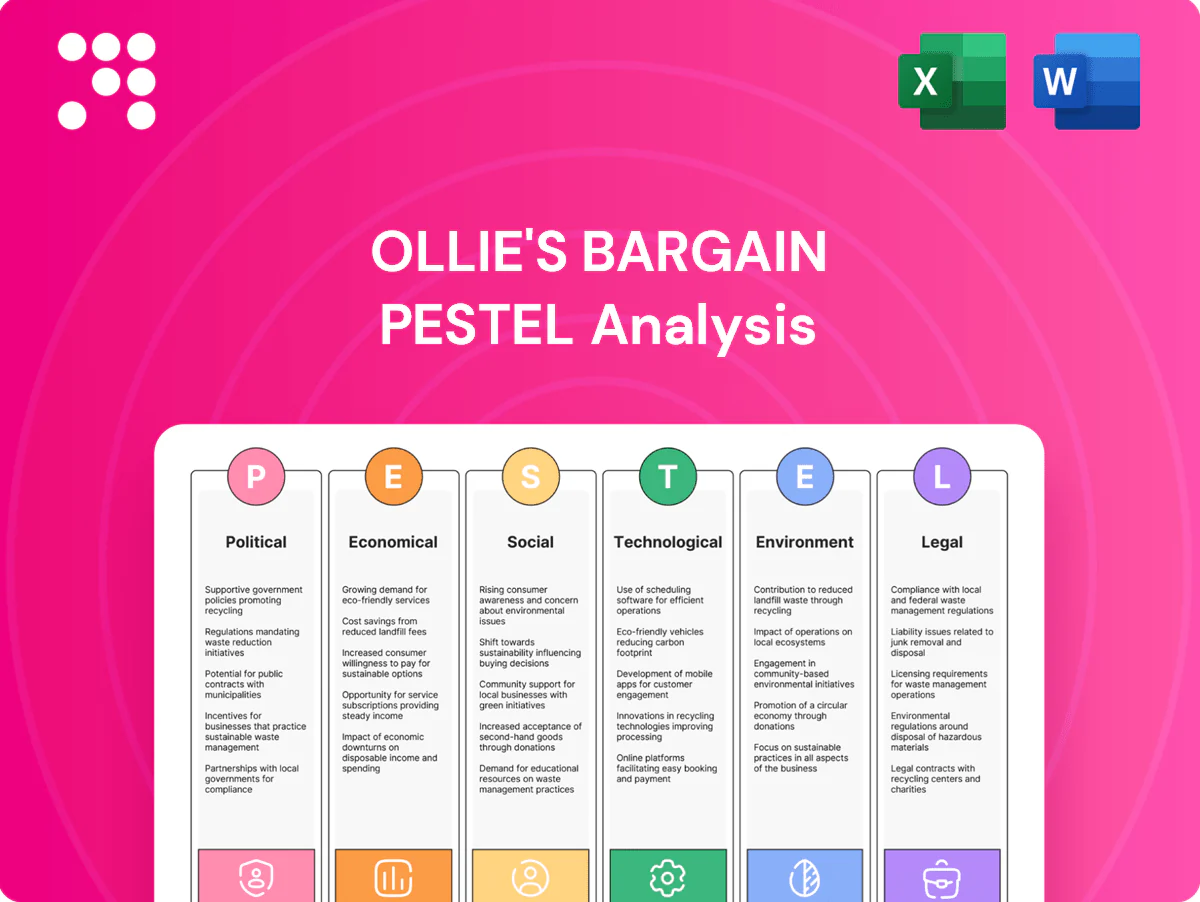

Ollie's Bargain PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Get strategic advantage with our PESTLE Analysis of Ollie's Bargain. Explore political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it's fully researched and ready to use. Purchase the full report now for actionable, exportable insights.

