 68% vendor lock, lead times 4–12 weeks

Supplier power is high: core OEMs hold >50% market share, lead times 4–12 weeks and 68% of operators report vendor-locked controls in 2024, raising switching costs and recurring fees. Kigali phase-down (up to 85% by 2047) and 2023–24 efficiency rules concentrate certified suppliers, with ISO/EHEDG premiums 5–15%.

| Metric | 2024 value |

|---|---|

| OEM concentration | >50% |

| Lead times | 4–12 weeks |

| Vendor lock | 68% |

| ISO/EHEDG premium | 5–15% |

What is included in the product

Tailored Porter’s Five Forces analysis for Olicar that uncovers competitive drivers, supplier and buyer influence, substitute threats, and entry barriers, with strategic commentary on disruptive risks and actionable insights for investor decks, business plans, or internal strategy documents.

Olicar's Porter's Five Forces one-sheet quickly highlights competitive pressures to ease strategic decision-making, with adjustable inputs and an instant radar visualization so teams can model scenarios and act without technical headaches.

Customers Bargaining Power

Industrial buyers are price-savvy

Industrial buyers now benchmark capex and opex across multiple integrators, with over 50% of procurement teams in 2024 reporting multi-vendor TCO comparisons. Transparent TCO models and lifecycle cost analyses compress equipment and maintenance margins. Buyers increasingly demand performance guarantees and uptime SLAs, and verified energy savings plus proven ROI are cited in 2024 as key levers sellers use to defend pricing.

Large accounts and centralized procurement

Enterprise buyers consolidate spend and run competitive tenders, with 2024 surveys showing >60% of large accounts favor centralized procurement to drive scale. Framework agreements often push discounts of 10–25% and lengthen payment terms toward 60–90 days, squeezing unit margins despite attractive volumes. Tiered pricing tied to multi-year service scopes can offset concessions by preserving blended margins over contract life.

Switching costs vary by integration depth

For turnkey systems embedded in production lines switching costs are high, with replacement often representing 30–50% of plant capex and downtime risks of days to weeks. For standalone chillers or compressors buyers can multi-source maintenance, cutting service spend by up to 30–40%. Documentation ownership and digital twins shift negotiating leverage—2024 surveys report 38% of buyers view digital twins as decisive. Proprietary performance baselines have cut churn ~25% in 2024 pilots.

Compliance and audit leverage

Food and beverage clients demand strict air quality and hygiene documentation under regimes like FSMA and standards such as HACCP, BRCGS and ISO 22000; non-compliance can trigger recalls or corrective actions that often cost companies millions. That enforcement threat gives buyers leverage to demand remedial work or penalties, while a proven compliance history—audit-ready reports and certifications—reduces buyer risk and weakens their bargaining stance.

- FSMA, HACCP, BRCGS, ISO 22000

- Non-compliance can trigger recalls costing millions

- Audit-ready reports preserve contract value

Demand cyclicality and budget timing

Demand cyclicality and budget timing raise buyer power as CAPEX freezes in downturns increase price sensitivity while OPEX reliability remains critical; peak seasons force expedited deliveries and higher service expectations, driving short-term leverage. Flexible financing and rental penetration (equipment rental market ~88B in 2023) shift power back to providers, and proactive maintenance plans reduce emergency discounts.

- CAPEX freezes → higher price sensitivity

- OPEX reliability → sustained demand

- Peak seasons → expedited service needs

- Financing/rental (≈88B 2023) → provider leverage

- Maintenance plans → fewer emergency discounts

Industrial buyers demand multi-vendor TCO, strict SLAs and digital-twin ROI—margins compress

Industrial buyers use multi-vendor TCO comparisons (50%+ in 2024), demanding SLAs and guaranteed ROI that compress margins.

Large accounts centralize procurement (>60% in 2024), extracting 10–25% discounts and extending payment terms to 60–90 days; tiered pricing can preserve blended margins.

Turnkey switches cost 30–50% of plant capex while multi-sourced O&M can cut service spend 30–40%; 38% cite digital twins as decisive in 2024.

| Metric | Year | Value |

|---|---|---|

| Multi-vendor TCO | 2024 | 50%+ |

| Centralized procurement | 2024 | >60% |

| Discounts | 2024 | 10–25% |

| Rental market | 2023 | $88B |

| Digital twins decisive | 2024 | 38% |

Same Document Delivered

Olicar Porter's Five Forces Analysis

This preview shows the exact Olicar Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted competitive assessment covering bargaining power of suppliers and buyers, threat of new entrants and substitutes, and industry rivalry. Once you buy, you’ll get instant access to this same ready-to-use document.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Olicar faces varied competitive pressures—from supplier leverage and buyer demands to substitution risks and potential new entrants—shaping margins and growth prospects. Our snapshot highlights key tensions and strategic levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to access detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

OEM concentration in compressors & chillers

Core equipment for compressed air, nitrogen generation, chillers and vacuum is dominated by a few global OEMs that together hold over 50% of respective equipment markets, increasing supplier leverage. Preferred access to spare parts, firmware and warranty servicing is often gated through authorized channels, constraining aftermarket margins. This raises pressure on equipment resale and lifecycle service contract profitability; diversifying approved vendors and building multi-brand capability mitigates concentration risk.