Political factors

Trade policy & tariffs

Import tariffs—including ongoing Section 301 duties affecting roughly $370 billion of Chinese goods—add roughly 7.5–25% to landed costs, squeezing Ollie’s closeout margins and forcing higher consumer prices or lower markdowns. Shifts in U.S.-China trade dynamics can reduce assortment availability and swing category margins by several percentage points. Favorable deals like USMCA and tariff suspensions widen low-cost sourcing options, while persistent uncertainty mandates flexible purchasing, diversified suppliers and hedging.

Regulatory oversight of discount retail

Ollie's Bargain Outlet (NASDAQ: OLLI) operates roughly 470 stores across the U.S. as of mid-2024, and local/state retail regulations directly affect store opening cadence and capitalized expansion costs. Zoning, permitting and community approvals commonly delay openings by 3–9 months, raising site development budgets. Pro-small-business political priorities can yield tax abatements or incentives, while policy shifts may either streamline or complicate approvals.

Infrastructure & logistics investment

Federal Infrastructure Investment and Jobs Act commits about 550 billion USD in new spending (2021) including roughly 17 billion USD for ports, lowering freight time and spoilage for mixed-lot inventories. US heavy/truck driver employment ~1.86 million (May 2023), so political support for FMCSA hours-of-service and rest rules directly shifts delivery schedules. Congestion pricing (eg NYC ~1 billion USD/year projected) and tolls raise regional distribution costs, while stable infrastructure funding improves network reliability.

Food assistance & consumer subsidies

Geopolitical supply disruptions

- Impact: irregular closeout supply, margin pressure

- Data point: container rates spike ~350% (2020–21)

- Mitigation: supplier/regional diversification

- Action: scenario planning for opportunistic buys

Tariffs cut margins 7.5-25%; freight strain meets SNAP demand

Tariffs (Section 301 on ~$370B Chinese goods) lift landed costs ~7.5–25%, squeezing margins and forcing flexible sourcing. Ollie’s ~470 stores (mid‑2024) face 3–9 month zoning delays and variable local incentives. Infrastructure spend (~$550B; ~$17B ports) and truck labor (~1.86M drivers) affect freight reliability and costs. SNAP (~41.9M FY2023) expansions boost value-retailer demand.

| Impact | Data | Action |

|---|---|---|

| Tariff pressure | ~7.5–25%; $370B | Diversify suppliers |

| Logistics | $17B ports; 1.86M drivers | Hedge freight |

| Demand | SNAP 41.9M | Shift consumables |

What is included in the product

Explores how macro-environmental factors uniquely affect Ollie’s Bargain across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks and opportunities.

A concise, visually segmented PESTLE summary of Ollie's Bargain that streamlines external risk assessment for meetings and presentations and can be dropped into slides or shared across teams; editable notes per region or business line let users tailor insights for faster decision-making.

Economic factors

Consumer price sensitivity

High inflation—peaking at 9.1% in June 2022 and moderating to about 3.4% in 2024—has pushed shoppers toward extreme-value channels, strengthening Ollie’s value proposition as price gaps with traditional retail widen. If deflation or aggressive competitor promotions occur, traffic and pricing power can compress quickly. Price elasticity varies by category and season, with staple and seasonal buys showing higher sensitivity.

Macro cycles & recession risk

Recession-driven liquidations historically expand closeout supply, often producing double-digit markdowns and boosting merchandise flow to off-price channels; Ollie’s benefited from elevated closeout inflows during 2020–2021 and remains positioned to source discounted freight in downturns.

Value retail typically sees resilient or rising foot traffic in recessions, with off-price retailers reporting stable same-store sales versus full-price peers; as recoveries lift sell-through, closeout availability tightens and margins normalize.

Ollie’s inventory discipline—lean replenishment in upcycles and opportunistic buys in downturns—helps balance abundance in recessions with scarcity in expansions, preserving gross margin flexibility.

Freight & fuel costs

Rising diesel (US on‑highway average ~3.88 USD/gal in July 2025, EIA) and ocean spot rates (Drewry WCI ~1,300 USD per 40ft June 2025) directly lift delivered costs and compress Ollie’s gross margin. Volatile spot rates force flexible routing, a mix of long‑term contracts and spot buys to stabilize landed costs. Aggressive backhauls and load optimization preserve unit economics, while DC proximity to stores reduces fuel exposure.

Labor availability & wage trends

Tight labor markets (US unemployment ~3.7% mid‑2024) have raised Ollie’s store and DC payrolls, though productivity tools and scheduling optimization can offset higher wages; economic slowdowns ease hiring but may lift retail shrink (≈1.8% of sales in 2023), while retention programs help stabilize operations during peak flows.

- Payroll pressure: higher hourly costs

- Offsets: automation, optimized scheduling

- Risk: slower economy reduces hiring but increases shrink

- Mitigation: retention programs for peak staffing

Interest rates & capital access

With the US federal funds rate at roughly 5.25–5.50% in mid‑2025, higher rates elevate lease, build‑out and inventory carry costs, slowing new‑store ROI and DC expansion, while lower rates support faster payback; strong access to working capital enables opportunistic bulk buys; rate volatility requires dynamic hurdle rates and phased pacing.

- Fed funds ~5.25–5.50% (mid‑2025)

- Higher rates ⇒ higher carry/financing costs

- Lower rates ⇒ faster store/DC ROI

- Volatility ⇒ dynamic hurdle rates & pacing

Tariffs cut margins 7.5-25%; freight strain meets SNAP demand

Sustained post‑2022 inflation (CPI ~3.4% in 2024) pushed shoppers to off‑price, boosting Ollie’s traffic and pricing power; tight closeout flows in recoveries can compress margins. Higher freight (diesel ~3.88 USD/gal Jul‑2025; Drewry WCI ~1,300 USD/40ft Jun‑2025) and Fed funds ~5.25–5.50% mid‑2025 raise carry costs; tight labor (U.S. ~3.7% mid‑2024) pressures payroll.

| Metric | Value |

|---|---|

| CPI 2024 | 3.4% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| Diesel (Jul‑2025) | $3.88/gal |

| Drewry WCI (Jun‑2025) | $1,300/40ft |

| Unemployment (mid‑2024) | 3.7% |

| Shrink (2023) | ≈1.8% |

Preview Before You Purchase

Ollie's Bargain PESTLE Analysis

The preview shown is the exact Ollie's Bargain PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. This screenshot reflects the real, final file with complete content and professional structure. No placeholders or teasers; you’ll download this same document immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Get strategic advantage with our PESTLE Analysis of Ollie's Bargain. Explore political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it's fully researched and ready to use. Purchase the full report now for actionable, exportable insights.

Political factors

Trade policy & tariffs

Import tariffs—including ongoing Section 301 duties affecting roughly $370 billion of Chinese goods—add roughly 7.5–25% to landed costs, squeezing Ollie’s closeout margins and forcing higher consumer prices or lower markdowns. Shifts in U.S.-China trade dynamics can reduce assortment availability and swing category margins by several percentage points. Favorable deals like USMCA and tariff suspensions widen low-cost sourcing options, while persistent uncertainty mandates flexible purchasing, diversified suppliers and hedging.

Regulatory oversight of discount retail

Ollie's Bargain Outlet (NASDAQ: OLLI) operates roughly 470 stores across the U.S. as of mid-2024, and local/state retail regulations directly affect store opening cadence and capitalized expansion costs. Zoning, permitting and community approvals commonly delay openings by 3–9 months, raising site development budgets. Pro-small-business political priorities can yield tax abatements or incentives, while policy shifts may either streamline or complicate approvals.

Infrastructure & logistics investment

Federal Infrastructure Investment and Jobs Act commits about 550 billion USD in new spending (2021) including roughly 17 billion USD for ports, lowering freight time and spoilage for mixed-lot inventories. US heavy/truck driver employment ~1.86 million (May 2023), so political support for FMCSA hours-of-service and rest rules directly shifts delivery schedules. Congestion pricing (eg NYC ~1 billion USD/year projected) and tolls raise regional distribution costs, while stable infrastructure funding improves network reliability.