Specialized parts and consumables

Filters, valves, desiccants, membranes, oils and refrigerants are often proprietary, creating supplier leverage; lead times commonly run 4–12 weeks in 2024 and minimum order quantities drive higher working capital. Dependency rises because price pass-through is limited in fixed-price maintenance contracts, squeezing margins. Standardizing SKUs and strategic inventory builds have reduced stockouts and cut SKU counts in pilot programs by around 30%, lowering exposure.

Technical lock-in and software controls

Modern Olicar systems embed vendor-licensed controls and diagnostics that 68% of operators reported in 2024 restrict third-party access, constraining optimization and remote monitoring. These access limits materially raise switching costs by locking in service, parts and recurring license fees. Negotiating open-protocol access and API connectivity reduces supplier leverage and can cut integration costs and downtime by a material margin.

Energy and refrigerant regulatory shifts

Refrigerant phase-downs under the Kigali Amendment (up to 85% reduction for HFCs by 2047) and tighter 2023–24 efficiency rules have reshaped supplier portfolios and pricing, concentrating power among certified low-GWP refrigerant and high-efficiency equipment suppliers. Compliance-driven retrofits raise supplier leverage during transition cycles, while supply volatility has disrupted project costing and maintenance schedules. Early procurement alignment on future-proof refrigerants and efficiency classes reduces renegotiation risk and cost overruns.

- Phase-down: Kigali up to 85% by 2047

- Efficiency: 2023–24 rules raised minimums ~10%

- Supplier leverage rises during transition/refit waves

- Early alignment cuts renegotiation and schedule risk

Service partnerships and certification requirements

Service partnerships for food and beverage standards demand certified components and documentation; suppliers with ISO or EHEDG certification commanded premiums of about 5–15% in 2023–24 industry reports. Auditable traceability increases reliance on those certified supply chains, while dual-sourcing certified lines preserves pricing leverage and resilience.

- ISO/EHEDG premiums 5–15% (2023–24)

- Traceability raises supplier reliance

- Dual-sourcing sustains leverage

Supply squeeze: OEMs >50% share, 68% vendor lock, lead times 4–12 weeks

Supplier power is high: core OEMs hold >50% market share, lead times 4–12 weeks and 68% of operators report vendor-locked controls in 2024, raising switching costs and recurring fees. Kigali phase-down (up to 85% by 2047) and 2023–24 efficiency rules concentrate certified suppliers, with ISO/EHEDG premiums 5–15%.

| Metric | 2024 value |

|---|---|

| OEM concentration | >50% |

| Lead times | 4–12 weeks |

| Vendor lock | 68% |

| ISO/EHEDG premium | 5–15% |

What is included in the product

Tailored Porter’s Five Forces analysis for Olicar that uncovers competitive drivers, supplier and buyer influence, substitute threats, and entry barriers, with strategic commentary on disruptive risks and actionable insights for investor decks, business plans, or internal strategy documents.

Olicar's Porter's Five Forces one-sheet quickly highlights competitive pressures to ease strategic decision-making, with adjustable inputs and an instant radar visualization so teams can model scenarios and act without technical headaches.

Customers Bargaining Power

Industrial buyers are price-savvy

Industrial buyers now benchmark capex and opex across multiple integrators, with over 50% of procurement teams in 2024 reporting multi-vendor TCO comparisons. Transparent TCO models and lifecycle cost analyses compress equipment and maintenance margins. Buyers increasingly demand performance guarantees and uptime SLAs, and verified energy savings plus proven ROI are cited in 2024 as key levers sellers use to defend pricing.

Large accounts and centralized procurement

Enterprise buyers consolidate spend and run competitive tenders, with 2024 surveys showing >60% of large accounts favor centralized procurement to drive scale. Framework agreements often push discounts of 10–25% and lengthen payment terms toward 60–90 days, squeezing unit margins despite attractive volumes. Tiered pricing tied to multi-year service scopes can offset concessions by preserving blended margins over contract life.

Switching costs vary by integration depth

For turnkey systems embedded in production lines switching costs are high, with replacement often representing 30–50% of plant capex and downtime risks of days to weeks. For standalone chillers or compressors buyers can multi-source maintenance, cutting service spend by up to 30–40%. Documentation ownership and digital twins shift negotiating leverage—2024 surveys report 38% of buyers view digital twins as decisive. Proprietary performance baselines have cut churn ~25% in 2024 pilots.