Food assistance & consumer subsidies

Geopolitical supply disruptions

- Impact: irregular closeout supply, margin pressure

- Data point: container rates spike ~350% (2020–21)

- Mitigation: supplier/regional diversification

- Action: scenario planning for opportunistic buys

Tariffs cut margins 7.5-25%; freight strain meets SNAP demand

Tariffs (Section 301 on ~$370B Chinese goods) lift landed costs ~7.5–25%, squeezing margins and forcing flexible sourcing. Ollie’s ~470 stores (mid‑2024) face 3–9 month zoning delays and variable local incentives. Infrastructure spend (~$550B; ~$17B ports) and truck labor (~1.86M drivers) affect freight reliability and costs. SNAP (~41.9M FY2023) expansions boost value-retailer demand.

| Impact | Data | Action |

|---|---|---|

| Tariff pressure | ~7.5–25%; $370B | Diversify suppliers |

| Logistics | $17B ports; 1.86M drivers | Hedge freight |

| Demand | SNAP 41.9M | Shift consumables |

What is included in the product

Explores how macro-environmental factors uniquely affect Ollie’s Bargain across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks and opportunities.

A concise, visually segmented PESTLE summary of Ollie's Bargain that streamlines external risk assessment for meetings and presentations and can be dropped into slides or shared across teams; editable notes per region or business line let users tailor insights for faster decision-making.

Economic factors

Consumer price sensitivity

High inflation—peaking at 9.1% in June 2022 and moderating to about 3.4% in 2024—has pushed shoppers toward extreme-value channels, strengthening Ollie’s value proposition as price gaps with traditional retail widen. If deflation or aggressive competitor promotions occur, traffic and pricing power can compress quickly. Price elasticity varies by category and season, with staple and seasonal buys showing higher sensitivity.

Macro cycles & recession risk

Recession-driven liquidations historically expand closeout supply, often producing double-digit markdowns and boosting merchandise flow to off-price channels; Ollie’s benefited from elevated closeout inflows during 2020–2021 and remains positioned to source discounted freight in downturns.

Value retail typically sees resilient or rising foot traffic in recessions, with off-price retailers reporting stable same-store sales versus full-price peers; as recoveries lift sell-through, closeout availability tightens and margins normalize.

Ollie’s inventory discipline—lean replenishment in upcycles and opportunistic buys in downturns—helps balance abundance in recessions with scarcity in expansions, preserving gross margin flexibility.

Freight & fuel costs

Rising diesel (US on‑highway average ~3.88 USD/gal in July 2025, EIA) and ocean spot rates (Drewry WCI ~1,300 USD per 40ft June 2025) directly lift delivered costs and compress Ollie’s gross margin. Volatile spot rates force flexible routing, a mix of long‑term contracts and spot buys to stabilize landed costs. Aggressive backhauls and load optimization preserve unit economics, while DC proximity to stores reduces fuel exposure.

Labor availability & wage trends

Tight labor markets (US unemployment ~3.7% mid‑2024) have raised Ollie’s store and DC payrolls, though productivity tools and scheduling optimization can offset higher wages; economic slowdowns ease hiring but may lift retail shrink (≈1.8% of sales in 2023), while retention programs help stabilize operations during peak flows.

- Payroll pressure: higher hourly costs

- Offsets: automation, optimized scheduling

- Risk: slower economy reduces hiring but increases shrink

- Mitigation: retention programs for peak staffing

Interest rates & capital access

With the US federal funds rate at roughly 5.25–5.50% in mid‑2025, higher rates elevate lease, build‑out and inventory carry costs, slowing new‑store ROI and DC expansion, while lower rates support faster payback; strong access to working capital enables opportunistic bulk buys; rate volatility requires dynamic hurdle rates and phased pacing.

- Fed funds ~5.25–5.50% (mid‑2025)

- Higher rates ⇒ higher carry/financing costs

- Lower rates ⇒ faster store/DC ROI

- Volatility ⇒ dynamic hurdle rates & pacing

Tariffs cut margins 7.5-25%; freight strain meets SNAP demand

Sustained post‑2022 inflation (CPI ~3.4% in 2024) pushed shoppers to off‑price, boosting Ollie’s traffic and pricing power; tight closeout flows in recoveries can compress margins. Higher freight (diesel ~3.88 USD/gal Jul‑2025; Drewry WCI ~1,300 USD/40ft Jun‑2025) and Fed funds ~5.25–5.50% mid‑2025 raise carry costs; tight labor (U.S. ~3.7% mid‑2024) pressures payroll.

| Metric | Value |

|---|---|

| CPI 2024 | 3.4% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| Diesel (Jul‑2025) | $3.88/gal |

| Drewry WCI (Jun‑2025) | $1,300/40ft |

| Unemployment (mid‑2024) | 3.7% |

| Shrink (2023) | ≈1.8% |

Preview Before You Purchase

Ollie's Bargain PESTLE Analysis

The preview shown is the exact Ollie's Bargain PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. This screenshot reflects the real, final file with complete content and professional structure. No placeholders or teasers; you’ll download this same document immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Get strategic advantage with our PESTLE Analysis of Ollie's Bargain. Explore political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, it's fully researched and ready to use. Purchase the full report now for actionable, exportable insights.

Political factors

Trade policy & tariffs

Import tariffs—including ongoing Section 301 duties affecting roughly $370 billion of Chinese goods—add roughly 7.5–25% to landed costs, squeezing Ollie’s closeout margins and forcing higher consumer prices or lower markdowns. Shifts in U.S.-China trade dynamics can reduce assortment availability and swing category margins by several percentage points. Favorable deals like USMCA and tariff suspensions widen low-cost sourcing options, while persistent uncertainty mandates flexible purchasing, diversified suppliers and hedging.

Regulatory oversight of discount retail

Ollie's Bargain Outlet (NASDAQ: OLLI) operates roughly 470 stores across the U.S. as of mid-2024, and local/state retail regulations directly affect store opening cadence and capitalized expansion costs. Zoning, permitting and community approvals commonly delay openings by 3–9 months, raising site development budgets. Pro-small-business political priorities can yield tax abatements or incentives, while policy shifts may either streamline or complicate approvals.

Infrastructure & logistics investment

Federal Infrastructure Investment and Jobs Act commits about 550 billion USD in new spending (2021) including roughly 17 billion USD for ports, lowering freight time and spoilage for mixed-lot inventories. US heavy/truck driver employment ~1.86 million (May 2023), so political support for FMCSA hours-of-service and rest rules directly shifts delivery schedules. Congestion pricing (eg NYC ~1 billion USD/year projected) and tolls raise regional distribution costs, while stable infrastructure funding improves network reliability.

Food assistance & consumer subsidies

Geopolitical supply disruptions

- Impact: irregular closeout supply, margin pressure

- Data point: container rates spike ~350% (2020–21)

- Mitigation: supplier/regional diversification

- Action: scenario planning for opportunistic buys

Tariffs cut margins 7.5-25%; freight strain meets SNAP demand

Tariffs (Section 301 on ~$370B Chinese goods) lift landed costs ~7.5–25%, squeezing margins and forcing flexible sourcing. Ollie’s ~470 stores (mid‑2024) face 3–9 month zoning delays and variable local incentives. Infrastructure spend (~$550B; ~$17B ports) and truck labor (~1.86M drivers) affect freight reliability and costs. SNAP (~41.9M FY2023) expansions boost value-retailer demand.

| Impact | Data | Action |

|---|---|---|

| Tariff pressure | ~7.5–25%; $370B | Diversify suppliers |

| Logistics | $17B ports; 1.86M drivers | Hedge freight |

| Demand | SNAP 41.9M | Shift consumables |

What is included in the product

Explores how macro-environmental factors uniquely affect Ollie’s Bargain across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives and investors identify risks and opportunities.