Compliance and audit leverage

Food and beverage clients demand strict air quality and hygiene documentation under regimes like FSMA and standards such as HACCP, BRCGS and ISO 22000; non-compliance can trigger recalls or corrective actions that often cost companies millions. That enforcement threat gives buyers leverage to demand remedial work or penalties, while a proven compliance history—audit-ready reports and certifications—reduces buyer risk and weakens their bargaining stance.

- FSMA, HACCP, BRCGS, ISO 22000

- Non-compliance can trigger recalls costing millions

- Audit-ready reports preserve contract value

Demand cyclicality and budget timing

Demand cyclicality and budget timing raise buyer power as CAPEX freezes in downturns increase price sensitivity while OPEX reliability remains critical; peak seasons force expedited deliveries and higher service expectations, driving short-term leverage. Flexible financing and rental penetration (equipment rental market ~88B in 2023) shift power back to providers, and proactive maintenance plans reduce emergency discounts.

- CAPEX freezes → higher price sensitivity

- OPEX reliability → sustained demand

- Peak seasons → expedited service needs

- Financing/rental (≈88B 2023) → provider leverage

- Maintenance plans → fewer emergency discounts

Industrial buyers demand multi-vendor TCO, strict SLAs and digital-twin ROI—margins compress

Industrial buyers use multi-vendor TCO comparisons (50%+ in 2024), demanding SLAs and guaranteed ROI that compress margins.

Large accounts centralize procurement (>60% in 2024), extracting 10–25% discounts and extending payment terms to 60–90 days; tiered pricing can preserve blended margins.

Turnkey switches cost 30–50% of plant capex while multi-sourced O&M can cut service spend 30–40%; 38% cite digital twins as decisive in 2024.

| Metric | Year | Value |

|---|---|---|

| Multi-vendor TCO | 2024 | 50%+ |

| Centralized procurement | 2024 | >60% |

| Discounts | 2024 | 10–25% |

| Rental market | 2023 | $88B |

| Digital twins decisive | 2024 | 38% |

Same Document Delivered

Olicar Porter's Five Forces Analysis

This preview shows the exact Olicar Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted competitive assessment covering bargaining power of suppliers and buyers, threat of new entrants and substitutes, and industry rivalry. Once you buy, you’ll get instant access to this same ready-to-use document.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Olicar faces varied competitive pressures—from supplier leverage and buyer demands to substitution risks and potential new entrants—shaping margins and growth prospects. Our snapshot highlights key tensions and strategic levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to access detailed ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

OEM concentration in compressors & chillers

Core equipment for compressed air, nitrogen generation, chillers and vacuum is dominated by a few global OEMs that together hold over 50% of respective equipment markets, increasing supplier leverage. Preferred access to spare parts, firmware and warranty servicing is often gated through authorized channels, constraining aftermarket margins. This raises pressure on equipment resale and lifecycle service contract profitability; diversifying approved vendors and building multi-brand capability mitigates concentration risk.

Specialized parts and consumables

Filters, valves, desiccants, membranes, oils and refrigerants are often proprietary, creating supplier leverage; lead times commonly run 4–12 weeks in 2024 and minimum order quantities drive higher working capital. Dependency rises because price pass-through is limited in fixed-price maintenance contracts, squeezing margins. Standardizing SKUs and strategic inventory builds have reduced stockouts and cut SKU counts in pilot programs by around 30%, lowering exposure.

Technical lock-in and software controls

Modern Olicar systems embed vendor-licensed controls and diagnostics that 68% of operators reported in 2024 restrict third-party access, constraining optimization and remote monitoring. These access limits materially raise switching costs by locking in service, parts and recurring license fees. Negotiating open-protocol access and API connectivity reduces supplier leverage and can cut integration costs and downtime by a material margin.

Energy and refrigerant regulatory shifts

Refrigerant phase-downs under the Kigali Amendment (up to 85% reduction for HFCs by 2047) and tighter 2023–24 efficiency rules have reshaped supplier portfolios and pricing, concentrating power among certified low-GWP refrigerant and high-efficiency equipment suppliers. Compliance-driven retrofits raise supplier leverage during transition cycles, while supply volatility has disrupted project costing and maintenance schedules. Early procurement alignment on future-proof refrigerants and efficiency classes reduces renegotiation risk and cost overruns.

- Phase-down: Kigali up to 85% by 2047

- Efficiency: 2023–24 rules raised minimums ~10%

- Supplier leverage rises during transition/refit waves

- Early alignment cuts renegotiation and schedule risk

Service partnerships and certification requirements

Service partnerships for food and beverage standards demand certified components and documentation; suppliers with ISO or EHEDG certification commanded premiums of about 5–15% in 2023–24 industry reports. Auditable traceability increases reliance on those certified supply chains, while dual-sourcing certified lines preserves pricing leverage and resilience.