A concise, visually segmented PESTLE summary of Ollie's Bargain that streamlines external risk assessment for meetings and presentations and can be dropped into slides or shared across teams; editable notes per region or business line let users tailor insights for faster decision-making.

Economic factors

Consumer price sensitivity

High inflation—peaking at 9.1% in June 2022 and moderating to about 3.4% in 2024—has pushed shoppers toward extreme-value channels, strengthening Ollie’s value proposition as price gaps with traditional retail widen. If deflation or aggressive competitor promotions occur, traffic and pricing power can compress quickly. Price elasticity varies by category and season, with staple and seasonal buys showing higher sensitivity.

Macro cycles & recession risk

Recession-driven liquidations historically expand closeout supply, often producing double-digit markdowns and boosting merchandise flow to off-price channels; Ollie’s benefited from elevated closeout inflows during 2020–2021 and remains positioned to source discounted freight in downturns.

Value retail typically sees resilient or rising foot traffic in recessions, with off-price retailers reporting stable same-store sales versus full-price peers; as recoveries lift sell-through, closeout availability tightens and margins normalize.

Ollie’s inventory discipline—lean replenishment in upcycles and opportunistic buys in downturns—helps balance abundance in recessions with scarcity in expansions, preserving gross margin flexibility.

Freight & fuel costs

Rising diesel (US on‑highway average ~3.88 USD/gal in July 2025, EIA) and ocean spot rates (Drewry WCI ~1,300 USD per 40ft June 2025) directly lift delivered costs and compress Ollie’s gross margin. Volatile spot rates force flexible routing, a mix of long‑term contracts and spot buys to stabilize landed costs. Aggressive backhauls and load optimization preserve unit economics, while DC proximity to stores reduces fuel exposure.

Labor availability & wage trends

Tight labor markets (US unemployment ~3.7% mid‑2024) have raised Ollie’s store and DC payrolls, though productivity tools and scheduling optimization can offset higher wages; economic slowdowns ease hiring but may lift retail shrink (≈1.8% of sales in 2023), while retention programs help stabilize operations during peak flows.

- Payroll pressure: higher hourly costs

- Offsets: automation, optimized scheduling

- Risk: slower economy reduces hiring but increases shrink

- Mitigation: retention programs for peak staffing

Interest rates & capital access

With the US federal funds rate at roughly 5.25–5.50% in mid‑2025, higher rates elevate lease, build‑out and inventory carry costs, slowing new‑store ROI and DC expansion, while lower rates support faster payback; strong access to working capital enables opportunistic bulk buys; rate volatility requires dynamic hurdle rates and phased pacing.

- Fed funds ~5.25–5.50% (mid‑2025)

- Higher rates ⇒ higher carry/financing costs

- Lower rates ⇒ faster store/DC ROI

- Volatility ⇒ dynamic hurdle rates & pacing

Tariffs cut margins 7.5-25%; freight strain meets SNAP demand

Sustained post‑2022 inflation (CPI ~3.4% in 2024) pushed shoppers to off‑price, boosting Ollie’s traffic and pricing power; tight closeout flows in recoveries can compress margins. Higher freight (diesel ~3.88 USD/gal Jul‑2025; Drewry WCI ~1,300 USD/40ft Jun‑2025) and Fed funds ~5.25–5.50% mid‑2025 raise carry costs; tight labor (U.S. ~3.7% mid‑2024) pressures payroll.

| Metric | Value |

|---|---|

| CPI 2024 | 3.4% |

| Fed funds (mid‑2025) | 5.25–5.50% |

| Diesel (Jul‑2025) | $3.88/gal |

| Drewry WCI (Jun‑2025) | $1,300/40ft |

| Unemployment (mid‑2024) | 3.7% |

| Shrink (2023) | ≈1.8% |

Preview Before You Purchase

Ollie's Bargain PESTLE Analysis

The preview shown is the exact Ollie's Bargain PESTLE Analysis you'll receive after purchase—fully formatted and ready to use. This screenshot reflects the real, final file with complete content and professional structure. No placeholders or teasers; you’ll download this same document immediately after checkout.