- ISO/EHEDG premiums 5–15% (2023–24)

- Traceability raises supplier reliance

- Dual-sourcing sustains leverage

Supply squeeze: OEMs >50% share, 68% vendor lock, lead times 4–12 weeks

Supplier power is high: core OEMs hold >50% market share, lead times 4–12 weeks and 68% of operators report vendor-locked controls in 2024, raising switching costs and recurring fees. Kigali phase-down (up to 85% by 2047) and 2023–24 efficiency rules concentrate certified suppliers, with ISO/EHEDG premiums 5–15%.

| Metric | 2024 value |

|---|---|

| OEM concentration | >50% |

| Lead times | 4–12 weeks |

| Vendor lock | 68% |

| ISO/EHEDG premium | 5–15% |

What is included in the product

Tailored Porter’s Five Forces analysis for Olicar that uncovers competitive drivers, supplier and buyer influence, substitute threats, and entry barriers, with strategic commentary on disruptive risks and actionable insights for investor decks, business plans, or internal strategy documents.

Olicar's Porter's Five Forces one-sheet quickly highlights competitive pressures to ease strategic decision-making, with adjustable inputs and an instant radar visualization so teams can model scenarios and act without technical headaches.

Customers Bargaining Power

Industrial buyers are price-savvy

Industrial buyers now benchmark capex and opex across multiple integrators, with over 50% of procurement teams in 2024 reporting multi-vendor TCO comparisons. Transparent TCO models and lifecycle cost analyses compress equipment and maintenance margins. Buyers increasingly demand performance guarantees and uptime SLAs, and verified energy savings plus proven ROI are cited in 2024 as key levers sellers use to defend pricing.

Large accounts and centralized procurement

Enterprise buyers consolidate spend and run competitive tenders, with 2024 surveys showing >60% of large accounts favor centralized procurement to drive scale. Framework agreements often push discounts of 10–25% and lengthen payment terms toward 60–90 days, squeezing unit margins despite attractive volumes. Tiered pricing tied to multi-year service scopes can offset concessions by preserving blended margins over contract life.

Switching costs vary by integration depth

For turnkey systems embedded in production lines switching costs are high, with replacement often representing 30–50% of plant capex and downtime risks of days to weeks. For standalone chillers or compressors buyers can multi-source maintenance, cutting service spend by up to 30–40%. Documentation ownership and digital twins shift negotiating leverage—2024 surveys report 38% of buyers view digital twins as decisive. Proprietary performance baselines have cut churn ~25% in 2024 pilots.

Compliance and audit leverage

Food and beverage clients demand strict air quality and hygiene documentation under regimes like FSMA and standards such as HACCP, BRCGS and ISO 22000; non-compliance can trigger recalls or corrective actions that often cost companies millions. That enforcement threat gives buyers leverage to demand remedial work or penalties, while a proven compliance history—audit-ready reports and certifications—reduces buyer risk and weakens their bargaining stance.

- FSMA, HACCP, BRCGS, ISO 22000

- Non-compliance can trigger recalls costing millions

- Audit-ready reports preserve contract value

Demand cyclicality and budget timing

Demand cyclicality and budget timing raise buyer power as CAPEX freezes in downturns increase price sensitivity while OPEX reliability remains critical; peak seasons force expedited deliveries and higher service expectations, driving short-term leverage. Flexible financing and rental penetration (equipment rental market ~88B in 2023) shift power back to providers, and proactive maintenance plans reduce emergency discounts.

- CAPEX freezes → higher price sensitivity

- OPEX reliability → sustained demand

- Peak seasons → expedited service needs

- Financing/rental (≈88B 2023) → provider leverage

- Maintenance plans → fewer emergency discounts

Industrial buyers demand multi-vendor TCO, strict SLAs and digital-twin ROI—margins compress

Industrial buyers use multi-vendor TCO comparisons (50%+ in 2024), demanding SLAs and guaranteed ROI that compress margins.

Large accounts centralize procurement (>60% in 2024), extracting 10–25% discounts and extending payment terms to 60–90 days; tiered pricing can preserve blended margins.

Turnkey switches cost 30–50% of plant capex while multi-sourced O&M can cut service spend 30–40%; 38% cite digital twins as decisive in 2024.

| Metric | Year | Value |

|---|---|---|

| Multi-vendor TCO | 2024 | 50%+ |

| Centralized procurement | 2024 | >60% |

| Discounts | 2024 | 10–25% |

| Rental market | 2023 | $88B |

| Digital twins decisive | 2024 | 38% |

Same Document Delivered

Olicar Porter's Five Forces Analysis

This preview shows the exact Olicar Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted competitive assessment covering bargaining power of suppliers and buyers, threat of new entrants and substitutes, and industry rivalry. Once you buy, you’ll get instant access to this same ready-to-use document.